Report Overview

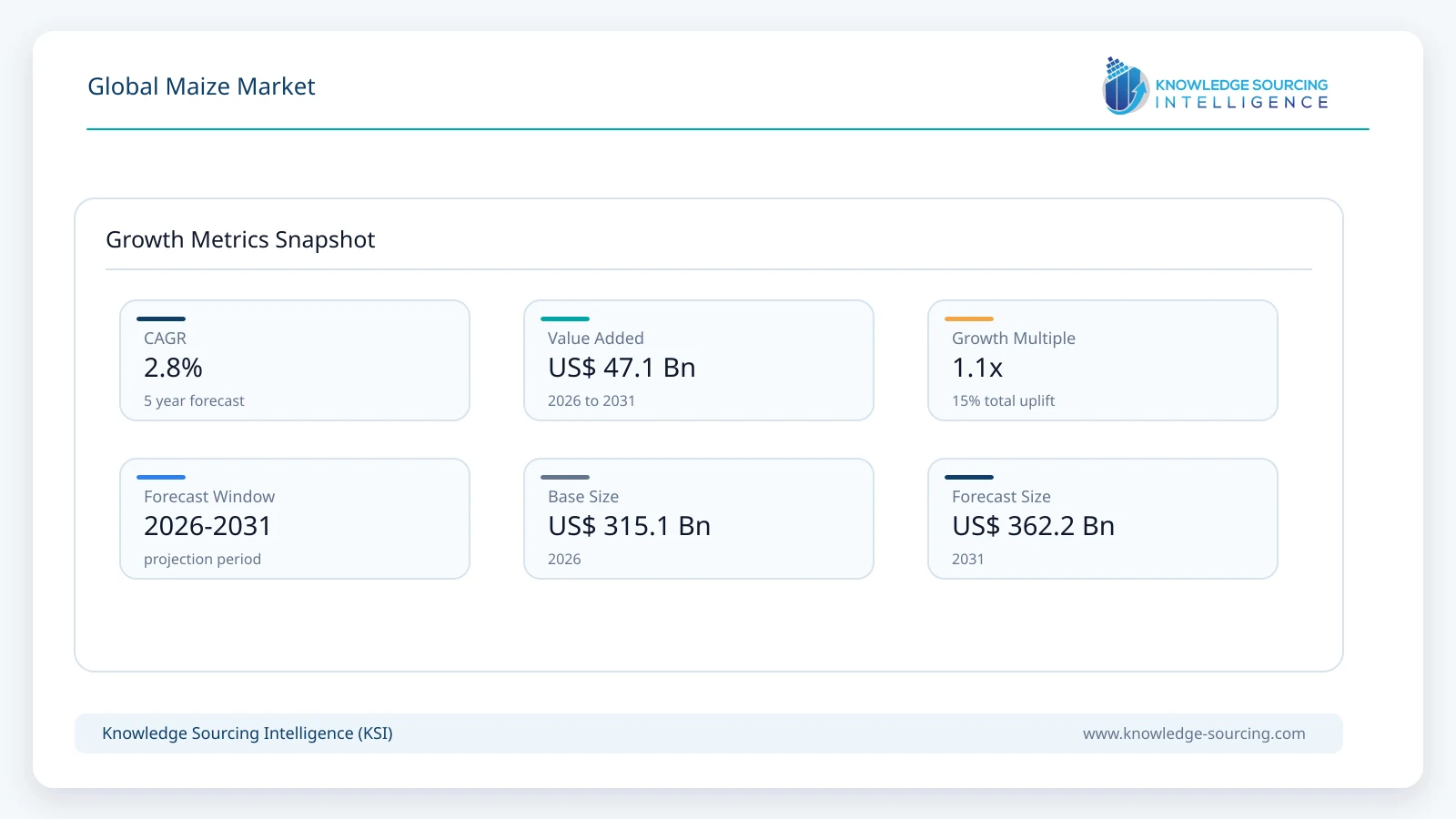

The Global Maize Market is expected to grow at a 2.83% CAGR, increasing to USD 362.2 billion by 2031 from USD 315.1 billion in 2026.

Highlights:

- 1Largest End-User (Animal Feed)The livestock sector accounts for the majority of global maize consumption, where the expansion of poultry and swine production in the Asia-Pacific region directly necessitates higher import volumes of high-protein maize varieties to sustain commercial growth.

- 2Regulatory Impact (EUDR)The European Union Deforestation Regulation (EUDR) mandates rigorous due diligence and geolocation mapping for maize imports, forcing a structural shift in supply chains toward certified "deforestation-free" origins and increasing compliance costs for exporters in South America and Southeast Asia.

- 3Regional Leader (North America)The United States remains the dominant global producer and exporter, contributing roughly 31% of global production; this concentration centers global price discovery on the U.S. Corn Belt’s weather patterns and domestic ethanol policy.

- 4Technology Transition (Biotechnology)The adoption of multi-trait genetically modified (GMO) hybrids is accelerating, with new approvals for four-way herbicide tolerance and drought-resistant traits directly increasing the demand for premium seeds that guarantee yield stability under volatile climatic conditions.

- 5Pricing Sensitivity (Input Costs)The market exhibits extreme sensitivity to natural gas prices, as nitrogen-based fertilizers represent a significant portion of production costs; this creates a direct correlation between energy price spikes and maize price floors, impacting profit margins for global grain processors.

The Global Maize Market forms the core of the global agricultural and food economy. It includes a large value chain that extends from seed production and farming to processing, trading, and industrial applications. Maize, which is also called corn, is one of the most widely grown cereal crops in the world. It continues to be a primary food source, an animal feed component, and a key raw material for various industries like biofuels, starches, sweeteners, and pharmaceuticals.

Leading manufacturing nations in 2024–2025 include Argentina (4% share), the United States with 31%, China with 24%, Brazil with 11%, and the European Union with 5% of the world's corn production. Additionally, the need for eco-friendly farming methods, easily traceable supply chains, and clean energy sources is changing the way maize is grown and processed in different parts of the world. The food division utilizes maize as a versatile raw material for products like cornmeal, snacks, cereals, and sweeteners, whereas the industrial side is using maize for bioplastics and ethanol.

On the other hand, the market is subjected to challenges such as climate variability, unstable commodity prices, and geopolitical disruptions that impact global trade routes and the export of grains.

The global maize market is governed by several regulatory frameworks and policies that are primarily aimed at maintaining food security, promoting sustainability, and ensuring fair trade. Some of the major regulations include the U.S. Farm Bill, which regulates maize subsidies and biofuel mandates, the European Union Common Agricultural Policy (CAP), which manages maize production and ensures compliance with environmental laws, and China’s Grain Security Law that monitors domestic reserves and imports. Additionally, there are internationally accepted standards from organizations, such as the Codex Alimentarius Commission and the World Trade Organization (WTO), which establish regulations for maize safety, labeling, and trade practices.

Furthermore, the policies enacted to address the climate crisis, such as the EU Renewable Energy Directive (RED II) and the U.S. Renewable Fuel Standard (RFS), are also determining the demand for maize for bioethanol production, thereby influencing global supply chains and pricing dynamics.

Key players in the Global Maize Market are top agribusiness and seed companies such as Archer-Daniels-Midland Company (ADM), Cargill, Incorporated, Bunge Global SA, Bayer AG, Corteva Agriscience, Syngenta AG, KWS SAAT SE & Co. KGaA, Limagrain Group, Bühler Group, Ingredion Incorporated, Roquette, Louis Dreyfus Company. These organizations influence the market through their extensive global supply chains, cutting-edge seed genetics, processing methods, and the wide range of maize-based products in their portfolios, and are primary drivers of innovation, sustainability, and competition in the entire value chain.

The maize market is expected to grow consistently during the next few years, largely due to technological innovation, broadening industrial applications, and the global shift towards eco-friendly agricultural systems and the use of renewable energy.

Market Dynamics

Market Drivers

Increasing need for sources of animal protein

Global livestock consumption has increased as a result of urbanization, growing affluence in emerging countries, and population expansion. The consumption of milk, meat, and eggs, which is rising at the cost of staple foods, has been proven to be closely connected with income levels and population increase. Hence, to fulfill the growing demand for meat and high-value animal protein, pressure on the livestock business has increased over the past several years. For instance, to increase milk output, dairy producers in India are progressively substituting crossbred cows and buffaloes for native, low-yielding dairy bovine breeds. One of the main components of practically all forms of compound feed for animals, including ruminants, poultry, swine, and aquaculture, is maize. Hence, the worldwide trade and market for maize are projected to be driven by the rising need for sources of animal-based protein.

The growing interest in products derived from maize as alternatives to conventional snacks.

Businesses that offer a healthy breakfast plan made up of ready-to-eat goods have dramatically increased due to consumer demand. There has also been a move towards healthier diets to lower cholesterol and manage blood sugar levels. This has led to a rise in the demand for maize. Maize is also utilized in various forms for home-cooked meals and restaurant dishes. A rising number of fast food restaurants are including maize on their menus.

Rising demand from the animal feed industry

According to the United States Department of Agriculture (USDA), maize remains the predominant feed grain and is used in over 95 percent of total feed grain produced and consumed in the United States. This remains true since maize is the primary energy source for feed manufacturing for poultry, beef, and hogs. The USDA Economic Research Service (ERS) Feed Grains Market Outlook (August 2025) predictions indicate a 250 million bushel increase for the 2025/26 marketing year in feed and residual use, representing strong feed demand required by stable livestock production. For total feed demand, the USDA Foreign Agricultural Service (FAS) indicates that in China, demand in 2024/25 is estimated at about 286.5 million metric tons, with maize remaining the most important component of total feed demand due to cost-effectiveness and high energy density compared to alternatives.

In India, demand for poultry feed showed a steady increase in demand for maize or corn. Total Indian maize consumption is now about 60% for domestic poultry feed. In developing regions, due to rising meat and dairy consumption and industrialization of livestock production, feed demand continues to grow as a trade factor, resulting in maize demand. Maize utilization for feed is expected to continue growing in the long term, which will support the expansion of maize trade. Additionally, maize utilization for feed is becoming established as a key component of overall maize demand.According to the United States Department of Agriculture (USDA), the harvested area for maize in 2025 is projected at 88.7 million acres, marking an increase of nearly 2 million acres from the previous year. The average yield is estimated at 188.8 bushels per acre, resulting in a total production forecast of 16.7 billion bushels. This growth reflects strong supply conditions supporting the U.S. animal feed industry, which remains the largest consumer of domestic maize. The increased production helps stabilize feed availability for livestock and poultry sectors, reinforcing maize’s central role in sustaining feed demand nationwide.

Market Restraints and Opportunities

Yield Volatility from Climate Extremes: Increasing frequencies of drought and high-heat events in key production zones (e.g., the U.S. Midwest and Brazil’s Mato Grosso) pose a structural risk to supply reliability, forcing industrial buyers to diversify sourcing and invest in resilient supply chain technologies.

Geopolitical Trade Barriers: The shift in China’s sourcing strategy, diversifying away from U.S. maize in favor of Brazilian and Argentine origins through new phytosanitary protocols, restructures global trade flows and forces traditional exporters to seek new markets in Southeast Asia and Africa.

Opportunity in Specialty and Organic Segments: Rising consumer demand for non-GMO and organic-certified livestock products in Europe and North America creates high-margin opportunities for identity-preserved (IP) maize supply chains that command a premium over bulk commodity grades.

Sustainable Aviation Fuel (SAF) Potential: The emerging market for Alcohol-to-Jet (ATJ) technology represents a significant future demand channel for maize-based ethanol, as airlines seek scalable feedstocks to meet carbon-neutrality commitments by 2050.

Raw Material And Pricing Analysis

The Global Maize Market, as a physical agricultural commodity, is deeply influenced by the pricing of its primary production inputs: nitrogen fertilizers, diesel fuel, and proprietary seed genetics. Nitrogen fertilizers, primarily urea and anhydrous ammonia, are synthesized from natural gas, making maize prices highly sensitive to fluctuations in the global energy complex. In the 2024-2025 period, regional pricing variations were stark; for instance, U.S. maize prices saw volatility due to Mississippi River transport disruptions, while Argentine prices declined following the government’s reduction of export duties from 12% to 0%. Margin management strategies for global processors like ADM and Bunge now rely heavily on integrated supply chain ownership and geographic hedging to mitigate these input price spikes and the inherent energy intensity of drying and transporting bulk grain.

Supply Chain Analysis

The global maize supply chain is characterized by a high degree of production concentration, with the "Big Four" (United States, China, Brazil, and Argentina) accounting for the majority of total output. This concentration creates significant regional risk exposure, where localized weather events or political shifts, such as China’s drive for self-sufficiency and its 2025 tightening of grain imports through bonded zones, can instantaneously disrupt global trade balances. Transportation constraints remain a perennial bottleneck; the reliance on barge traffic in the U.S. and truck-based logistics in Brazil’s interior creates "basis" volatility, where the local price at the farm gate differs significantly from the international FOB price.

Manufacturing and processing are increasingly integrated near production hubs to minimize transportation costs. Large-scale wet-milling facilities, which convert maize into starch, sweeteners, and ethanol, are highly energy-intensive and typically located near both corn production and cheap energy sources. Furthermore, the supply chain is adapting to new hazard classifications and environmental standards, particularly regarding mycotoxin management in humid climates, which necessitates sophisticated testing and sorting infrastructure at every transfer point from the farm to the end-user

Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

United States | USDA / Renewable Fuel Standard (RFS) | Mandates minimum volumes of renewable fuels, providing a guaranteed demand floor for roughly 30-40% of the U.S. corn crop for ethanol production. |

Europe | European Food Safety Authority (EFSA) / Green Deal | Imposes strict limits on chemical pesticide residues and restricts the cultivation of most GM maize varieties, driving demand for non-GMO and organic imports. |

China | National Development and Reform Commission (NDRC) | Manages strategic grain reserves and import quotas (TRQs) to ensure domestic food security, directly influencing global trade volumes and price parity. |

Brazil | Ministry of Agriculture (MAPA) | Provides subsidized credit and insurance for "Safrinha" corn production, encouraging the expansion of double-cropping systems in the Cerrado region. |

International | Cartagena Protocol on Biosafety | Governs the transboundary movement of Living Modified Organisms (LMOs), impacting the documentation and handling requirements for global GM maize shipments. |

Key Developments

May 2026: Bayer AG reported strong first-quarter 2026 Crop Science growth, driven by higher corn seed and traits sales across North America, Europe, the Middle East, Africa, and Latin America, reflecting continued expansion of its maize seed portfolio.

May 2026: Corteva Agriscience announced the creation of Vylor, its planned Agriculture Productivity business, highlighting the world's largest seed production network and industry-leading corn genetics and seed portfolio to accelerate innovation for maize growers.

March 2026: Bayer Crop Science advanced commercialization of its Preceon® Smart Corn System, bringing its short-stature maize technology closer to U.S. rollout to improve crop resilience, management flexibility, and yield protection under challenging field conditions.

Market Segmentation

By Application: Animal Feed

By Application, the global maize market is segmented into Food and Beverage, Animal Feed, Biofuel and Ethanol, Pharmaceutical, Paper and Pulp, and Others. Animal feed is the largest industrial usage of maize internationally and the largest demand category in coarse grain consumption; the rising production of livestock and poultry directly leads to increased purchases of maize by feed formulators and integrators. The energy values, starch profile, and relative economic aspects make maize the prime base ingredient of commercial rations, ranging from intensive poultry farming operations to extensive cattle operations. As a result, feed mills and integrators purchase maize in bulk during predictable seasonal cycles. The regional demand situation is important. In the United States, increasing herd sizes and improvements in feed utilization efficiency ensure stable domestic demand for maize, despite competition from ethanol and exports. USDA figures, both projections and monthly outlooks, indicate that feed and residual use will be a principal category in the maize disappearance figure.

On the supply side, changes in government production forecasts and intervention policies (such as stockpiling, minimum purchase prices, and import controls) influence the purchasing behavior of buyers. As official supply forecasts tighten, large feed buyers use forward purchase contracts to maintain their positions. When prices or policy signals render maize relatively expensive, buyers switch rations, substituting maize with alternative grains. Additionally, the global outlook for coarse grains indicates a year-on-year increase in their consumption, largely driven by feed consumption. As a result, feed buyers will remain a major source of stable demand for maize. The procurement departments, feed millers, and integrators view maize as a strategic raw material. They closely monitor government supply reports, seasonal yield reports, and national consumption ratios of feed to determine the most propitious time to purchase and effectively manage their risks.

According to the USDA’s Foreign Agricultural Service, the European Union’s total corn supply increased from 86,626 thousand metric tons in 2024 to 86,826 thousand metric tons in 2025, reflecting a slight recovery in availability. This improvement stems from stable domestic production and moderate import growth to support feed manufacturing needs. Maize remains a primary feed grain across the EU, particularly in the livestock and poultry sectors, due to its high energy content and nutritional value. The consistent rise in supply strengthens the animal feed segment by ensuring steady input availability, supporting livestock productivity, and contributing to the overall stability of the regional maize market.

By Cultivation Method: Genetically Modified (GMO)

Genetically modified (GMO) maize dominates the production landscapes of the world’s leading exporters, including the United States, Brazil, and Argentina. The demand for GMO varieties is driven by the operational necessity of managing large-scale monocultures efficiently. Stacked-trait seeds, combining insect resistance (Bt traits) with multiple herbicide tolerances, allow for reduced tillage and lower labor requirements, which are critical in regions facing agricultural labor shortages. While certain markets, notably the European Union and parts of Africa, maintain strict non-GMO preferences for human consumption, the global industrial and feed segments are structurally dependent on the yield stability and cost-efficiencies provided by GMO technology.

By Type: Dent Maize

Dent maize (Zea mays indentata) is the most widely cultivated type globally, primarily due to its high starch content and suitability for both industrial processing and animal feed. The "dent" in the kernel, caused by the unequal drying of hard and soft starch, facilitates easier grinding and processing in wet-milling facilities. This type's operational advantage lies in its versatility; a single harvest of dent maize can be diverted into ethanol production, high-fructose corn syrup, or livestock rations based on real-time market signals. Its dominance is supported by the extensive R&D pipelines of major seed companies, which prioritize dent maize for the introduction of new biotechnological traits.

Regional Analysis

North America: the US Market Analysis

The increase in the production of Biofuel, which is Ethanol in the United States, is a major driver for the demand for maize, with about 40 percent, i.e., about 5 billion bushels, in the last 10 years, according to the data from the U.S. Department of Agriculture (USDA) reported in February 2023. The growing biofuel production and export are also being fueled by stringent country policies and regulations, such as the Renewable Fuel Standard Program Implementation, and emerging low-carbon fuel incentives, along with state low-carbon fuel standards across the region. They are fueling the maize production and demand.

Moreover, maize is also utilized as the country’s primary feed grain, accounting for a considerable share of the total feed grain consumption and production. This is promoted by the expansion of the livestock sector in the country, along with growing domestic and global consumption of livestock products such as meat, eggs, and dairy.

The country is experiencing a rise in meat consumption, which is expected to remain high due to population growth, thereby increasing the feed demand in the coming years. According to OECD data, poultry meat consumption in the country was 34.9 kilograms per capita, while pork and beef and veal meat consumption were 21.8 and 23.3 kilograms per capita in 2024. This represents a steady growth in domestic consumption, which will promote maize production and demand in the region.

The country ranks first in maize production, accounting for 30.6 percent of the global production in 2024, as per USDA data. Maize production in 2024/2025 was 377.63 million metric tons, an increase from 346.7 million metric tons in 2022/2023. This is largely utilized in feed consumption and ethanol production in the country.

In addition to this, the maize production in the country is majorly concentrated in the corn belt region, which includes states like Iowa and Illinois, representing about 33 percent of the country's crop production. Besides the application of maize in animal feed and ethanol production for biofuel, it is also utilized in the food and other industrial sectors in the form of oils, sweeteners, and starches.

Furthermore, the significant export demand for maize, which accounts for 10-15 percent of the total production, with main markets including Mexico, China, and Japan, also promotes the market. The export is expected to remain consistent due to a rise in global food security concerns and supply chain disruptions from competitor countries like Ukraine, which offers the U.S. maize market a significant growth opportunity.

Asia Pacific

The Asia-Pacific region is the fastest-growing consumer market, driven by China’s massive industrial processing sector and the expanding livestock industries in Southeast Asia. China’s "self-sufficiency first" policy is a defining regional trend, as the government invests heavily in domestic yield improvements to reduce reliance on the "Big Four" exporters. Meanwhile, countries like India are emerging as significant players, with maize acreage expanding to 12.09 million hectares in 2024-25, fueled by a domestic push for maize-based ethanol to replace water-intensive rice-based production.

South America

South America, particularly Brazil and Argentina, has become the primary challenger to North American market dominance. Brazil’s "Safrinha" (second crop) maize production has transformed the country into a year-round exporter, increasingly filling the supply gaps in the Chinese market. The region’s growth is characterized by the rapid adoption of advanced seed technology and a competitive cost structure bolstered by favorable currency exchange rates and recent tariff liberalizations in Argentina, which have aggressively positioned South American maize in the global export corridor.

Europe

The European market is defined by its strict regulatory environment and a focus on sustainability and non-GMO production. Demand is driven by a sophisticated livestock sector and a growing bio-plastic industry. However, production is constrained by environmental regulations limiting nitrogen use and the upcoming EUDR traceability mandates. This has led to a bifurcated market where Eastern European countries like Romania and Ukraine focus on bulk exports, while Western European nations specialize in high-value, identity-preserved maize for the food and specialty chemical industries.

Middle East And Africa

In Africa, maize remains a critical food security crop, primarily in the form of white maize. However, the region is seeing a transition in countries like South Africa, which utilizes GMO yellow maize for a sophisticated commercial feed sector. The Middle East remains a major import-dependent region, where demand is driven by a lack of arable land and a growing poultry sector in Saudi Arabia and the UAE. Infrastructure development in regional ports and domestic feed milling is key to meeting the increasing demand in this geographically constrained market.

List of Companies

Archer-Daniels-Midland Company (ADM)

Cargill, Incorporated

Bunge Global SA

Bayer AG

Corteva Agriscience

Syngenta AG

KWS SAAT SE & Co. KGaA

Limagrain Group

Bühler Group

Ingredion Incorporated

Roquette

Louis Dreyfus Company

Archer-Daniels-Midland Company (ADM)

ADM maintains a dominant position in the global maize market through its massive "origination" and processing network. The company’s strategy focuses on vertical integration, moving from grain collection and storage to deep-processing into high-value derivatives like lysine, citric acid, and ethanol. ADM’s competitive advantage lies in its logistical prowess; it operates a global fleet of barges, trucks, and ships that allow it to capture arbitrage opportunities between different regional maize prices.

In recent years, ADM has shifted its focus toward "regenerative agriculture," partnering with farmers to implement low-carbon cultivation practices. This strategy is designed to meet the growing demand from CPG companies for "Scope 3" emission reductions in their supply chains. By branding its maize derivatives as sustainably sourced, ADM differentiates its products from bulk commodities, securing long-term contracts with premium food and beverage manufacturers.

Corteva Agriscience

Corteva Agriscience, following its spin-off from DowDuPont, has established itself as a technology leader in the maize seed and crop protection market. Its strategy is centered on its "PowerCore" and "Enlist" biotechnology platforms, which provide farmers with sophisticated solutions for pest and weed management. The company’s geographic strength is particularly notable in North and South America, where its Pioneer brand remains a market leader in hybrid corn sales.

The company’s technology differentiation is evidenced by its focus on "short-stature" corn, which offers better wind resistance and allows for late-season nitrogen application. This innovation directly addresses the structural need for yield stability in the face of climate change. Corteva’s integration model combines high-performance seeds with digital agronomy tools, creating a "locked-in" ecosystem for growers that maximizes output while optimizing input costs.

Cargill, Incorporated

Cargill is one of the world’s largest privately-held corporations and a central player in the global maize trade. Its market position is anchored by its vast network of wet-milling and dry-milling plants, which convert maize into a dizzying array of products for the food, feed, and industrial sectors. Cargill’s strategy is increasingly focused on the "bio-industrial" space, using maize starch as a renewable replacement for petroleum-based chemicals in plastics and adhesives.

The company’s geographic strength is truly global, with a significant footprint in every major production and consumption hub. Cargill’s competitive advantage stems from its unparalleled market intelligence and risk management capabilities, allowing it to navigate the extreme price volatility inherent in the maize market. By investing in regional processing hubs in Asia and South America, Cargill ensures it can serve the fastest-growing demand centers with locally sourced and processed maize products.

Analyst View

The global maize market is transitioning toward a technology-intensive, decarbonized value chain. Structural demand from the biofuel and animal feed sectors, particularly in Asia, remains the primary driver. Despite climate-induced yield volatility, advancements in CRISPR-based seed technology and evolving trade policies will sustain market resilience and long-term expansion through 2031.

Maize Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 315.1 billion |

| Total Market Size in 2031 | USD 362.2 billion |

| Forecast Unit | Billion |

| Growth Rate | 2.83% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Cultivation Method, Distribution Channel, Application, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

By Cultivation Method

By Distribution Channel

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. GLOBAL MAIZE MARKET BY TYPE

5.1. Introduction

5.2. Dent Maize

5.3. Flint Maize

5.4. Sweet Maize

5.5. Popcorn

5.6. Others

6. GLOBAL MAIZE MARKET BY CULTIVATION METHOD

6.1. Introduction

6.2. Genetically Modified (GMO)

6.3. Conventional (Non-GMO)

6.4. Organic

7. GLOBAL MAIZE MARKET BY DISTRIBUTION CHANNEL

7.1. Introduction

7.2. Business-to-Business (B2B)

7.3. Business-to-Consumer (B2C)

8. GLOBAL MAIZE MARKET BY APPLICATION

8.1. Introduction

8.2. Food and Beverage

8.3. Animal Feed

8.4. Biofuel and Ethanol

8.5. Pharmaceutical

8.6. Paper and Pulp

8.7. Others

9. GLOBAL MAIZE MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. By Type

9.2.2. By Cultivation Method

9.2.3. By Distribution Channel

9.2.4. By Application

9.2.5. By Country

9.2.5.1. USA

9.2.5.2. Canada

9.2.5.3. Mexico

9.3. South America

9.3.1. By Type

9.3.2. By Cultivation Method

9.3.3. By Distribution Channel

9.3.4. By Application

9.3.5. By Country

9.3.5.1. Brazil

9.3.5.2. Argentina

9.3.5.3. Others

9.4. Europe

9.4.1. By Type

9.4.2. By Cultivation Method

9.4.3. By Distribution Channel

9.4.4. By Application

9.4.5. By Country

9.4.5.1. Germany

9.4.5.2. France

9.4.5.3. United Kingdom

9.4.5.4. Spain

9.4.5.5. Others

9.5. Middle East and Africa

9.5.1. By Type

9.5.2. By Cultivation Method

9.5.3. By Distribution Channel

9.5.4. By Application

9.5.5. By Country

9.5.5.1. Saudi Arabia

9.5.5.2. UAE

9.5.5.3. Israel

9.5.5.4. Others

9.6. Asia Pacific

9.6.1. By Type

9.6.2. By Cultivation Method

9.6.3. By Distribution Channel

9.6.4. By Application

9.6.5. By Country

9.6.5.1. China

9.6.5.2. India

9.6.5.3. Japan

9.6.5.4. South Korea

9.6.5.5. Indonesia

9.6.5.6. Taiwan

9.6.5.7. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. Archer-Daniels-Midland Company (ADM)

11.2. Cargill, Incorporated

11.3. Bunge Global SA

11.4. Bayer AG

11.5. Corteva Agriscience

11.6. Syngenta AG

11.7. KWS SAAT SE & Co. KGaA

11.8. Limagrain Group

11.9. Bühler Group

11.10. Ingredion Incorporated

11.11. Roquette

11.12. Louis Dreyfus Company

12. RESEARCH METHODOLOGY

List of Figures

List of Tables

Navigate

Trusted by the world's leading organizations