Report Overview

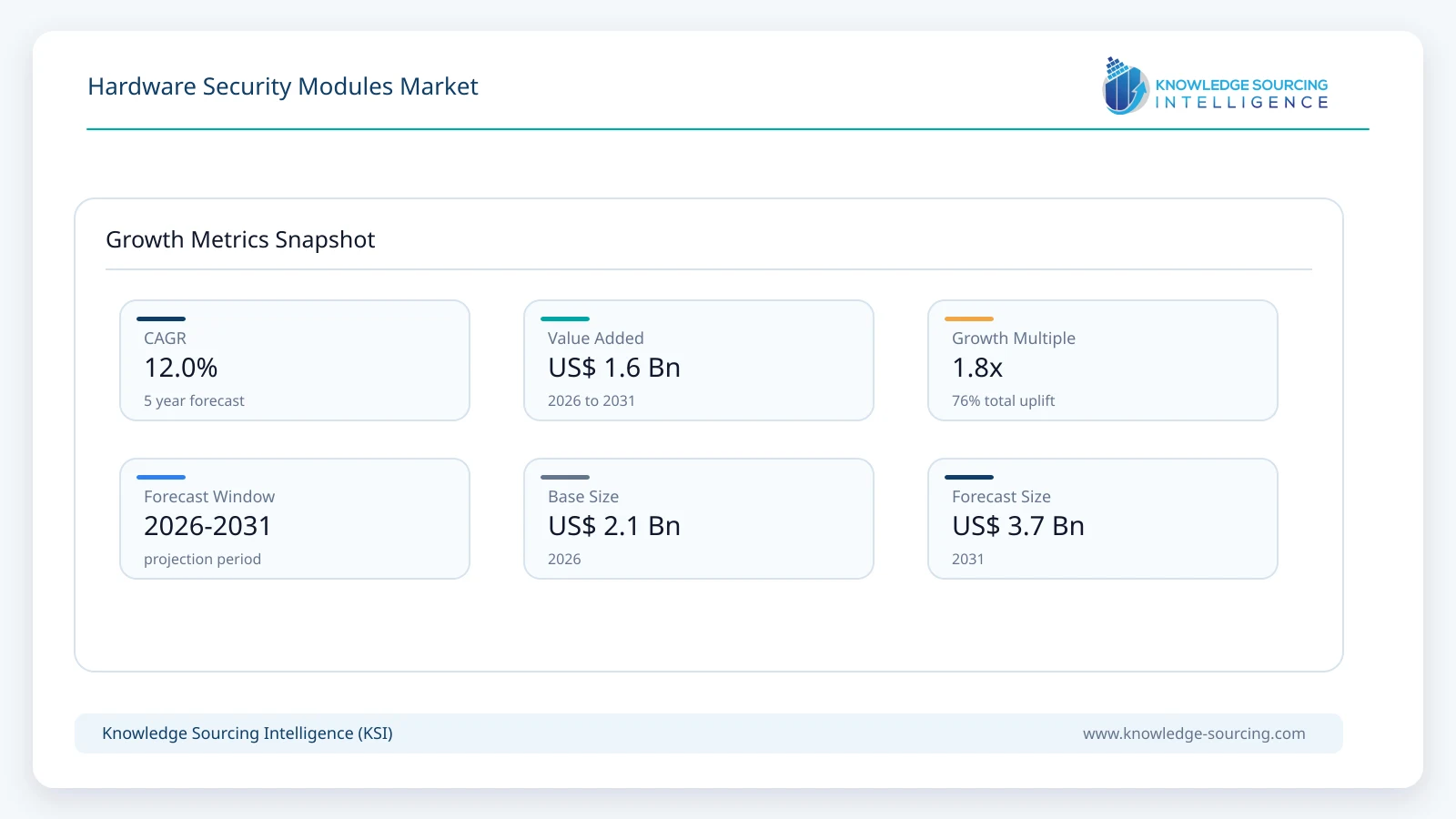

The global hardware security module (HSM) market is forecast to grow at a CAGR of 12.0%, reaching USD 3.7 billion in 2031 from USD 2.1 billion in 2026.

Highlights:

- 1Proliferation of Hyper-Scale DatacentersRapid expansion of multi-tenant cloud architectures creates severe shared-infrastructure security risks, which directly force enterprises to deploy dedicated hardware security modules to isolate multi-party cryptographic keys.

- 2Adoption of Post-Quantum Standards:Emerging quantum computing threats expose standard asymmetric encryption algorithms to catastrophic mathematical compromise, which immediately accelerates the integration of crypto-agile, firmware-upgradable hardware modules.

- 3Enforcement of Data Localization LawsImplementation of national data sovereignty mandates requires local verification of sensitive user records, which structurally dictates the installation of physical, geography-specific hardware trust roots.

- 4Growth of Machine-to-Machine NetworksEscalating deployment of automated industrial Internet of Things endpoints increases credential spoofing vulnerabilities, which systematically drives demand for hardware modules to anchor decentralized device identities.

The global expansion of cloud-native application architectures establishes a continuous requirement for specialized, single-tenant cryptographic hardware boundary isolation. Legacy enterprise infrastructures rely on localized physical perimeters, but modern multi-tenant environments introduce complex risks of hypervisor exploitation and unauthorized cross-tenant memory access. These threat vectors shift buyer priorities toward root-of-trust architectures that guarantee absolute control over the entire cryptographic key lifecycle. Hardware security modules fulfill this operational requirement by executing critical operations, including asymmetric key generation and cryptographic signature verification, inside isolated, hardened microkernels. This architectural decoupling prevents administrative overrides from compromising root keys, ensuring that even privileged infrastructure operators cannot extract active enterprise secrets.

Modern public key infrastructures exhibit an absolute engineering dependency on hardware-based cryptographic co-processors to maintain high-throughput communication security. High-volume transaction environments, such as digital banking and automated machine-to-machine authentication networks, demand thousands of concurrent cryptographic operations per second. Software-driven central processing units suffer from extreme processing overhead when managing asymmetric RSA or Elliptic Curve Cryptography handshakes, causing severe operational latency and application timeouts. Hardware security modules eliminate this performance constraint by offloading intensive mathematical computations to dedicated application-specific integrated circuits optimized for cryptographic acceleration. This hardware offloading enables enterprises to scale automated connection signing without degrading user application performance, locking HSM devices into the core architecture of enterprise networks.

Stringent regional data protection acts and international financial security standards act as the primary coercive mechanisms driving systematic hardware-based encryption adoption. Regulations such as the European Union’s General Data Protection Regulation and the Payment Card Industry Data Security Standard mandate explicit separation between encrypted data storage and cryptographic key management environments. Compliance auditors reject software-only key storage frameworks due to their inherent vulnerability to operating system breaches and offline brute-force attacks. Hardware security modules provide the precise technical compliance mechanisms required, offering verifiable physical tracking and strict multi-party administrative authentication policies. These regulatory frameworks eliminate corporate discretion regarding security expenditures, forcing organizations to embed validated cryptographic hardware directly into their operational workflows.

Within the emerging digital threat landscape, hardware-enforced cryptographic agility represents a vital strategic asset for maintaining long-term institutional data sovereignty. The impending commercialization of quantum computing platforms threatens to render standard RSA and ECC algorithms obsolete, exposing historical encrypted archives to retroactive decryption. Organizations are proactively integrating flexible, firmware-upgradable hardware modules capable of executing newly standardized post-quantum cryptographic algorithms without requiring complete physical hardware replacement. This proactive integration secures long-cycle industrial data assets against future exfiltration and decryption risks, preserving operational integrity across decadal horizons. Consequently, the selection and deployment of scalable hardware security modules operate as a critical determinant of corporate risk posture and technological longevity.

Market Dynamics

Drivers

Escalation of Advanced Persistent Threats: Organized cyber-espionage groups are increasingly targeting enterprise key management systems, which directly shifts corporate security spending toward hardware-enforced, tamper-responsive cryptographic boundaries.

Expansion of Digital Payment Ecosystems: Sovereign real-time payment infrastructures require instantaneous, high-throughput transaction authorization, which continuously forces commercial banks to scale their local hardware security module capacity.

Mandatory Zero-Trust Network Architecture Migration: Corporate security frameworks are systematically removing implicit network trust models, which establishes an immediate dependency on hardware modules to validate every digital identity.

Integration of Client-Side Cloud Encryption: Enterprise cloud consumers are demanding absolute control over their external workloads, which drives widespread adoption of local hardware modules connected via secure remote APIs.

Restraints and Opportunities

Extreme Capital Expenditures for Upgrades: High acquisition costs for certified physical hardware components create severe budget friction, which heavily restricts immediate deployment within mid-market enterprises.

Shortage of Specialized Cryptographic Engineers: Complex configuration requirements for multi-tenant hardware architectures exceed available IT personnel skillsets, which introduces operational integration delays across legacy industries.

Transition to Hybrid Cryptographic Ecosystems: The ongoing co-existence of legacy software environments and decentralized public cloud networks provides a significant commercial opportunity for vendors developing multi-platform, unified hardware control interfaces.

Automation of Cryptographic Key Lifecycles: Evolving infrastructure-as-code deployment models enable the automated provisioning of containerized hardware resources, which significantly reduces long-term operational maintenance costs for enterprise consumers.

Supply Chain Analysis

The global manufacturing ecosystem for hardware security modules exhibits an exceptional degree of concentration and vertical dependency on specialized semiconductor foundries. The initial stage of the supply chain involves the production of custom, tamper-resistant cryptographic application-specific integrated circuits and field-programmable gate arrays. These highly specialized silicon wafers are fabricated exclusively by a limited number of advanced semiconductor facilities possessing specialized certification for high-assurance security components.

Once fabricated, these secure processors are transferred to specialized hardware assembly facilities where engineers embed automated physical defenses, including reactive wire meshes and opaque epoxy coatings designed to trigger instant zeroization upon physical breach.

The assembled physical modules undergo rigorous external validation procedures conducted by accredited testing laboratories to secure essential regulatory clearances, including Federal Information Processing Standards Level 3 and Level 4 certifications.

The completed, certified units move through highly restricted distribution networks directly to enterprise security integrators, hyperscale cloud vendors, and defense contractors. This final delivery phase requires strict chain-of-custody tracking protocols to eliminate the possibility of interdiction or malicious firmware modification during transit, creating an insulated, high-barrier operational pipeline.

Government Regulations

The table below outlines the core international regulatory frameworks dictating the installation and functional validation of hardware security modules across diverse operating jurisdictions.

Regulation / Standard | Governing Body | Core Technical Mandate | Direct Impact on HSM Demand |

FIPS 140-3 | National Institute of Standards and Technology (USA) | Mandates explicit physical tamper-resistance and cryptographic boundary isolation for federal data systems. | Restricts public sector procurement exclusively to certified hardware modules, forcing structural product compliance upgrades. |

PCI DSS v4.0 | PCI Security Standards Council | Requires physical separation of decryption keys from cardholder data environments during transaction processing. | Forces global financial institutions to deploy high-throughput hardware co-processors to clear payment flows legally. |

eIDAS Regulation | European Union | Regulates electronic identification and trust services, requiring qualified signature creation devices to utilize validated hardware. | Accelerates corporate demand for specialized, network-attached hardware modules to authenticate cross-border commercial transactions. |

Key Developments

Utimaco Certification (April 2026): Utimaco secured full FIPS 140-3 certification across its entire general-purpose hardware portfolio, including the u.trust GP HSM Se-Series, establishing verified compliance with advanced physical security standards.

April 2026: Thales Trusted Cyber Technologies launched the CipherTrust Manager k160 Mk II, a compact cryptographic key management platform. It offers advanced hardware-backed security, physical optimization, and enhanced cryptographic controls for enterprise infrastructures.

Thales Launch (September 2025): Thales Trusted Cyber Technologies announced the release of version 7.15.0 for its Luna T-Series network and PCIe modules, integrating standardized post-quantum cryptographic algorithms directly into the hardware firmware.

August 2025: Marvell expanded its cloud security footprint by integrating LiquidSecurity HSMs into the Microsoft Azure Cloud HSM service. This deployment brings FIPS 140-3 Level 3 single-tenant hardware security to scalable cloud infrastructure.

Market Segmentation

By Type

The internal structural architecture of hardware security modules dictates their operational integration capacity and suitability for specific enterprise application environments. LAN-Based and Network-Attached HSMs function as autonomous, independent network nodes that provide centralized cryptographic services across distributed enterprise architectures. High-volume corporate datacenters are continuously deploying these network-attached systems because modern application environments require accessible, multi-tenant cryptographic resources. This deployment trend places significant pressure on legacy peripheral systems, which cannot scale dynamically to accommodate automated containerized microservices. Consequently, enterprises are consolidating their cryptographic infrastructure into centralized network modules, transforming corporate network architecture into an API-driven hardware trust environment.

PCI-Based and Embedded Plugin HSMs connect directly to dedicated host server motherboards via local peripheral component interconnect express slots. Specialized industrial applications and localized appliance manufacturers depend heavily on these integrated cards to deliver ultra-low latency cryptographic execution. Software processes running on the host server access the hardware acceleration card directly, eliminating the network hop latencies inherent in external architectures. This physical proximity restricts access to a single host system, which limits scaling capacity within dynamic, cloud-native application environments. Organizations utilize these embedded plugins primarily for fixed, dedicated infrastructure roles, maintaining stable operational perimeters for high-priority local workloads.

USB-Based and Portable HSMs offer highly mobile, disconnected cryptographic boundary execution for specialized offline management tasks. Root certificate authorities and field-deployed tactical systems require physical, compact units to perform isolated cryptographic signing operations. These portable devices operate using host-powered connections, which completely removes the requirement for external power delivery infrastructure in austere operating environments. This disconnected nature prevents continuous automated application access, which restricts the format to specialized administrative validation workflows. Administrative teams deploy portable modules exclusively for high-value root-key maintenance ceremonies, establishing an absolute physical air-gap for critical enterprise secrets.

By Application

The deployment configuration of hardware security modules across specific functional environments reflects the varying data velocity and structural trust requirements of enterprise operations. Banking and Financial Institutions run continuous, high-volume transactional workloads that demand deterministic, real-time cryptographic verification. Global payment networks are processing billions of concurrent authorization flows, which forces financial entities to deploy specialized hardware modules optimized for PIN translation and EMV validation. This processing volume strains standard compute networks, which lack the specialized microcode needed to accelerate financial symmetric ciphers. As a result, financial institutions are hardcoding hardware security modules into their core settlement pipelines, ensuring continuous transactional integrity.

Healthcare environments exhibit a rapidly accelerating requirement for hardware-enforced data isolation to secure sensitive patient records. Connected medical diagnostic systems and decentralized clinical networks are uploading continuous data streams, which exposes patient information to unauthorized cloud intercept risks. Regulatory healthcare frameworks mandate verifiable access controls and end-to-end payload encryption, which increases the technical complexity of hospital IT systems. IT administrators respond by deploying centralized hardware security modules to manage enterprise data encryption keys securely, preventing administrative privilege escalation from exposing patient records. This deployment strategy hardens hospital storage arrays against external ransomware threats, locking down institutional clinical data.

Corporate data architectures are transitioning toward absolute zero-trust credential verification models to counter perimeter network erosion. Distributed corporate workforces require continuous access to internal development servers and proprietary cloud databases, which increases credential spoofing vulnerabilities. Security engineering teams are deploying network-attached hardware security modules to anchor internal identity provider keys and code-signing certificates. This deployment prevents attackers from generating fraudulent administrative access tokens during network intrusions, halting lateral movement within compromised perimeters. The integration of hardware trust roots establishes a definitive verification mechanism for corporate authorization, stabilizing infrastructure access patterns.

By Industry Vertical

The structural integration of cryptographic hardware across distinct industry verticals is governed by the specific regulatory liabilities and operational environments of each sector. The Banking and Financial Services vertical operates as the primary anchor for advanced high-throughput cryptographic hardware procurement. Financial institutions must maintain uninterrupted compliance with sovereign central bank operational resilience mandates, which penalize transactional downtime or data breaches severely. This regulatory pressure drives continuous capital allocation toward highly redundant, clustered hardware security module deployments across geographically isolated primary datacenters. Financial technology platforms are adopting containerized hardware architectures to support high-velocity digital asset processing, reinforcing the absolute necessity of hardware roots.

The Government sector demands maximum-assurance physical security boundaries to protect sensitive public records and classification systems. National security agencies and civil registries process massive volumes of citizen biometric profiles and defense communications, which attract highly sophisticated state-sponsored cyber threats. Federal information security standards legally restrict government networks to hardware modules possessing verified physical tamper-responsive mechanisms. This absolute mandate eliminates software-only key storage mechanisms from state architectures, forcing procurement departments to acquire dedicated, military-grade hardware modules. Consequently, state infrastructure deployment patterns remain strictly tied to validated physical components, isolating sovereign communications from external network compromise.

The Industrial and Manufacturing Industry is rapidly integrating automated hardware authentication to secure distributed robotic assembly infrastructure. Modern factory systems utilize interconnected industrial Internet of Things sensors to optimize production efficiency, which introduces vulnerable network endpoints to the manufacturing floor. Unauthorized firmware modifications can disrupt physical manufacturing lines, exposing operators to severe physical hazards and causing significant production stoppages. Manufacturing operators are responding by deploying embedded hardware security modules to execute automated cryptographic signature checks on all incoming firmware updates. This implementation prevents unauthenticated control commands from reaching operational machinery, securing industrial automation pipelines against remote network manipulation.

Regional Analysis

The geographic distribution of hardware security module deployment is governed by regional technological infrastructure development and the enforcement intensity of local data protection legislation.

North America represents a mature, highly regulated market driven by the widespread adoption of sovereign cloud architectures and stringent federal information security mandates. Federal agencies and enterprise defense contractors operate under strict FedRAMP High and FIPS 140-3 validation guidelines, which systematically require physical cryptographic isolation. This legal architecture forces tech vendors to build specialized, hardware-enforced cloud regions, which directly sustains domestic demand for advanced network-attached modules. Commercial financial markets centered in major metropolitan zones are continuously scaling their transaction processing infrastructure, which forces enterprise data centers to install low-latency hardware co-processors. This continuous expansion anchors the regional market structure within high-value, certified physical deployments.

Europe exhibits a highly compliance-driven demand profile characterized by strict national data sovereignty regulations and pan-European security frameworks. The ongoing execution of the European Union’s Digital Operational Resilience Act and the NIS2 Directive forces critical infrastructure operators to implement verified cryptographic key control models. Organizations cannot legally utilize unisolated shared cloud infrastructure to store core sovereign root keys, which drives immediate deployment of single-tenant hardware security modules. Industrial automation sectors across central European manufacturing centers are scaling their automated device-identity architectures, which increases demand for embedded plugin modules. This regulatory alignment standardizes corporate security spending across the continent, forcing permanent hardware integration.

The Asia Pacific region is experiencing rapid infrastructure expansion characterized by the massive construction of hyper-scale datacenters and the overhaul of domestic digital payment networks. Sovereignties, including China and India, are fully implementing comprehensive domestic data protection acts, which mandate strict local processing and localized encryption of citizen data assets. This legislative push creates an immediate requirement for physical hardware trust anchors within newly established local data infrastructure facilities. High-velocity regional financial ecosystems are rolling out state-backed real-time payment interfaces, which demand high-throughput hardware security modules to clear transactions instantaneously. This rapid infrastructure deployment shifts regional procurement toward high-density network-attached systems, accelerating industrial structural evolution.

Competitive Landscape

Thales Group

Utimaco GmbH

International Business Machines Corporation

Futurex

Hewlett Packard Enterprise Company

Company Profiles

Thales Group

Thales Group strategically distinguishes itself through its comprehensive, global dominance in validated hardware-enforced data security architecture across public and private sectors. The company’s flagship Luna network-attached modules operate as the industry benchmark for high-assurance cryptographic isolation within large-scale enterprise data centers. Thales actively maintains deep integration hooks across major public cloud providers via its unified hybrid key management software platforms. This hybrid architectural positioning allows enterprise customers to manage localized physical hardware modules and cloud-based hardware instances through a singular, consolidated pane of glass. Consequently, the organization preserves a highly defensive competitive moat anchored by deep sovereign defense relationships and extensive regulatory compliance certifications globally.

Utimaco GmbH

Utimaco GmbH strategically distinguishes itself by optimizing its hardware development around highly customizable, containerized multi-tenancy architectures for cloud service providers. The organization’s general-purpose hardware family utilizes an advanced, software-defined partition model that supports up to 31 completely independent cryptographic containers on a singular physical platform. This granular isolation capability allows cloud vendors and telecommunication operators to provision independent hardware cryptographic environments for discrete clients without incurring massive physical hardware footprint expansion costs. Furthermore, Utimaco focuses heavily on developing agile post-quantum firmware extensions, which positions the company as a primary technical enabler for long-cycle infrastructure future-proofing initiatives.

Futurex

Futurex strategically distinguishes itself by engineering completely unified, native cryptographic architectures that combine general-purpose data encryption and financial payment processing capabilities inside a single physical platform. The company's proprietary Base Architecture Model relies on a fully synchronized, single-codebase framework that completely eliminates system reconfiguration downtime during vertical scaling operations. This architectural unification allows global financial technology platforms and tier-one banking institutions to consolidate disparate security hardware stacks into a streamlined, high-performance computing environment. By offering flexible deployment models spanning localized physical appliances, hybrid clouds, and its dedicated VirtuCrypt cloud platform, Futurex maintains exceptional operational deployment flexibility.

Analyst View

The deployment structure of global cryptographic key infrastructure is rapidly shifting toward dedicated, network-attached hardware roots of trust. This structural transition is unfolding because software-only isolation frameworks fail to withstand emerging multi-tenant memory exploits, forcing enterprise compliance officers to mandate verified physical silicon boundaries.

Hardware Security Module (HSM) Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 2.1 billion |

| Total Market Size in 2031 | USD 3.7 billion |

| Forecast Unit | Billion |

| Growth Rate | 12.0% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Deployment Type, Application, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

- LAN-Based HSM/Network-Attached HSM

- PCI-Based/Embedded Plugins HSM

- USB-Based/Portable HSM

By Deployment Type

- Cloud

- On-Premise

By Application

- Retail Stores

- Transportation

- Corporate

- Hospitality

- Banking and Financial Institutions

- Healthcare

- Sports & Entertainment

- Others

By Industry Vertical

- Banking and Financial Services

- Government

- IT and Communications

- Industrial and Manufacturing Industry

- Energy and Utilities

- Retail and Consumer Products

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Thailand

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

2. RESEARCH METHODOLOGY

2.1. Research Data

2.2. Assumptions

3. EXECUTIVE SUMMARY

3.1. Research Highlights

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Force Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

5. HARDWARE SECURITY MODULES (HSM) MARKET, BY TYPE

5.1. Introduction

5.2. LAN-Based HSM/Network-Attached HSM

5.3. PCI-Based/Embedded Plugins HSM

5.4. USB-Based/Portable HSM

6. HARDWARE SECURITY MODULES (HSM) MARKET, BY DEPLOYMENT

6.1. Introduction

6.2. Cloud

6.3. On-Premise

7. HARDWARE SECURITY MODULES (HSM) MARKET, BY APPLICATION

7.1. Introduction

7.2. Retail Stores

7.3. Transportation

7.4. Corporate

7.5. Hospitality

7.6. Banking and Financial Institutions

7.7. Healthcare

7.8. Sports and Entertainment

7.9. Others

8. HARDWARE SECURITY MODULES (HSM) MARKET, BY INDUSTRY VERTICAL

8.1. Introduction

8.2. Banking and Financial Services

8.3. Government

8.4. IT and Communications

8.5. Industrial and Manufacturing Industry

8.6. Energy and Utilities

8.7. Retail and Consumer Products

8.8. Others

9. HARDWARE SECURITY MODULES (HSM) MARKET, BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. USA

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. Germany

9.4.2. France

9.4.3. United Kingdom

9.4.4. Spain

9.4.5. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. UAE

9.5.3. Israel

9.5.4. Others

9.6. Asia Pacific

9.6.1. China

9.6.2. Japan

9.6.3. India

9.6.4. South Korea

9.6.5. Indonesia

9.6.6. Taiwan

9.6.7. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Emerging Players and Market Lucrativeness

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Vendor Competitiveness Matrix

11. COMPANY PROFILES

11.1. Thales Group

11.2. Utimaco GmbH

11.3. International Business Machines Corporation

11.4. Futurex

11.5. Hewlett Packard Enterprise Company

11.6. ATOS SE

11.7. Yubico

11.8. Ultra Electronics

11.9. Yubico

11.10. Securosys SA

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations