Report Overview

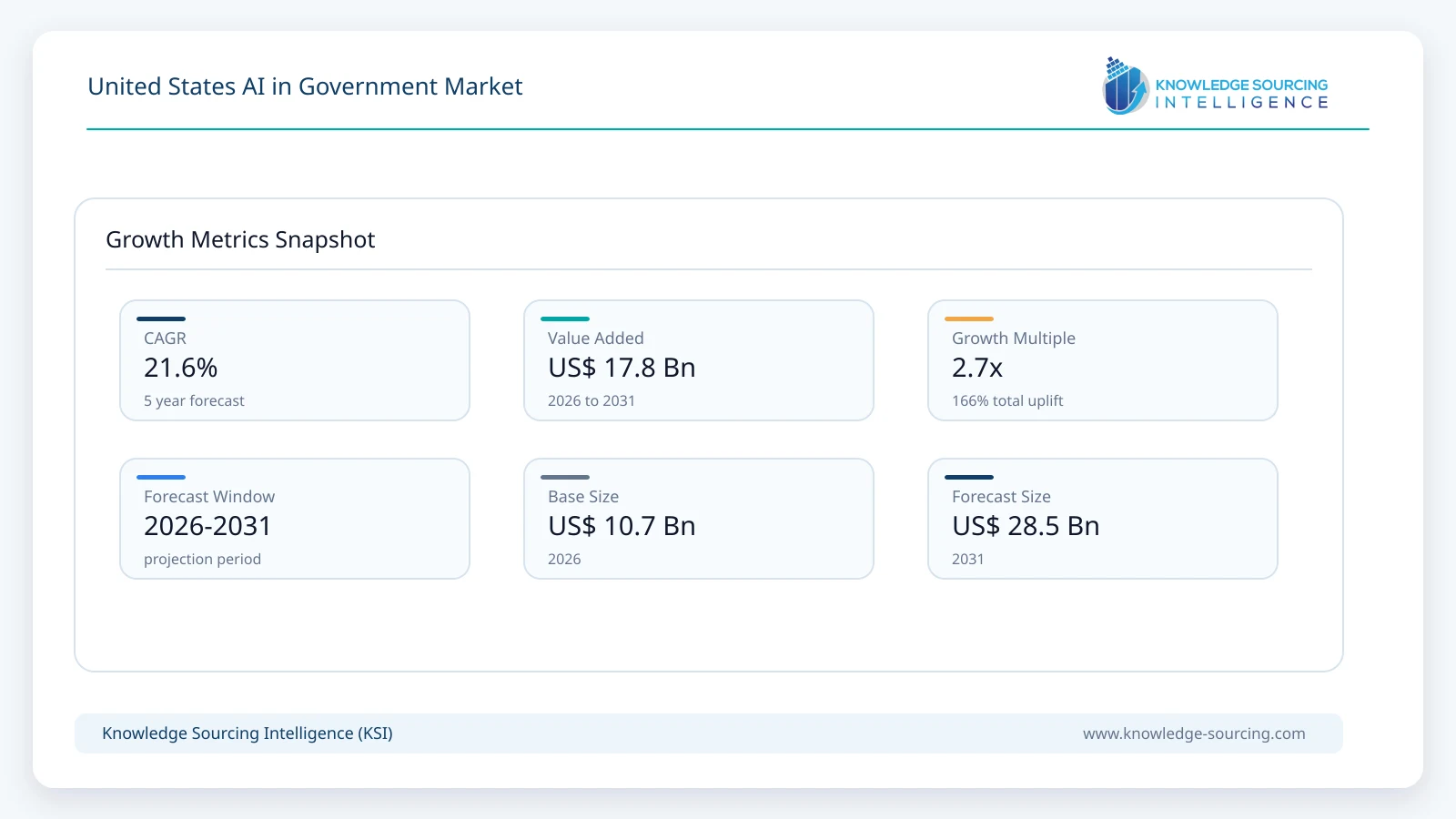

The US AI in Government Market is forecast to grow at a CAGR of 21.6%, reaching USD 28.5 billion in 2031 from USD 10.7 billion in 2026.

Highlights:

- 1Growing federal investment in AI-enabled public administration and national security remains the principal demand catalyst.

- 2Software represents the leading offering segment because agencies prioritize scalable analytics, automation, and decision-support capabilities.

- 3Defense, cybersecurity, and citizen service modernization continue to generate substantial procurement opportunities.

- 4Machine learning remains the most widely implemented technology owing to its versatility across fraud detection, predictive analytics, and operational planning.

- 5Federal responsible AI policies and cybersecurity regulations increasingly influence procurement specifications.

- 6Competition increasingly depends on integration expertise, cloud compatibility, regulatory compliance, and long-term managed services.

The United States AI in Government market comprises artificial intelligence software, hardware infrastructure, and professional services deployed by federal, state, and local government agencies to improve public administration, national security, regulatory enforcement, public service delivery, and operational efficiency. The market encompasses machine learning, natural language processing (NLP), deep learning, and computer vision technologies integrated into mission-critical government workflows, ranging from defense intelligence and cybersecurity to healthcare administration and transportation management.

Demand is being shaped by agencies seeking to process expanding volumes of structured and unstructured data while addressing workforce shortages, rising cybersecurity threats, and increasing citizen expectations for digital public services. AI adoption has moved beyond pilot initiatives toward agency-wide modernization programs supported by dedicated funding, cloud migration strategies, and enterprise data platforms. Procurement decisions increasingly prioritize secure, explainable, and interoperable AI systems capable of operating within highly regulated government environments.

Federal agencies remain the largest purchasers due to sizeable technology modernization budgets and national security requirements. However, state governments and municipal authorities are expanding investments in AI-powered citizen engagement, traffic management, fraud detection, and emergency response systems. Procurement frameworks increasingly emphasize compliance with cybersecurity standards, responsible AI principles, domestic cloud hosting, and integration with existing enterprise software ecosystems.

The supplier ecosystem includes global technology providers, enterprise software vendors, defense contractors, consulting organizations, and specialized AI platform developers. Competition extends beyond algorithm performance to include implementation capabilities, lifecycle support, regulatory compliance expertise, and long-term service contracts. Multi-year procurement cycles encourage vendors to establish strategic partnerships with cloud providers, systems integrators, and government contractors to improve bidding competitiveness.

Growing investment in data governance has become an important revenue driver. Agencies increasingly recognize that AI deployment depends on high-quality datasets, secure infrastructure, and standardized information management. As a result, demand extends beyond AI software licenses to include consulting, cloud migration, workforce training, cybersecurity services, and AI lifecycle management.

Government buyers also place considerable emphasis on transparency and accountability. Purchasing decisions increasingly evaluate explainability, auditability, bias mitigation, and compliance with emerging federal AI governance requirements. Vendors capable of documenting model performance and maintaining continuous monitoring gain competitive advantages in government procurement processes.

Market Drivers

Expansion of Federal AI Modernization Programs

Federal agencies continue allocating resources toward modernizing legacy systems using AI-enabled analytics and automation. Agencies managing taxation, public benefits, immigration, healthcare, and transportation seek improved operational efficiency without proportionally expanding their workforce. Buyers increasingly favor enterprise AI platforms capable of integrating with existing cloud infrastructure while meeting federal security requirements. Suppliers respond by expanding government-certified cloud offerings, implementation services, and governance capabilities, strengthening recurring revenue opportunities through long-term modernization contracts.

Rising Cybersecurity Requirements Across Government Networks

Public-sector organizations face escalating cyber threats targeting critical infrastructure, defense assets, and citizen information. AI enables continuous network monitoring, anomaly detection, automated incident response, and predictive threat intelligence, reducing investigation times and improving security operations. Procurement increasingly favors platforms combining AI with zero-trust security architectures and real-time analytics. Vendors demonstrating interoperability with existing cybersecurity frameworks gain stronger positions during competitive government procurement.

Demand for Efficient Citizen Service Delivery

Government agencies continue facing pressure to reduce administrative complexity while improving accessibility for citizens. AI-powered virtual assistants, document processing, multilingual communication, and workflow automation shorten service delivery times and improve operational consistency. Procurement decisions increasingly emphasize measurable improvements in response time, case management, and administrative cost reduction. This encourages suppliers to develop configurable AI applications tailored to government service environments rather than generic enterprise software.

Increasing Availability of Government Data Infrastructure

Large-scale cloud adoption and enterprise data modernization programs provide stronger foundations for AI deployment. Agencies investing in secure data lakes, standardized records management, and cloud-native applications create favorable conditions for advanced analytics. Vendors increasingly bundle AI software with consulting, governance, and integration services to address implementation complexity. The resulting ecosystem supports sustained demand for both technology platforms and professional services.

Market Restraints and Challenges

Data Governance and Information Quality Constraints

Many agencies continue operating fragmented legacy databases developed across multiple decades. Inconsistent data standards reduce model accuracy and increase implementation timelines. Organizations often require extensive data cleansing before deploying AI solutions, increasing project costs and delaying expected returns. Suppliers increasingly provide data engineering services to address these implementation barriers.

Regulatory and Ethical Compliance Requirements

Government agencies operate under strict transparency, privacy, and accountability obligations. AI systems supporting public decisions require explainability, audit trails, and bias assessment before deployment. Compliance activities extend procurement cycles and increase implementation costs for both buyers and vendors. Suppliers investing in responsible AI governance frameworks are better positioned to satisfy evolving procurement requirements.

Workforce Capability Gaps

Successful AI deployment requires personnel capable of managing models, validating outputs, and interpreting analytical results. Many agencies continue facing shortages of AI specialists and data scientists. This increases reliance on external consulting firms while raising long-term operating costs. Vendors increasingly provide workforce training, managed services, and low-code AI platforms to reduce technical barriers.

Budget Allocation and Procurement Complexity

Government procurement processes often involve lengthy approvals, competitive bidding requirements, and fiscal budget limitations. Multi-year procurement cycles can delay commercialization despite strong technology demand. Suppliers mitigate these challenges by offering modular deployment approaches, subscription pricing, and phased implementation strategies aligned with government budgeting practices.

Major Segment Analysis

Software

Software represents the most commercially important segment because government organizations increasingly prioritize enterprise AI platforms that improve operational decision-making without requiring extensive hardware replacement. Demand spans predictive analytics, document intelligence, conversational AI, cybersecurity analytics, fraud detection, and mission planning applications.

Government buyers evaluate software based on security certifications, scalability, interoperability, explainability, and compatibility with existing cloud environments. Rather than purchasing isolated AI applications, agencies increasingly seek integrated platforms capable of supporting multiple departments through centralized governance and standardized model management.

Competition within the software segment depends heavily on implementation flexibility, compliance capabilities, and lifecycle management. Vendors differentiate through prebuilt government workflows, configurable AI models, and integration with enterprise resource planning, cybersecurity platforms, and cloud infrastructure. Subscription licensing, continuous software updates, and managed services generate recurring revenue while strengthening long-term customer relationships. As agencies continue consolidating technology platforms, software providers with broad government portfolios remain well positioned to secure multi-year procurement agreements.

Competitive Landscape

The United States AI in Government market demonstrates competition among enterprise software providers, global consulting firms, defense contractors, cloud technology companies, and specialized AI developers, including Accenture plc, Microsoft Corporation, IBM Corporation, C3.ai, Inc., SAS Institute Inc., DataRobot, Inc., Deloitte Touche Tohmatsu Limited, Palantir Technologies Inc., RTX Corporation, and DigitalAI.

Competitive positioning depends on government security credentials, implementation experience, cloud partnerships, regulatory compliance, and integration capabilities rather than algorithm performance alone. Vendors increasingly combine software platforms with consulting, managed services, cybersecurity expertise, and workforce training to strengthen customer retention.

Strategic collaborations with federal agencies, defense organizations, hyperscale cloud providers, and systems integrators remain central to business expansion. Companies also invest in responsible AI capabilities, model governance, explainability, and secure deployment architectures to address evolving procurement requirements. Geographic presence across federal, state, and local government markets further enhances competitive positioning by enabling localized implementation support and long-term service delivery.

Recent Developments

March 2026: Palantir announced additional government AI platform deployments supporting operational planning and mission decision-making within U.S. public-sector organizations. Commercial relevance: reinforces demand for enterprise-scale AI platforms in defense and government operations.

February 2026: The U.S. Department of the Treasury announced a public-private AI cybersecurity and risk management initiative, releasing resources developed with government and industry partners to support secure AI adoption across the U.S. financial sector.

April 2025: Microsoft expanded sovereign AI and government cloud capabilities supporting U.S. public-sector organizations with enhanced security, compliance, and AI services. Commercial relevance: strengthens secure AI deployment across federal agencies.

Regulatory and Policy Environment

The regulatory environment continues evolving as federal agencies establish governance frameworks for trustworthy AI deployment. Executive directives promoting responsible AI use require agencies to evaluate safety, transparency, privacy, and accountability before operational implementation. Procurement increasingly incorporates risk assessment, documentation, human oversight, and continuous monitoring requirements throughout AI system lifecycles.

Cybersecurity compliance remains equally important. Government buyers require adherence to federal cybersecurity frameworks, cloud authorization programs, data protection standards, and secure software development practices. Contractors serving defense and civilian agencies increasingly align products with federal security certification requirements to remain eligible for procurement opportunities.

Government modernization initiatives further encourage standardized data management, cloud adoption, and interoperable digital infrastructure. These policies improve implementation consistency while expanding demand for consulting, integration, governance, and lifecycle management services supporting enterprise AI adoption.

Outlook and Strategic Implications

The United States AI in Government market is expected to remain supported by sustained modernization spending, expanding cybersecurity requirements, and continued investment in data-driven public administration. Procurement strategies are expected to shift toward enterprise-wide AI platforms capable of supporting multiple agencies through standardized governance and secure cloud infrastructure.

Investment priorities will increasingly emphasize explainable AI, cybersecurity integration, automated compliance monitoring, and data quality improvement. Buyers are also expected to prioritize suppliers capable of delivering measurable operational outcomes alongside regulatory compliance and long-term technical support.

Competition is likely to intensify around trusted implementation capabilities rather than standalone AI functionality. Vendors combining secure software platforms, consulting expertise, systems integration, workforce training, and responsible AI governance will remain better positioned to secure multi-year government contracts.

Although regulatory complexity, workforce shortages, and procurement timelines will continue influencing deployment speed, sustained federal investment and expanding public-sector digital modernization programs are expected to create attractive commercial opportunities for technology providers throughout the forecast period.

United States AI in Government Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 10.7 billion |

| Total Market Size in 2031 | USD 28.5 billion |

| Forecast Unit | Billion |

| Growth Rate | 21.6% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Offering, Technology, Application |

| Companies |

|

Market Segmentation

By Offering

By Technology

By Application

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter's Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. UNITED STATES AI IN GOVERNMENT MARKET BY OFFERING

5.1. Introduction

5.2. Hardware

5.3. Software

5.4. Services

6. UNITED STATES AI IN GOVERNMENT MARKET BY TECHNOLOGY

6.1. Introduction

6.2. Machine Learning

6.3. Deep Learning

6.4. Natural Language Processing (NLP)

6.5. Computer Vision

7. UNITED STATES AI IN GOVERNMENT MARKET BY APPLICATION

7.1. Introduction

7.2. Public Safety and Security

7.3. Cybersecurity

7.4. Citizen Services

7.5. Defense and Intelligence

7.6. Transportation and Smart Infrastructure

7.7. Healthcare and Public Health

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Accenture plc

9.2. Microsoft Corporation

9.3. IBM Corporation

9.4. C3.ai, Inc.

9.5. SAS Institute Inc.

9.6. DataRobot, Inc.

9.7. Deloitte Touche Tohmatsu Limited

9.8. Palantir Technologies Inc.

9.9. RTX Corporation

9.10. DigitalAI

10. APPENDIX

10.1. Currency

10.2. Assumptions

10.3. Base and Forecast Years Timeline

10.4. Key Benefits for Stakeholders

10.5. Research Methodology

10.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations