Report Overview

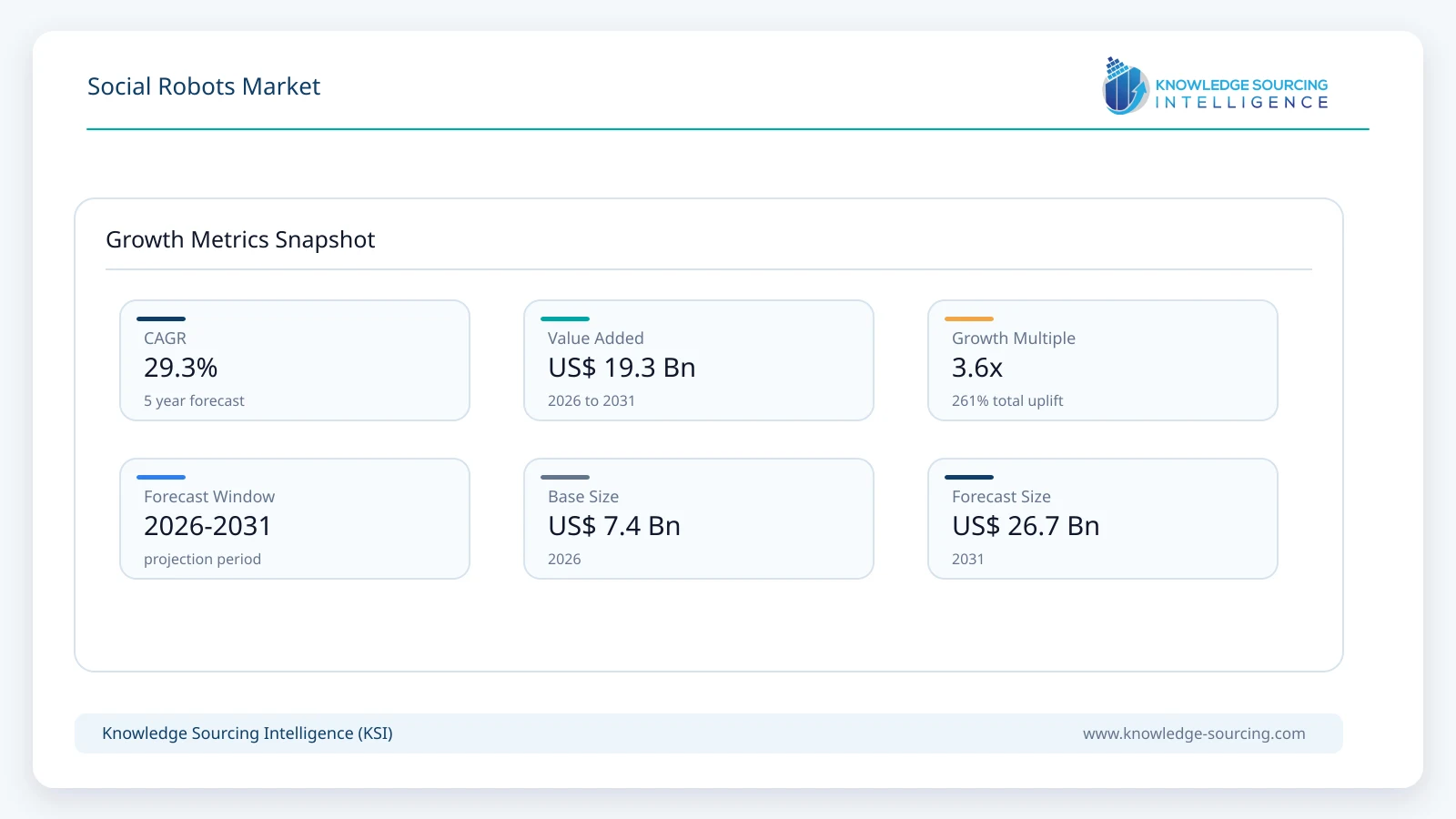

The Social Robots market is forecast to grow at a CAGR of 29.3%, reaching USD 26.7 billion in 2031 from USD 7.4 billion in 2026.

Highlights:

- 1Rising labor shortages in healthcare, hospitality, and customer service continue to support commercial demand for social robots.

- 2Healthcare and elderly care represent the most commercially important end-user segment due to aging populations and long-term care requirements.

- 3Asia Pacific remains a major manufacturing and adoption center supported by robotics investment and government innovation initiatives.

- 4Artificial intelligence capabilities, particularly natural language processing and computer vision, continue to improve interaction quality and application flexibility.

- 5Data privacy, artificial intelligence governance, and medical device regulations increasingly influence procurement decisions.

- 6Competition is shifting toward integrated hardware-software ecosystems supported by recurring software and service revenues.

The social robots market comprises physically embodied robotic systems designed to interact with humans through speech, facial expressions, gestures, and contextual awareness. Unlike conventional industrial robots that focus on repetitive manufacturing tasks, social robots are developed to support communication, companionship, education, healthcare, customer engagement, and public-facing services. Advances in artificial intelligence, natural language processing, computer vision, speech recognition, cloud connectivity, and embedded computing have expanded their commercial viability across institutional and consumer applications.

Commercial demand is primarily driven by organizations seeking to improve service quality, address labor shortages, enhance user engagement, and provide personalized interactions at scale. Healthcare providers are deploying social robots to assist elderly individuals with daily routines, medication reminders, cognitive stimulation, and patient engagement. Educational institutions use interactive robots to improve STEM learning outcomes, language education, and individualized instruction. Retailers, hospitality providers, museums, airports, and public agencies are evaluating robotic assistants to manage repetitive customer interactions while allowing employees to focus on higher-value responsibilities.

Purchasing decisions differ substantially across end-user industries. Healthcare organizations emphasize clinical reliability, data privacy, patient acceptance, interoperability with digital health systems, and long-term technical support. Educational institutions evaluate curriculum compatibility, ease of programming, multilingual capability, and maintenance costs. Commercial service providers prioritize return on investment, customer satisfaction metrics, software upgrade capability, and integration with existing customer relationship management platforms.

The industry structure combines specialized robotics manufacturers with software developers, artificial intelligence providers, sensor suppliers, and system integrators. Hardware remains a substantial contributor to project value because advanced sensors, cameras, processors, mobility platforms, and actuators account for significant production costs. However, software subscriptions, cloud-based analytics, artificial intelligence updates, and maintenance contracts are becoming increasingly important revenue sources throughout the operational lifecycle.

Technology adoption has accelerated as improvements in speech recognition accuracy, emotion detection, edge computing, and cloud-based learning enable more natural human-robot interactions. Buyers increasingly favor modular platforms capable of receiving software enhancements without replacing core hardware, reducing total ownership costs while extending deployment life. The availability of application programming interfaces (APIs) also enables organizations to customize robots for industry-specific workflows.

Supply chain considerations remain an important purchasing factor. Semiconductor availability, sensor procurement, battery technologies, and precision component manufacturing influence production schedules and pricing. Consequently, manufacturers are expanding supplier diversification strategies while increasing regional assembly capabilities to improve delivery reliability and mitigate geopolitical risks.

Market Drivers

Growing demand for elderly care assistance

Population aging has increased pressure on healthcare systems, caregivers, and long-term care facilities. Many countries continue to experience shortages of nursing staff, creating demand for technologies that supplement—not replace—human caregivers. Social robots support medication reminders, cognitive exercises, companionship, mobility assistance, and communication with family members.

Healthcare providers increasingly procure robotic solutions that improve patient engagement while reducing caregiver workload. Manufacturers are responding by incorporating emotion recognition, multilingual communication, and remote monitoring capabilities, expanding commercial opportunities within assisted living facilities and home healthcare programs.

Expansion of customer-facing automation

Retail, hospitality, transportation hubs, and public service organizations seek consistent customer engagement while managing operational costs. Social robots provide information services, visitor guidance, multilingual assistance, and appointment management without replacing complex human decision-making.

Buyers increasingly evaluate robots based on integration with digital kiosks, reservation systems, loyalty platforms, and customer analytics. Suppliers therefore compete through software interoperability, deployment flexibility, and industry-specific application packages rather than hardware specifications alone.

Improvements in artificial intelligence capabilities

Natural language processing, speech recognition, computer vision, and machine learning have substantially improved conversational accuracy and contextual understanding. These developments reduce interaction errors while expanding the range of practical commercial applications.

Organizations increasingly expect robots to recognize user intent, maintain conversational continuity, and personalize interactions. Vendors invest heavily in software development because improved intelligence creates opportunities for recurring subscription revenues alongside initial hardware sales.

Increased investment in educational technologies

Educational institutions continue expanding interactive learning environments that improve student participation and digital literacy. Social robots support coding education, language instruction, autism intervention programs, and collaborative classroom activities.

Procurement decisions increasingly consider curriculum compatibility, ease of teacher training, software update availability, and classroom durability. Manufacturers therefore develop programmable platforms suitable for both primary education and advanced robotics instruction.

Market Restraints and Challenges

High acquisition and lifecycle costs

Although hardware prices have gradually declined, complete deployments remain capital-intensive. Organizations must account for installation, customization, software licensing, employee training, maintenance, cybersecurity updates, and replacement components.

Budget-sensitive institutions may delay purchases despite operational benefits. Vendors increasingly address this challenge through leasing models, robotics-as-a-service offerings, and subscription-based software licensing.

Privacy and cybersecurity concerns

Social robots collect voice recordings, facial images, behavioral information, and interaction data. Organizations deploying these systems must comply with privacy legislation while maintaining secure storage and transmission of sensitive information.

Healthcare providers, educational institutions, and public agencies face particularly stringent compliance requirements. Manufacturers therefore invest in encrypted communications, local data processing, user consent mechanisms, and regular security updates.

Human acceptance and trust

Successful deployment depends on user willingness to interact with robotic systems. Acceptance varies across age groups, cultures, and application settings. Poor conversational quality or inconsistent behavior can reduce engagement and affect investment returns.

Suppliers increasingly conduct user-centered design studies, improve emotional expression capabilities, and provide customizable personalities that align with local cultural expectations.

Technical integration complexity

Enterprise buyers frequently require integration with electronic health records, customer management platforms, scheduling software, payment systems, or educational applications. Integration challenges increase deployment costs and project timelines.

Manufacturers mitigate these issues by providing standardized APIs, cloud management platforms, and partnerships with enterprise software providers.

Major Segment Analysis

Healthcare and Elderly Care Remains the Leading End-User Segment

Healthcare and elderly care represent the most commercially influential segment because demographic trends continue expanding demand for long-term care services while healthcare workforce shortages persist across numerous developed economies.

Hospitals, rehabilitation centers, nursing homes, and home healthcare providers increasingly deploy social robots for patient engagement, rehabilitation exercises, emotional support, cognitive therapy, and routine communication. Rather than replacing healthcare professionals, these systems supplement clinical teams by managing repetitive interactions and supporting continuous patient engagement.

Procurement decisions emphasize reliability, regulatory compliance, infection control, multilingual communication, interoperability with healthcare information systems, and long-term technical support. Buyers also prioritize software update capability because artificial intelligence functionality continues improving throughout the product lifecycle.

Competition within this segment extends beyond robotic hardware. Vendors differentiate through healthcare-specific software applications, remote monitoring services, clinical partnerships, cybersecurity capabilities, and integration with digital health platforms. Long-term maintenance contracts and software subscriptions strengthen recurring revenue while improving customer retention.

Regional Analysis

North America

North America maintains strong demand supported by advanced healthcare infrastructure, technology adoption, university research, and commercial investment in artificial intelligence. Healthcare providers, airports, retailers, and hospitality operators continue evaluating robotic assistants to improve service delivery while addressing workforce shortages. Strict cybersecurity and privacy regulations influence procurement specifications, encouraging suppliers to strengthen compliance capabilities.

Europe

European adoption benefits from aging demographics, industrial automation expertise, and public investment in robotics research. Educational institutions and healthcare organizations represent major buyers, while privacy legislation influences system architecture and data management practices. Organizations increasingly prioritize transparent artificial intelligence systems and responsible deployment practices.

Asia Pacific

Asia Pacific represents both a major manufacturing base and an important demand center. China, Japan, South Korea, Singapore, and Taiwan maintain extensive robotics ecosystems supported by government innovation programs, electronics manufacturing capabilities, and artificial intelligence investment. Aging populations in Japan and South Korea further stimulate demand for elderly care applications, while expanding service industries support commercial deployment across retail and hospitality.

Middle East & Africa

Governments across Gulf countries continue investing in digital public services, smart city initiatives, healthcare modernization, and tourism infrastructure, creating opportunities for customer-facing robotic solutions. Adoption remains selective because implementation costs and technical expertise vary across countries, although premium hospitality and healthcare facilities increasingly evaluate social robotics applications.

Competitive Landscape

Competition within the social robots market combines established robotics developers with specialized artificial intelligence companies focused on human-machine interaction. Suppliers differentiate through conversational quality, mobility performance, emotional interaction capability, software ecosystems, cloud connectivity, and vertical-specific applications rather than hardware performance alone.

Companies continue expanding partnerships with healthcare providers, educational institutions, research organizations, and enterprise software vendors to strengthen commercialization opportunities. Geographic expansion increasingly relies on local distribution partners and system integrators capable of providing implementation, customization, and after-sales support.

Software capabilities are becoming a major competitive differentiator because buyers increasingly expect continuous functionality improvements throughout the product lifecycle. Vendors therefore invest in artificial intelligence model development, multilingual communication, cybersecurity enhancements, and remote fleet management platforms that generate recurring revenue beyond hardware sales.

Recent Developments

June 2026: UBTECH Robotics introduced on-device AI with natural conversation, human-like facial expressions, and long-term companionship functions in its latest home humanoid robot, marking a significant expansion into consumer social robotics.

February 2026: Agibot demonstrated humanoid robots in a large-scale AI-powered entertainment showcase ahead of China's Lunar New Year, highlighting social interaction, education, and entertainment capabilities for consumer-facing robotics applications.

January 2026: SoftBank Robotics continued expanding enterprise service robot deployments through regional partner collaborations supporting hospitality and customer service automation. The initiative increases market reach while strengthening recurring service opportunities.

Regulatory and Policy Environment

The regulatory framework governing social robots continues expanding as artificial intelligence adoption increases across healthcare, education, and public services. Data protection regulations require organizations to implement secure handling of personal information collected through voice recognition, facial recognition, and behavioral monitoring.

Medical applications may require compliance with healthcare device regulations depending on intended functionality, while educational deployments must satisfy child privacy requirements and institutional cybersecurity standards. International standards governing robot safety, functional reliability, and human-machine interaction continue supporting procurement consistency across commercial deployments.

Governments also continue supporting robotics research through innovation funding, university collaboration programs, artificial intelligence strategies, and advanced manufacturing initiatives. These programs encourage commercialization while promoting responsible deployment, cybersecurity resilience, and trustworthy artificial intelligence development.

Outlook and Strategic Implications

Between 2026 and 2031, investment priorities are expected to shift toward intelligent software platforms capable of supporting continuous learning, multilingual communication, emotional interaction, and seamless enterprise integration. Buyers will increasingly evaluate total lifecycle value instead of initial acquisition cost, creating opportunities for subscription-based software, predictive maintenance, and robotics-as-a-service business models.

Healthcare, education, hospitality, and public service organizations are likely to remain the primary commercial buyers because these sectors continue balancing service quality with workforce availability. Procurement decisions will increasingly emphasize cybersecurity, regulatory compliance, software interoperability, and long-term vendor support.

Competitive positioning will depend on artificial intelligence performance, ecosystem partnerships, application specialization, and recurring service capabilities rather than standalone hardware innovation. Companies capable of combining reliable robotic platforms with adaptable software architectures and industry-specific solutions are expected to strengthen their commercial position while responding to evolving customer requirements and regulatory expectations.

Social Robots Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 7.4 billion |

| Total Market Size in 2031 | USD 26.7 billion |

| Forecast Unit | Billion |

| Growth Rate | 29.3% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Product Type, Key Technology, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

By Product Type

By Key Technology

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

4.1. Artificial Intelligence and Generative AI

4.2. Natural Language Processing

4.3. Computer Vision

4.4. Emotion Recognition and Human-Robot Interaction

4.5. Edge AI and Autonomous Navigation

5. SOCIAL ROBOTS MARKET BY COMPONENT

5.1. Introduction

5.2. Hardware

5.3. Software

5.4. Services

6. SOCIAL ROBOTS MARKET BY PRODUCT TYPE

6.1. Introduction

6.2. Companion Robots

6.3. Educational Robots

6.4. Healthcare and Elderly Care Robots

6.5. Customer Service Robots

6.6. Entertainment Robots

6.7. Telepresence Robots

6.8. Others

7. SOCIAL ROBOTS MARKET BY KEY TECHNOLOGY

7.1. Introduction

7.2. Natural Language Processing (NLP)

7.3. Machine Learning

7.4. Computer Vision

7.5. Speech Recognition

7.6. Emotion Recognition

7.7. Others

8. SOCIAL ROBOTS MARKET BY END-USER

8.1. Introduction

8.2. Healthcare and Elderly Care

8.3. Education

8.4. Retail

8.5. Hospitality

8.6. Media and Entertainment

8.7. Public Services

8.8. Others

9. SOCIAL ROBOTS MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. USA

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. Germany

9.4.2. France

9.4.3. United Kingdom

9.4.4. Italy

9.4.5. Spain

9.4.6. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. UAE

9.5.3. Israel

9.5.4. Others

9.6. Asia Pacific

9.6.1. China

9.6.2. Japan

9.6.3. South Korea

9.6.4. India

9.6.5. Australia

9.6.6. Singapore

9.6.7. Taiwan

9.6.8. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Product Portfolio Analysis

10.4. Mergers, Acquisitions, Agreements, and Collaborations

10.5. Competitive Dashboard

11. COMPANY PROFILES

11.1. SoftBank Robotics

11.2. UBTECH Robotics Corp. Ltd.

11.3. Blue Frog Robotics

11.4. Intuition Robotics, Inc.

11.5. Furhat Robotics AB

11.6. Hanson Robotics Limited

11.7. Aeolus Robotics Corporation

11.8. Knightscope, Inc.

11.9. PAL Robotics

11.10. Engineered Arts Limited

11.11. Temi Global Ltd.

11.12. Embodied, Inc.

12. APPENDIX

12.1. Currency

12.2. Assumptions

12.3. Base and Forecast Years Timeline

12.4. Key Benefits to the Stakeholders

12.5. Research Methodology

12.6. Abbreviations

Navigate

Trusted by the world's leading organizations