Report Overview

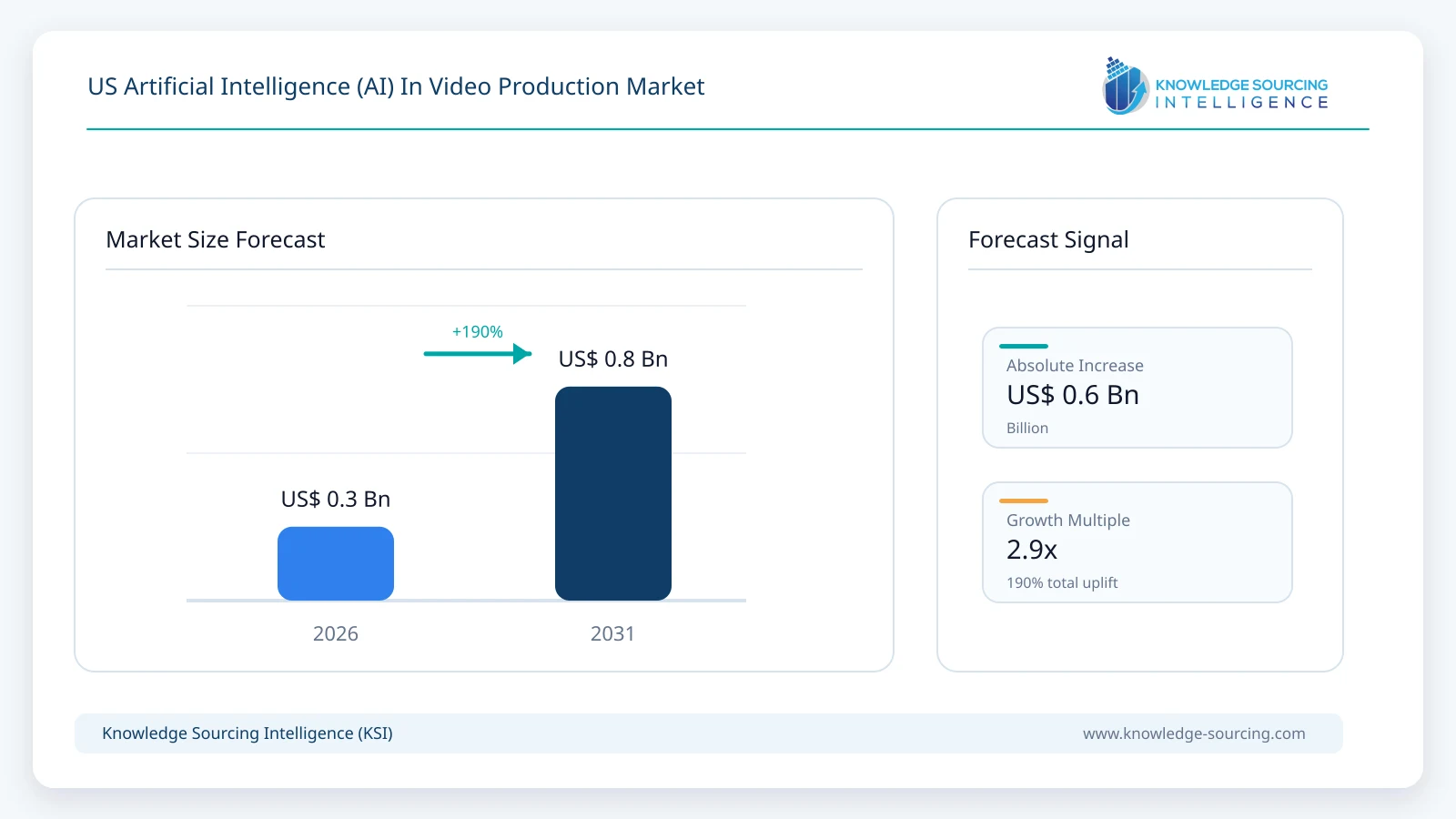

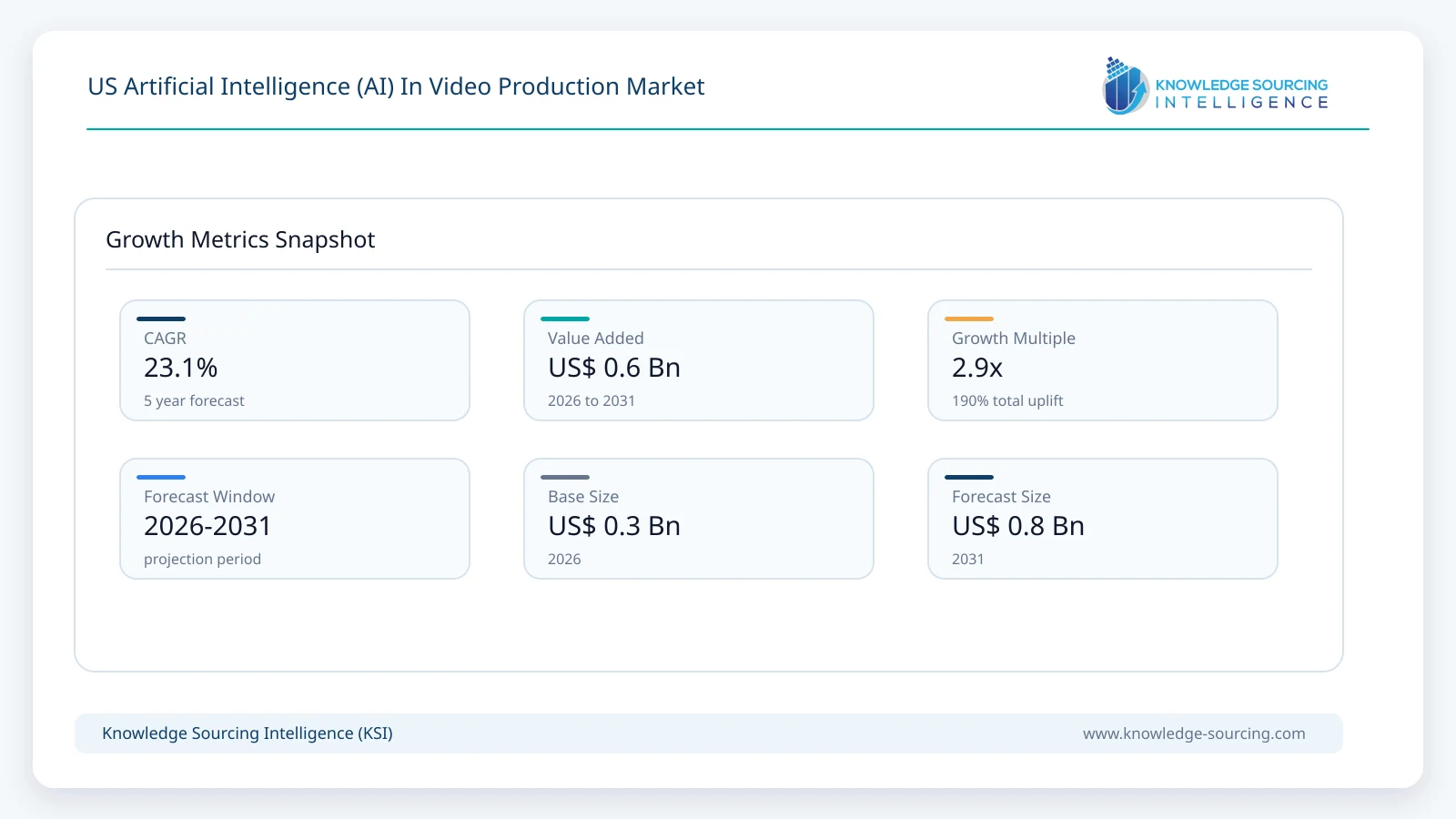

The US artificial intelligence in video production market is set to reach USD 0.84 billion in 2031, growing at a CAGR of 23.1% from USD 0.29 billion in 2026.

Highlights:

- 1The explosive demand for online content, driven by short-form social media and direct-to-consumer streaming services, directly compels production entities to adopt AI for hyper-efficient content generation and localization, fundamentally increasing the market size.

- 2Major technology vendors, including Adobe and Blackmagic Design, are embedding powerful generative AI features, such as smart tracking and scene extension, directly into widely used post-production software, shifting the point of purchase from specialized tools to mainstream platform subscriptions.

- 3Regulatory uncertainty from the U.S. Copyright Office regarding the copyrightability of purely AI-generated video outputs drives mandatory demand for AI tools that provide auditable provenance, authorship tracking, and clear separation of human-edited vs. synthetic content.

- 4Leading media and entertainment companies, exemplified by Netflix's internal adoption, are deploying AI for complex, high-stakes tasks like de-aging and complex VFX substitution, demonstrating AI's shift from a novelty tool to a mission-critical component for cost-effective, large-scale video production.

The US Artificial Intelligence (AI) in Video Production Market encompasses software and services that leverage machine learning, computer vision, and generative models to automate, enhance, and create video content across all phases of the production lifecycle from script analysis (pre-production) to automated editing (production) and generative visual effects (post-production). This market is currently defined by a radical disruption caused by the maturity of Generative AI, transitioning AI's role from a simple efficiency tool for tasks like transcription and color correction to a creative partner capable of synthesizing entirely new visual and audio assets. The economic pressure to produce high-quality, high-volume content while managing production costs acts as the core driver, forcing enterprises and content creators to invest in AI platforms that compress timelines and expand creative scope without proportional increases in human labor.

US Artificial Intelligence (AI) In Video Production Market Analysis:

Growth Drivers

The insatiable consumer demand for personalized and localized video content is the primary propellant. Streaming services and digital marketers require content variation across thousands of geographic and demographic segments, compelling a direct investment in AI solutions that automate versioning, localization (e.g., lip-sync adjustment, automated dubbing), and content optimization, thereby creating new demand for the Services and Post-Production segments. Second, the commoditization of high-performance computing (HPC) via cloud platforms has lowered the entry barrier for computationally intensive generative AI. This increased accessibility enables smaller studios and individual creators to deploy advanced models, democratizing access to professional-grade tools and significantly broadening the demand base for AI-driven software. Lastly, the imperative to reduce time-to-market for video campaigns and content releases drives demand for AI tools that accelerate the most time-consuming processes, such as intelligent asset management, automated rough cuts, and speech-to-text editing.

Challenges and Opportunities

A significant market challenge is the ethical and legal ambiguity surrounding synthetic media and deepfakes, which fosters distrust and limits adoption in news and sensitive corporate communications. This constraint, however, presents a clear opportunity: mandatory demand for AI solutions focused on content authentication, digital watermarking, and provenance tracking to establish trust. Another headwind is the high cost and specialized expertise required to train, fine-tune, or host proprietary high-fidelity generative models. This capital barrier creates a major opportunity for Software-as-a-Service (SaaS) providers who offer pay-per-use, pre-trained, and continuously updated models, converting high fixed costs into scalable operational expenses and expanding the user base among Enterprises and Content Creators.

Supply Chain Analysis

Since the US AI in Video Production Market is primarily a software and service offering, its supply chain is intangible, centered on data, models, and computational infrastructure. The core dependencies are the cloud infrastructure providers (Amazon, Google, Microsoft) that supply the vast GPU and TPU compute clusters essential for training and running large generative video models. The supply chain hub is therefore concentrated in major US data center regions. A critical dependency is the availability and licensing of training data, which dictates the quality and ethical foundation of the AI models; this resource is global and complex to manage. Tariffs on specialized camera sensors and post-production hardware manufactured overseas increase the capital expenditure for production studios, dampening the demand for high-end AI Video Software subscriptions. Logistical complexities arise from managing data privacy compliance across different jurisdictions when sourcing training material. This structural dependency on cloud HPC for processing power and massive datasets for model creation makes the market highly sensitive to cloud pricing and data regulatory shifts.

Government Regulations:

Regulations and guidance, though nascent, are primarily focused on consumer protection, ethical use, and intellectual property, all of which directly shape the demand profile for AI video production tools.

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

|---|---|---|

Federal | U.S. Copyright Office (USCO) Guidance | The USCO's report, confirming that purely AI-generated content lacks human authorship, and therefore cannot be copyrighted, decreases demand for fully autonomous "text-to-video" systems for commercial use. It simultaneously increases demand for AI tools that facilitate human modification and arrangement of AI outputs to meet the "human authorship" requirement for copyright protection. |

Federal | Federal Communications Commission (FCC) Rules | The FCC confirmed that AI-generated voices constitute "artificial or prerecorded voice" under the Telephone Consumer Protection Act (TCPA). This mandates prior express consent for their use in telemarketing, which restricts the demand for AI voice cloning and generation in marketing video campaigns for regulated sectors. |

Federal | Federal Trade Commission (FTC) | The FTC uses its authority against deceptive practices. The risk of FTC enforcement against video content that misrepresents real people or products (e.g., AI deepfakes in advertising) generates mandatory demand for AI tools that incorporate clear disclosure and forensic watermarking capabilities to mitigate legal risk. |

US Artificial Intelligence (AI) In Video Production Market Segment Analysis:

By Application: Film & TV

The Film & TV segment presents a substantial and high-value demand center, driven by the imperative for visual complexity at lower marginal costs. The demand is specifically catalyzed by the studio system's need to produce "tentpole" content that is rich in computer-generated imagery (CGI) and visual effects (VFX) without the proportional escalation of human labor and time associated with traditional VFX pipelines. AI tools are increasingly procured to automate intermediate VFX steps: rotoscoping, object tracking, background replacement, and complex post-production tasks like digital de-aging (as verified by Netflix's use). This demand for AI is not about simple automation but about enabling a level of visual quality and speed previously unattainable. The industry utilizes AI to shorten the asset creation-to-final-shot cycle, directly converting production timeline constraints into demand for specialized AI software and services.

By End-User: Content Creators

The Content Creators segment is defined by a high-volume, rapid-turnaround content demand model where speed and consistency are prioritized over the ultra-high fidelity required for feature films. The specific demand driver is the need for velocity and variety in short-form content creation. Creators require AI tools that can perform immediate, streamlined post-production tasks like automatic subtitle generation, dynamic re-framing for multiple social platforms (e.g., vertical video optimization), and automatic background music selection/mixing. The accessibility and low-cost nature of these AI tools enable creators to exponentially increase their content output without hiring full production teams. This segment’s demand is focused heavily on SaaS models and integrated platform features that simplify the workflow from raw footage capture to multi-platform distribution.

US AI in Video Production Market Competitive Environment and Analysis:

The competitive landscape is characterized by a battle between established software giants integrating AI into their platforms and agile startups building next-generation, pure-play generative tools. Market share is segmented primarily by the production stage (editing vs. generative) and the price point (professional suite vs. creator SaaS).

Adobe

Adobe maintains a dominant strategic position by integrating its proprietary AI technology, Adobe Sensei and Firefly, directly into its industry-standard Creative Cloud applications like Premiere Pro and After Effects. This strategy focuses on providing seamless, feature-based upgrades that leverage AI for high-impact editing tasks such as Generative Extend (which lengthens clips non-destructively) and advanced audio editing tools. Adobe’s extensive user base and platform lock-in generate demand by offering AI capabilities as a natural extension of existing, mission-critical workflows, effectively requiring editors to adopt the AI features to remain competitive without migrating to a new platform.

Blackmagic Design

Blackmagic Design competes by embedding powerful, GPU-accelerated AI tools directly into its single, comprehensive post-production suite, DaVinci Resolve. Its strategy centers on providing end-to-end, high-performance capabilities, including color grading, editing, and VFX, at a lower cost barrier than subscription-based competitors. Verifiable features like IntelliTrack AI and UltraNR noise reduction drive demand by offering professional-grade automation and image quality enhancements within an integrated environment, specifically targeting high-end colorists and editors seeking an integrated, performance-optimized alternative.

US Artificial Intelligence (AI) In Video Production Market Developments:

April 2025: Blackmagic Design Announces DaVinci Resolve 20

Blackmagic Design announced DaVinci Resolve 20, a major update featuring over 100 new tools, including new DaVinci AI features like AI IntelliScript and AI Audio Assistant. This product launch intensifies competition in the Post-Production Process segment by providing advanced, AI-driven automation for script-to-timeline editing and intelligent audio mixing. The addition of such high-level, integrated AI functions creates a compelling migration or upgrade catalyst for post-production professionals seeking integrated workflow efficiencies.

US Artificial Intelligence (AI) In Video Production Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 0.29 billion |

| Total Market Size in 2031 | USD 0.84 billion |

| Forecast Unit | Billion |

| Growth Rate | 23.1% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Process, Application, End-User |

| Companies |

|

Market Segmentation

By Component

By Process

By Application

By End-user

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter's Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. US ARTIFICIAL INTELLIGENCE (AI) IN VIDEO PRODUCTION MARKET BY COMPONENT

5.1. Introduction

5.2. Software

5.3. Services

6. US ARTIFICIAL INTELLIGENCE (AI) IN VIDEO PRODUCTION MARKET BY PROCESS

6.1. Introduction

6.2. Pre-Production

6.3. Production

6.4. Post-Production

7. US ARTIFICIAL INTELLIGENCE (AI) IN VIDEO PRODUCTION MARKET BY APPLICATION

7.1. Introduction

7.2. Marketing & Advertising

7.3. Film & TV

7.4. Social Media Content Creation

7.5. Corporate Training & Education

8. US ARTIFICIAL INTELLIGENCE (AI) IN VIDEO PRODUCTION MARKET BY END-USER

8.1. Introduction

8.2. Media & Entertainment Companies

8.3. Advertising Agencies

8.4. Enterprises

8.5. Content Creators

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. AI Screenwriter

10.2. ToolBaz

10.3. Steve AI

10.4. Elai.io

10.5. GliaStar

10.6. Adobe

10.7. Runway AI

10.8. Synthesia

10.9. FlexChip

10.10. Pictory.ai

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key benefits for the stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations