Report Overview

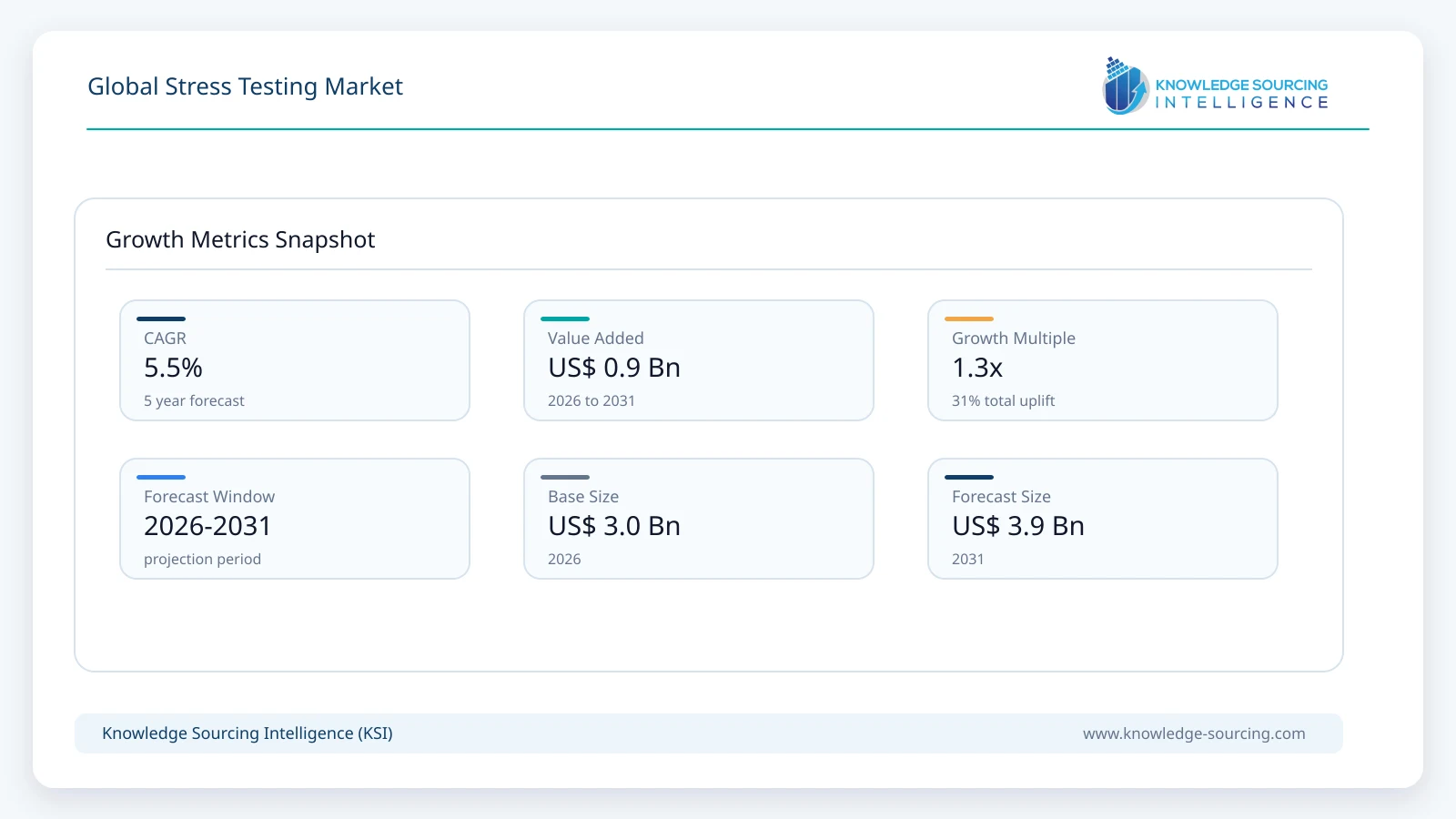

The Global Stress Testing Market is forecast to grow at a CAGR of 5.5%, reaching USD 3.88 billion in 2031 from USD 2.97 billion in 2026.

Highlights:

- 1Aging populations are increasing cardiac screening volumes because cardiovascular disease prevalence rises significantly across patients above 60 years of age.

- 2Hospitals are adopting integrated stress testing platforms because fragmented cardiovascular workflows increase reporting delays and clinician workload.

- 3Demand for stress echocardiography systems is rising because providers require radiation-free diagnostic pathways for repeated cardiac assessment.

- 4Outpatient cardiac centers are expanding stress ECG installations because healthcare systems are attempting to reduce tertiary hospital congestion.

The stress testing market exists within the broader cardiovascular diagnostics ecosystem where clinical decision-making depends on early identification of ischemic heart disease, arrhythmias, exercise intolerance, and cardiac dysfunction. Coronary artery disease remains a primary demand generator because healthcare systems continue prioritizing non-invasive risk stratification methods that reduce invasive catheterization dependency. Diagnostic demand is increasing across outpatient cardiology networks because aging populations are generating larger volumes of chronic cardiovascular monitoring requirements.

Healthcare providers are adopting advanced stress imaging systems because reimbursement structures increasingly reward earlier disease detection and reduced hospitalization rates. Nuclear imaging systems and stress echocardiography platforms remain strategically important because physicians require higher diagnostic specificity for complex cardiovascular cases. Cardiopulmonary exercise testing systems are also gaining adoption since pulmonary-cardiac overlap conditions are becoming more clinically relevant in aging and post-acute care populations.

Regulatory agencies continue strengthening cardiovascular diagnostic quality requirements because inaccurate interpretation increases treatment delays and unnecessary interventions. Healthcare systems therefore depend on integrated diagnostic platforms that improve workflow consistency, reporting accuracy, and data interoperability. This dependency is encouraging long-term investment in connected cardiovascular diagnostic infrastructure rather than standalone testing equipment procurement.

Market Dynamics

Market Drivers

Rising Cardiovascular Disease Burden: Cardiovascular disease remains the primary structural demand driver because healthcare systems require scalable diagnostic pathways for earlier intervention. Patient volumes are increasing across cardiology departments because sedentary lifestyles, diabetes prevalence, obesity, and hypertension continue to elevate long-term cardiac risk exposure. Healthcare providers are expanding non-invasive stress testing capacity since delayed cardiovascular diagnosis increases hospitalization frequency and treatment costs. Diagnostic device procurement, therefore, remains closely linked to national cardiovascular disease management priorities.

Expansion of Outpatient Cardiology Infrastructure: Outpatient cardiovascular diagnostics reduce inpatient dependency because healthcare systems seek lower-cost disease management models. Independent diagnostic centers and ambulatory cardiac clinics are increasing procurement of compact stress ECG and imaging systems because patient preference is shifting toward shorter diagnostic turnaround times. Manufacturers are responding through portable and workflow-optimized platforms that support decentralized testing environments. The market consequently reflects rising demand for flexible diagnostic systems with lower infrastructure requirements.

Integration of Digital Cardiology Platforms: Cardiology departments depend on integrated data management because disconnected reporting systems increase interpretation variability and workflow inefficiency. Demand is shifting toward digitally connected stress testing platforms because healthcare providers are attempting to centralize cardiovascular data access across multiple facilities. Companies are embedding AI-assisted interpretation, cloud storage, and remote review functionality into stress testing ecosystems. Diagnostic platforms, therefore, increasingly compete through interoperability and workflow intelligence rather than hardware capability alone.

Growth in Preventive Cardiac Screening: Preventive healthcare strategies reduce long-term treatment expenditure because early cardiovascular intervention lowers acute cardiac event incidence. Employers, insurers, and preventive health programs are increasing cardiovascular screening initiatives since chronic disease management costs continue rising globally. Stress testing utilization is expanding across asymptomatic high-risk populations because clinicians require scalable tools for exercise tolerance evaluation and ischemic risk assessment. Preventive screening therefore strengthens recurring diagnostic testing demand.

Market Restraints

High installation and maintenance costs limit adoption because advanced nuclear imaging and stress echocardiography systems require specialized infrastructure and trained personnel.

Diagnostic variability persists because interpretation accuracy depends heavily on clinician expertise and imaging quality consistency.

Reimbursement limitations constrain testing expansion because several healthcare systems continue restricting coverage for preventive cardiac diagnostics.

Market Opportunities

AI-Enabled Cardiac Interpretation Systems: Cardiology departments require faster reporting because patient volumes continue increasing while specialist availability remains constrained. AI-assisted interpretation tools are improving workflow standardization through automated ECG analysis and imaging support capabilities. Healthcare providers are adopting intelligent diagnostic systems because consistent interpretation reduces repeat testing rates. AI integration, therefore, creates expansion opportunities across both hospital and outpatient cardiovascular diagnostics.

Expansion of Home-Based Cardiac Monitoring: Remote cardiovascular monitoring supports chronic disease management because healthcare systems increasingly prioritize decentralized care delivery. Portable stress assessment and connected ECG platforms are entering long-term cardiac monitoring pathways since patients require continuous disease surveillance outside hospital settings. Technology providers are developing wearable-compatible cardiac diagnostics because the telecardiology infrastructure continues expanding. Home-based diagnostics, therefore, represent a long-term market expansion opportunity.

Emerging Market Healthcare Infrastructure Investments: Developing healthcare systems are expanding cardiovascular diagnostic capacity because non-communicable disease burdens continue rising across urban populations. Governments are increasing investment in tertiary care hospitals and diagnostic imaging infrastructure since cardiovascular disease management has become a public health priority. Manufacturers are entering cost-sensitive markets through modular and scalable stress testing systems. Emerging economies, therefore, represent significant future installation potential.

Multi-Modality Cardiac Imaging Demand: Complex cardiovascular conditions require integrated diagnostic assessment because single-modality testing often limits clinical certainty. Hospitals are adopting hybrid imaging strategies that combine nuclear imaging, stress echocardiography, and ECG monitoring because precision diagnostics reduce downstream intervention risks. Manufacturers are expanding software interoperability across diagnostic platforms to support integrated cardiac evaluation pathways. Multi-modality diagnostics therefore continue strengthening high-value procurement demand, benefits from broader application expansion beyond cardiovascular imaging.

Supply Chain Analysis

The stress testing market depends on a multi-tiered supply chain involving semiconductor suppliers, imaging component manufacturers, electrode and sensor producers, software developers, and hospital distribution partners. Imaging-intensive systems require specialized detector technologies and high-performance computing infrastructure because cardiac imaging interpretation depends on real-time processing accuracy. Semiconductor shortages and electronic component supply instability continue affecting production timelines because cardiovascular diagnostic systems increasingly incorporate advanced digital processing architecture.

Manufacturers are regionalizing portions of their supply chains because geopolitical uncertainty and transportation disruptions increase procurement risk exposure. Healthcare providers are demanding longer equipment lifecycle support because diagnostic system replacement costs remain high across public healthcare systems. Companies are strengthening service-based business models through long-term maintenance contracts and software subscription ecosystems. The market therefore increasingly values supply reliability and technical support infrastructure alongside hardware performance.

Government Regulations

Region | Regulation/ Authority | Market Impact |

United States | U.S. Food and Drug Administration (FDA) | Increases clinical evidence requirements for stress testing systems. |

Europe | European Commission | Strengthens post-market surveillance obligations |

China | National Medical Products Administration | Encourages domestic manufacturing partnerships |

Market Segmentation

By Product Type

Stress ECG systems maintain broad adoption because hospitals and outpatient clinics require cost-efficient cardiovascular screening infrastructure. Demand is increasing for stress echocardiography systems because clinicians prefer radiation-free diagnostic pathways for repeated cardiac evaluation. Nuclear imaging systems remain important in complex ischemic assessment because physicians require higher diagnostic specificity for advanced coronary disease cases. Cardiopulmonary exercise testing systems are gaining relevance because integrated pulmonary-cardiac assessment demand continues expanding across chronic disease management programs. Product competition, therefore, increasingly centers on interoperability, workflow efficiency, and diagnostic precision.

By Test Type

Exercise stress testing remains the foundational diagnostic approach because physical exertion-based assessment provides scalable cardiovascular risk evaluation. Pharmacological stress testing demand is increasing because elderly and mobility-limited patients require alternative cardiac assessment methods. Nuclear stress testing continues expanding within tertiary hospitals because complex cardiac imaging cases require higher sensitivity and functional visualization capabilities. Healthcare providers are adopting differentiated testing approaches because patient populations increasingly present with multiple chronic comorbidities that complicate standard diagnostic pathways.

By Indication

Coronary artery disease represents the largest demand segment because ischemic heart disease remains the dominant cardiovascular burden globally. Heart failure diagnostics are expanding because aging populations continue increasing chronic cardiac management requirements. Cardiac arrhythmia evaluation demand is rising because wearable monitoring technologies are improving arrhythmia detection rates across outpatient populations. Congenital heart disease testing remains clinically important because long-term survival improvements are increasing adult congenital cardiac monitoring needs. Diagnostic demand therefore increasingly reflects chronic disease continuity rather than episodic acute care dependence.

Regional Analysis

North America Market Analysis

North America maintains a dominant position in the stress testing market because cardiovascular disease prevalence continues generating sustained diagnostic demand across hospital and outpatient settings. The United States healthcare system supports extensive cardiac diagnostic infrastructure because reimbursement mechanisms favor early disease detection and preventive cardiovascular management. Hospitals are increasing investment in AI-enabled diagnostic ecosystems because clinician shortages and rising cardiac patient volumes are pressuring workflow efficiency. Cardiology networks are consolidating diagnostic operations since integrated cardiovascular reporting reduces duplicate testing and interpretation variability.

Outpatient cardiac centers are expanding across suburban healthcare markets because patients increasingly prefer lower-cost and faster-access diagnostic environments. Stress echocardiography and nuclear imaging demand remain strong because tertiary care hospitals continue managing high volumes of complex ischemic heart disease cases. Digital cardiology adoption is accelerating because healthcare providers require centralized patient monitoring across multisite networks. Remote cardiac monitoring solutions are also gaining adoption because insurers and healthcare systems are attempting to reduce avoidable cardiac admissions.

Europe Market Analysis

Europe sustains strong stress testing demand because aging populations continue increasing cardiovascular disease management requirements across public healthcare systems. Universal healthcare frameworks prioritize preventive cardiac assessment because long-term hospitalization reduction remains a central cost containment objective. Hospitals are modernizing cardiovascular imaging infrastructure since older diagnostic systems limit workflow efficiency and interoperability. Demand is increasingly shifting toward integrated stress echocardiography and digital ECG platforms because healthcare providers require scalable diagnostics within constrained reimbursement environments.

Western European countries continue investing in advanced cardiac imaging because tertiary care systems manage rising volumes of chronic coronary artery disease and heart failure cases. Eastern European healthcare systems are expanding cardiovascular diagnostic accessibility because non-communicable disease burdens continue rising across aging urban populations. Portable and lower-cost stress ECG systems are gaining traction because regional healthcare providers require scalable deployment across decentralized hospital networks.

Asia Pacific Market Analysis

Asia Pacific represents the fastest structural expansion environment because cardiovascular disease prevalence is increasing alongside rapid urbanization, sedentary lifestyles, and aging demographics. China and India are expanding tertiary healthcare infrastructure because governments are attempting to manage rising chronic disease burdens through earlier diagnosis and intervention. Hospitals are increasing procurement of stress ECG and imaging systems since cardiovascular screening demand continues rising across middle-income populations.

Japan maintains advanced diagnostic adoption because its aging population generates sustained long-term cardiac monitoring requirements. Southeast Asian healthcare systems are expanding cardiovascular diagnostics because economic growth is improving healthcare accessibility and insurance penetration. Demand is shifting toward cost-efficient and scalable diagnostic systems because public hospitals continue operating under infrastructure and staffing constraints.

Rest of the World

The Rest of the World region reflects uneven but expanding stress testing demand because cardiovascular disease burdens are increasing across Latin America, the Middle East, and parts of Africa. Urban healthcare systems are strengthening cardiac diagnostic infrastructure since non-communicable diseases continue replacing infectious diseases as primary healthcare burdens. Governments are investing in tertiary hospital expansion because cardiac disease management increasingly affects national healthcare expenditure.

Middle Eastern countries are adopting advanced cardiovascular imaging systems because healthcare diversification programs prioritize specialized medical infrastructure development. Latin American healthcare providers are increasing demand for stress ECG systems because public hospitals require scalable cardiovascular diagnostics within constrained budgets. African healthcare systems continue facing infrastructure limitations because specialist shortages and diagnostic funding gaps restrict broader imaging adoption.

Regulatory Landscape

Regulatory oversight within the stress testing market is strengthening because cardiovascular diagnostics directly influence high-risk clinical decision-making. Regulatory agencies require extensive clinical validation because inaccurate stress testing interpretation increases risks of delayed intervention or unnecessary invasive procedures. Manufacturers are investing heavily in software verification, cybersecurity compliance, and post-market surveillance systems because digital cardiology integration continues expanding.

Artificial intelligence integration is creating additional regulatory scrutiny because automated interpretation systems increasingly participate in clinical decision pathways. Authorities are developing updated frameworks for AI-enabled diagnostics since algorithm transparency and patient data integrity have become central compliance concerns. Companies are therefore restructuring product development processes around regulatory documentation and lifecycle monitoring capabilities.

Cross-border commercialization remains complex because medical device approval requirements differ substantially across regions. Manufacturers are regionalizing regulatory strategies because localized clinical evidence and compliance adaptation reduce market entry delays. Regulatory sophistication consequently functions as a competitive differentiator within the stress testing industry.

Pipeline Analysis

The stress testing market pipeline increasingly focuses on AI-assisted cardiovascular diagnostics because healthcare systems require faster and more scalable interpretation capabilities. Companies are developing cloud-connected stress ECG platforms since multisite healthcare networks depend on centralized cardiac data access. Portable diagnostic technologies are also entering development pipelines because decentralized cardiovascular monitoring demand continues increasing across outpatient and preventive care settings.

Imaging innovation remains concentrated around workflow efficiency and diagnostic precision because hospitals require improved throughput without compromising clinical accuracy. Advanced echocardiography software, automated image quantification systems, and integrated reporting tools are gaining strategic importance because specialist shortages continue affecting cardiology departments globally. Nuclear imaging optimization is also progressing because providers require lower-radiation diagnostic alternatives without reducing imaging sensitivity.

Digital cardiology convergence continues to reshape pipeline priorities because wearable devices, telecardiology platforms, and AI analytics increasingly operate within interconnected cardiovascular ecosystems. Manufacturers are therefore prioritizing interoperability and longitudinal patient monitoring rather than isolated diagnostic functionality.

Competitive Landscape

Philips

Philips differentiates itself through connected cardiovascular care platforms that integrate imaging, patient monitoring, and workflow analytics. The company is strengthening cloud-enabled cardiology solutions because multisite healthcare systems increasingly require centralized cardiovascular data access.

Siemens Healthineers

Siemens Healthineers sustains competitive strength through advanced imaging precision and integrated diagnostic infrastructure capabilities. The company is investing heavily in cardiovascular imaging optimization because complex coronary disease management requires higher diagnostic sensitivity and workflow consistency.

Fujifilm Holdings Corporation

Fujifilm Holdings Corporation leverages imaging expertise and digital healthcare integration to strengthen cardiovascular diagnostic positioning. The company is expanding software-enabled imaging workflows because healthcare systems require faster image accessibility and reporting efficiency.

Canon Medical Systems Corporation

Canon Medical Systems Corporation maintains competitive differentiation through advanced imaging, visualization, and precision diagnostic technologies. The company is strengthening cardiovascular imaging integration because hospitals increasingly require multi-modality cardiac assessment capabilities.

Nihon Kohden Corporation

Nihon Kohden Corporation focuses on patient monitoring and diagnostic reliability across cardiovascular care environments. The company is expanding stress ECG and cardiac monitoring integration because healthcare providers increasingly require continuous cardiovascular surveillance capabilities.

Schiller AG

Schiller AG differentiates itself through specialized cardiopulmonary diagnostics and exercise testing expertise. The company is strengthening cardiopulmonary exercise testing portfolios because integrated pulmonary-cardiac evaluation demand continues to increase in chronic disease management.

AliveCor

AliveCor remains strategically distinct because it focuses on mobile and AI-enabled cardiac diagnostics outside conventional hospital infrastructure. The company is expanding remote cardiovascular monitoring capabilities because preventive cardiac management and ambulatory care demand continue to increase.

Key Developments

April 2026: ESMA launched its sixth EU-wide stress test for central counterparties to assess resilience under adverse market scenarios. The exercise covers 16 CCPs and, for the first time, includes recovery and resolution impacts on financial stability.

June 2025: GE HealthCare reported new molecular imaging advances aimed at improving cardiac diagnostics, including better visualization of perfusion and ischemia. The update highlights how PET/CT and SPECT/CT tools can help clinicians detect disease earlier and assess heart function more precisely.

May 2025: The University of Cincinnati reported on a device that could help diagnose depression by analyzing heart-related signals. The approach points to a noninvasive screening method that may identify mental-health risk through physiological biomarkers.

Strategic Insights and Future Market Outlook

The stress testing market is transitioning toward digitally integrated cardiovascular diagnostics because healthcare systems increasingly prioritize continuous disease management over episodic intervention. Hospitals are restructuring cardiac care pathways around interoperable data ecosystems since fragmented diagnostics increase operational inefficiency and treatment delays. AI-enabled interpretation systems are therefore becoming strategically important because cardiology departments face rising patient volumes and specialist shortages simultaneously.

Outpatient and decentralized cardiac diagnostics are expanding because healthcare providers seek lower-cost disease management infrastructure with broader patient accessibility. Portable ECG systems, cloud-enabled imaging platforms, and remote monitoring technologies are increasing in relevance since chronic cardiovascular disease management increasingly occurs outside tertiary hospitals. Manufacturers are consequently repositioning product strategies around workflow integration, software intelligence, and recurring service ecosystems rather than standalone equipment sales.

Emerging economies continue to represent long-term growth potential because cardiovascular disease burdens are increasing faster than existing diagnostic infrastructure capacity. Companies capable of balancing affordability, regulatory adaptability, and digital integration are likely to strengthen competitive positioning across both mature and developing healthcare systems. The market, therefore, increasingly rewards operational flexibility and ecosystem integration capabilities.

The stress testing industry ultimately reflects broader structural changes within cardiovascular care, where earlier diagnosis, decentralized monitoring, and integrated digital workflows are reshaping healthcare delivery models. Diagnostic systems that improve accessibility, workflow efficiency, and longitudinal patient management remain central to future market evolution.

Global Stress Testing Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 2.97 billion |

| Total Market Size in 2031 | USD 3.88 billion |

| Forecast Unit | USD Billion |

| Growth Rate | 5.5% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Product Type, Test Type, Indication, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Geography

Key Countries Analysis

Regulatory & Policy Landscape

Table of Contents

1. Executive Summary

1.1 Market Overview

1.2 Key Findings

1.3 Executive Insights

1.4 Market Attractiveness Analysis

1.5 Snapshot of Technological Advancements

1.6 Key Strategic Recommendations

1.7 Future Growth Outlook

2. Disease & Epidemiology Analysis

2.1 Overview of Cardiovascular Diseases

2.2 Clinical Importance of Cardiac Stress Testing

2.3 Epidemiology of Coronary Artery Disease

2.3.1 Global Prevalence of Coronary Artery Disease

2.3.2 Incidence Trends

2.3.3 Mortality Trends Associated with Cardiovascular Disorders

2.4 Epidemiology of Cardiac Arrhythmias

2.5 Epidemiology of Heart Failure

2.6 Epidemiology of Ischemic Heart Disease

2.7 Risk Factor Analysis

2.7.1 Hypertension

2.7.2 Diabetes Mellitus

2.7.3 Obesity

2.7.4 Sedentary Lifestyle

2.7.5 Smoking and Tobacco Use

2.8 Aging Population Impact on Stress Testing Demand

2.9 Patient Population Eligible for Stress Testing

2.10 Diagnostic Rate and Screening Trends

2.11 Burden of Cardiovascular Diseases by Healthcare Setting

2.12 Epidemiology Forecast and Future Disease Burden

3. Market Dynamics

3.1 Market Overview

3.2 Market Drivers

3.2.1 Rising Burden of Cardiovascular Diseases

3.2.2 Increasing Adoption of Non-Invasive Diagnostics

3.2.3 Technological Advancements in Cardiac Imaging

3.2.4 Growth in Preventive Cardiology Programs

3.2.5 Expansion of Ambulatory Cardiac Care Centers

3.3 Market Restraints

3.3.1 High Cost of Advanced Imaging Systems

3.3.2 Limited Access in Low-Resource Settings

3.3.3 Radiation Exposure Concerns in Nuclear Stress Testing

3.3.4 Shortage of Skilled Cardiology Professionals

3.4 Market Opportunities

3.4.1 AI-Integrated Stress Testing Platforms

3.4.2 Portable and Wearable Cardiac Monitoring Solutions

3.4.3 Emerging Market Expansion

3.4.4 Telecardiology Integration

3.5 Market Challenges

3.5.1 Reimbursement Variability

3.5.2 Regulatory Compliance Complexity

3.5.3 Equipment Maintenance and Operational Costs

3.6 Porter’s Five Forces Analysis

3.7 PESTLE Analysis

3.8 Value Chain Analysis

3.9 Pricing Analysis

3.10 Technology Assessment

3.11 Impact of Digital Health and Artificial Intelligence

3.12 Impact of Healthcare Infrastructure Development

4. Commercial & Market Access

4.1 Commercial Landscape Overview

4.2 Reimbursement Framework Overview

4.2.1 Public Reimbursement Models

4.2.2 Private Insurance Coverage

4.3 Market Access Challenges

4.4 Procurement Trends in Hospitals and Diagnostic Centers

4.5 Healthcare Spending Analysis

4.6 Adoption Trends Across End Users

4.7 Role of Group Purchasing Organizations

4.8 Health Technology Assessment Trends

4.9 Coding and Billing Considerations

4.10 Commercialization Strategies Adopted by Market Players

5. Innovation & Pipeline Landscape

5.1 Overview of Innovation Ecosystem

5.2 Emerging Technologies in Stress Testing

5.2.1 AI-Assisted ECG Interpretation

5.2.2 Cloud-Based Cardiac Diagnostics

5.2.3 Wearable Cardiac Stress Monitoring Systems

5.2.4 Digital Stress Testing Platforms

5.3 Pipeline Diagnostic Technologies

5.3.1 Phase I Innovations

5.3.2 Phase II Innovations

5.3.3 Phase III Innovations

5.4 Mechanism of Technology Integration

5.5 Software and Algorithmic Advancements

5.6 Integration of Machine Learning in Cardiac Imaging

5.7 Patent Landscape Analysis

5.8 Clinical Trials Landscape

5.9 Collaborations, Partnerships, and Licensing Activities

5.10 Future Innovation Trends

6. Treatment Landscape

6.1 Role of Stress Testing in Cardiovascular Disease Management

6.2 Current Diagnostic Pathways

6.3 Stress Testing Modalities Overview

6.3.1 Exercise Stress Testing

6.3.2 Nuclear Stress Testing

6.3.3 Stress Echocardiography

6.3.4 Pharmacologic Stress Testing

6.3.5 Cardiopulmonary Exercise Testing

6.3.6 Cardiac Magnetic Resonance Stress Testing

6.4 Comparative Analysis of Stress Testing Modalities

6.5 Clinical Practice Guidelines Overview

6.5.1 American College of Cardiology Guidelines

6.5.2 European Society of Cardiology Guidelines

6.5.3 Asian Cardiology Society Recommendations

6.6 Patient Selection Criteria

6.7 Diagnostic Accuracy and Clinical Outcomes

6.8 Workflow Integration in Cardiology Departments

6.9 Future Trends in Diagnostic Cardiology

7. Global Stress Testing Market Size & Forecast

7.1 Global Market Overview

7.2 Historical Market Size Analysis (2021–2025)

7.3 Market Forecast Analysis (2026–2033)

7.4 Market Size by Product Type

7.5 Market Size by Test Type

7.6 Market Size by Indication

7.7 Market Size by End User

7.8 Market Size by Region

7.9 Absolute Dollar Opportunity Analysis

7.10 Incremental Growth Analysis

7.11 Market Share Analysis

7.12 Scenario-Based Forecast Analysis

8. Global Stress Testing Market Segmentation

8.1 By Product Type

8.1.1 Stress ECG Systems

8.1.2 Stress Echocardiography Systems

8.1.3 Nuclear Imaging Systems

8.1.4 Cardiopulmonary Exercise Testing Systems

8.1.5 Others

8.2 By Test Type

8.2.1 Exercise Stress Testing

8.2.2 Pharmacological Stress Testing

8.2.3 Nuclear Stress Testing

8.2.4 Others

8.3 By Indication

8.3.1 Coronary Artery Disease

8.3.2 Heart Failure

8.3.3 Cardiac Arrhythmias

8.3.4 Congenital Heart Disease

8.3.5 Others

8.4 By End User

8.4.1 Hospitals & Cardiology Clinics

8.4.2 Ambulatory Surgical Centers

8.4.3 Diagnostic Imaging Centers

8.4.5 Academic and Research Institutes

9. Geographical Analysis (Regional Level)

9.1 North America

9.1.1 Market Size and Forecast

9.1.2 Demand Drivers

9.1.3 Regional Regulatory Overview

9.1.4 Competitive Landscape

9.1.5 Technological Adoption Trends

9.2 Europe

9.2.1 Market Size and Forecast

9.2.2 Demand Drivers

9.2.3 Regional Regulatory Overview

9.2.4 Competitive Landscape

9.2.5 Technological Adoption Trends

9.3 Asia-Pacific

9.3.1 Market Size and Forecast

9.3.2 Demand Drivers

9.3.3 Regional Regulatory Overview

9.3.4 Competitive Landscape

9.3.5 Technological Adoption Trends

9.4 Latin America

9.4.1 Market Size and Forecast

9.4.2 Demand Drivers

9.4.3 Regional Regulatory Overview

9.4.4 Competitive Landscape

9.4.5 Technological Adoption Trends

9.5 Middle East & Africa

9.5.1 Market Size and Forecast

9.5.2 Demand Drivers

9.5.3 Regional Regulatory Overview

9.5.4 Competitive Landscape

9.5.5 Technological Adoption Trends

10. Key Countries Analysis

10.1 United States

10.1.1 Market Size and Forecast

10.1.2 Cardiovascular Disease Epidemiology

10.1.3 FDA Regulatory Framework

10.1.4 Reimbursement Environment

10.1.5 Presence of Key Companies and Products

10.2 Canada

10.2.1 Market Size and Forecast

10.2.2 Cardiovascular Disease Epidemiology

10.2.3 Regulatory Framework

10.2.4 Reimbursement Environment

10.2.5 Presence of Key Companies and Products

10.3 Germany

10.3.1 Market Size and Forecast

10.3.2 Cardiovascular Disease Epidemiology

10.3.3 MDR Regulatory Framework

10.3.4 Reimbursement Environment

10.3.5 Presence of Key Companies and Products

10.4 United Kingdom

10.4.1 Market Size and Forecast

10.4.2 Cardiovascular Disease Epidemiology

10.4.3 MHRA Regulatory Framework

10.4.4 Reimbursement Environment

10.4.5 Presence of Key Companies and Products

10.5 France

10.5.1 Market Size and Forecast

10.5.2 Cardiovascular Disease Epidemiology

10.5.3 Regulatory Framework

10.5.4 Reimbursement Environment

10.5.5 Presence of Key Companies and Products

10.6 Italy

10.6.1 Market Size and Forecast

10.6.2 Cardiovascular Disease Epidemiology

10.6.3 Regulatory Framework

10.6.4 Reimbursement Environment

10.6.5 Presence of Key Companies and Products

10.7 Spain

10.7.1 Market Size and Forecast

10.7.2 Cardiovascular Disease Epidemiology

10.7.3 Regulatory Framework

10.7.4 Reimbursement Environment

10.7.5 Presence of Key Companies and Products

10.8 China

10.8.1 Market Size and Forecast

10.8.2 Cardiovascular Disease Epidemiology

10.8.3 NMPA Regulatory Framework

10.8.4 Reimbursement Environment

10.8.5 Presence of Key Companies and Products

10.9 Japan

10.9.1 Market Size and Forecast

10.9.2 Cardiovascular Disease Epidemiology

10.9.3 PMDA Regulatory Framework

10.9.4 Reimbursement Environment

10.9.5 Presence of Key Companies and Products

10.10 India

10.10.1 Market Size and Forecast

10.10.2 Cardiovascular Disease Epidemiology

10.10.3 CDSCO Regulatory Framework

10.10.4 Reimbursement Environment

10.10.5 Presence of Key Companies and Products

10.11 South Korea

10.11.1 Market Size and Forecast

10.11.2 Cardiovascular Disease Epidemiology

10.11.3 MFDS Regulatory Framework

10.11.4 Reimbursement Environment

10.11.5 Presence of Key Companies and Products

10.12 Australia

10.12.1 Market Size and Forecast

10.12.2 Cardiovascular Disease Epidemiology

10.12.3 TGA Regulatory Framework

10.12.4 Reimbursement Environment

10.12.5 Presence of Key Companies and Products

10.13 Brazil

10.13.1 Market Size and Forecast

10.13.2 Cardiovascular Disease Epidemiology

10.13.3 ANVISA Regulatory Framework

10.13.4 Reimbursement Environment

10.13.5 Presence of Key Companies and Products

10.14 Mexico

10.14.1 Market Size and Forecast

10.14.2 Cardiovascular Disease Epidemiology

10.14.3 COFEPRIS Regulatory Framework

10.14.4 Reimbursement Environment

10.14.5 Presence of Key Companies and Products

10.15 Saudi Arabia

10.15.1 Market Size and Forecast

10.15.2 Cardiovascular Disease Epidemiology

10.15.3 SFDA Regulatory Framework

10.15.4 Reimbursement Environment

10.15.5 Presence of Key Companies and Products

10.16 South Africa

10.16.1 Market Size and Forecast

10.16.2 Cardiovascular Disease Epidemiology

10.16.3 SAHPRA Regulatory Framework

10.16.4 Reimbursement Environment

10.16.5 Presence of Key Companies and Products

11. Regulatory & Policy Landscape

11.1 Overview of Global Medical Device Regulations

11.2 United States Regulatory Framework (FDA)

11.3 Europe Regulatory Framework (EU MDR)

11.4 Japan Regulatory Framework (PMDA)

11.5 India Regulatory Framework (CDSCO)

11.6 China Regulatory Framework (NMPA)

11.7 Regulatory Approval Pathways for Cardiac Diagnostic Devices

11.8 Clinical Validation Requirements

11.9 Quality and Safety Standards

11.10 Data Privacy and Cybersecurity Regulations

11.11 Reimbursement and HTA Policies

11.12 Future Regulatory Trends

12. Competitive Landscape

12.1 Market Share Analysis

12.2 Competitive Benchmarking

12.3 Strategic Positioning of Key Players

12.4 Product Portfolio Analysis

12.5 Pricing and Technology Comparison

12.6 Recent Developments

12.6.1 Product Launches

12.6.2 Regulatory Approvals

12.6.3 Collaborations and Partnerships

12.6.4 Acquisitions and Mergers

12.7 SWOT Analysis

12.8 Strategic Recommendations for Market Participants

13. Company Profiles

13.1 GE HealthCare

13.1.1 Company Overview

13.1.2 Stress Testing Product Portfolio

13.1.3 Cardiac Diagnostic Solutions

13.1.4 Key Indications

13.1.5 Recent Developments

13.1.6 Pipeline and Innovation Focus

13.2 Philips

13.2.1 Company Overview

13.2.2 Stress Testing Product Portfolio

13.2.3 Cardiac Imaging Solutions

13.2.4 Key Indications

13.2.5 Recent Developments

13.2.6 Pipeline and Innovation Focus

13.3 Siemens Healthineers

13.3.1 Company Overview

13.3.2 Stress Testing Product Portfolio

13.3.3 Cardiology Imaging Systems

13.3.4 Key Indications

13.3.5 Recent Developments

13.3.6 Pipeline and Innovation Focus

13.4 Fujifilm Holdings Corporation

13.4.1 Company Overview

13.4.2 Cardiology Diagnostic Portfolio

13.4.3 Stress Echocardiography Solutions

13.4.4 Key Indications

13.4.5 Recent Developments

13.4.6 Pipeline and Innovation Focus

13.5 Canon Medical Systems Corporation

13.5.1 Company Overview

13.5.2 Cardiac Imaging Portfolio

13.5.3 Stress Testing Technologies

13.5.4 Key Indications

13.5.5 Recent Developments

13.5.6 Pipeline and Innovation Focus

13.6 Nihon Kohden Corporation

13.6.1 Company Overview

13.6.2 ECG and Stress Testing Systems

13.6.3 Cardiology Product Portfolio

13.6.4 Key Indications

13.6.5 Recent Developments

13.6.6 Pipeline and Innovation Focus

13.7 Schiller AG

13.7.1 Company Overview

13.7.2 Stress ECG Systems

13.7.3 Cardiopulmonary Exercise Testing Solutions

13.7.4 Key Indications

13.7.5 Recent Developments

13.7.6 Pipeline and Innovation Focus

13.8 Hillrom

13.8.1 Company Overview

13.8.2 Cardiology Diagnostic Solutions

13.8.3 Stress Testing and ECG Portfolio

13.8.4 Key Indications

13.8.5 Recent Developments

13.8.6 Pipeline and Innovation Focus

13.9 AliveCor

13.9.1 Company Overview

13.9.2 AI-Enabled Cardiac Diagnostic Products

13.9.3 Remote Cardiac Monitoring Solutions

13.9.4 Key Indications

13.9.5 Recent Developments

13.9.6 Pipeline and Innovation Focus

13.10 Cardiac Science Corporation

13.10.1 Company Overview

13.10.2 Stress Testing Systems

13.10.3 Cardiology Diagnostic Portfolio

13.10.4 Key Indications

13.10.5 Recent Developments

13.10.6 Pipeline and Innovation Focus

14. Future Outlook

14.1 Future Market Trends

14.2 AI and Digital Cardiology Transformation

14.3 Shift Toward Preventive Cardiovascular Diagnostics

14.4 Future of Remote and Ambulatory Stress Testing

14.5 Emerging Business Models

14.6 Investment and Funding Trends

14.7 Opportunities in Emerging Markets

14.8 Strategic Outlook for Stakeholders

14.9 Long-Term Market Forecast

15. Methodology

15.1 Research Methodology Overview

15.2 Secondary Research

15.3 Primary Research

15.4 Data Collection and Validation

15.5 Forecasting Methodology

15.6 Market Estimation Models

15.7 Assumptions and Limitations

15.8 Abbreviations and Definitions

15.9 Sources and References

Navigate

Trusted by the world's leading organizations