Report Overview

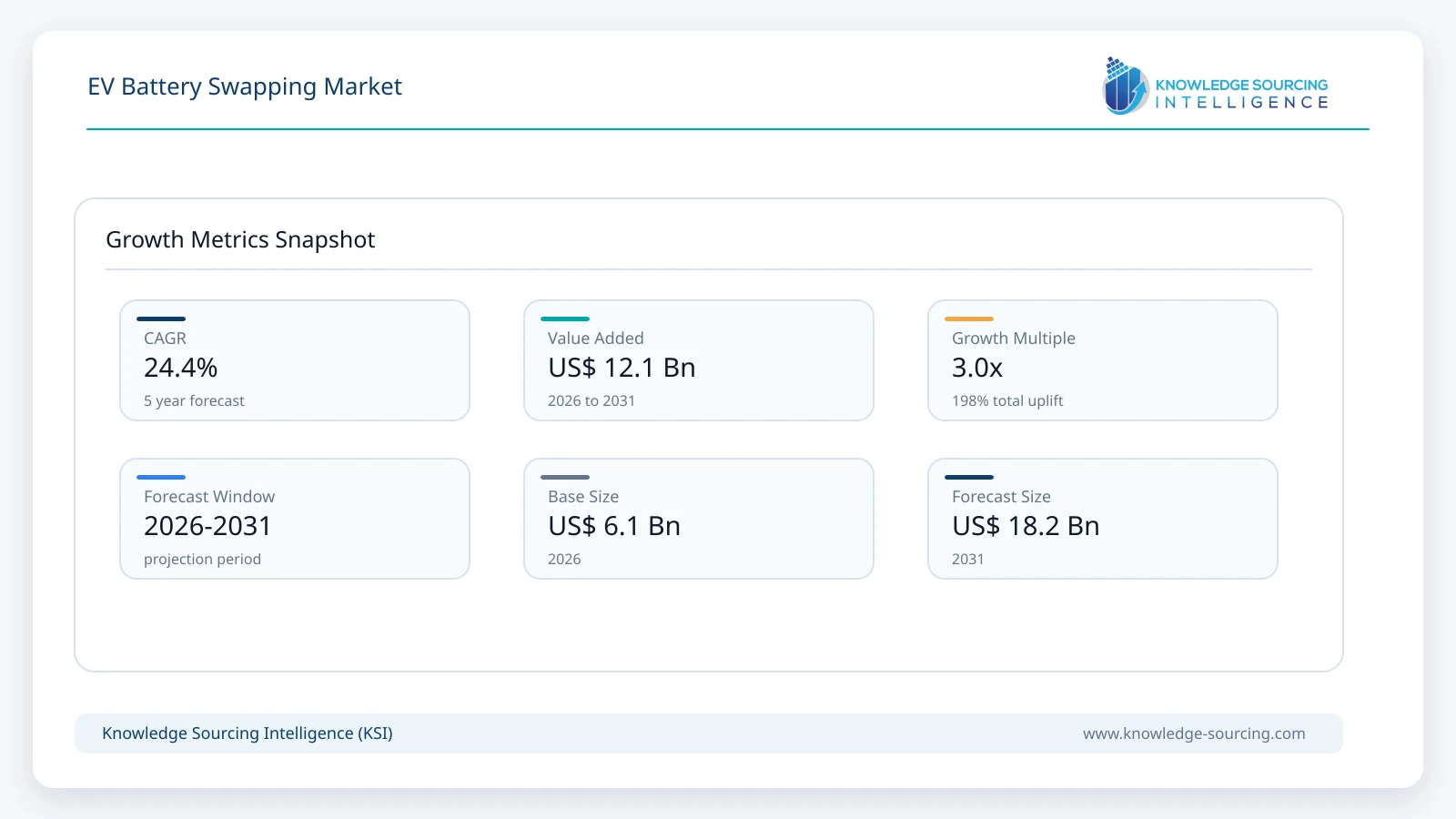

The EV Battery Swapping Market will expand from USD 6.1 billion in 2026 to USD 18.2 billion by 2031, advancing at a 24.4% CAGR during the forecast period.

Highlights:

- 1Decoupling battery costsMarket operators are decoupling battery ownership costs from vehicles via subscription-based Battery-as-a-Service models.

- 2Expanding infrastructure networksInfrastructure providers are aggressively expanding automatic swapping station networks to eliminate consumer range anxiety.

- 3Enforcing compliance rulesGovernment regulators are enforcing strict modular standards and replaceability compliance to achieve national interoperability.

- 4Minimizing commercial downtimeFleet logistics companies are increasingly adopting quick-swapping technologies for minimizing vehicle operational downtime.

The current state of the global Electric Vehicles (EV) battery swap industry is in a phase of technological shift, from a niche technological solutions offering to a key enabler in the energy recharge paradigm for cities. This is mainly because of the “Battery-as-a-Service” (BaaS) model, where the battery cost is not directly linked to the electric vehicle, thus removing the barrier for adoption. The rising grid strain due to quick charging, in a bid to meet the demands of a growing city, is being countered by battery swap technologies, where batteries are charged off-peak in automated stations.

Market dynamics over the last few years show an unmistakable split in adoption trends between the passenger and commercial markets. Passenger car sharing is still largely restricted to China and select European cities. However, the two-three-wheeler market in the Asia Pacific region has shown swift adoption based on the high utilization rate of the last-mile delivery fleet, with industrial-grade demand from a fully functional support ecosystem of standardized battery swap solutions with vehicle downtime of less than five minutes – direct to IC engine refueling.

Increase Infrastructure Rollout: Market leaders, like NIO, have broken the barrier of over 2,480 battery swap stations as of late 2024, with a focused "Battery Swapping in Every County" plan aiming for over 5,000 by the end of 2025 to overcome range issues.

Strategic Joint Ventures and Scaling: In 2024, Sun Mobility and Indian Oil Corporation entered a joint venture regarding the installation of 10,000 battery-swapping stations across 40 cities in India, utilizing 37,000 fueling stations in an attempt to convert refueling points into energy services destinations.

Standardization & Regulatory Compliance: The EU Battery Regulation 2023/1542 requires battery passports & replaceability standards to be met by 2024 & 2025, which compels OEM manufacturers to adopt modular battery designs with a preference for swapping "interoperability" as an ideal solution.

Market Demand: The global market for EV battery swapping is fueled by an increasing demand in commercial vehicle fleets, where lowering downtime is the main driver for demand change in comparison with traditional plugging charging.

Market Dynamics

Market Drivers

The main catalyst driving the electric vehicle battery swapping market is the need to minimize downtime for vehicles, specifically in commercial and fleet applications. In the case of ride-sharing services and logistics companies, having to wait 30 minutes to an hour for the result of any standard DC Fast Charge makes an immediate impact on the utilization rates and, consequently, the revenues generated. Full battery swaps with technology solutions offered by Ample and NIO take less than five minutes. The driving force here, in this case, arises due to the efficiency achieved by enterprises wanting the utilization rate of the vehicles to be at its highest, thus directly requiring an infrastructural solution in battery swaps. According to IEA reports, over 17 million electric cars were sold in 2024; with an increased pool of electric cars on the road, the jam at the respective common charge points makes way for users looking for the certainty that comes with the “swapping” booths.

Secondly, the decoupling of battery costs through the BaaS model has completely changed the nature of demand in this sector. The battery range tends to account for around 30% to 40% of an electric vehicle’s overall price. In this subscription model, companies like Sun Mobility and Gogoro have reduced the entry barrier cost for consumers. The financial impact due to battery deterioration and technology shifts has also been transferred from consumers to companies through these subscription services. In terms of cost, countries like India and Indonesia are extremely price-sensitive, and this factor affects the adoption of electric two- or three-wheelers, as the cost at which these vehicles are sold is an impediment for consumers.

Advances made in the technological front of automation and integration for grids also drive market growth. The new autonomous swapping stations rely on robotic arms to perform the swapping of batteries without the assistance of drivers. The swapping stations act as a form of energy storage technology (BESS), where the batteries can be charged during off-peak times when the electricity prices are lower. This makes it advantageous for the energy sector to invest in swapping technology, considering that this technology offsets the peak demand associated with fast charging.

Finally, the density in urban areas, as well as the absence of home charging stations make battery swapping a necessary alternative. Even in Shanghai, Shenzhen, and Paris, a large number of people live in high-rise buildings that lack parking spaces and charging facilities. Moreover, battery swapping becomes the only feasible option available to people in lieu of scouring the streets in search of available charging stations. Additionally, the zero-emission zones in urban areas make EV adoption compulsory as there is a lack of charging facilities in their residential areas.

Market Restraints & Opportunities

The market will have a tough time standardizing the batteries and making them compatible with each other. At the moment, most manufacturers have standardizable proprietary shapes and cooling systems, so the use of the swapping station will be restricted to a certain brand. But it also poses a great chance to third-party energy aggregators who may develop “modular” batteries that can be adapted to most vehicles.

Supply Chain Analysis

The supply chain for battery swapping is highly centralized, with China accounting for a significant share of global battery production and refining as of 2025. Key hubs in East Asia dominate the manufacturing of the automated robotic components and the high-density lithium-ion cells required for swapping. Logistical complexities arise from the necessity of maintaining a battery inventory required to ensure a charged pack is always available at every station. This creates a dependency on a steady supply of lithium, cobalt, and nickel, making the market sensitive to mineral price volatility.

The imposition of trade tariffs between 2024 and 2025 has introduced substantial headwinds for the global expansion of battery swapping hardware. Specifically, the US and EU have implemented increased duties on Chinese-manufactured automated battery exchange mechanisms and lithium-ion cells.

In the supply chain, these tariffs have disrupted the cost-efficiency of the BaaS model. Since the profit margins of subscription services are thin, any increase in the capital cost of the "battery buffer" or the swapping station itself directly extends the break-even period for operators. Consequently, in markets with high tariffs, there is a visible shift toward prioritizing manual swapping or lower-cost station designs to maintain price parity for the end-user.

Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

|---|---|---|

European Union | EU Battery Regulation 2023/1542 | Mandates "Battery Passports" by 2027 and enhances replaceability requirements. This forces manufacturers to design modular, easily accessible battery compartments, directly facilitating the technical feasibility of swapping for third-party providers. |

China | MIIT / 2025 Vehicle Trade-In Policy | Provides subsidies up to RMB 20,000 for scrapping old vehicles for new EVs. Specific technical standards for swapping stations are incentivized to ensure national interoperability, driving the "Battery Swapping in Every County" initiative. |

India | PM E-DRIVE Scheme (Sept 2024) | Allocates INR 10,900 crore to support EV infrastructure. Specifically includes "Battery Swapping" under its interoperability guidelines, providing financial incentives for operators to deploy stations in high-density urban corridors. |

Key Developments

June 2026: Spiro announced it had secured US$215 million in equity financing to accelerate expansion of its battery-swapping infrastructure, local manufacturing, and electric mobility operations across Africa, including entry into new markets.

June 2026: Spiro confirmed that the investment will expand its network beyond 2,500 smart battery-swapping stations supporting over 100,000 electric vehicles, while adding solar-powered swap stations and strengthening battery lifecycle capabilities across African markets.

June 2026: Reliance New Energy confirmed preparations to roll out battery-swapping services for electric two-wheelers serving India's logistics and delivery sector, supporting commercial fleet electrification and expanding the country's EV energy infrastructure.

May 2026: VinFast confirmed that its Indonesian battery-swapping ecosystem would support the newly introduced e-motorcycles through flexible Battery-as-a-Service (BaaS) and battery-swapping models, strengthening its regional EV infrastructure rollout following the product launch.

Market Segmentation

By Vehicle Type: Two-Wheelers

The two-wheeler segment represents the most mature and high-volume portion of the battery swapping market, particularly in the Asia-Pacific region. Demand in this segment is driven by the extreme price sensitivity of the consumer base and the high utilization of gig-economy delivery riders. Unlike passenger cars, two-wheeler batteries are lightweight (typically 10-12 kg), allowing for manual swapping without the need for expensive robotic infrastructure. This reduces the capital expenditure for station operators and allows for the deployment of small, cabinet-sized "swap points" at convenience stores and fuel stations. In Taiwan, Gogoro has demonstrated that this model can achieve near-total market penetration for urban transit, as the speed of a manual swap (under 30 seconds) is superior to any existing charging technology.

By Service Model: Battery-as-a-Service (BaaS)

The BaaS model is the dominant demand catalyst for the battery swapping market because it addresses the "total cost of ownership" (TCO) concerns of both retail and commercial buyers. Under this model, the consumer purchases the vehicle "body" while the battery is provided via a monthly subscription or pay-per-use fee. This eliminates the risk of battery degradation, a major concern in the resale market, as the operator is responsible for maintaining the health and end-of-life recycling of the cells. For commercial fleets, BaaS provides a predictable operating expense (OPEX) instead of a large upfront capital expense (CAPEX), allowing logistics companies to scale their electric fleets more aggressively. This financial structure is particularly effective in emerging markets where credit availability for high-cost EVs is limited.

Regional Analysis

North America Market Analysis

In the United States, demand for battery swapping is primarily concentrated in the commercial fleet and car-sharing sectors rather than the private passenger market. The prevalence of single-family homes with private garages makes home charging the primary replenishment method for individual owners, reducing the retail demand for swapping. However, for high-mileage fleets in urban centers like San Francisco and New York, the speed of swapping is a competitive necessity. Companies like Ample have targeted this demand by partnering with ride-hail operators to provide rapid energy replenishment. Growth in the US is currently constrained by a lack of national standardization and the impact of tariffs on imported hardware, though the Inflation Reduction Act (IRA) offers potential incentives for domestic station manufacturing.

South America Market Analysis

The Brazilian market is marked by the "push" for electric two- and three-wheelers for the last-mile distribution of logistics in the urban areas of São Paulo. This is driven chiefly by the high fuel price that leads to additional costs due to the "last mile" problem in urban areas, which has become costly for gas-powered vehicles that require extensive infrastructure for fueling. Swapping is considered an answer for the power infrastructure problem, which is inadequate in the older districts where improvements are not economical for the installation of high-speed charging points.

Europe Market Analysis

The French market is an important driver of growth in battery swapping in the European region, thanks to the French government's very ambitious decarbonization policy and the extension of "Low Emission Zones" in Paris, Lyon, and other cities. Micro-mobility and small cars are in high demand in the French market. The French market also acts as a pilot project in the passenger car battery replacement market, as NIO has launched its first "Power Swap Stations" to facilitate its entry in this market. The government's encouragement of circular economy projects, such as the "EU Battery Passport," urges French citizens to opt for battery swapping, as this also guarantees sustainability, an important factor in France.

Middle East and Africa Market Analysis

The Saudi Arabian market is turning out to be an important hub for EV-infrastructure development under the umbrella of ‘Vision 2030’. The government is encouraging an increasing adoption of EVs in an attempt to cut down on oil consumption within the country itself, presenting an interesting demand trend for high-performance swapping solutions that are resilient against high temperatures. Here, it is more about autonomous and temperature-controlled swap stations that are capable of handling battery thermal management in a desert environment. Smart cities like ‘NEOM’ are being developed with battery swap technology embedded within their automated transport system infrastructure.

Asia Pacific Market Analysis

China currently leads in battery swapping. This is because there are overall national standards as well as full subsidies from the government. This segment is supported by high two-wheeler swapping as well as a growing car swapping network. Most of the players in the battery swapping market in China are taking advantage of government policies that include swapping stations in the category of "new infrastructure," just like 5G communications, as well as high-speed railways. This is further supported by the "Battery Swapping in Every County" policy. This will ensure that EVs can move along the expressways all over the country. This is further assisted by overall control over the battery chain in China. This further enables China to install battery swapping in the cheapest manner worldwide.

List of Companies

NIO

Gogoro

Ample

Sun Mobility

Battery Smart

Aulton

KYMCO

Tycorun

VoltUp

Scin Power

The competition in the EV battery-swap market is characterized by a combination of specialized tech players and overall energy companies. The key strategic area that is being focused on at present is vertical integration, where a firm could control both design and station hardware, as well as an ecosystem strategy that focuses on developing an industry-wide common standard.

NIO

NIO is a leader in the passenger car battery swap industry. The business positioning strategy of the company is formulated through its "Power Grid" ecosystem, which encompasses home charging, mobile charging van solutions, in addition to its flagship Power Swap Stations (PSS) offering.

Gogoro

Gogoro is the world’s largest player in the market for swapping in two-wheelers. Gogoro’s “Gogoro Network” is an open system in which different manufacturers (like Yamaha and Suzuki) have designed their products to be compatible with Gogoro’s branded standardized batteries. Gogoro’s battery swapping business model has helped the company acquire more than 90% market share for electric two-wheelers in Taiwan.

Sun Mobility

Sun Mobility's main area of focus for the Indian markets, as well as the emerging markets, is the “Battery as a Service” model. The competitive edge for the company in the electric vehicle industry is its “Smart Battery” concept that could work effectively for two-wheelers, three-wheelers, or small four-wheelers.

EV Battery Swapping Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 6.1 billion |

| Total Market Size in 2031 | USD 18.2 billion |

| Forecast Unit | USD Billion |

| Growth Rate | 24.4% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Vehicle Type, Service Model, Battery Swapping Station, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Vehicle Type

By Service Model

By Battery Swapping Station

By Battery Type

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. EV BATTERY SWAPPING MARKET BY VEHICLE TYPE

5.1. Introduction

5.2. Passenger Cars

5.3. Commercial Vehicles

5.4. Two-Wheelers

5.5. Three-Wheelers

6. EV BATTERY SWAPPING MARKET BY SERVICE MODEL

6.1. Introduction

6.2. Battery-as-a-Service (BaaS) / Subscription Model

6.3. Pay-Per-Use Model

7. EV BATTERY SWAPPING MARKET BY BATTERY SWAPPING STATION

7.1. Introduction

7.2. Manual Battery Swapping Station

7.3. Autonomous Battery Swapping Station

8. EV BATTERY SWAPPING MARKET BY BATTERY TYPE

8.1. Introduction

8.2. Lithium-Ion

8.3. Lead Acid

8.4. Others

9. EV BATTERY SWAPPING MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. USA

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. United Kingdom

9.4.2. Germany

9.4.3. France

9.4.4. Spain

9.4.5. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. UAE

9.5.3. Others

9.6. Asia Pacific

9.6.1. China

9.6.2. India

9.6.3. Japan

9.6.4. South Korea

9.6.5. Indonesia

9.6.6. Thailand

9.6.7. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. NIO

11.2. Gogoro

11.3. Ample

11.4. Sun Mobility

11.5. Battery Smart

11.6. Aulton

11.7. KYMCO

11.8. Tycorun

11.9. VoltUp

11.10. Scin Power

12. APPENDIX

12.1. Currency

12.2. Assumptions

12.3. Base and Forecast Years Timeline

12.4. Key benefits for the stakeholders

12.5. Research Methodology

12.6. Abbreviations

Navigate

Trusted by the world's leading organizations