Report Overview

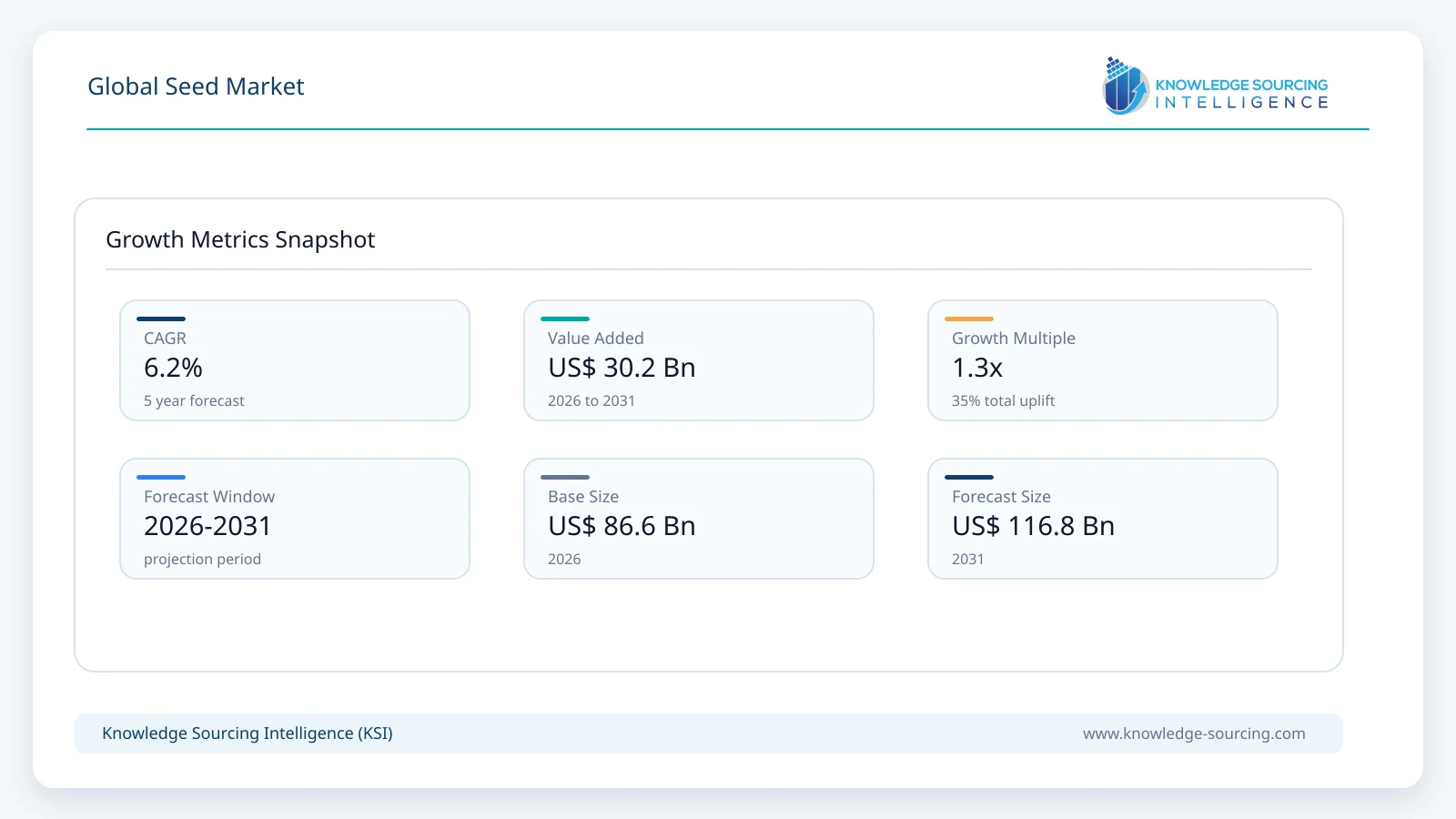

The global seed market is forecast to grow at a CAGR of 6.16%, reaching USD 116.80 billion in 2031 from USD 86.61 billion in 2026.

Highlights:

- 1Rising food demand and the need to improve agricultural productivity continue to stimulate investment in high-quality commercial seeds.

- 2Cereals and grainsremain the largest commercial crop segment because of their importance in global food and feed production.

- 3Asia Pacific represents the largest demand center owing to extensive agricultural production and government-supported seed improvement programs.

- 4Biotechnology, marker-assisted breeding, and digital breeding technologies are improving seed performance and accelerating variety development.

- 5Certified seed adoption is increasing as governments strengthen seed quality regulations and traceability systems.

- 6Competition is driven by breeding capabilities, germplasm access, trait development, regional adaptation, and agronomic support.

The seed market comprises the research, breeding, production, processing, treatment, and commercialization of seeds used for agricultural and horticultural crop cultivation. It includes conventional and trait-enhanced seeds developed to improve yield potential, pest and disease resistance, herbicide tolerance, climate resilience, and crop quality. Commercial demand spans cereals and grains, oilseeds and pulses, fruits and vegetables, and specialty crops, serving growers ranging from smallholder farmers to large commercial agricultural enterprises.

The market plays a critical role in global agricultural productivity because seed quality directly influences crop establishment, yield stability, and farm profitability. Farmers increasingly purchase certified seeds to improve germination rates, achieve uniform crop stands, and reduce production risks associated with adverse weather, pests, and diseases. Procurement decisions are influenced by local agro-climatic conditions, trait performance, regulatory approvals, seed treatment technologies, availability of agronomic support, and expected return on investment rather than seed price alone.

Population growth, changing dietary patterns, and pressure on limited arable land continue to increase demand for high-performing seed varieties. According to the Food and Agriculture Organization (FAO), global cereal production reached approximately 2.85 billion tonnes in 2024, highlighting the importance of improved seed genetics in supporting food security and maintaining agricultural productivity.

Climate variability has further strengthened investment in crop breeding and seed innovation. Seed companies are expanding research programs focused on drought tolerance, disease resistance, improved nutrient-use efficiency, and climate adaptation. Biotechnology, marker-assisted breeding, genomic selection, and digital breeding tools are shortening variety development timelines while improving breeding accuracy. These innovations enable companies to introduce varieties that meet the changing requirements of farmers, processors, and food manufacturers.

Government support also contributes to market development through certified seed distribution programs, crop improvement initiatives, and agricultural extension services. According to the Organisation for Economic Co-operation and Development (OECD), innovation in plant breeding remains essential for improving agricultural productivity while reducing environmental impacts associated with crop production.

Market Drivers

Growing Demand for Higher Agricultural Productivity

Increasing global food consumption and limited availability of additional arable land require farmers to produce higher yields from existing farmland. Improved seed genetics play a central role in achieving this objective by enhancing crop establishment, resistance to biotic and abiotic stress, and harvest consistency.

Commercial growers increasingly purchase certified hybrid and improved open-pollinated varieties because they offer better yield potential and greater resilience than farm-saved seed. Seed suppliers continue investing in breeding programs that improve productivity while addressing local agronomic conditions.

Expansion of Climate-Resilient Seed Development

Climate variability is increasing demand for varieties capable of tolerating drought, heat stress, salinity, flooding, and emerging crop diseases. Farmers are seeking seeds that maintain stable yields under unpredictable weather conditions while reducing production risk.

Seed companies are expanding genomic breeding, molecular marker technologies, and field evaluation programs to develop climate-resilient varieties. These investments strengthen product differentiation while supporting national food security objectives.

Adoption of Advanced Plant Breeding Technologies

Plant breeding has become increasingly technology intensive. Marker-assisted selection, doubled haploid technology, genomic prediction, and biotechnology are improving breeding efficiency and reducing the time required to commercialize new varieties.

According to the International Seed Federation (ISF), innovation in seed breeding remains essential for increasing agricultural productivity and strengthening food systems through improved crop genetics.

Companies continue investing in research partnerships, breeding stations, and digital phenotyping platforms to accelerate product development and improve regional adaptation.

Government Programs Supporting Certified Seed Adoption

Many governments continue implementing certified seed distribution programs to improve crop productivity and enhance national food security. Public investments in breeder seed production, seed certification laboratories, extension services, and farmer education encourage adoption of improved varieties.

Certification systems also strengthen buyer confidence by ensuring varietal purity, germination standards, and seed health, reducing risks associated with counterfeit or low-quality planting material.

Market Restraints and Challenges

High Research and Development Costs

Developing new commercial seed varieties requires substantial long-term investment in breeding, field trials, laboratory testing, regulatory approval, and seed multiplication. Development cycles often extend over several years before commercialization, increasing financial risk for seed companies.

Smaller regional breeders may face challenges competing with multinational companies that possess extensive germplasm collections, advanced breeding technologies, and global research networks.

Regulatory Complexity

Seed commercialization is governed by national regulations covering variety registration, intellectual property protection, phytosanitary requirements, biosafety, and seed certification. Regulatory differences across countries can delay market entry and increase compliance costs, particularly for biotechnology-derived traits.

Companies increasingly invest in regulatory affairs expertise and regional testing programs to facilitate product approvals across multiple markets.

Counterfeit and Informal Seed Markets

In several developing agricultural economies, uncertified and counterfeit seeds continue to affect farmer confidence and reduce productivity. Low-quality planting material may result in poor germination, inconsistent crop performance, and financial losses for growers.

Governments and industry associations are strengthening certification systems, traceability measures, and enforcement activities to improve market integrity while increasing awareness of certified seed benefits.

Major Segment Analysis

Cereals and Grains

The cereals and grains segment represents the largest commercial opportunity within the seed market because crops such as maize, wheat, rice, barley, and sorghum form the foundation of global food, feed, and industrial supply chains. These crops occupy the largest share of cultivated agricultural land and account for a substantial proportion of commercial seed demand worldwide.

Farmers prioritize seed varieties that provide high yield potential, resistance to diseases and insect pests, tolerance to herbicides, and adaptability to local climatic conditions. Commercial buyers also consider maturity period, grain quality, lodging resistance, and compatibility with mechanized farming systems when selecting seed products.

Competition within this segment depends on breeding capabilities, regional germplasm development, agronomic support, and the ability to introduce improved hybrids and trait-enhanced varieties with consistent field performance. Companies investing in precision breeding, biotechnology, and climate-resilient crop development are expected to strengthen their competitive position as growers seek solutions that improve productivity while reducing production risk.

Regional Analysis

North America

North America remains one of the most technologically advanced seed markets owing to the widespread adoption of hybrid and trait-enhanced seeds, large-scale commercial farming, and well-established intellectual property protection. The United States and Canada continue to invest in plant breeding, biotechnology, and precision agriculture to improve productivity and resource efficiency. Farmers increasingly procure seeds based on agronomic performance, drought tolerance, disease resistance, and compatibility with digital farming practices. According to the United States Department of Agriculture (USDA), improved seed genetics remain a major contributor to long-term gains in agricultural productivity and crop yields.

Europe

Europe emphasizes sustainable crop production, varietal innovation, and regulatory compliance. Demand is supported by certified seed adoption, advanced breeding programs, and increasing interest in climate-resilient crop varieties. Countries such as Germany, France, and the United Kingdom continue investing in research focused on disease resistance, improved nutrient-use efficiency, and adaptation to changing climatic conditions. Procurement decisions increasingly consider sustainability, traceability, and compliance with national and European seed regulations.

Asia Pacific

Asia Pacific represents the largest regional market because of its extensive agricultural production, growing population, and government-supported seed improvement initiatives. China and India account for substantial commercial seed demand owing to large cultivation areas for cereals, oilseeds, pulses, and vegetables. Governments continue supporting certified seed distribution, public breeding programs, and farmer extension services to improve national food security. Rising mechanization, expanding hybrid seed adoption, and increasing private-sector investment are further strengthening market opportunities throughout the region.

South America and Middle East & Africa

South America remains an important market for soybean, maize, and sunflower seeds, supported by export-oriented agriculture in Brazil and Argentina. Farmers continue adopting improved hybrids and biotechnology-derived traits to increase productivity while managing weed and insect pressure. In the Middle East and Africa, demand is influenced by food security strategies, water scarcity, and investment in climate-resilient crop varieties. Although certified seed penetration remains lower than in developed markets, public-private partnerships and government-supported agricultural modernization programs continue expanding commercial opportunities.

Competitive Landscape

The global seed market is characterized by a combination of multinational agricultural biotechnology companies and regional breeding specialists competing through genetic innovation, crop diversification, distribution networks, and agronomic support services. Competition extends beyond seed sales to include breeding expertise, trait development, digital agronomy platforms, and farmer advisory services that improve crop performance throughout the production cycle.

Companies including Bayer AG, Corteva Agriscience, Syngenta Group, Groupe Limagrain, KWS SAAT SE & Co. KGaA, BASF SE, DLF Seeds A/S, Sakata Seed Corporation, Takii & Co., Ltd., Rijk Zwaan Zaadteelt en Zaadhandel B.V., Enza Zaden Beheer B.V., East-West Seed International, Advanta Seeds, Cargill, Incorporated, Land O'Lakes, Inc., Ball Horticultural Company, Beck's Hybrids, Hazera Seeds Ltd., Longping High-Tech Agriculture Co., Ltd., and Nuziveedu Seeds Limited continue investing in advanced breeding technologies, expanded germplasm collections, biotechnology research, and regional testing programs.

Strategic differentiation increasingly depends on the development of climate-resilient varieties, stacked trait technologies, localized breeding programs, and comprehensive technical support. Partnerships with research institutions, licensing agreements for proprietary traits, and expansion of seed production facilities remain important approaches for strengthening market presence. Companies with diversified crop portfolios and strong regional distribution networks are better positioned to address varying agronomic conditions and changing farmer requirements across global agricultural markets.

Recent Developments

February 2026: KWS SAAT SE & Co. KGaA announced continued investment in global breeding infrastructure and research programs to accelerate the development of disease-resistant and climate-adapted crop varieties. Commercial relevance: The investment strengthens long-term product innovation and supports regional breeding capabilities.

September 2025: Corteva Agriscience introduced additional soybean and corn seed varieties developed through advanced breeding technologies for the 2026 planting season. Commercial relevance: The expanded portfolio improves regional product availability and supports productivity under diverse growing conditions.

May 2025: Bayer AG announced the commercial expansion of its next-generation DEKALB maize hybrids across selected markets, incorporating improved drought tolerance and enhanced agronomic performance. Commercial relevance: The launch strengthens Bayer's cereal seed portfolio while supporting farmer demand for climate-resilient hybrids.

Regulatory and Policy Environment

The seed market is governed by regulations covering variety registration, seed certification, phytosanitary measures, plant breeders' rights, biotechnology approvals, and international seed trade. Regulatory compliance is essential to ensure varietal identity, seed quality, germination standards, and protection against the spread of plant pests and diseases.

The International Seed Testing Association (ISTA) establishes internationally recognized standards for seed sampling and laboratory testing, supporting quality assurance and facilitating global seed trade.

The Organisation for Economic Co-operation and Development (OECD) administers the OECD Seed Schemes, which harmonize varietal certification and facilitate international movement of certified seed among participating countries.

The International Plant Protection Convention (IPPC) develops phytosanitary standards that reduce the risk of introducing plant pests during international seed trade. Compliance with these standards is increasingly important as seed companies expand global distribution networks.

Many governments also support certified seed adoption through subsidy programs, breeder seed production, extension services, and investments in national seed certification agencies. These initiatives improve farmer access to high-quality planting material while strengthening agricultural productivity and food security.

Outlook and Strategic Implications

The global seed market is expected to benefit from sustained investment in crop genetics, climate adaptation, and precision agriculture throughout the 2026 to 2031 period. Increasing demand for higher agricultural productivity, combined with limited expansion of cultivable land, will continue to encourage adoption of improved hybrid and trait-enhanced seed varieties.

Future procurement decisions are expected to prioritize yield stability, stress tolerance, disease resistance, input-use efficiency, and compatibility with precision farming technologies. Farmers are likely to place greater emphasis on seeds capable of maintaining consistent performance under increasingly variable climatic conditions.

Seed companies are expected to increase investment in genomic selection, gene editing where permitted, digital breeding platforms, and localized research programs that improve regional adaptation. Expanded collaboration with research institutes, universities, and agricultural organizations will support faster development of commercially viable varieties.

Despite opportunities, regulatory complexity, intellectual property protection, counterfeit seed distribution, and climate uncertainty will remain important business considerations. Companies capable of combining strong breeding capabilities with regional market knowledge, regulatory expertise, and extensive distribution networks are expected to maintain competitive advantages. Continued public investment in agricultural research, certified seed programs, and sustainable farming practices will further support long-term demand for high-quality commercial seeds across both developed and emerging agricultural economies.

Seed Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 86.61 billion |

| Total Market Size in 2031 | USD 116.80 billion |

| Forecast Unit | Billion |

| Growth Rate | 6.16% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Origin, Trait, Crop Type, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Origin

- Genetically Modified (GM) Seeds

- Conventional Seeds

By Trait

- Herbicide-Tolerant

- Insect-Resistant

- Stacked Traits

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Other Crops

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Others

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Israel

- Others

- Asia Pacific

- China

- India

- Japan

- Australia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

3.2. CXO Perspective

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Market Opportunities

4.4. Porter’s Five Forces Analysis

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Power of Buyers

4.4.3. Threat of New Entrants

4.4.4. Threat of Substitutes

4.4.5. Competitive Rivalry in the Industry

4.5. Industry Value Chain Analysis

4.6. Analyst View

5. GLOBAL SEED MARKET BY ORIGIN

5.1. Introduction

5.2. Genetically Modified (GM) Seeds

5.3. Conventional Seeds

6. GLOBAL SEED MARKET BY TRAIT

6.1. Introduction

6.2. Herbicide-Tolerant

6.3. Insect-Resistant

6.4. Stacked Traits

7. GLOBAL SEED MARKET BY CROP TYPE

7.1. Introduction

7.2. Cereals and Grains

7.3. Oilseeds and Pulses

7.4. Fruits and Vegetables

7.5. Other Crops

8. GLOBAL SEED MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Origin

8.2.2. By Trait

8.2.3. By Crop Type

8.2.4. By Country

8.2.4.1. United States

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Origin

8.3.2. By Trait

8.3.3. By Crop Type

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Origin

8.4.2. By Trait

8.4.3. By Crop Type

8.4.4. By Country

8.4.4.1. Germany

8.4.4.2. France

8.4.4.3. United Kingdom

8.4.4.4. Others

8.5. Middle East and Africa

8.5.1. By Origin

8.5.2. By Trait

8.5.3. By Crop Type

8.5.4. By Country

8.5.4.1. Saudi Arabia

8.5.4.2. United Arab Emirates

8.5.4.3. Israel

8.5.4.4. Others

8.6. Asia Pacific

8.6.1. By Origin

8.6.2. By Trait

8.6.3. By Crop Type

8.6.4. By Country

8.6.4.1. China

8.6.4.2. India

8.6.4.3. Japan

8.6.4.4. Australia

8.6.4.5. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Bayer AG

10.2. Corteva Agriscience

10.3. Syngenta Group

10.4. Groupe Limagrain

10.5. KWS SAAT SE & Co. KGaA

10.6. BASF SE

10.7. DLF Seeds A/S

10.8. Sakata Seed Corporation

10.9. Takii & Co., Ltd.

10.10. Rijk Zwaan Zaadteelt en Zaadhandel B.V.

10.11. Enza Zaden Beheer B.V.

10.12. East-West Seed International

10.13. Advanta Seeds

10.14. Cargill, Incorporated

10.15. Land O'Lakes, Inc.

10.16. Ball Horticultural Company

10.17. Beck's Hybrids

10.18. Hazera Seeds Ltd.

10.19. Longping High-Tech Agriculture Co., Ltd.

10.20. Nuziveedu Seeds Limited

Navigate

Trusted by the world's leading organizations