Report Overview

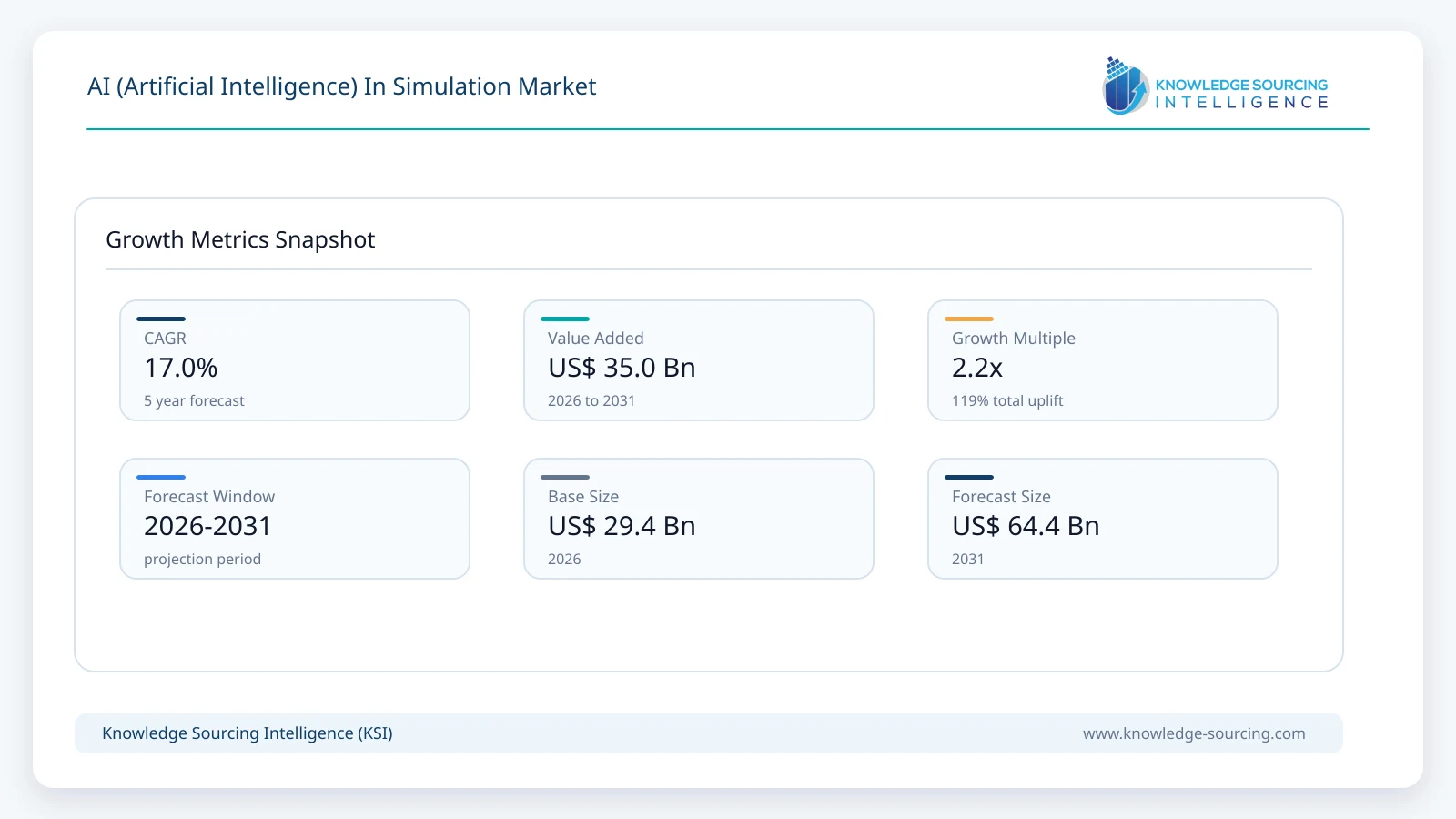

The Global AI (Artificial Intelligence) in Simulation market is forecast to grow at a CAGR of 17.0%, reaching USD 64.36 billion in 2031 from USD 29.35 billion in 2026.

Highlights:

- 1Advancements in Simulation TechnologyEnhanced AI-driven simulations improve product design and manufacturing efficiency.

- 2Cost and Efficiency GainsAI simulations optimize processes, reducing costs and physical prototyping needs.

- 3North American LeadershipMajor tech firms drive AI simulation innovation and market growth.

- 4Industry ApplicationsAI simulations enhance automotive, aerospace, and construction through predictive analytics.

Artificial intelligence in simulation is a type of simulation model used to mimic the characteristics of the real world by leveraging the cognitive learning capabilities of human intelligence. Artificial intelligence industry technologies replicate human intelligence through machine learning processes. Simulation is a virtual representation of real-world environments created using computer-based technologies. These simulations provide critical applications across various industries, including aerospace, automotive, construction, and telecommunications, supporting the development of advanced products and innovative solutions.

Multiple types of simulation models are available across the industry, including the agent-based model, the Monte Carlo model, and the system dynamics model, among others. Agent-based models concentrate on individual "agents" within a system and simulate intricate interactions like shopkeepers and customers. Monte Carlo models conduct multiple simulations to statistically evaluate potential outcomes. System dynamics models depict complex systems with interconnected elements and analyze how alterations in one part can impact others.

A major factor that is forecasted to boost the global AI in the simulation market can be attributed to the advancements in simulation technology, demand for predictive analysis, enhanced efficiency, and reduced cost.

The global AI ecosystem has witnessed massive growth in developing new technologies, which can be credited to the advancement in the technological landscape worldwide. AI in the simulation model also offers multiple advantages, which include boosting the efficiency in the production development phase of the industries and understanding the features and issues through real-world simulation tests, and reducing the overall manufacturing cost of the industries.

AI in Simulation Market Growth Drivers:

Advancements in simulation technology.

The application of simulation technology has increased significantly, mainly to enhance the manufacturing processes of multiple industries, including improving the designs of the products, which further helps reduce manufacturing expenses. The simulations aid in forecasting product performance, pinpointing manufacturing challenges, and providing a safe training environment for workers. The increasing emphasis on product optimization and industrial automation also resulted in advancements in simulation technologies.

Many companies and organizations have introduced new technologies that boost the capability of simulation technologies. For instance, Ansys, a global leader in simulation technology, introduced its latest technology to boost simulation technology advancements. The Ansys Discovery software is a simulation-driven 3D design tool that can be used to create and analyze 3D models within a virtual setting. Similarly, Toyota also integrated additional technological advancements in its THUMS (Total Human Model for Safety) software system, designed to simulate the human body's response in automobile accidents and enhance the vehicle's safety features.

Boosting efficiency and cutting down costs in the manufacturing sector.

Businesses are always searching for methods to optimize operations and decrease costs. AI-powered simulations assist in analyzing procedures to identify inefficiencies, predict potential problems, and reduce the need for costly physical prototypes. Consequently, this leads to enhanced efficiency and reduced expenses. The growing AI and simulation in the manufacturing industry can be attributed to the continuous efforts to improve production processes, coupled with proactive measures to promote industrial automation.

For instance, in July 2023, Mercedes-Benz AG started conducting trials with ChatGPT in live operations, expediting the integration of smart tools within the MO360 digital production ecosystem, which was initially launched in 2020. In order to enhance the processing of production data, such as that related to quality control, ChatGPT will serve as a versatile, voice-activated interface for production staff.

AI in Simulation Market Restraints:

Data bias can restrain the AI simulation market growth.

AI simulations are capable of acquiring knowledge from data. In cases where the data contains concealed biases, such as making judgments based on race rather than merit, the simulation could unintentionally adopt these biases and consequently make unjust decisions. As a result, incorrect or detrimental consequences may arise.

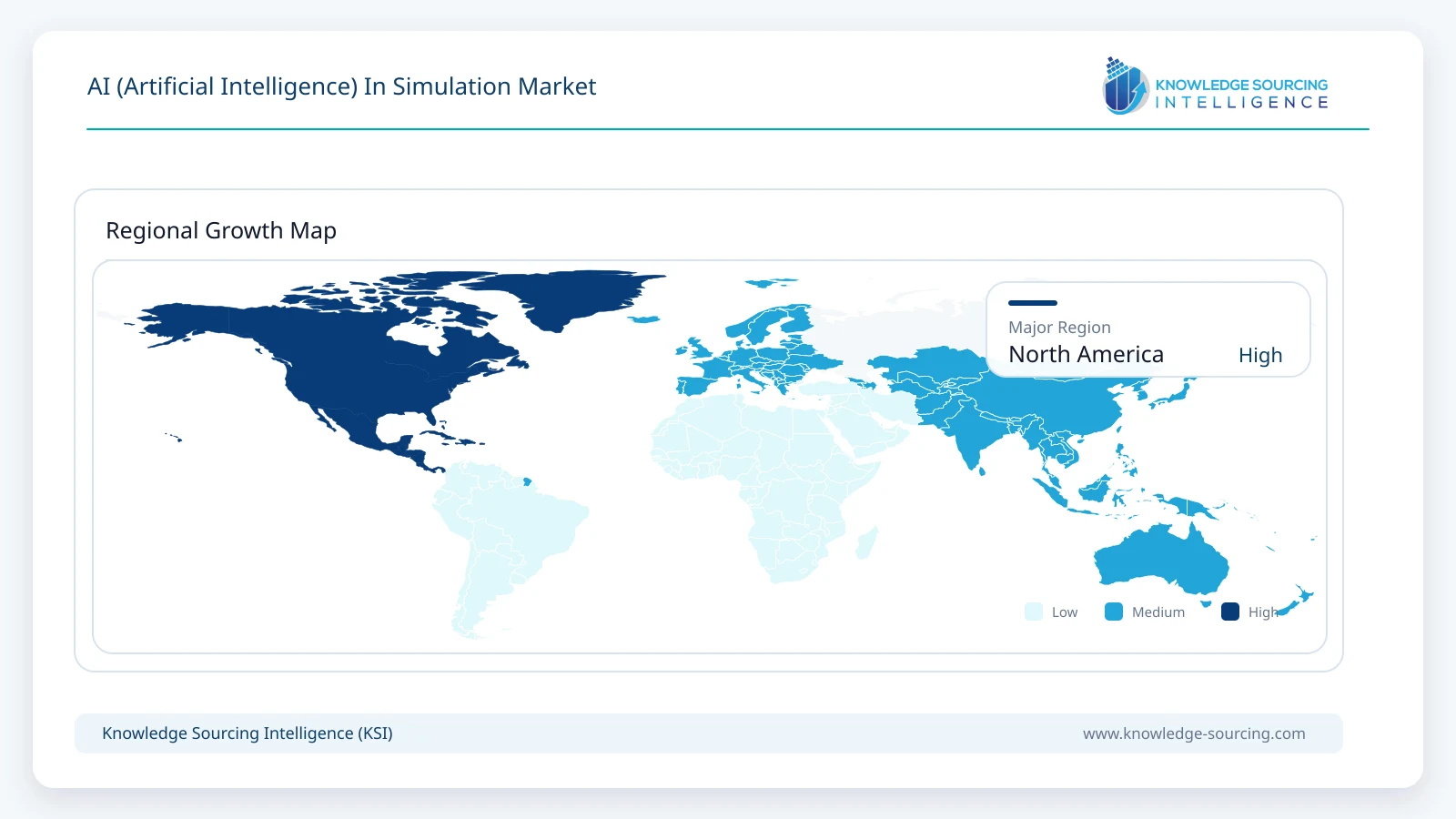

AI in the Simulation Market Geographical Outlook:

North America is forecasted to hold a major market share

North America is anticipated to account for a significant share of the AI simulation market as major technology companies in the region are leading the way in AI research and development. This growth is establishing a strong presence in the AI simulation market and prioritizes the cultivation of innovation.

In October 2023, the Defence Advanced Research Projects Agency (DARPA) developed an innovative method of modeling and simulation to enhance the autonomy of different platforms, including drones and uncrewed vehicles. This fresh approach aims to overcome the constraints of conventional high-fidelity simulations utilized in training autonomous systems. In May 2023, a research collaboration at Ontario Tech University aimed to develop simulated medical training technology specifically designed for physicians in remote areas.

Major Players and Products in AI in Simulation Market:

Altair OptiStruct: Altair OptiStruct, an integral part of the Altair HyperWorks suite, is a robust structural analysis and optimization software. It is extensively utilized by engineers to examine the performance of structures under different loads and conditions and enhance designs in terms of weight, strength, and other essential performance criteria.

Hexagon: Hexagon (HxGN), previously known as MSC, offers Smart Build Insight, which is a cutting-edge solution developed by Hexagon to enhance building design and construction by connecting the office and the field. It achieves this by harnessing digitalization across the entire construction process.

AI in Simulation Market Key Developments:

In October 2023, Altair launched Altair HyperWorks 2023, the ultimate Computer Aided Engineering (CAE) platform, offering engineers an extensive array of design and simulation products tailored for various industries such as automotive, aerospace, electronics, and beyond. This platform empowers engineers of all proficiency levels with unparalleled comprehensiveness, power, versatility, and openness.

In October 2023, Foxconn partnered with NVIDIA to integrate the latter’s technology and aimed at facilitating diverse applications, including the digitalization of manufacturing and inspection procedures, the progression of AI-powered electric vehicles and robotics systems, and the expansion of language-based generative AI services.

In February 2023, AVEVA, a well-known international leader in industrial software, launched its latest software, AVEVA Predictive Analytics. This state-of-the-art software is specifically developed to meet the predictive monitoring requirements of diverse industrial sectors, such as oil and gas, power, chemicals, mining and minerals, and manufacturing.

List of Top AI in Simulation Companies:

AnyLogic

IBM

Altair

Sky Engine AI

Hadean

AI in Simulation Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 29.35 billion |

| Total Market Size in 2031 | USD 64.36 billion |

| Forecast Unit | Billion |

| Growth Rate | 17.0% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Technology, Deployment, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Technology

- Simulation Modeling

- Predictive & Prescriptive Analytics

- Platform as a Service (PaaS)

- Others

By Deployment

- Cloud

- On-Premise

By End-User

- Automotive

- Infrastructure

- Manufacturing

- Education

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- UK

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Taiwan

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key benefits for the stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. The Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. AI (ARTIFICIAL INTELLIGENCE) IN THE SIMULATION MARKET BY TECHNOLOGY

5.1. Introduction

5.2. Simulation Modeling

5.3. Predictive & Prescriptive Analytics

5.4. Platform as a Service (PaaS)

5.5. Others

6. AI (ARTIFICIAL INTELLIGENCE) IN THE SIMULATION MARKET BY DEPLOYMENT

6.1. Introduction

6.2. Cloud

6.3. On-premise

7. AI (ARTIFICIAL INTELLIGENCE) IN THE SIMULATION MARKET BY END-USER

7.1. Introduction

7.2. Automotive

7.3. Infrastructure

7.4. Manufacturing

7.5. Education

7.6. Others

8. AI (ARTIFICIAL INTELLIGENCE) IN THE SIMULATION MARKET BY GEOGRAPHY

8.1. Introduction

8.1. North America

8.1.1. By Technology

8.1.2. By Deployment

8.1.3. By End-User

8.1.4. By Country

8.1.4.1. United States

8.1.4.2. Canada

8.1.4.3. Others

8.2. South America

8.2.1. By Technology

8.2.2. By Deployment

8.2.3. By End-User

8.2.4. By Country

8.2.4.1. Brazil

8.2.4.2. Argentina

8.2.4.3. Others

8.3. Europe

8.3.1. By Technology

8.3.2. By Deployment

8.3.3. By End-User

8.3.4. By Country

8.3.4.1. Germany

8.3.4.2. France

8.3.4.3. United Kingdom

8.3.4.4. Spain

8.3.4.5. Others

8.4. Middle East and Africa

8.4.1. By Technology

8.4.2. By Deployment

8.4.3. By End-User

8.4.4. By Country

8.4.4.1. Saudi Arabia

8.4.4.2. UAE

8.4.4.3. Israel

8.4.4.4. Others

8.5. Asia Pacific

8.5.1. By Technology

8.5.2. By Deployment

8.5.3. By End-User

8.5.4. By Country

8.5.4.1. China

8.5.4.2. Japan

8.5.4.3. India

8.5.4.4. South Korea

8.5.4.5. Indonesia

8.5.4.6. Taiwan

8.5.4.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. AnyLogic

10.2. IBM

10.3. Altair

10.4. Sky Engine AI

10.5. Hadean

10.6. MSC (Hexagon)

10.7. CosmoTech

10.8. Simulation Labs

10.9. ANSYS, Inc

10.10. Cognata

10.11. Zenarate

10.12. Collimator

Navigate

Trusted by the world's leading organizations