Report Overview

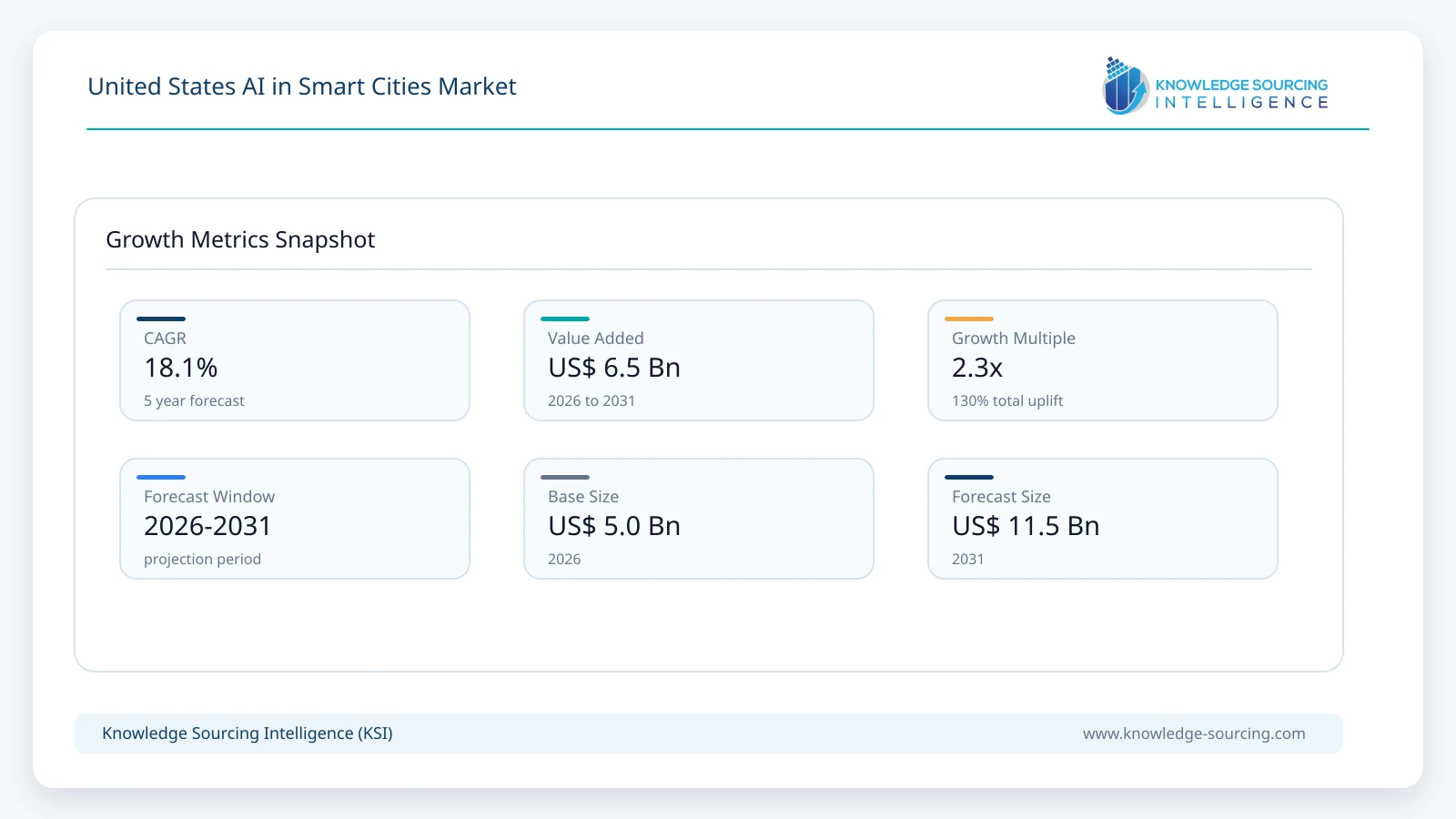

The US AI in Smart Cities Market is forecast to grow at a CAGR of 18.1%, reaching USD 11.5 billion in 2031 from USD 5.0 billion in 2026.

Highlights:

- 1Growing demandis supported by federal and state investments in intelligent transportation systems, public infrastructure modernization, and connected municipal services.

- 2Traffic managementrepresents one of the largest commercial applications because transportation agencies seek congestion reduction, incident prediction, and adaptive traffic control.

- 3Machine learningremains a foundational technology for predictive maintenance, operational forecasting, and infrastructure optimization across multiple city departments.

- 4Cloud-based deploymentcontinues to attract greater adoption due to scalability, centralized analytics, and reduced infrastructure management requirements.

- 5Federal cybersecurity guidance and AI governance initiativesincreasingly influence procurement specifications for municipal technology projects.

- 6Competition is shiftingtoward integrated platforms combining AI software, cloud services, networking infrastructure, and operational technology.

The United States AI in Smart Cities market comprises artificial intelligence software, analytics platforms, edge intelligence, cloud infrastructure, and integrated decision-support systems deployed to improve the planning, operation, and management of urban infrastructure and public services. AI technologies enable municipalities, transportation agencies, utilities, emergency response organizations, and public administrators to process large volumes of real-time data from sensors, connected infrastructure, cameras, and digital platforms. The resulting insights support operational efficiency, service reliability, resource optimization, and public safety while reducing long-term operating costs.

Demand is primarily driven by state and local governments seeking measurable improvements in transportation efficiency, energy utilization, public safety, and infrastructure maintenance. Procurement decisions increasingly emphasize interoperability with existing digital infrastructure, cybersecurity compliance, scalability, and long-term lifecycle costs rather than standalone software functionality. Buyers also evaluate vendors based on implementation expertise, data governance capabilities, and the ability to integrate AI applications across multiple municipal departments.

Federal infrastructure investment continues to create opportunities for AI deployment in transportation systems, utility modernization, broadband expansion, and environmental monitoring. Programs administered through agencies such as the U.S. Department of Transportation (USDOT), Department of Energy (DOE), and National Institute of Standards and Technology (NIST) encourage municipalities to adopt digital technologies that improve operational performance while strengthening infrastructure resilience. As cities expand connected infrastructure, AI becomes an operational layer that converts sensor-generated information into actionable recommendations.

Cloud deployment remains the preferred implementation model because municipalities require scalable computing resources for processing traffic data, surveillance feeds, environmental sensors, and utility networks. Nevertheless, organizations responsible for critical infrastructure continue to maintain hybrid and on-premises deployments where latency, regulatory requirements, or security policies necessitate local data processing.

Technology adoption is no longer confined to large metropolitan areas. Mid-sized municipalities increasingly pursue phased smart city initiatives focused on specific operational challenges, including predictive maintenance of public assets, intelligent traffic signal management, automated incident detection, and energy optimization in municipal facilities. These targeted deployments offer measurable operational returns while limiting upfront capital expenditure.

The supplier landscape combines cloud service providers, semiconductor companies, industrial automation vendors, enterprise software firms, networking specialists, and infrastructure technology providers. Competition increasingly depends on ecosystem partnerships that combine AI models, connectivity, cybersecurity, industrial sensors, and municipal software platforms into integrated solutions capable of supporting long-term digital infrastructure programs.

Market Drivers

Expansion of Intelligent Transportation Infrastructure

Transportation agencies face mounting pressure to improve roadway efficiency without proportionally expanding physical infrastructure. AI-powered traffic optimization enables adaptive signal timing, congestion forecasting, and automated incident response using real-time traffic information. Public authorities increasingly prioritize solutions capable of reducing travel delays while improving emergency vehicle routing. Technology suppliers therefore invest in integrated traffic analytics platforms that combine AI, connected cameras, roadside sensors, and cloud-based traffic management systems.

Rising Investment in Infrastructure Asset Management

Municipal governments oversee extensive networks of roads, bridges, utilities, street lighting, and public buildings that require continuous maintenance. Traditional inspection methods are labor-intensive and often identify issues only after deterioration has progressed. Predictive analytics supported by machine learning allows infrastructure managers to prioritize maintenance based on asset condition rather than fixed schedules. This improves capital allocation while reducing service disruptions and repair costs, making AI-supported maintenance an attractive procurement category.

Utility Modernization and Energy Efficiency Programs

Electric utilities and municipal energy departments increasingly deploy AI to balance electricity demand, integrate distributed renewable generation, detect network anomalies, and improve building energy management. Growing electrification, distributed energy resources, and grid modernization programs require advanced forecasting capabilities that conventional automation systems cannot easily deliver. Suppliers responding to utility demand increasingly integrate AI into broader energy management platforms supporting operational efficiency and sustainability objectives.

Growth of Public Safety Applications

Law enforcement agencies, emergency management organizations, and municipal security departments continue adopting AI-assisted video analytics, anomaly detection, and predictive resource allocation. Computer vision improves situational awareness by identifying traffic incidents, unauthorized access, abandoned objects, and emergency conditions more rapidly than manual monitoring alone. Procurement increasingly favors platforms capable of supporting multiple public safety applications while complying with evolving privacy and cybersecurity requirements.

Market Restraints and Challenges

Complex Data Governance Requirements

Municipal AI systems collect information from cameras, sensors, connected vehicles, utilities, and citizen services. Managing this information requires strict governance policies covering privacy, data ownership, retention, and cybersecurity. Compliance obligations increase implementation complexity, particularly for cities integrating multiple legacy systems. Vendors increasingly address this challenge through enhanced encryption, identity management, and transparent AI governance capabilities.

Legacy Infrastructure Integration

Many municipalities operate aging operational technology that predates modern AI platforms. Integrating legacy transportation control systems, utility networks, and municipal databases often requires customized engineering, increasing deployment costs and project timelines. Buyers therefore prioritize suppliers with proven integration capabilities and open architecture platforms capable of supporting gradual modernization.

Budget Constraints Across Municipal Governments

Although AI can reduce long-term operating expenses, many cities face constrained annual budgets and competing infrastructure priorities. Procurement decisions frequently depend on grant availability, measurable return on investment, and phased deployment strategies rather than comprehensive citywide implementation. Solution providers increasingly offer modular deployments and subscription pricing to reduce financial barriers.

Workforce and Technical Skills Shortages

Successful AI implementation requires expertise in data science, cybersecurity, cloud computing, and operational technology. Many municipal organizations experience difficulty recruiting and retaining these specialized skills. As a result, buyers increasingly seek managed services, vendor training programs, and automated system management capabilities that reduce internal resource requirements.

Major Segment Analysis

Traffic Management

Traffic management represents one of the most commercially significant application segments because transportation congestion directly affects economic productivity, fuel consumption, logistics efficiency, and public safety. Urban transportation authorities increasingly require predictive systems capable of analyzing traffic flows, weather conditions, construction activity, and incident reports simultaneously. AI enables continuous optimization instead of relying on fixed traffic control schedules.

Procurement priorities emphasize reliability, interoperability with existing intelligent transportation infrastructure, and measurable operational improvements. Agencies seek solutions capable of integrating roadside sensors, connected vehicle information, surveillance cameras, and geographic information systems within a unified operational environment.

Competition extends beyond software performance. Vendors differentiate through deployment experience, cloud integration, cybersecurity capabilities, and long-term maintenance services. Revenue opportunities continue expanding as municipalities modernize transportation infrastructure using federal funding programs and pursue broader connected mobility initiatives.

Competitive Landscape

Competition within the United States AI in Smart Cities market combines enterprise software providers, cloud platform operators, semiconductor manufacturers, industrial automation companies, networking specialists, and digital infrastructure providers. IBM Corporation, Microsoft Corporation, Google LLC, Amazon Web Services, Inc., NVIDIA Corporation, Cisco Systems, Inc., Intel Corporation, Siemens AG, Oracle Corporation, and Schneider Electric SE compete by delivering integrated technology ecosystems rather than standalone AI applications.

Product differentiation increasingly depends on AI model performance, cloud scalability, cybersecurity, edge computing, digital twin capabilities, industrial connectivity, and interoperability with municipal infrastructure. Strategic partnerships between cloud providers, networking companies, utilities, transportation agencies, and systems integrators continue strengthening competitive positioning. Geographic expansion increasingly focuses on partnerships with municipal governments and infrastructure operators implementing long-term modernization programs.

Recent Developments

March 2026: NVIDIA introduced additional enterprise AI infrastructure enhancements supporting physical AI, digital twins, and edge computing applications. Commercially, the technology improves scalability for transportation management, infrastructure monitoring, and city operations requiring high-performance AI processing.

January 2026: Microsoft announced expanded AI capabilities across its cloud and public sector offerings to support government organizations deploying secure generative AI and intelligent data analytics. The development strengthens municipal AI deployment options while emphasizing responsible AI governance.

October 2025: Amazon Web Services expanded services supporting government organizations through additional generative AI capabilities and public sector cloud innovations. The announcement provides municipalities with broader AI deployment options while addressing security and compliance requirements.

Regulatory and Policy Environment

The regulatory framework for AI in U.S. smart cities continues evolving through federal guidance, state legislation, and agency-specific standards. NIST's AI Risk Management Framework provides organizations with structured guidance for trustworthy AI development, deployment, and governance. Municipal buyers increasingly reference these principles during procurement evaluations.

Federal infrastructure legislation continues supporting investments in transportation modernization, broadband deployment, electric grid improvements, and infrastructure resilience, indirectly encouraging AI adoption across municipal operations. Transportation agencies also align projects with USDOT intelligent transportation initiatives and cybersecurity guidance for connected infrastructure.

Cybersecurity remains a critical procurement consideration. Municipal organizations increasingly require compliance with recognized federal cybersecurity practices, secure cloud architectures, identity management standards, and continuous monitoring capabilities. Vendors demonstrating transparent AI governance, explainability, privacy protections, and secure data handling strengthen their competitiveness during public sector procurement processes.

Outlook and Strategic Implications

The United States AI in Smart Cities market is expected to experience sustained investment as municipalities seek operational efficiency, infrastructure resilience, and improved public service delivery. Procurement strategies are shifting toward integrated platforms capable of supporting multiple departments rather than isolated technology deployments.

Investment priorities will increasingly include predictive infrastructure maintenance, intelligent transportation systems, AI-assisted emergency management, digital utility operations, and environmental monitoring. Cloud platforms combined with edge computing will become more prevalent as cities process larger volumes of real-time operational data while addressing latency and security requirements.

Competitive positioning will depend less on individual AI algorithms and more on ecosystem integration, implementation expertise, cybersecurity capabilities, and long-term managed services. Vendors able to demonstrate measurable operational outcomes, regulatory compliance, and scalable deployment models are expected to strengthen their position in municipal procurement programs.

Challenges related to budget constraints, workforce availability, cybersecurity, and legacy infrastructure integration will continue influencing purchasing decisions. Nevertheless, federal infrastructure funding, AI governance standards, and continued modernization of transportation and utility networks are expected to create substantial commercial opportunities for technology providers serving the United States AI in Smart Cities market over the forecast period.

United States AI in Smart Cities Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 5.0 billion |

| Total Market Size in 2031 | USD 11.5 billion |

| Forecast Unit | Billion |

| Growth Rate | 18.1% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Technology, Application, Deployment Mode |

| Companies |

|

Market Segmentation

By Technology

By Application

By Deployment Mode

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter's Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. UNITED STATES AI IN SMART CITIES MARKET BY TECHNOLOGY

5.1. Introduction

5.2. Machine Learning

5.3. Natural Language Processing (NLP)

5.4. Computer Vision

5.5. Deep Learning

5.6. Predictive Analytics

6. UNITED STATES AI IN SMART CITIES MARKET BY APPLICATION

6.1. Introduction

6.2. Traffic Management

6.3. Public Safety and Security

6.4. Energy Management

6.5. Infrastructure Management

6.6. Environmental Monitoring

6.7. Smart Governance

7. UNITED STATES AI IN SMART CITIES MARKET BY DEPLOYMENT MODE

7.1. Introduction

7.2. Cloud-Based

7.3. On-Premises

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. IBM Corporation

9.2. Microsoft Corporation

9.3. Google LLC

9.4. Amazon Web Services, Inc.

9.5. NVIDIA Corporation

9.6. Cisco Systems, Inc.

9.7. Intel Corporation

9.8. Siemens AG

9.9. Oracle Corporation

9.10. Schneider Electric SE

10. APPENDIX

10.1. Currency

10.2. Assumptions

10.3. Base and Forecast Years Timeline

10.4. Key Benefits for Stakeholders

10.5. Research Methodology

10.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations