Report Overview

Instrument Transformer Market Size:

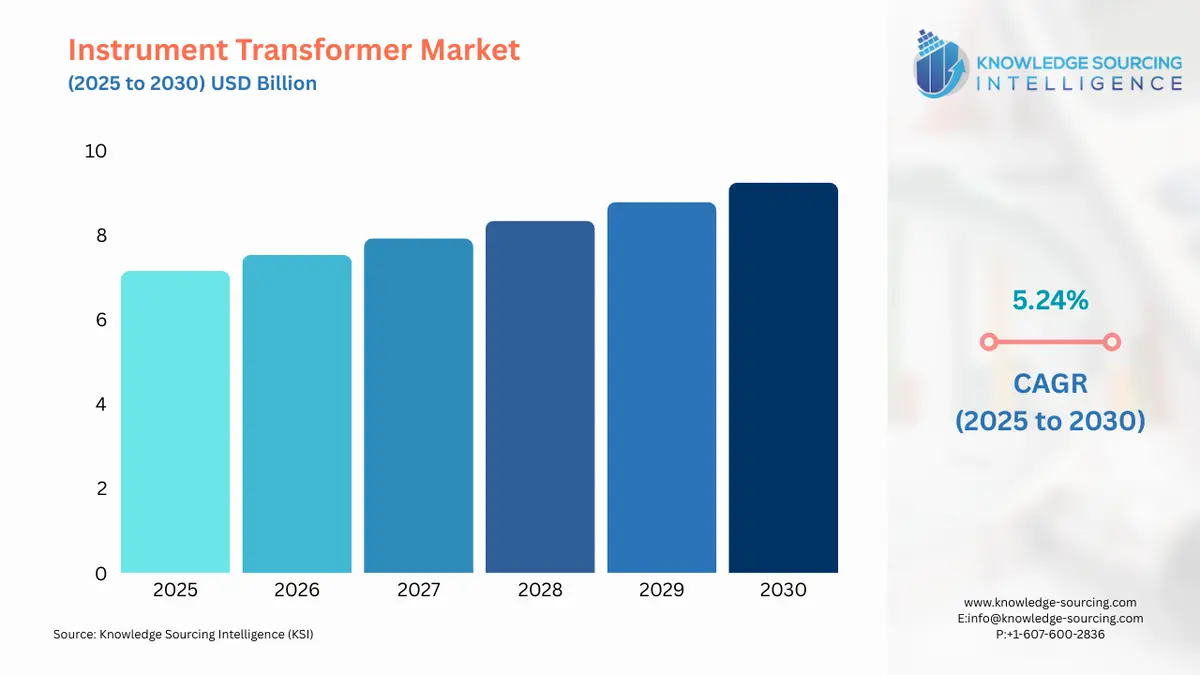

Instrument Transformer Market, growing at a 5.08% CAGR, is projected to achieve USD 9.632 billion in 2031 from USD 7.154 billion in 2025.

The adoption of instrument transformers to help with the effective monitoring and protection of power systems and ensure reliable operations is due to the rapid expansion of power transmission and distribution networks. This helps to meet the rising energy demand from residential spaces, commercial establishments, railways, metros, and other industries.

Another element driving development is the expanding renovation work being done on the current grid network as a result of the growing complexity of the electrical infrastructure and the rise in power demand from end users. As per IEA data, the industrial sector used 36.6 EJ of electricity in 2021 and is projected to use 48.9 EJ by 2030. This shows that there will be a high demand for instrument transformers in the future.

Instrument Transformer Market Growth Drivers:

Growing Demand For Sustainable Power Transmission Solutions

Instrument transformers are gaining popularity due to the increased use of renewable energy sources, such as solar panels in residential structures, to make it easier to connect and measure the energy produced by these sources. Instrument transformers make it possible to precisely measure the voltage and current going into and out of household solar energy systems, enabling homeowners to keep track of their energy output and make the most of renewable resources.

According to the World Economic Forum data, Gujarat's residential rooftop solar capacity will expand from 0.085 GW in 2019 to 1.2 GW in 2022, fueling the demand for instrument transformers.

Further, the Centre for Sustainable Systems stated that in 2021, the residential sector consumed 3.79 trillion kWh, or 96% of all the power sold in the United States. The International Energy Agency (IEA) predicts that by 2027, the total electricity generated by renewable sources will increase to 38.10 % of the total energy consumed from 28% in 2021 surging the demand for instrument transformers.

Furthermore, the Power Grid Corporation of India Limited stated in November 2022 that it plans to build a transmission line for roughly USD 2.43 billion to make it easier to move excess power from Raigarh, Chhattisgarh to the south. In May 2022, Hitachi Energy and Arteche announced the formation of a new joint venture (JV) called Arteche Hitachi Energy Instrument Transformers S.L. in compliance with the contract agreed in December 2021.

Instrument Transformer Market Geographical Outlook:

The United States in North America is an Expected Dominant Market

There are several factors that are driving the growth of the instrument transformer market in the USA such as the integration of renewable energy followed by smart grid implementation. The increasing focus on renewable energy sources such as wind and solar power requires advanced monitoring and control systems. Instrument transformers play a vital role in accurately measuring and managing the variable power outputs from these sources, ensuring grid stability.

As per the Center for Climate and Energy Solution, the United States consumption of renewables is anticipated to increase in the next 30 years with an average annual rate of 2.4%, which is higher than the usual growth rate of 0.5% each year. In the United States, renewables made up nearly 20% of utility-scale U.S. electricity generation in 2020 with the bulk power coming from wind power and hydropower which can be seen in the figure below.

Additionally, the transition to smart grids involves the integration of digital technologies for efficient monitoring, communication, and control of the electrical grid. Instrument transformers are crucial for providing real-time data that enables better decision-making and grid optimization.

The USA's power infrastructure has been ageing, leading to the need for upgrades and replacements. Modern instrument transformers with advanced features and technologies can improve the efficiency and reliability of the grid. Moreover, as the population grows and industrial activities expand, the demand for electricity continues to rise. This drives the need for robust and reliable power transmission and distribution infrastructure, in turn boosting the demand for instrument transformers.

Market Segmentation:

By Type

Current Transformer

Potential Transformer

By Voltage

Low

Medium

High

By End-User

Residential

Commercial

Industrial

By Geography

North America

USA

Canada

Mexico

South America

Brazil

Argentina

Others

Europe

Germany

France

United Kingdom

Spain

Others

Middle East and Africa

Saudi Arabia

UAE

Others

Asia Pacific

China

India

Japan

South Korea

Indonesia

Thailand

Others

Market Segmentation

By Type

By Voltage

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. INSTRUMENT TRANSFORMER MARKET BY TYPE

5.1. Introduction

5.2. Current Transformer

5.3. Potential Transformer

6. INSTRUMENT TRANSFORMER MARKET BY VOLTAGE

6.1. Introduction

6.2. Low

6.3. Medium

6.4. High

7. INSTRUMENT TRANSFORMER MARKET BY END-USER

7.1. Introduction

7.2. Residential

7.3. Commercial

7.4. Industrial

8. INSTRUMENT TRANSFORMER MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. USA

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Argentina

8.3.3. Others

8.4. Europe

8.4.1. Germany

8.4.2. France

8.4.3. United Kingdom

8.4.4. Spain

8.4.5. Others

8.5. Middle East and Africa

8.5.1. Saudi Arabia

8.5.2. UAE

8.5.3. Others

8.6. Asia Pacific

8.6.1. China

8.6.2. India

8.6.3. Japan

8.6.4. South Korea

8.6.5. Indonesia

8.6.6. Thailand

8.6.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Amran Instrument Transformers

10.2. CG Power & Industrial Solutions Ltd.

10.3. General Electric

10.4. Hitachi Energy Ltd (Hitachi Group)

10.5. Instrument Transformer Equipment Corporation, Inc.

10.6. Meramec Instrument Transformer Co.

10.7. NISSIN ELECTRIC Co., Ltd

10.8. Ritz Instrument Transformers GmbH

10.9. Schneider Electric

10.10. Vamet Industries

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key benefits for the stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations