Report Overview

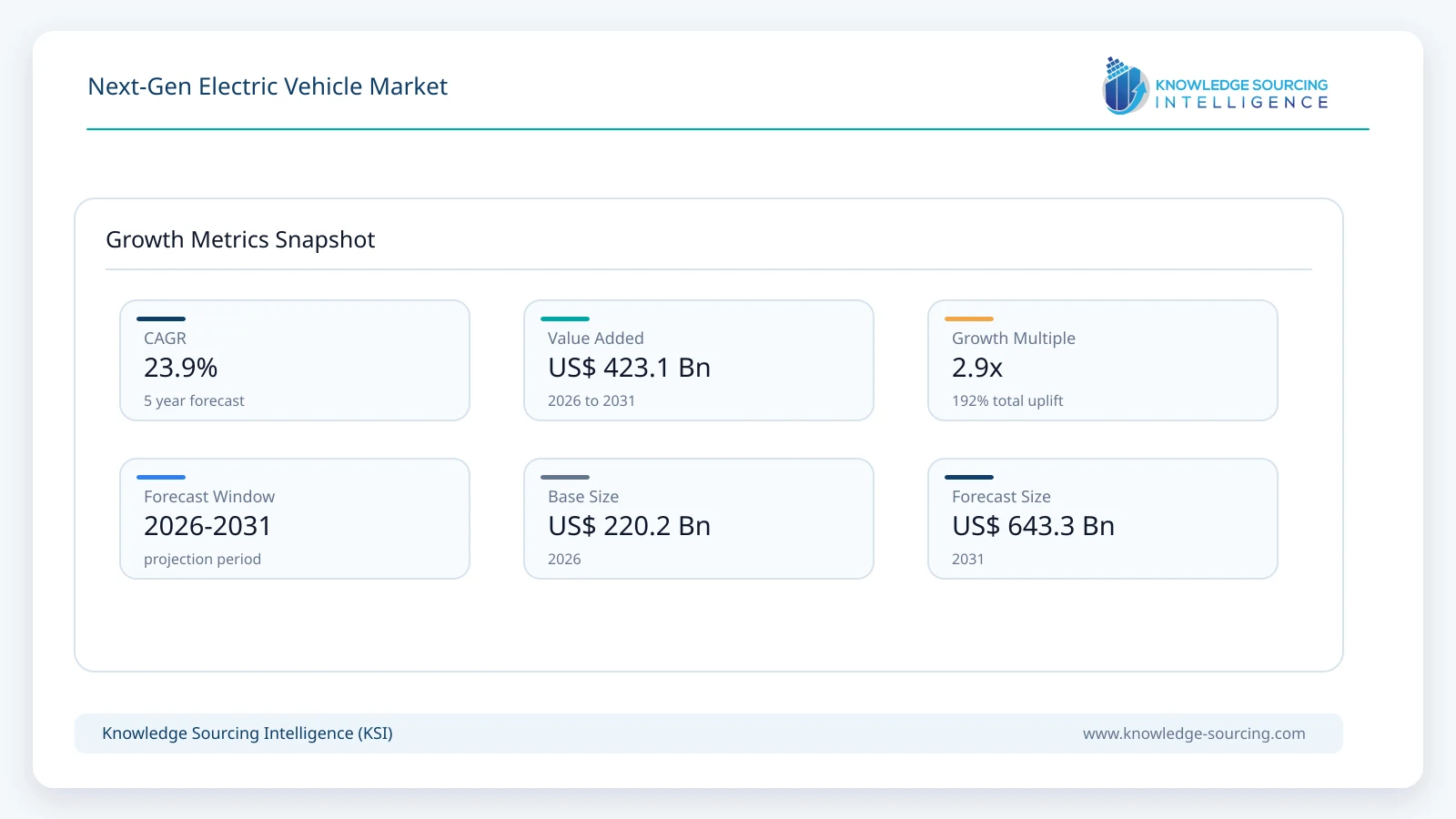

The Next-Gen Electric Vehicle Market is anticipated to surge from USD 220.2 billion in 2026 to USD 643.3 billion by 2031, advancing at a 23.9% CAGR during the forecast period.

Highlights:

- 1Transitioning DemandGlobal manufacturers are rapidly launching specialized electric vehicle segments to capture a larger commercial consumer base.

- 2Accelerating InnovationAutomakers are actively commercializing solid-state and sodium-ion batteries to enhance safety and affordability.

- 3Regionalizing ProductionCompanies are shifting toward localized manufacturing hubs to bypass tightening international trade restrictions.

- 4Upgrading ArchitecturesCommercial fleet operators are quickly adopting 800-volt charging systems to drastically reduce downtime.

The global Next Gen Electric Vehicle market is undergoing a significant paradigm shift due to the marriage of superior high-performance battery technology and trade protectionism. As of January 2026, as the original equipment manufacturers (OEMs) have transitioned away from generalized adoption of electric vehicles towards creating highly specialized segments of demand driven by technology, the challenge for OEMs has shifted to capturing the larger commercial consumer base. This evolutionary stage is marked by the emergence of an evolving battery marketplace, which has resulted in significant innovation around charging speeds, safety, and cost competitiveness.

The current dynamics of the industry are based on an intricate mix of regulatory requirements and raw material supply issues. Furthermore, with the increasing introduction of software-defined vehicles (SDVs) and 800-volt charging systems being adopted as a standard to compete favorably at the premium market level and the need for manufacturers to minimize total cost of ownership (TCO) for the mass market, global manufacturers have balanced the need for technological leadership with the need to have a regionalized supply chain due to the added challenges of the cross-border vehicle export market created by changes to trade policies between the United States and the European Union.

Mass-Scale Commercialisation of Solid-State Batteries (SSB): Leading original equipment manufacturers (OEMs), notably Toyota and its partner Sumitomo Metal Mining, formalised cathode development agreements in late 2025 to achieve mass production of high-density solid-state cells by the 2027–2028 window. This technological shift directly addresses the long-standing demand for increased energy density and safety, effectively marginalising the performance ceiling of liquid-electrolyte lithium-ion systems.

Geopolitical Re-alignment via Section 301 Tariffs: The United States’ implementation of a 100% tariff on Chinese-manufactured electric vehicles (EVs) in September 2024 has triggered a structural pivot in global supply chains. This regulatory barrier forces a decoupling of the North American market from Chinese-produced low-cost units, shifting demand toward domestic manufacturing hubs and incentivising non-Chinese OEMs to localise battery production within free-trade zones.

Market Entry of Sodium-Ion (Na-ion) Architectures: In late 2025, CATL commenced mass production of its "Naxtra" sodium-ion battery series. This development addresses the demand for price-sensitive, entry-level electric mobility, particularly in the two- and three-wheeler segments and budget passenger vehicles, by leveraging the abundance and cost-efficiency of sodium over volatile lithium supplies.

Localized Production Surges in Non-Traditional Hubs: Middle Eastern and South American markets are transitioning from import-dependency to localized manufacturing, evidenced by Saudi Arabia’s Ceer and Lucid projects reaching critical employment milestones in late 2025 and Brazil’s "Fuel of the Future" legislation. These initiatives create a regional demand for customized EV architectures, such as ethanol-electric hybrids, that align with local energy resources and infrastructure.

Market Dynamics

Market Drivers

A key driver of the emerging market for next-generation electric vehicles is the increase in battery energy density associated with new technologies using solid-state and high-silicon anode batteries. Consumer interest in longer-range vehicles (greater than 800 km) with less weight than existing battery packs creates demand for these newer generation pulse cells. New governmental regulations requiring commercial vehicle manufacturers to significantly increase their sales of zero-emission vehicles, including the U.S. Environmental Protection Agency's (EPA) Multi-Pollutant Emission Standards for 2027–2032 and the Euro 7 agreement finalised in 2024, will also add momentum to this shift to electric (and other) vehicles. The EPA has established substantial economic penalties for the continued production of internal combustion engines (ICEs) that will subsidise the development of electric vehicles. At the same time, US tariffs of 100% on Chinese imports have created a significant void in North America for lower-cost, locally made electric vehicles and have resulted in substantial investments from domestic companies to fill this void.

Market Restraints & Opportunities

Despite how difficult it can be to attract long-term demand growth (especially in the commercial and heavy-duty vehicle segments), there are very few commercial “megawatt-scale” (350 kW+) Charging Solutions anywhere. Because Electric Vehicles (“EVs”) use charging solutions that connect back onto the Grid, an overall lack of large battery installations causes constraints throughout the entire Electric Vehicle Supply Chain (e.g., Fleet Operators) because of the high cost of building out a High-Powered Charger Infrastructure compared to existing ICE fleets. This creates an opening for Electrical Vehicle-to-Grid (V2G) Technology, where EV batteries can function as Distributed Energy Storage Systems. This creates a new value proposition for EV owners and, consequently, increases the overall usage of bi-directionally-capable charging EVs. In addition, the sharp drop-off in Lithium Prices in 2024 and 2025 created short-term volatility for Lithium Producers, but it allowed for an increase in battery affordability. It has since opened demand for large-format batteries for the long-haul/Fleet Operator/Heavy-Duty Truck markets that would have been previously unfeasible.

Raw Material and Pricing Analysis

As we have seen since the price peaks in 2022, volatility will exist in the new generation of electric vehicles, and the "Critical Mineral Trinity" (lithium, nickel and cobalt) will dictate these pricing dynamics through 2024/2025. The temporary oversupply of lithium and nickel in the market, combined with the expansion of lithium iron phosphate (LFP) chemistry (which does not utilise cobalt or nickel), has caused a major correction in the market. However, there is renewed pressure being placed on the supply chain due to an increased demand for next-generation, high-nickel cathodes and solid-state electrolytes. The mineral sourcing requirements outlined in the US Inflation Reduction Act (IRA) will have the effect of bifurcating the mineral pricing system, where "IRA-compliant" minerals sourced from free-trade partners will be priced at a premium compared to non-compliant minerals. Furthermore, the demand for domestic mining and refining projects located in Australia, Canada, and the US has increased, since OEMs are seeking to qualify their customers for tax credits associated with sourcing compliant minerals.

Supply Chain Analysis

The global EV supply chain is transitioning from a "Global-JIT" (Just-in-Time) model to a "Regional-JIC" (Just-in-Case) architecture. China remains the dominant production hub, controlling over 50% of global battery manufacturing capacity, but its influence is being challenged by the rapid construction of "Gigafactories" in North America and Europe. Logistical complexities have increased due to new environmental, social, and governance (ESG) reporting mandates, such as the EU Battery Passport, which requires full traceability of raw materials. This shift increases demand for localized supply chains that minimize the carbon footprint of logistics. Dependencies on specific refined materials, such as spherical graphite and high-purity manganese, remain a strategic vulnerability, prompting OEMs like Tesla and GM to sign direct off-take agreements with miners to bypass third-party distributors.

Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

|---|---|---|

United States | USTR Section 301 (Sept 2024) | Imposes 100% duty on Chinese EVs and 25% on batteries; shifts demand toward domestic US-made or FTA-partner vehicles. |

European Union | Euro 7 Standards (Finalized 2024) | Mandates stricter brake and tire emission limits for all vehicles; increases demand for EVs with regenerative braking systems. |

Brazil | "Fuel of the Future" Law (2024/2025) | Increases mandatory ethanol blending to 30% and incentivizes ethanol-electric hybrids; creates niche demand for flex-fuel EVs. |

Saudi Arabia | PIF Localization Mandates | Requires 45% local component sourcing by 2030; drives demand for regional Tier-1 suppliers to support Ceer and Lucid. |

China | NEV Dual-Credit Scheme | Adjusts credit weights to favor ultra-long range and high-efficiency BEVs; maintains high demand for high-density battery tech. |

Key Developments

June 2026: BYD officially presented its latest next-generation electric vehicle lineup, including the e-Vali electric van making its UK show debut at Company Car in Action 2026, highlighting expanded commercial EV offerings and advanced electrification technologies.

June 2026: Mercedes-Benz officially commenced series production of its next-generation high-performance axial-flux electric motor at the Berlin-Marienfelde plant, supporting future Mercedes-AMG electric vehicles with higher power density, efficiency, and compact drivetrain architecture.

April 2026: BYD officially unveiled the all-new Sealion 08 battery-electric and plug-in hybrid SUV at the 2026 Beijing Auto Show, showcasing its next-generation Ocean Series platform, Blade Battery technology, and advanced electrified powertrain options.

March 2026: Xiaomi officially launched the new-generation SU7 sedan in China, beginning immediate customer deliveries with upgraded V6s Plus motors, higher-voltage architecture, longer driving range, and enhanced intelligent vehicle capabilities.

Market Segmentation

By Technology: Solid-State Batteries (SSB)

Solid-State Battery Technology is being driven by the global need within the automotive industry to resolve the current dilemma of "safety-density," solved by the traditional use of a flammable liquid electrolyte as the main component in lithium-ion batteries. Whereas lithium-ion batteries have been constructed with liquid electrolytes that are flammable and present a high risk of thermal runaway and combustion and therefore posing additional risk, solid-state batteries contain solid ceramic or polymer electrolytes which are naturally stable. With significant advances in interface resistance (the blockage of quick ion transportation between the electrodes) being made by both ProLogium and Toyota within the next 10 years, the increase in demand from both high performance and luxury automotive segments will create more opportunities to create new products that meet consumer needs (highly safe and providing rapid recharge capabilities of 10% - 60% in 10 minutes). Pilot production of future designs has begun in late 2025 and has already influenced the design of developing future vehicle platforms with smaller and lighter designs that provide for improved aerodynamics and distance travelled per charge. Although predicted to be a low-volume/high-margin contributor until more mass production occurs in 2027, companies that are working on proprietary solid electrolytes are experiencing high levels of capital investments.

By End-User: Commercial Vehicles

The commercial vehicle market, which includes delivery vans, heavy trucks, and municipal buses, is growing rapidly as companies strive for more sustainable solutions and also find the total cost of ownership (TCO) for commercial vehicles is much lower than for passenger vehicles. Unlike passenger vehicles, where purchasing decision is affected by consumer emotions, such as range anxiety and aesthetics, the commercial vehicle market base their purchasing decisions on the math of utility. Major cities across Europe have implemented "Zero-Emission Zones," which impacted the operation of diesel-powered vans to the point where it is no longer economically feasible; as a result, the demand for electric-powered light commercial vehicles (e-LCVs) has risen sharply. Additionally, the introduction of 800V and 1000V electric truck architectures in 2024-2025 will drastically reduce the amount of time it takes to charge an electric truck, therefore making them competitive with diesel trucks for regional logistics operations. The availability of government-funded "green corridors," where high-power, megawatt-charging infrastructure has been established, has removed the final barrier to electrification for long-haul trucking. Together, all these factors have collectively led to record order volumes for Class 8 electric trucks from manufacturers such as Tesla, Volvo, and Nikola as logistics providers look to "future-proof" their fleet against impending carbon tax and diesel bans.

Regional Analysis

North America Market Analysis

The United States market is characterized by significant USTR Section 301 tariff intervention which has eliminated the potential for Chinese price competition domestically. As a result of this protectionism, there has been a shift in demand away from lower-cost imports towards the "Big Three" (General Motors, Ford and Stellantis) and Tesla, as they ramp up production of batteries domestically in North America. Additionally, the United States market's demand for next-generation battery electric vehicles (BEVs) is heavily weighted toward larger-format vehicles including pickup trucks and full-size SUVs. The launch of the Tesla Cybertruck and Chevrolet Silverado EV in the 2024 to 2025 timeframe indicates an increased demand for high-performance electric work vehicles among consumers. However, there are still varying levels of demand for such vehicles depending on availability of fast charge stations, as demand for this type of vehicle is concentrated heavily in coastal states. The National Electric Vehicle Infrastructure (NEVI) formula program began yielding results in 2025 with the proliferation of fast-charging stations along interstates leading to increased demand for these vehicles in less populated, more rural states making up the rest of the country.

South America Market Analysis

Brazil has a very unique "hybrid-first" approach to the next-generation battery electric vehicle (BEV) market. The reason behind this approach is Brazil's existing, extensive infrastructure for ethanol. The 2024 "Fuel of the Future" Act provides a framework to engineer and build ethanol fuel cell and ethanol/electric hybrid vehicles while placing limited importance on the manufacturing of pure battery powered BEVs. This strategy leverages Brazil's position as a leading sugarcane producer by lowering the need for very expensive lithium-ion batteries from foreign sources. In 2025, BYD and Stellantis both announced plans to develop local production of "Bio-Hybrid" platforms in Brazil's Territory.

Europe Market Analysis

Traditionally considered the hub of the European automotive manufacturing base, Germany now faces a transitional dilemma of decreased EV buying interest while transitioning away from ICE based vehicle development. While the termination of Federal EV financing programs at the end of 2023 caused some slowing in the demand for EVs, that demand rebounded in 2025 when Volkswagen, BMW and Mercedes-Benz introduced new dedicated platforms referred to as "Next Generation". (Ie, Volkswagen SSP and BMW Neue Klasse) The German automotive market is focused primarily on SDVs, wherein the vehicle’s value is derived from the digital services offered and autonomous driving capabilities of the vehicles themselves and no longer solely based on mechanical specifications. Demand for SDVs has been hampered as a result of rising energy prices and inefficient permitting processes for charging stations. The adoption of the final Euro 7 standard places more emphasis on purchasing "clean" or sustainable EVs, with consumer interests shifting to utilizing sustainable materials in EV interiors and low-emission manufacturing methods.

Middle East and Africa Market Analysis

Saudi Arabia is quickly becoming the center of the Next Generation EV market in the Middle East thanks to both the Saudi Public Investment Fund (PIF) and the Vision 2030 economic development program. Current demand is not consumer-led but is being driven by a massive state-supported industrialisation and machine manufacturing development. In late 2025, Ceer (the first locally produced Saudi-built EV brand) and Lucid Motors achieved significant production achievements at their respective production facilities located in King Abdullah Economic City (KAEC). In order to stimulate demand, the Saudi government has made a commitment to purchase a minimum of 100 thousand EVs during the next 10 years. The local market is characterised by an engineering demand for "Extreme Climate" vehicles requiring advanced battery thermal management systems.

Asia Pacific Market Analysis

China is the most technologically advanced and largest Electric Vehicle (EV) market in the world and has commenced the phase of "mass adoption" with next-generation (NG) technologies. By 2025, the Chinese market transitioned from volume demands to intelligence-driven demands, thus requiring all competitive models to offer No Map (NM) navigate on autopilot (NOA) functionality in urban environments (i.e. through the use of radar/micro-sdk).

Currently, China is experiencing a significant pricing war, which has led to the mid-range EV price being equivalent to the Internal Combustion Engine (ICE). This has resulted in substantial demand for EV replacement. By 2025, when CATL's new Sodium-ion battery technology was introduced to the market, and the launch of BYD’s new Blade Battery, the entry-level price point for mid-range EVs greatly decreased. Although there is significant tariff obfuscation associated with export demand from China, the movement of Original Equipment Manufacturers (OEMs) in China to the Southeast, Central and the Middle East is very strong.

In 2025, the Chinese government updated its "Dual Credit" Program, adding efficiency standards that eliminated many smaller businesses and created a consolidation around large market leaders, such as BYD, Li Auto and Geely.

List of Companies

Tesla, Inc.

BYD Auto

Volkswagen Group

Toyota Motor Corporation

Hyundai Motor Group

General Motors

Ford Motor Company

BMW Group

Mercedes-Benz Group

Stellantis

The competitive landscape of the Next Gen Electric Vehicle Market is bifurcated between legacy OEMs attempting a structural "re-tooling" and pure-play EV manufacturers focused on vertical integration. The dominant theme of 2025 is the race for "Battery Autonomy," where companies are bypassing Tier-1 suppliers to develop in-house cell chemistries and mineral refining capabilities. Software is the second major battleground; the ability to deliver over-the-air (OTA) updates that improve vehicle range and performance post-purchase is now a prerequisite for market leadership.

Tesla, Inc.

Tesla has defined the standard for profitability in the Electric Vehicle industry and the model of vertical integration. In 2024 and 2025, Tesla focused on increasing its production ability with the 4680 cells and finalising their new manufacturing process that allows for a 50% production cost reduction. Tesla's competitive edge lies in its Supercharger network, which has essentially become the "de facto" North American Charging Standard (NACS) and its Full Self-Driving (FSD) Software. By licensing their charging technology to competitors and providing their FSD Software as a Cloud-based Software as a Service (SaaS) solution, Tesla is expanding its revenue models beyond hardware sales, with recent increased activity on the "Model 2" platform (a high volume production, low-cost vehicle), which follows their strategy of gaining volume experience in global markets.

BYD Auto

BYD has surpassed Tesla in total NEV (New Energy Vehicle) volume, leveraging its history as a battery manufacturer to maintain a cost structure that is arguably the lowest in the industry. BYD’s "Blade Battery" technology, which utilizes a cell-to-pack (CTP) architecture, has become a high-demand component even for other OEMs. In 2025, BYD’s strategic focus shifted toward global manufacturing localization to circumvent trade barriers. The arrival of production equipment at its Hungary plant in December 2025 and the construction of its Brazilian hub indicate a move toward becoming a truly global OEM. BYD’s product strategy involves a "multi-brand" approach, from the budget-friendly Seagull to the ultra-luxury Yangwang brand, allowing it to capture demand across all socioeconomic segments.

Toyota Motor Corporation

Toyota has transitioned from a perceived "EV laggard" to a leader in the next-generation battery roadmap. The company’s "Multi-Pathway" strategy—investing in HEVs, PHEVs, BEVs, and FCEVs—has proven resilient as pure BEV demand growth fluctuated in 2024. Toyota’s most significant strategic move is its commitment to solid-state batteries. By partnering with Sumitomo Metal Mining for cathode development in late 2025 and ramping up its North Carolina battery plant, Toyota is positioning itself to own the "Premium EV" segment of the late 2020s. Its focus on 800km+ range and 10-minute charging is a direct play for the "reluctant adopter" segment that has stayed away from current-generation EVs due to range and charging concerns.

Next-Gen Electric Vehicle Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 220.2 billion |

| Total Market Size in 2031 | USD 643.3 billion |

| Forecast Unit | Billion |

| Growth Rate | 23.9% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Vehicle Type, Propulsion Type, Battery Technology, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Vehicle Type

By Propulsion Type

By Battery Technology

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. NEXT-GEN ELECTRIC VEHICLE MARKET BY VEHICLE TYPE

5.1. Introduction

5.2. Passenger Vehicles

5.3. Commercial Vehicles

5.4. Two- & Three-Wheelers

5.5. Electric Buses

6. NEXT-GEN ELECTRIC VEHICLE MARKET BY PROPULSION TYPE

6.1. Introduction

6.2. Battery Electric Vehicles (BEVs)

6.3. Plug-in Hybrid Electric Vehicles (PHEVs)

6.4. Hybrid Electric Vehicles (HEVs)

6.5. Fuel Cell Electric Vehicles (FCEVs)

7. NEXT-GEN ELECTRIC VEHICLE MARKET BY BATTERY TECHNOLOGY

7.1. Introduction

7.2. Lithium-Ion Batteries

7.3. Solid-State Batteries

7.4. Sodium-Ion Batteries

7.5. Lithium-Sulfur Batteries

8. NEXT-GEN ELECTRIC VEHICLE MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Vehicle Type

8.2.2. By Propulsion Type

8.2.3. By Battery Technology

8.2.4. By Country

8.2.4.1. USA

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Vehicle Type

8.3.2. By Propulsion Type

8.3.3. By Battery Technology

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Vehicle Type

8.4.2. By Propulsion Type

8.4.3. By Battery Technology

8.4.4. By Country

8.4.4.1. Germany

8.4.4.2. France

8.4.4.3. United Kingdom

8.4.4.4. Spain

8.4.4.5. Others

8.5. Middle East and Africa

8.5.1. By Vehicle Type

8.5.2. By Propulsion Type

8.5.3. By Battery Technology

8.5.4. By Country

8.5.4.1. UAE

8.5.4.2. Saudi Arabia

8.5.4.3. Others

8.6. Asia Pacific

8.6.1. By Vehicle Type

8.6.2. By Propulsion Type

8.6.3. By Battery Technology

8.6.4. By Country

8.6.4.1. China

8.6.4.2. Japan

8.6.4.3. South Korea

8.6.4.4. India

8.6.4.5. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Tesla, Inc.

10.2. BYD Auto

10.3. Volkswagen Group

10.4. Toyota Motor Corporation

10.5. Hyundai Motor Group

10.6. General Motors

10.7. Ford Motor Company

10.8. BMW Group

10.9. Mercedes-Benz Group

10.10. Stellantis

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key benefits for the stakeholders

11.5. Research Methodology

11.6. Abbreviations

Navigate

Trusted by the world's leading organizations