Report Overview

UK 5G Network Infrastructure Highlights

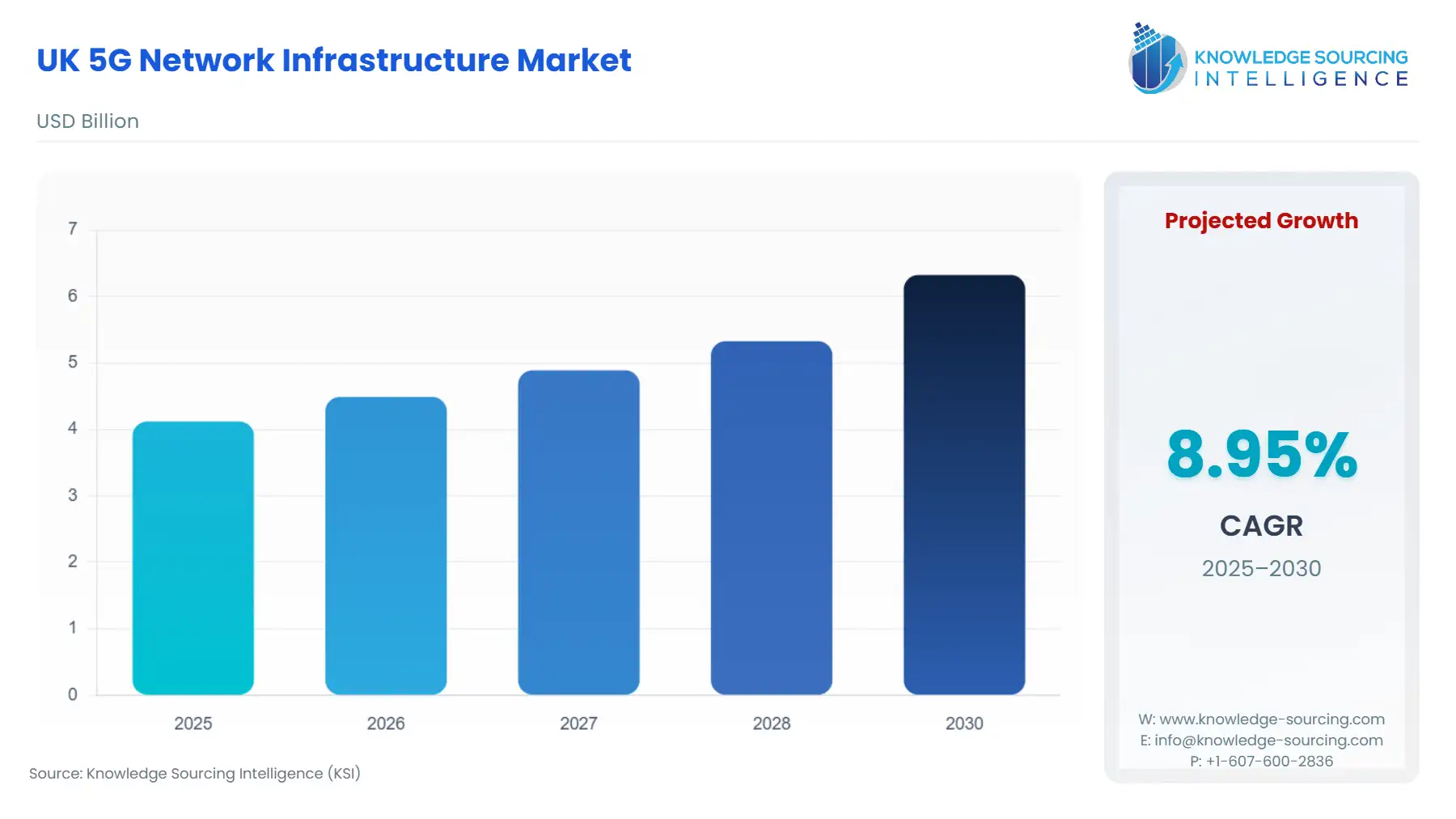

UK 5G Network Infrastructure Market Size:

The UK 5G Network Infrastructure market is forecast to grow at a CAGR of 9.0%, reaching USD 6.3 billion in 2031 from USD 4.1 billion in 2026.

The UK 5G Network Infrastructure market is transitioning from an initial, capacity-driven Non-Standalone deployment phase to a more complex, services-led Standalone paradigm. This evolution is fundamentally shifting investment from basic radio access network (RAN) build-out towards the integration of sophisticated core and edge computing elements necessary to monetize the technology's ultra-low latency and network slicing capabilities.

The market dynamic is uniquely shaped by a blend of aggressive government-backed coverage targets, a robust regulatory framework focused on supply chain security and diversification, and MNO consolidation activity aimed at achieving the scale required for capital-intensive national infrastructure deployment. The confluence of these factors creates an imperative for network operators to accelerate their transformation into fully converged, software-centric service providers.

________________________________________________________________

UK 5G Network Infrastructure Market Analysis

Growth Drivers

The imperative for high-speed connectivity, particularly the government's ambitious 5G coverage and gigabit broadband targets, propels core demand. The commitment to deliver Standalone (SA) 5G services—as opposed to Non-Standalone, which overlays 5G on existing 4G core—directly increases the demand for new 5G Core Network software and hardware capable of supporting advanced functions like ultra-low latency and massive machine-to-machine communications. Furthermore, the strategic investment in the Shared Rural Network to enhance 4G geographic coverage to 95% of the UK landmass creates a direct demand pull for cost-effective, multi-mode RAN infrastructure that can be upgraded to 5G in previously underserved rural locations. The increasing commercial availability of private 5G networks further catalyzes demand for Edge Infrastructure and Network Management and Orchestration tools by enabling dedicated, mission-critical enterprise applications in sectors like manufacturing and logistics.

Challenges and Opportunities

The primary challenge constraining market expansion is the substantial capital expenditure required for network densification, particularly the rollout of high-frequency mmWave spectrum infrastructure, which necessitates a significantly higher volume of small cells compared to mid-band deployment. This financial constraint creates an opportunity for Shared Infrastructure models, where operators pool resources, thereby reducing individual CapEx and accelerating deployment. The regulatory mandate to remove and restrict certain high-risk vendors presents a concurrent challenge by imposing significant migration costs, yet it generates a clear opportunity and corresponding demand increase for new, diversified RAN and Core vendors, particularly those offering Open RAN solutions to lower vendor lock-in.

Raw Material and Pricing Analysis

The UK 5G Network Infrastructure Market fundamentally relies on the supply chain for complex electronic components, which are highly sensitive to global raw material pricing. Key hardware elements—Radio Units, Baseband Units, and Core Network Servers—are heavily dependent on essential materials, including rare earth elements for specialized magnets in antennas, high-purity copper for connectivity, and various semiconductor components. The global supply chain volatility and the geopolitical constraints on semiconductor fabrication capacity impose pricing pressure and lengthen lead times for hardware components. This instability directly influences MNO procurement strategies, increasing demand for software-defined and virtualised components, such as cloud-native 5G Core, which rely less on proprietary physical hardware and offer more flexible pricing models (e.g., subscription-based Network Management and Orchestration).

Supply Chain Analysis

The 5G network infrastructure supply chain is globally distributed, with core production hubs primarily situated in East Asia (semiconductor manufacturing, precision electronics) and Scandinavia/North America (network equipment design and software). Logistical complexities stem from the highly specialized nature of components and the dependency on just-in-time delivery for complex site build-outs. A critical dependency exists on a limited number of global Tier 1 vendors (e.g., Ericsson, Nokia, Samsung) for high-end RAN and Core systems, a factor the UK government is actively seeking to mitigate through its vendor diversification strategy. This reliance, coupled with the long lead times for bespoke equipment, means any disruption to manufacturing or shipping rapidly impacts the market's ability to meet aggressive rollout schedules, creating a structural constraint on deployment speed.

UK 5G Network Infrastructure Market Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

|---|---|---|

United Kingdom | The Telecommunications (Security) Act 2021 | Directly increases demand for compliant network gear and services from diversified vendors. Forces MNOs to undertake substantial capital expenditure for network replacement, specifically within the RAN and Core Network segments, and necessitates new investment in security and compliance software (part of Network Management and Orchestration). |

United Kingdom | Ofcom (Office of Communications) | Ofcom's spectrum management, including the award of low-band (700 MHz), mid-band (3.4-3.8 GHz), and the upcoming mmWave (26/40 GHz) licenses, is the primary growth catalyst for new RAN equipment across all frequency bands. Release of mmWave spectrum in 2025 directly stimulates demand for high-density Edge Infrastructure and small cells in urban centres. |

United Kingdom | Shared Rural Network (SRN) Initiative | The joint government/MNO commitment for 4G geographic coverage to 95% of the UK landmass by the end of 2025 creates a sustained, mandated demand for multi-RAN and Transport Network equipment in Total Not-Spot areas, effectively expanding the addressable market beyond profitable urban centres. |

________________________________________________________________

UK 5G Network Infrastructure Market Segment Analysis

By Component: 5G Core Network

The 5G Core Network segment represents a pivotal growth area due to the industry's shift from Non-Standalone (NSA) to Standalone (SA) architecture. NSA allowed MNOs to launch initial 5G services by leveraging the existing 4G core, limiting new infrastructure demand. Conversely, the transition to SA, a strategy embraced by all major UK operators, is the sole pathway to monetizing the full potential of 5G, particularly ultra-low latency and network slicing. This necessitates a fundamental replacement or parallel deployment of the core network with cloud-native, software-defined infrastructure. The growth driver is rooted in the enterprise sector's need for differentiated, assured services, such as dedicated slices for connected and autonomous vehicles or real-time industrial automation (Manufacturing and Industrial Automation end-user). This commercial imperative directly drives operator demand for new 5G Core Network function software, including Access and Mobility Management Function (AMF), Session Management Function (SMF), and User Plane Function (UPF), alongside associated Network Management and Orchestration solutions to dynamically manage these virtualised resources. The security and vendor diversification mandates further accelerate the replacement cycle, ensuring sustained capital investment in this segment.

By End-User: Manufacturing and Industrial Automation

The Manufacturing and Industrial Automation end-user segment is poised to become a significant, high-value growth driver for private 5G Network deployments and dedicated network slicing capacity within public carrier networks. The necessity is intrinsically linked to the segment's digital transformation imperative, focusing on Industry 4.0 applications that require guaranteed quality of service (QoS) and ultra-reliable low latency communication (URLLC). Industrial use cases, such as real-time control of automated guided vehicles (AGVs), predictive maintenance using thousands of IoT sensors, and high-definition video analytics for quality assurance, cannot be reliably served by public 4G or Wi-Fi. This technical limitation directly translates into demand for bespoke private 5G network infrastructure, including dedicated RAN, small-scale Core Network functions deployed on-premise, and Edge Infrastructure for localized data processing. The economic value is high as these deployments represent operational expenditure savings and increased productivity for manufacturers, thus validating the CapEx for specialized, high-performance infrastructure equipment that is distinct from the mass-market mobile broadband rollout.

________________________________________________________________

UK 5G Network Infrastructure Market Competitive Environment and Analysis

The UK 5G Network Infrastructure market presents a hybrid competitive structure, defined by a highly consolidated Mobile Network Operator (MNO) landscape and a more diverse, but constrained, equipment vendor ecosystem. The MNO space is dominated by major players like BT Group (via EE), Vodafone Group Plc, and Three UK, all of whom are engaged in massive capital investment programs and, in the case of Vodafone and Three, pursuing a merger to achieve the scale necessary to sustain national build-out. The equipment vendor segment is heavily influenced by the UK government's vendor diversification strategy, which has created opportunities for non-traditional and Open RAN suppliers. This regulatory-driven upheaval in the supply chain forces MNOs to broaden their procurement base, thereby intensifying competition among infrastructure providers.

BT Group plc (via EE)

BT Group plc (via EE) holds a strong competitive position anchored by its substantial spectrum holdings across low, mid, and high bands, and its long-standing presence as the UK's largest mobile operator. The company's strategy focuses on network convergence, integrating its 5G network with its fixed fibre infrastructure to create a single, seamless, 'smart converged network.' Their product strategy, evidenced by the rollout of 5G Standalone (5G+) and a vast small cell program, aims to deliver higher reliability and capacity in dense urban environments and for critical enterprise customers.

Ericsson Limited

Ericsson Limited maintains a critical strategic position as one of the two main remaining Tier 1 suppliers permitted in the UK's network core and a major supplier of RAN equipment. The company's competitive advantage is its portfolio of high-performance Radio Access Network (RAN) equipment and its cloud-native 5G Core solutions. Their strategy is deeply aligned with MNO migration towards 5G Standalone, as demonstrated by the September 2025 announcement of a multibillion-pound contract with VodafoneThree to power a majority of their next-generation network, confirming their role as a principal infrastructure partner during the nation's mandated security and technology transition.

________________________________________________________________

UK 5G Network Infrastructure Market Developments:

September 2025: VodafoneThree Signs Multibillion-Pound Investment Deals with Ericsson and Nokia. The newly formed VodafoneThree entity announced a definitive agreement for an unprecedented £11 billion network investment plan, which includes selecting Ericsson and Nokia to deliver part of the infrastructure. This commitment is front-loaded, with the goal of nearly three-quarters of the population having access to the fastest 5G speeds in year one and 90% access to 5G Standalone (5G SA) in year three, accelerating the deployment schedule for 5G Core Network and high-capacity RAN equipment.

July 2024: Virgin Media O2 (VMO2) Reports Substantial Progress in Shared Rural Network (SRN). VMO2 announced that the Glencoe Mountain Resort became the 227th site to benefit from improved 4G coverage as part of the SRN programme, highlighting the successful deployment of new masts in challenging rural locations across the UK. This infrastructure build, which brings 4G to new areas, lays the essential backhaul and physical site infrastructure groundwork for eventual 5G upgrades, supporting the long-term expansion of the Transport or Backhaul Network segment.

________________________________________________________________

UK 5G Network Infrastructure Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 4.12 billion |

| Total Market Size in 2031 | USD 6.3258 billion |

| Growth Rate | 8.95% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Spectrum Band, Deployment Type, End User |

| Companies |

|

UK 5G Network Infrastructure Market Segmentation

BY COMPONENT

RAN

5G Core Network

Transport or Backhaul Network

Edge Infrastructure

Network Management and Orchestration

Others

BY SPECTRUM BAND

Low-band (<1 GHz)

Mid-band (1-6 GHz)

High-band/ mmWave (>24 GHz)

BY DEPLOYMENT TYPE

Public Carrier Networks

Private 5G Networks

Shared Infrastructure

Hybrid

BY DEPLOYMENT MODE

Standalone

Non-Standalone

BY END-USER

Telecom Operators

Manufacturing and Industrial Automation

Transportation & Logistics

Energy and Utilities

Healthcare

Education

Retail and Hospitality

Public Sector

Other Enterprises