Report Overview

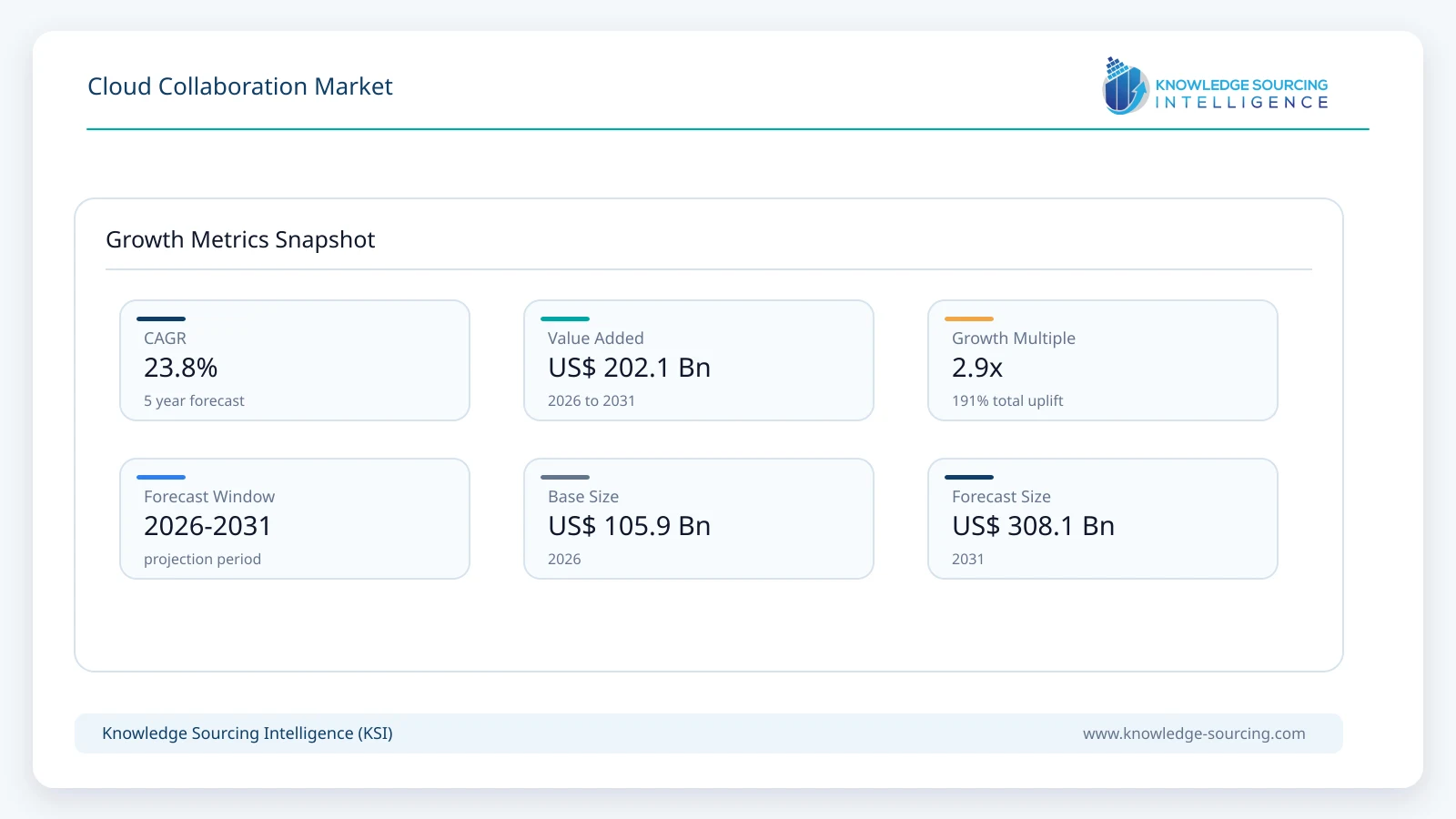

The Cloud Collaboration Market is forecast to grow at a CAGR of 23.80%, reaching USD 308.06 billion in 2031 from USD 105.93 billion in 2026.

Highlights:

- 1Hybrid and distributed workforce models remain the primary commercial catalyst supporting enterprise collaboration software investments.

- 2Public cloud deployment continues to represent the largest adoption segment because of lower infrastructure investment and rapid scalability.

- 3Asia Pacific presents substantial expansion opportunities due to enterprise digitization, cloud infrastructure investment, and expanding technology adoption among SMEs.

- 4Artificial intelligence-enabled productivity features, including meeting summarization and workflow automation, are becoming important purchasing criteria.

- 5Data privacy regulations and industry-specific compliance requirements are encouraging stronger investment in governance, encryption, and identity management capabilities.

- 6Competition increasingly centers on integrated collaboration ecosystems rather than individual communication applications.

The cloud collaboration market comprises software platforms and cloud-based services that enable employees, business partners, customers, and distributed teams to communicate, share content, manage projects, and collaborate in real time through internet-enabled infrastructure. The market includes enterprise communication applications, cloud productivity suites, document collaboration platforms, virtual meeting solutions, workflow collaboration tools, and integrated communication ecosystems delivered through public, private, and hybrid cloud deployment models. Organizations increasingly view cloud collaboration as an operational necessity rather than a discretionary technology investment because business continuity, workforce flexibility, customer responsiveness, and cross-functional coordination depend on seamless digital communication.

Demand is being shaped by structural changes in enterprise operating models. Hybrid work arrangements, geographically dispersed supply chains, multinational project teams, and growing reliance on external contractors require organizations to support secure collaboration beyond traditional office networks. Buyers now evaluate platforms based on integration capabilities, security controls, governance features, scalability, regulatory compliance, artificial intelligence-assisted productivity, and total cost of ownership rather than standalone messaging or conferencing capabilities.

Enterprise procurement decisions increasingly involve multiple business functions instead of only information technology departments. Human resources prioritize employee engagement and workplace flexibility, finance departments seek subscription cost optimization, cybersecurity teams focus on identity management and compliance, while operational leaders emphasize workflow automation and application interoperability. This broader purchasing approach has encouraged vendors to expand unified collaboration ecosystems instead of offering isolated communication products.

Cloud infrastructure expansion has also altered competitive dynamics. Major cloud providers combine productivity software, communication services, identity management, analytics, and AI-powered assistants within integrated enterprise platforms, making ecosystem compatibility an important purchasing consideration. Smaller vendors compete by delivering specialized collaboration experiences, industry-focused capabilities, simplified deployment, or superior customer service.

Technology investments are increasingly directed toward embedded artificial intelligence that summarizes meetings, automates note generation, organizes collaborative content, improves search capabilities, and assists workflow management. Buyers are also placing greater emphasis on zero-trust security architectures, data residency options, encryption standards, and governance features to comply with industry regulations.

The market benefits from continuous enterprise modernization initiatives, although purchasing decisions remain influenced by cybersecurity risks, migration complexity, subscription management, and integration costs associated with replacing legacy collaboration environments.

Market Drivers

Expansion of Hybrid Workforce Operating Models

Organizations continue to redesign workplace strategies around flexible employment models that combine office-based and remote work. This structural shift has created sustained demand for collaboration platforms capable of supporting continuous communication across multiple locations, devices, and business units. Buyers increasingly require persistent messaging, document collaboration, virtual meetings, and project management within unified environments. Vendors respond by integrating communication, scheduling, productivity, and AI-assisted collaboration into single subscription offerings, improving customer retention while expanding recurring revenue opportunities.

Enterprise Cloud Migration and Application Modernization

Many organizations are replacing on-premises productivity software with cloud-native environments to simplify software maintenance and improve scalability. Cloud collaboration platforms fit naturally into broader enterprise modernization programs because they reduce infrastructure management requirements while supporting centralized administration. Procurement decisions increasingly favor solutions capable of integrating with enterprise resource planning, customer relationship management, cybersecurity, and workflow automation platforms, strengthening long-term supplier relationships.

Growing Importance of Cybersecurity and Compliance

Organizations operating within regulated industries require collaboration environments that support encryption, identity verification, audit logging, access controls, and data governance. Financial institutions, healthcare providers, government agencies, and multinational corporations increasingly evaluate collaboration software through risk management frameworks rather than productivity considerations alone. Vendors continue expanding compliance certifications and security capabilities to address procurement requirements and improve competitiveness in regulated sectors.

Artificial Intelligence Enhancing Employee Productivity

Embedded AI functions have become important differentiators across enterprise collaboration platforms. Automatic meeting transcription, intelligent search, document summarization, translation services, task generation, and contextual recommendations reduce administrative workloads while improving information accessibility. Buyers increasingly consider measurable productivity improvements alongside licensing costs, encouraging suppliers to accelerate AI integration throughout their collaboration portfolios.

Market Restraints and Challenges

Data Sovereignty and Regulatory Complexity

Organizations operating across multiple jurisdictions face varying data residency, privacy, and cybersecurity requirements. Financial services, healthcare, education, and public sector institutions often require localized storage and strict governance controls. These regulatory obligations increase deployment complexity and may limit adoption of standardized global collaboration environments. Vendors mitigate these concerns through regional data centers, configurable compliance controls, and localized cloud infrastructure partnerships.

Integration with Legacy Enterprise Systems

Many enterprises continue operating older communication platforms, document repositories, and business applications that cannot be replaced immediately. Integrating modern collaboration platforms with existing technology environments frequently requires customized development, extended implementation timelines, and specialized consulting resources. These additional costs influence procurement decisions and delay migration schedules, particularly among large organizations.

Subscription Cost Management

While cloud delivery reduces capital expenditure, recurring subscription fees have become a growing concern for enterprise buyers managing multiple software-as-a-service contracts. Organizations increasingly evaluate software utilization, license optimization, and return on investment before expanding deployments. Vendors are responding through flexible licensing structures, bundled services, and enterprise-wide pricing agreements designed to improve long-term customer retention.

Cybersecurity Threats Targeting Collaboration Platforms

Collaboration applications have become attractive targets for phishing campaigns, credential theft, ransomware distribution, and unauthorized data access. Security incidents may reduce buyer confidence and increase compliance obligations. Suppliers continue investing in advanced threat detection, multifactor authentication, identity governance, endpoint protection, and security monitoring capabilities to strengthen customer confidence.

Major Segment Analysis

Public Cloud Deployment

Public cloud deployment represents the most commercially significant deployment model because it offers rapid implementation, lower upfront infrastructure costs, and simplified software maintenance. Small and medium-sized enterprises frequently select public cloud environments because they avoid capital investment while providing immediate access to enterprise-grade collaboration capabilities. Large enterprises also continue adopting public cloud services for selected business functions where scalability and operational flexibility outweigh infrastructure ownership.

Buyer requirements extend beyond communication capabilities. Organizations increasingly prioritize uptime guarantees, application integration, cybersecurity certifications, administrative controls, AI-enabled productivity features, and compatibility with existing cloud ecosystems. Procurement teams also evaluate vendor financial stability, geographic infrastructure coverage, and long-term product development strategies before committing to enterprise-wide deployments.

Competition within this segment increasingly depends on platform breadth rather than individual application performance. Vendors differentiate themselves through integrated productivity suites, developer ecosystems, AI functionality, security capabilities, and cross-platform interoperability. Public cloud deployment therefore remains a major contributor to recurring subscription revenue while supporting continuous feature expansion through software updates.

Regional Analysis

North America

North America maintains a leading position due to widespread enterprise cloud adoption, advanced digital infrastructure, high software spending, and early implementation of hybrid work policies. Financial services, technology companies, healthcare organizations, and public institutions continue expanding collaboration investments while emphasizing cybersecurity, compliance, and AI integration. Mature cloud ecosystems also support continuous innovation through partnerships between software providers and hyperscale cloud operators.

Europe

European demand reflects strong regulatory oversight alongside enterprise modernization initiatives. Data privacy regulations encourage organizations to prioritize governance, encryption, and regional data hosting capabilities. Manufacturing, financial services, education, and government agencies represent important customer groups. Although regulatory compliance increases implementation complexity, it also creates opportunities for vendors offering advanced security and localized cloud infrastructure.

Asia Pacific

Asia Pacific demonstrates substantial commercial opportunity due to expanding enterprise digitization, increasing cloud infrastructure investment, and rising adoption among small and medium-sized businesses. Government-supported digital economy initiatives, growing technology sectors, and expanding internet connectivity contribute to stronger collaboration software demand. Cost sensitivity remains important, encouraging suppliers to provide scalable subscription models suitable for organizations of varying sizes.

Middle East and Africa

Digital government initiatives, smart city investments, financial sector modernization, and expanding telecommunications infrastructure support regional demand. Public sector organizations and large enterprises increasingly deploy collaboration platforms to improve operational efficiency and service delivery. Budget limitations, uneven digital infrastructure, and cybersecurity capability gaps remain adoption constraints across several markets.

South America

South American demand continues to strengthen as organizations modernize enterprise information technology infrastructure and adopt cloud-based business applications. Retail, financial services, education, and telecommunications industries increasingly invest in collaboration technologies to improve workforce productivity. Economic uncertainty and currency fluctuations continue influencing enterprise technology budgets, encouraging phased implementation strategies.

Competitive Landscape

Competition is characterized by integrated software ecosystems rather than standalone collaboration products. Microsoft Corporation, Google LLC, Cisco Systems, Inc., Zoom Communications, Inc., Salesforce, Inc. (Slack), GoTo Technologies USA, LLC, and Zoho Corporation Private Limited compete through platform integration, enterprise security, artificial intelligence capabilities, workflow automation, and subscription flexibility.

Product differentiation increasingly depends on unified productivity environments that combine messaging, meetings, document collaboration, workflow management, identity services, and AI-assisted productivity. Strategic partnerships with cloud infrastructure providers, enterprise software vendors, cybersecurity companies, and systems integrators strengthen customer acquisition and long-term platform adoption. Geographic expansion, localized compliance capabilities, and industry-specific solutions remain important competitive priorities across global enterprise markets.

Recent Developments

July 2026: Zoom announced the general availability of Zoom Phone Local Survivability for Zoom for Government, enabling resilient cloud telephony with local call continuity while integrating with existing Cisco, Avaya, Poly, and Microsoft Teams environments.

June 2026: Cisco unveiled Cisco Cloud Control at Cisco Live 2026, a unified cloud platform integrating networking, security, observability, compute, and collaboration with AI agents to simplify enterprise collaboration and IT operations.

March 2026: Zoom introduced an expanded enterprise agentic AI platform at Enterprise Connect 2026, adding AI Companion 3.0 enhancements, custom AI agents, and workflow orchestration across Zoom Workplace, Zoom Phone, and Zoom CX to streamline cloud collaboration.

June 2025: Zoom Communications introduced additional AI Companion enhancements supporting meeting summaries, workflow automation, and collaborative productivity across enterprise users. Commercial relevance: reinforces value beyond video conferencing and supports platform expansion.

May 2025: Microsoft expanded AI-powered collaboration capabilities across Microsoft 365 through broader Copilot enhancements, improving meeting intelligence, document collaboration, and enterprise productivity. Commercial relevance: strengthens integrated AI differentiation for enterprise customers.

Regulatory and Policy Environment

The regulatory environment increasingly influences procurement decisions across the cloud collaboration market. Data protection legislation such as the European Union's General Data Protection Regulation (GDPR), California Consumer Privacy Act (CCPA), sector-specific healthcare privacy requirements, and financial cybersecurity regulations require organizations to implement stronger governance and security controls.

Government cybersecurity frameworks encourage zero-trust architectures, multifactor authentication, encryption, identity management, and continuous monitoring for enterprise collaboration environments. International standards including ISO/IEC 27001, SOC reporting frameworks, and cloud security certifications increasingly form part of enterprise procurement requirements.

Public sector cloud adoption programs across North America, Europe, Asia Pacific, and the Middle East continue encouraging migration toward secure digital workplace solutions while emphasizing compliance, resilience, accessibility, and data sovereignty. Vendors capable of demonstrating regulatory compliance and transparent governance practices maintain stronger competitive positioning during enterprise procurement evaluations.

Outlook and Strategic Implications

Over the forecast period, enterprise purchasing decisions will increasingly prioritize collaboration platforms that combine communication, productivity, workflow automation, cybersecurity, governance, and artificial intelligence within unified cloud ecosystems. Organizations are expected to consolidate software portfolios to reduce operational complexity while improving interoperability across business applications.

Investment priorities will increasingly include AI-assisted productivity, cybersecurity enhancement, cloud-native application integration, analytics, and automation capabilities. Buyers will continue evaluating suppliers based on measurable operational efficiency, regulatory compliance, and long-term platform sustainability rather than communication functionality alone.

Competition is expected to intensify as vendors expand ecosystem partnerships, integrate generative AI into everyday workflows, and strengthen enterprise administration capabilities. Subscription optimization, customer retention, and platform extensibility will remain important commercial priorities.

Potential risks include evolving cybersecurity threats, regulatory changes affecting cross-border data management, integration complexity, and pricing pressure within mature enterprise markets. Nevertheless, organizations seeking greater workforce flexibility, operational resilience, and collaborative efficiency are expected to sustain long-term investment in cloud collaboration platforms, supporting continued innovation across enterprise communication and productivity technologies.

Cloud Collaboration Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 105.93 billion |

| Total Market Size in 2031 | USD 308.06 billion |

| Forecast Unit | Billion |

| Growth Rate | 23.80% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Deployment Model, End-User Industry, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

By End-User Industry

- BFSI

- IT and Telecommunications

- Healthcare

- Retail and E-commerce

- Manufacturing

- Government and Public Sector

- Education

- Media and Entertainment

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Thailand

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

3.2. CXO Perspective

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. CLOUD COLLABORATION MARKET BY DEPLOYMENT MODEL

5.1. Introduction

5.2. Public Cloud

5.3. Private Cloud

5.4. Hybrid Cloud

6. CLOUD COLLABORATION MARKET BY END-USER INDUSTRY

6.1. Introduction

6.2. BFSI

6.3. IT and Telecommunications

6.4. Healthcare

6.5. Retail and E-commerce

6.6. Manufacturing

6.7. Government and Public Sector

6.8. Education

6.9. Media and Entertainment

6.10. Others

7. CLOUD COLLABORATION MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. By Deployment Model

7.2.2. By End-User Industry

7.2.3. By Country

7.2.3.1. United States

7.2.3.2. Canada

7.2.3.3. Mexico

7.3. South America

7.3.1. By Deployment Model

7.3.2. By End-User Industry

7.3.3. By Country

7.3.3.1. Brazil

7.3.3.2. Argentina

7.3.3.3. Others

7.4. Europe

7.4.1. By Deployment Model

7.4.2. By End-User Industry

7.4.3. By Country

7.4.3.1. Germany

7.4.3.2. United Kingdom

7.4.3.3. France

7.4.3.4. Italy

7.4.3.5. Spain

7.4.3.6. Others

7.5. Middle East and Africa

7.5.1. By Deployment Model

7.5.2. By End-User Industry

7.5.3. By Country

7.5.3.1. Saudi Arabia

7.5.3.2. United Arab Emirates

7.5.3.3. South Africa

7.5.3.4. Others

7.6. Asia Pacific

7.6.1. By Deployment Model

7.6.2. By End-User Industry

7.6.3. By Country

7.6.3.1. China

7.6.3.2. Japan

7.6.3.3. India

7.6.3.4. South Korea

7.6.3.5. Australia

7.6.3.6. Indonesia

7.6.3.7. Thailand

7.6.3.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Microsoft Corporation

9.2. Google LLC

9.3. Cisco Systems, Inc.

9.4. Zoom Communications, Inc.

9.5. Salesforce, Inc. (Slack)

9.6. GoTo Technologies USA, LLC

9.7. Zoho Corporation Private Limited

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations