Report Overview

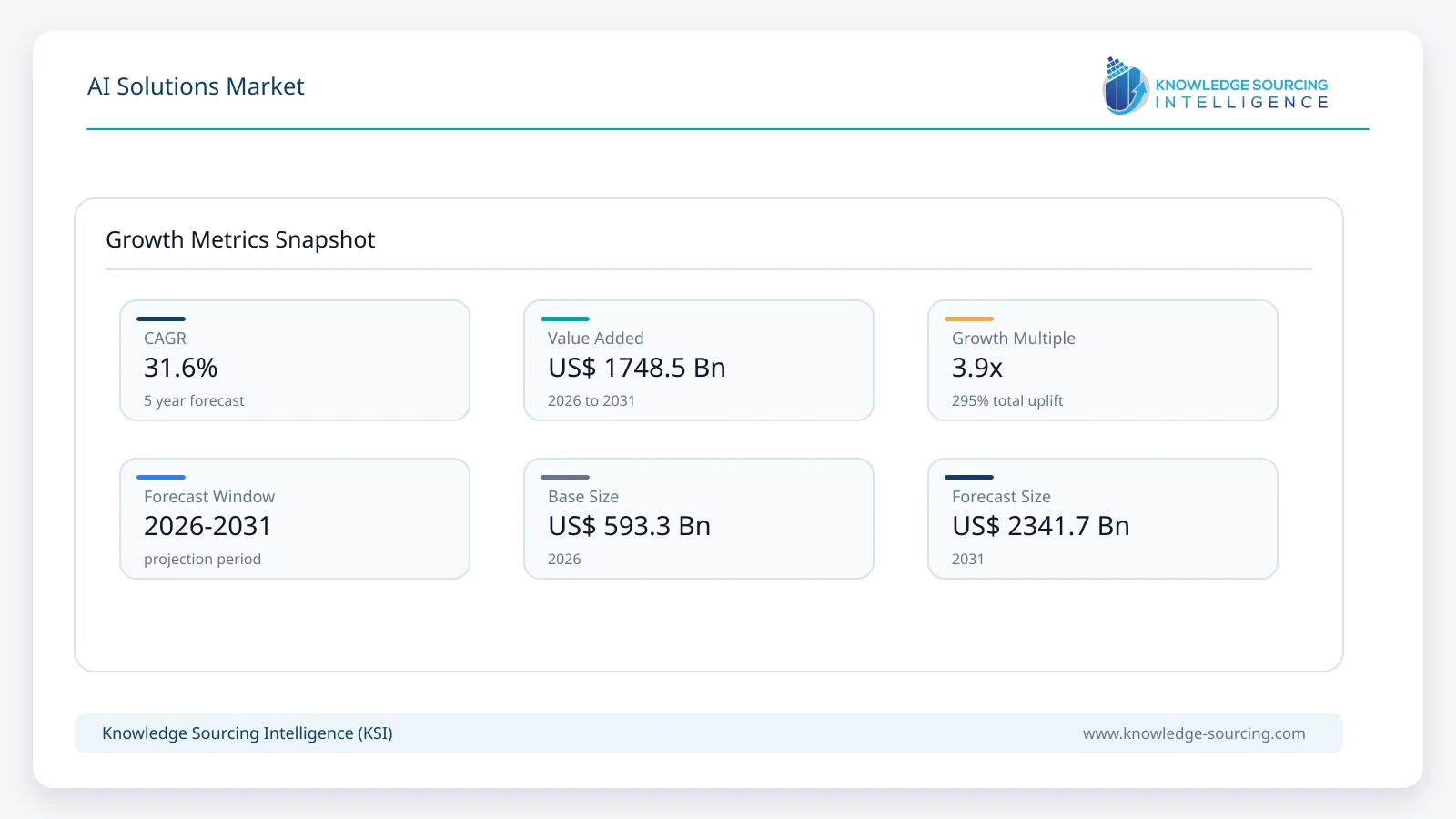

The AI Solutions Market is forecast to grow at a CAGR of 31.60%, reaching USD 2,341.73 billion in 2031 from USD 593.28 billion in 2026.

Highlights:

- 1Enterprise productivity improvement remains one of the strongest purchasing motivations for AI solutions across multiple industries.

- 2Cloud deployment continues to attract strong customer interest due to scalability, continuous software updates, and lower infrastructure management requirements.

- 3Generative AI is expanding enterprise use cases in customer service, software development, document processing, and knowledge management.

- 4North America maintains strong commercial demand because of technology investment, AI infrastructure availability, and enterprise digital maturity.

- 5Regulatory developments concerning AI governance, transparency, privacy, and risk management are influencing procurement and deployment strategies.

- 6Competition increasingly centers on platform integration, domain-specific AI capabilities, governance tools, and enterprise-grade security.

The AI solutions market comprises software platforms, application frameworks, embedded artificial intelligence capabilities, deployment services, and managed offerings that enable organizations to automate decision-making, improve operational efficiency, generate business insights, and develop intelligent customer-facing applications. The market covers cloud-based and on-premise deployments supporting machine learning (ML), natural language processing (NLP), computer vision, generative AI, forecasting, and optimization across industries including banking, healthcare, manufacturing, retail, telecommunications, government, and energy.

Enterprise demand has shifted from experimental AI initiatives toward production-scale deployments that address measurable business outcomes. Organizations are prioritizing solutions capable of reducing operating costs, improving workforce productivity, strengthening customer engagement, and supporting faster operational decisions. Procurement decisions increasingly emphasize model reliability, governance, interoperability with existing enterprise software, cybersecurity, regulatory compliance, and total cost of ownership rather than algorithm performance alone.

Large enterprises continue to account for a considerable share of spending because they possess substantial datasets, mature IT infrastructure, and dedicated AI governance teams. However, cloud-native AI platforms, pre-trained foundation models, and software-as-a-service delivery have lowered technical barriers for mid-sized organizations, broadening the customer base across multiple sectors. Buyers increasingly seek integrated platforms that combine model development, deployment, monitoring, security, and lifecycle management instead of purchasing fragmented AI tools from multiple vendors.

The competitive environment reflects a combination of hyperscale cloud providers, enterprise software vendors, consulting firms, AI platform developers, and specialized analytics companies. Suppliers compete through ecosystem partnerships, industry-specific AI models, infrastructure optimization, developer tools, and enterprise integration capabilities. Strategic alliances with semiconductor providers, cloud infrastructure companies, and systems integrators have become essential for scaling commercial deployments.

Growing investment in enterprise data modernization also supports market expansion. Organizations recognize that AI performance depends heavily on high-quality data management, governance frameworks, and scalable computing infrastructure. Consequently, AI procurement increasingly accompanies investments in cloud migration, cybersecurity, enterprise data platforms, and application modernization.

Market Drivers

Enterprise Automation and Operational Efficiency

Organizations continue to automate repetitive workflows to improve productivity and address labor shortages in administrative, technical, and operational functions. AI solutions support intelligent document processing, predictive maintenance, fraud detection, customer support automation, and workflow optimization.

Buyers increasingly evaluate AI investments using measurable financial indicators such as operating expense reduction, faster processing times, and workforce efficiency improvements. Solution providers respond by offering packaged AI applications with faster implementation cycles and industry-specific workflows, reducing deployment complexity while improving customer adoption.

Expansion of Cloud Computing Infrastructure

Global investment in hyperscale cloud infrastructure has substantially increased enterprise access to AI computing resources. Organizations no longer need extensive capital expenditure to develop and deploy sophisticated AI models.

Cloud-based AI platforms offer flexible computing capacity, integrated development environments, and managed machine learning services that reduce implementation time. Suppliers continue expanding regional cloud availability, enabling organizations to meet data residency requirements while supporting large-scale AI workloads.

Growing Availability of Enterprise Data

Businesses generate increasing volumes of structured and unstructured data from ERP systems, connected equipment, digital commerce platforms, industrial sensors, financial transactions, and customer interactions. Organizations increasingly view these datasets as strategic assets capable of supporting predictive analytics and intelligent decision-making.

AI vendors have responded by strengthening data integration capabilities, enabling organizations to connect multiple enterprise systems while improving data governance and model performance.

Rising Demand for Industry-Specific AI Applications

Generic AI platforms are gradually giving way to industry-oriented solutions designed around sector-specific workflows, regulatory requirements, and operational challenges. Healthcare organizations require clinical documentation support, manufacturers prioritize predictive maintenance, while financial institutions seek fraud detection and risk assessment capabilities.

Industry specialization reduces deployment timelines and improves return on investment, making sector-focused AI applications attractive for enterprise buyers.

Market Restraints and Challenges

Data Privacy and Regulatory Compliance

AI implementation frequently involves processing sensitive personal, financial, healthcare, and operational information. Compliance with privacy regulations and emerging AI governance requirements increases implementation complexity, particularly for multinational organizations operating across multiple jurisdictions.

Organizations invest additional resources in data governance, audit trails, explainability, and model monitoring before approving enterprise-wide deployment.

High Infrastructure and Computing Costs

Advanced AI models require substantial computing capacity, specialized processors, storage systems, and networking infrastructure. Organizations with extensive inference workloads face rising operational expenditures associated with cloud computing and accelerated hardware.

Suppliers increasingly optimize model architectures, improve inference efficiency, and introduce consumption-based pricing to reduce customer cost pressures.

Shortage of Skilled AI Professionals

Successful deployment extends beyond purchasing AI software. Organizations require experienced data scientists, machine learning engineers, cybersecurity professionals, AI governance specialists, and domain experts capable of integrating AI into business processes.

Limited availability of specialized talent extends implementation schedules and increases consulting expenditures, particularly for organizations beginning their AI adoption journey.

Integration with Legacy Enterprise Systems

Many enterprises operate complex IT environments built over several decades. Integrating AI solutions with existing ERP platforms, databases, manufacturing systems, and business applications often requires extensive customization.

Technology providers increasingly address this challenge through standardized APIs, low-code integration tools, and pre-built enterprise connectors that simplify deployment.

Major Segment Analysis

Cloud Deployment

Cloud deployment represents one of the most commercially significant segments because it enables organizations to deploy AI applications without extensive investment in dedicated infrastructure. Enterprises benefit from elastic computing resources, centralized model management, continuous software updates, and access to advanced GPU infrastructure that would otherwise require substantial capital expenditure.

Buyers increasingly favor cloud-based AI solutions for customer analytics, conversational AI, forecasting, and enterprise automation due to shorter implementation cycles and simplified scalability. Cloud platforms also support collaborative model development across geographically distributed teams while providing integrated security, monitoring, and lifecycle management capabilities.

Competition within this segment extends beyond computing capacity. Suppliers differentiate through managed AI services, industry-specific development environments, foundation model access, governance capabilities, and integration with broader enterprise software ecosystems. Commercial success increasingly depends on providing complete AI platforms rather than standalone infrastructure.

As organizations pursue enterprise-wide AI adoption, cloud deployment continues generating recurring subscription revenue while supporting continuous software innovation, making it a commercially attractive segment for both customers and technology providers.

Regional Analysis

North America maintains strong market demand due to substantial enterprise technology spending, mature cloud infrastructure, advanced semiconductor availability, and extensive AI research investment. Large corporations across financial services, healthcare, manufacturing, and technology sectors continue expanding AI deployments while government initiatives encourage responsible AI development and cybersecurity improvements.

Europe emphasizes trustworthy AI adoption supported by regulatory frameworks, industrial automation, and enterprise software modernization. Manufacturing, automotive, financial services, and healthcare organizations increasingly invest in compliant AI solutions that support operational efficiency while addressing privacy and governance requirements. Regulatory compliance remains a major purchasing consideration throughout the region.

Asia Pacific represents a major investment destination supported by industrial digitalization, expanding cloud infrastructure, semiconductor manufacturing, and government-backed AI strategies. China, Japan, South Korea, India, and Australia continue investing in AI research, manufacturing automation, financial technology, healthcare innovation, and smart infrastructure, supporting sustained enterprise demand.

Middle East and Africa continues expanding AI adoption through national digital economy programs, smart city initiatives, public sector modernization, and investment in cloud infrastructure. Adoption remains concentrated among government agencies, financial institutions, energy companies, and telecommunications providers, although workforce development remains an important constraint.

South America demonstrates gradual adoption as organizations modernize enterprise IT infrastructure and expand cloud utilization. Financial institutions, retailers, mining companies, and telecommunications operators increasingly evaluate AI solutions for operational efficiency, customer engagement, and predictive analytics. Economic uncertainty and uneven digital infrastructure continue influencing investment timing.

Competitive Landscape

The AI solutions market remains moderately concentrated, with competition driven by technology breadth, enterprise integration capabilities, cloud infrastructure access, AI governance features, and industry expertise. IBM Corporation, Microsoft Corporation, Google LLC, NVIDIA Corporation, Oracle Corporation, Accenture plc, Amazon Web Services, Inc., SAP SE, SAS Institute Inc., Palantir Technologies Inc., C3.ai, Inc., and Altair Engineering Inc. compete across different layers of the AI value chain.

Competitive positioning increasingly depends on comprehensive enterprise platforms rather than isolated AI models. Vendors continue expanding partnerships with cloud providers, semiconductor manufacturers, consulting organizations, and enterprise software companies to strengthen deployment capabilities and accelerate customer implementation. Industry-specific AI solutions, proprietary foundation models, enterprise security, responsible AI frameworks, and integrated data platforms remain important areas of differentiation.

Recent Developments

June 2026: Microsoft expanded enterprise AI capabilities across its commercial cloud portfolio with additional governance, agentic AI, and security features. The enhancements support broader enterprise deployment while strengthening compliance and operational oversight.

March 2026: NVIDIA introduced new enterprise AI infrastructure and accelerated computing platforms designed to support large-scale reasoning and generative AI workloads. The launch strengthens enterprise computing capacity for commercial AI applications.

December 2025: Google announced expanded enterprise generative AI capabilities integrated across Google Cloud services, providing organizations with enhanced model customization, security controls, and productivity applications. The development supports wider enterprise adoption.

Regulatory and Policy Environment

AI regulation continues evolving as governments seek to balance innovation with consumer protection, privacy, cybersecurity, and accountability. Data protection legislation, sector-specific compliance requirements, and emerging AI governance frameworks increasingly influence enterprise procurement decisions.

Organizations deploying AI solutions must address transparency, bias mitigation, cybersecurity resilience, model documentation, human oversight, and data governance requirements. Financial services, healthcare, and public sector deployments typically face stricter compliance obligations due to the sensitivity of regulated information.

Government investment programs supporting AI research, semiconductor manufacturing, cloud infrastructure, workforce development, and digital public services continue encouraging commercial adoption. Industry standards relating to AI risk management, cybersecurity, model validation, and responsible AI practices are becoming integral components of enterprise purchasing requirements.

Outlook and Strategic Implications

The AI solutions market is expected to progress from isolated application deployments toward enterprise-wide intelligent operating environments during the forecast period. Organizations are expected to prioritize scalable AI platforms capable of supporting multiple business functions while maintaining governance, cybersecurity, and regulatory compliance.

Investment priorities are likely to emphasize AI infrastructure optimization, enterprise data management, domain-specific foundation models, agentic AI, model lifecycle management, and secure deployment architectures. Procurement strategies are expected to increasingly favor integrated platforms that combine development, deployment, monitoring, and governance capabilities under unified commercial agreements.

Competition will likely intensify around ecosystem development, enterprise partnerships, vertical specialization, and infrastructure efficiency. Vendors capable of demonstrating measurable business outcomes, simplified deployment, regulatory compliance, and lower operating costs are expected to strengthen their competitive positions.

Long-term market performance will depend on enterprise confidence in AI governance, continued availability of advanced computing infrastructure, workforce readiness, responsible regulatory implementation, and sustained investment in data quality. Organizations aligning AI investments with measurable operational objectives and scalable governance frameworks are expected to achieve stronger commercial returns throughout the forecast period.

AI Solutions Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 593.28 billion |

| Total Market Size in 2031 | USD 2,341.73 billion |

| Forecast Unit | Billion |

| Growth Rate | 31.60% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Deployment, Function, Industry Vertical, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Deployment

- Cloud

- On-Premise

By Function

- Machine Learning

- Natural Language Processing

- Computer Vision

- Generative AI

- Forecasting and Optimization

By Industry Vertical

- BFSI

- Healthcare

- Retail and E-commerce

- Manufacturing

- IT and Telecommunications

- Automotive

- Government and Public Sector

- Energy and Utilities

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Spain

- Italy

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits for Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. AI SOLUTIONS MARKET BY DEPLOYMENT

5.1. Introduction

5.2. Cloud

5.3. On-Premise

6. AI SOLUTIONS MARKET BY FUNCTION

6.1. Introduction

6.2. Machine Learning

6.3. Natural Language Processing

6.4. Computer Vision

6.5. Generative AI

6.6. Forecasting and Optimization

7. AI SOLUTIONS MARKET BY INDUSTRY VERTICAL

7.1. Introduction

7.2. BFSI

7.3. Healthcare

7.4. Retail and E-commerce

7.5. Manufacturing

7.6. IT and Telecommunications

7.7. Automotive

7.8. Government and Public Sector

7.9. Energy and Utilities

7.10. Others

8. AI SOLUTIONS MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Deployment

8.2.2. By Function

8.2.3. By Industry Vertical

8.2.4. By Country

8.2.4.1. United States

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Deployment

8.3.2. By Function

8.3.3. By Industry Vertical

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Deployment

8.4.2. By Function

8.4.3. By Industry Vertical

8.4.4. By Country

8.4.4.1. Germany

8.4.4.2. France

8.4.4.3. United Kingdom

8.4.4.4. Spain

8.4.4.5. Italy

8.5. Middle East and Africa

8.5.1. By Deployment

8.5.2. By Function

8.5.3. By Industry Vertical

8.5.4. By Country

8.5.4.1. United Arab Emirates

8.5.4.2. Saudi Arabia

8.5.4.3. South Africa

8.6. Asia Pacific

8.6.1. By Deployment

8.6.2. By Function

8.6.3. By Industry Vertical

8.6.4. By Country

8.6.4.1. China

8.6.4.2. Japan

8.6.4.3. India

8.6.4.4. South Korea

8.6.4.5. Australia

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. IBM Corporation

10.2. Microsoft Corporation

10.3. Google LLC

10.4. NVIDIA Corporation

10.5. Oracle Corporation

10.6. Accenture plc

10.7. Amazon Web Services, Inc.

10.8. SAP SE

10.9. SAS Institute Inc.

10.10. Palantir Technologies Inc.

10.11. C3.ai, Inc.

10.12. Altair Engineering Inc.

Navigate

Trusted by the world's leading organizations