Report Overview

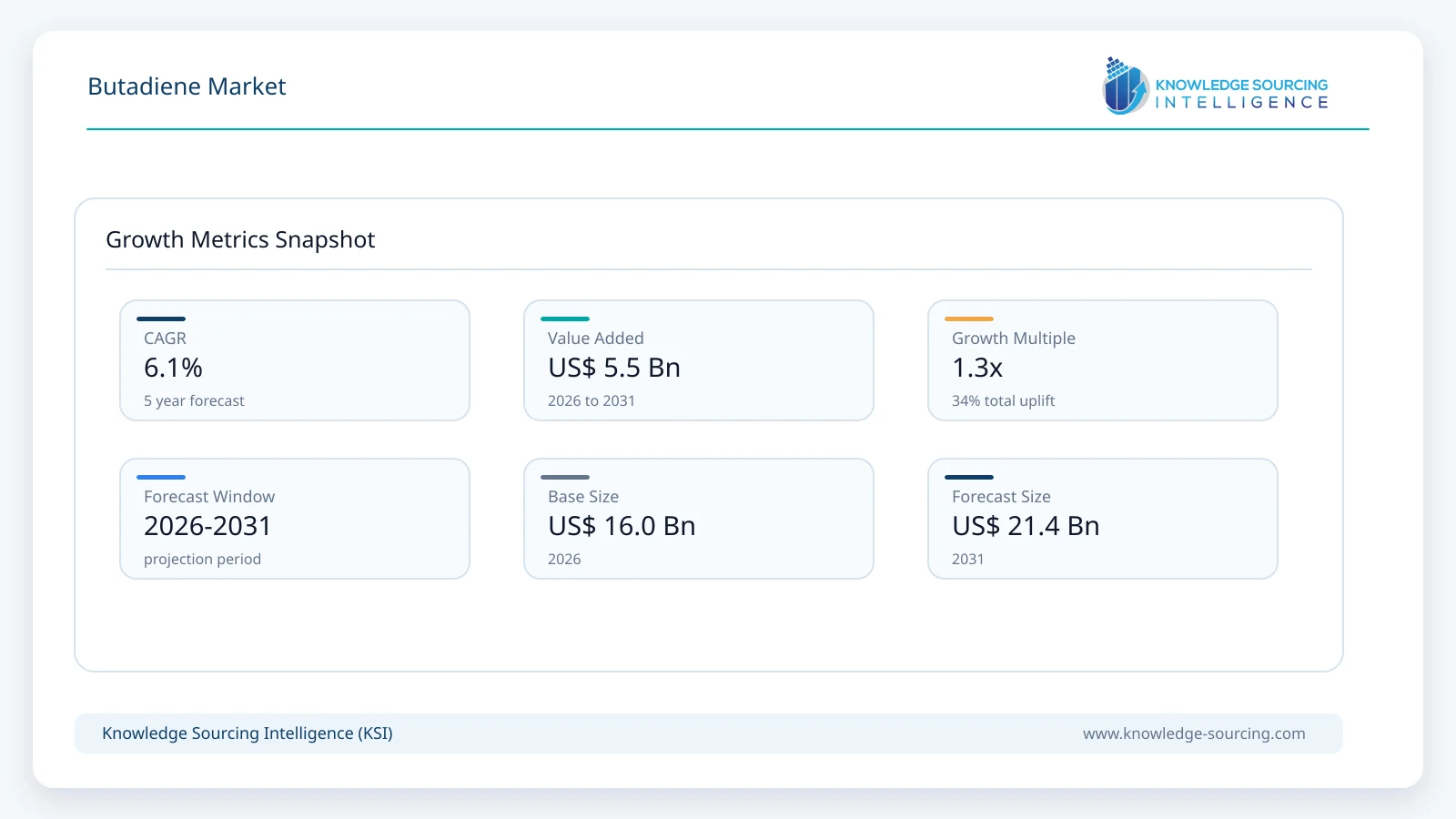

The Butadiene market is forecast to grow at a CAGR of 6.08%, reaching USD 21.44 billion in 2031 from USD 15.96 billion in 2026.

Highlights:

- 1Rising tire production remains the principal demand catalyst for butadiene consumption worldwide.

- 2Styrene-Butadiene Rubber (SBR)represents the largest application segment due to extensive use in passenger and commercial vehicle tires.

- 3Asia Pacific accounts for the largest regional demand because of its concentration of automotive manufacturing and petrochemical production.

- 4Investments in integrated steam crackers and downstream polymer facilities continue improving supply reliability.

- 5Environmental regulations promoting lower rolling resistance tires are supporting demand for high-performance synthetic rubber formulations.

- 6Competition is influenced by feedstock integration, production scale, operational efficiency, logistics capability, and long-term customer relationships.

The butadiene market comprises the production, distribution, and commercial utilization of 1,3-butadiene, a key petrochemical intermediate primarily derived as a co-product of naphtha steam cracking and refinery operations. Butadiene serves as an essential feedstock for synthetic rubbers, engineering plastics, latex products, and specialty chemicals used across automotive, construction, industrial manufacturing, consumer goods, and healthcare industries. Demand is closely linked to downstream polymer production rather than direct consumption, making purchasing decisions highly dependent on automotive manufacturing trends, industrial output, and feedstock availability.

Synthetic rubber manufacturers represent the largest buyers of butadiene because the material is required for producing styrene-butadiene rubber (SBR), polybutadiene rubber (PBR), nitrile rubber (NBR), and other elastomers used in tires, conveyor belts, industrial hoses, footwear, and mechanical goods. Procurement strategies increasingly emphasize long-term supply contracts, feedstock security, consistent product purity, and integration with downstream polymer manufacturing facilities to reduce exposure to raw material price fluctuations.

The automotive industry continues to underpin commercial demand. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production exceeded 92 million units in 2024, sustaining demand for synthetic rubber used in tires, seals, vibration control components, and engineered automotive parts.

Growth in engineering plastics also contributes to market expansion. Acrylonitrile Butadiene Styrene (ABS), produced using butadiene as a principal raw material, is widely used in automotive interiors, electrical equipment, consumer electronics, and household appliances because of its impact resistance, dimensional stability, and ease of processing. Expanding investments in electronics manufacturing and industrial automation continue to support consumption across these downstream industries.

Supply conditions remain strongly influenced by feedstock economics. Because butadiene is primarily recovered during ethylene production, its availability depends on cracker operating rates and the choice of feedstocks such as naphtha or ethane. According to the International Energy Agency (IEA), petrochemicals remain among the largest contributors to future oil demand, highlighting the continuing importance of petrochemical intermediates such as butadiene within global manufacturing supply chains.

Market Drivers

Expansion of Global Tire Manufacturing

The tire industry remains the largest consumer of butadiene because synthetic rubber is an essential raw material for passenger vehicles, commercial vehicles, agricultural machinery, and industrial equipment. Tire manufacturers continue developing products with improved durability, fuel efficiency, and wet-weather performance, increasing demand for premium synthetic rubber grades.

According to the European Tyre and Rubber Manufacturers' Association (ETRMA), replacement tire demand continues to represent a substantial share of global tire consumption, providing a stable source of downstream demand for synthetic rubber manufacturers.

Long-term supply agreements between butadiene producers and synthetic rubber manufacturers remain common to ensure stable production and reduce procurement risk.

Growth in Engineering Plastics Production

Increasing production of consumer electronics, household appliances, electrical components, and automotive interiors continues supporting demand for ABS resins. Manufacturers require butadiene with consistent purity to produce engineering plastics meeting stringent mechanical performance and processing requirements.

Producers are expanding downstream integration with ABS manufacturing facilities to improve value addition and strengthen supply chain resilience.

Rising Industrialization Across Asia Pacific

Asia Pacific continues expanding petrochemical capacity alongside automotive manufacturing, electronics production, and industrial equipment manufacturing. China, India, South Korea, and Japan remain major consumers because integrated refining and petrochemical complexes provide efficient access to butadiene feedstocks.

Investment in refinery expansion and steam cracking capacity improves regional supply while supporting downstream production of synthetic rubber and engineering plastics.

Integration of Petrochemical Value Chains

Large petrochemical companies increasingly integrate refining, steam cracking, butadiene extraction, and downstream polymer production within single manufacturing complexes. Vertical integration improves operational efficiency, reduces logistics costs, enhances feedstock security, and minimizes exposure to market volatility.

Integrated production also enables manufacturers to optimize production planning according to downstream demand patterns and changing feedstock economics.

Market Restraints and Challenges

Feedstock Price Volatility

Butadiene prices are closely linked to crude oil markets, naphtha pricing, and ethylene production economics. Variations in refinery operating rates and cracker feedstock selection frequently influence supply availability and pricing, creating uncertainty for downstream manufacturers.

Synthetic rubber producers increasingly use long-term procurement contracts and diversified sourcing strategies to reduce exposure to raw material volatility.

Dependence on Co-Product Availability

Unlike dedicated petrochemicals, butadiene is largely produced as a co-product during steam cracking. Changes in cracker feedstocks, particularly increased ethane utilization in some regions, can reduce butadiene recovery volumes even when downstream demand remains strong.

Producers continue investing in on-purpose butadiene technologies and extraction efficiency improvements to strengthen supply flexibility.

Environmental and Carbon Reduction Pressures

Petrochemical manufacturers face increasing pressure to reduce greenhouse gas emissions, improve energy efficiency, and comply with evolving environmental regulations. Capital investment in cleaner production technologies, emissions control systems, and energy-efficient operations may increase operating costs while requiring long-term modernization strategies.

Major Segment Analysis

Styrene-Butadiene Rubber (SBR)

Styrene-Butadiene Rubber represents the largest application segment because it serves as the principal synthetic rubber used in tire manufacturing. SBR combines abrasion resistance, durability, processability, and cost efficiency, making it suitable for passenger vehicle tires, truck tires, industrial belts, footwear, adhesives, and various molded rubber products.

Demand is driven primarily by automotive production, replacement tire markets, and expanding transportation infrastructure. Tire manufacturers increasingly require SBR grades that improve rolling resistance, wet traction, and tread durability to meet evolving vehicle performance standards and environmental regulations aimed at improving fuel efficiency.

Competition within this segment centers on product consistency, polymer quality, feedstock integration, manufacturing efficiency, and long-term supply reliability. Producers with integrated butadiene extraction and synthetic rubber production capabilities are better positioned to maintain stable supply, optimize production costs, and respond to changing customer requirements. Continued innovation in tire compounds, coupled with rising global vehicle ownership and industrial manufacturing, is expected to sustain SBR as the leading commercial application throughout the forecast period.

Regional Analysis

Asia Pacific

Asia Pacific represents the largest regional market for butadiene due to its concentration of petrochemical production, tire manufacturing, automotive assembly, and engineering plastics industries. China, Japan, South Korea, India, and Indonesia account for a substantial share of global consumption because they host integrated refining, steam cracking, synthetic rubber, and polymer manufacturing facilities. China remains the dominant consumer owing to its extensive automotive, electronics, and industrial manufacturing sectors. According to the International Energy Agency (IEA), Asia accounts for the majority of global petrochemical capacity additions, reinforcing the region's importance in the butadiene value chain.

North America

North America maintains a strong market position through integrated petrochemical infrastructure and established synthetic rubber production. The United States benefits from extensive refinery and steam cracking capacity supported by a mature chemicals industry. Although greater ethane utilization has altered butadiene recovery volumes in recent years, investments in extraction technologies and downstream integration continue to support reliable supply. Automotive manufacturing, replacement tire demand, industrial equipment production, and ABS resin manufacturing remain important consumption drivers across the region.

Europe

Europe continues to represent a mature butadiene market characterized by advanced manufacturing capabilities and stringent environmental standards. Germany, France, Italy, Spain, and the United Kingdom remain important consumers due to their automotive, industrial machinery, and specialty chemical industries. Procurement decisions increasingly incorporate sustainability objectives, operational efficiency, and supply security. European manufacturers continue investing in energy-efficient production processes while optimizing existing petrochemical assets to remain competitive under evolving carbon reduction policies.

Middle East & Africa and South America

The Middle East continues expanding its petrochemical industry through integrated refinery and chemical complexes supported by abundant hydrocarbon resources. Saudi Arabia has strengthened its position in downstream chemicals through investments in synthetic rubber and petrochemical production. South America, led by Brazil and Argentina, generates demand from automotive manufacturing, industrial rubber products, and construction materials. However, regional consumption remains comparatively smaller because of limited local butadiene production capacity and dependence on imports in several markets.

Competitive Landscape

The butadiene market is characterized by competition among vertically integrated energy and petrochemical companies with upstream refining operations, steam crackers, extraction facilities, and downstream polymer production. Market competitiveness depends on feedstock availability, production scale, logistics capabilities, operational efficiency, long-term customer relationships, and integration with synthetic rubber and engineering plastics manufacturing.

Companies including Lotte Chemical Corporation, JSR Corporation, China Petroleum & Chemical Corporation (Sinopec), ENEOS Holdings, Inc., Zeon Corporation, ExxonMobil Corporation, BASF SE, Shell plc, LyondellBasell Industries Holdings B.V., Reliance Industries Limited, TPC Group, China National Petroleum Corporation (CNPC), and SABIC compete by optimizing production efficiency, expanding downstream integration, and improving supply chain resilience. Producers continue investing in advanced extraction technologies, process optimization, and reliability improvements to maintain consistent product quality while reducing production costs.

Long-term supply agreements with tire manufacturers, synthetic rubber producers, and engineering plastics companies remain an important competitive strategy because they provide demand stability despite fluctuations in feedstock prices. Companies with integrated refining and petrochemical operations generally maintain stronger margins by balancing upstream and downstream market conditions.

Recent Developments

March 2026: Reliance Industries Limited reported continued expansion of specialty chemicals and downstream petrochemical integration through investments at its Jamnagar manufacturing complex. Commercial relevance: Expanded integrated production strengthens feedstock security and improves operational flexibility for downstream chemical manufacturing.

September 2025: SABIC signed additional collaboration agreements to accelerate circular polymer solutions through expanded chemical recycling initiatives. Commercial relevance: Increased circular feedstock development supports long-term sustainability objectives across the petrochemical value chain, including butadiene-derived products.

Regulatory and Policy Environment

The butadiene market operates under regulations governing chemical manufacturing, occupational exposure, industrial emissions, transportation, and environmental protection. Manufacturers must comply with national chemical safety legislation while maintaining product quality and operational safety throughout the supply chain.

In the United States, the Occupational Safety and Health Administration (OSHA) regulates workplace exposure to 1,3-butadiene through occupational exposure limits and comprehensive safety requirements for industrial facilities handling the substance.

Within Europe, 1,3-butadiene is regulated under the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework administered by the European Chemicals Agency (ECHA). Manufacturers and importers must comply with registration, hazard communication, and risk management obligations before placing products on the European market.

Environmental regulations governing industrial emissions, energy efficiency, and greenhouse gas reduction continue encouraging petrochemical producers to modernize manufacturing facilities and improve operational performance. Increasing investment in process optimization, carbon reduction technologies, and circular feedstock utilization is expected to influence capital allocation across the industry during the forecast period.

Outlook and Strategic Implications

The butadiene market is expected to remain closely linked to long-term demand from synthetic rubber, engineering plastics, and specialty chemical industries between 2026 and 2031. Tire manufacturing will continue representing the largest source of consumption as vehicle ownership, freight transportation, and replacement tire demand support steady production volumes.

Investment priorities are expected to focus on integrated petrochemical complexes, modernization of butadiene extraction units, process efficiency improvements, and technologies that reduce emissions while improving production economics. Manufacturers are also likely to evaluate alternative feedstocks and circular chemical production pathways to strengthen long-term supply resilience.

Procurement strategies among downstream manufacturers will increasingly emphasize supply reliability, feedstock diversification, product consistency, and long-term contractual relationships to reduce exposure to commodity price volatility. Companies capable of integrating upstream refining with downstream polymer production are expected to maintain stronger competitive positions through improved cost control and operational flexibility.

Potential risks include fluctuations in crude oil prices, changing cracker feedstock economics, environmental compliance costs, and cyclical demand from the automotive industry. Nevertheless, sustained investment in transportation, industrial manufacturing, infrastructure development, and engineering plastics production is expected to provide stable commercial opportunities for butadiene producers throughout the 2026 to 2031 forecast period.

Butadiene Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 15.96 billion |

| Total Market Size in 2031 | USD 21.44 billion |

| Forecast Unit | Billion |

| Growth Rate | 6.08% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Application, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Application

- Styrene-Butadiene Rubber (SBR)

- Polybutadiene

- Nitrile Rubber

- Styrene Butadiene Latex

- Acrylonitrile Butadiene Styrene (ABS)

- Adiponitrile

- Polychloroprene

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits for Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Market Opportunities

4.4. Porter’s Five Forces Analysis

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Power of Buyers

4.4.3. Threat of New Entrants

4.4.4. Threat of Substitutes

4.4.5. Competitive Rivalry in the Industry

4.5. Industry Value Chain Analysis

4.6. Analyst View

5. BUTADIENE MARKET BY APPLICATION

5.1. Introduction

5.2. Styrene-Butadiene Rubber (SBR)

5.3. Polybutadiene

5.4. Nitrile Rubber

5.5. Styrene Butadiene Latex

5.6. Acrylonitrile Butadiene Styrene (ABS)

5.7. Adiponitrile

5.8. Polychloroprene

5.9. Others

6. BUTADIENE MARKET BY GEOGRAPHY

6.1. Introduction

6.2. North America

6.2.1. By Application

6.2.2. By Country

6.2.2.1. United States

6.2.2.2. Canada

6.2.2.3. Mexico

6.3. South America

6.3.1. By Application

6.3.2. By Country

6.3.2.1. Brazil

6.3.2.2. Argentina

6.3.2.3. Others

6.4. Europe

6.4.1. By Application

6.4.2. By Country

6.4.2.1. Germany

6.4.2.2. United Kingdom

6.4.2.3. France

6.4.2.4. Italy

6.4.2.5. Spain

6.4.2.6. Others

6.5. Middle East and Africa

6.5.1. By Application

6.5.2. By Country

6.5.2.1. Saudi Arabia

6.5.2.2. United Arab Emirates

6.5.2.3. Others

6.6. Asia Pacific

6.6.1. By Application

6.6.2. By Country

6.6.2.1. China

6.6.2.2. Japan

6.6.2.3. India

6.6.2.4. South Korea

6.6.2.5. Australia

6.6.2.6. Indonesia

6.6.2.7. Others

7. COMPETITIVE ENVIRONMENT AND ANALYSIS

7.1. Major Players and Strategy Analysis

7.2. Market Share Analysis

7.3. Mergers, Acquisitions, Agreements, and Collaborations

7.4. Competitive Dashboard

8. COMPANY PROFILES

8.1. Lotte Chemical Corporation

8.2. JSR Corporation

8.3. China Petroleum & Chemical Corporation (Sinopec)

8.4. ENEOS Holdings, Inc.

8.5. Zeon Corporation

8.6. ExxonMobil Corporation

8.7. BASF SE

8.8. Shell plc

8.9. LyondellBasell Industries Holdings B.V.

8.10. Reliance Industries Limited

8.11. TPC Group

8.12. China National Petroleum Corporation (CNPC)

8.13. SABIC

Navigate

Trusted by the world's leading organizations