Report Overview

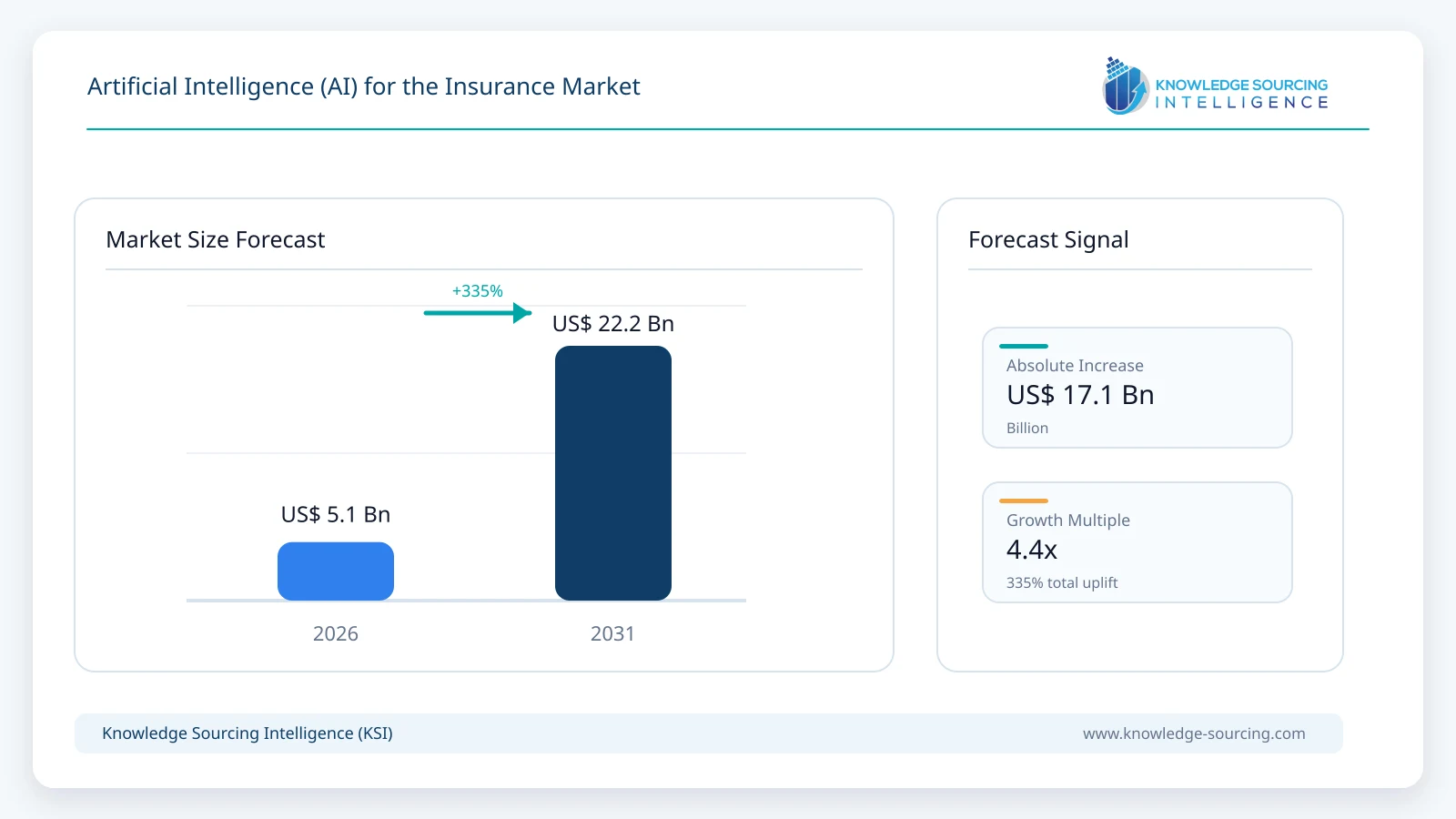

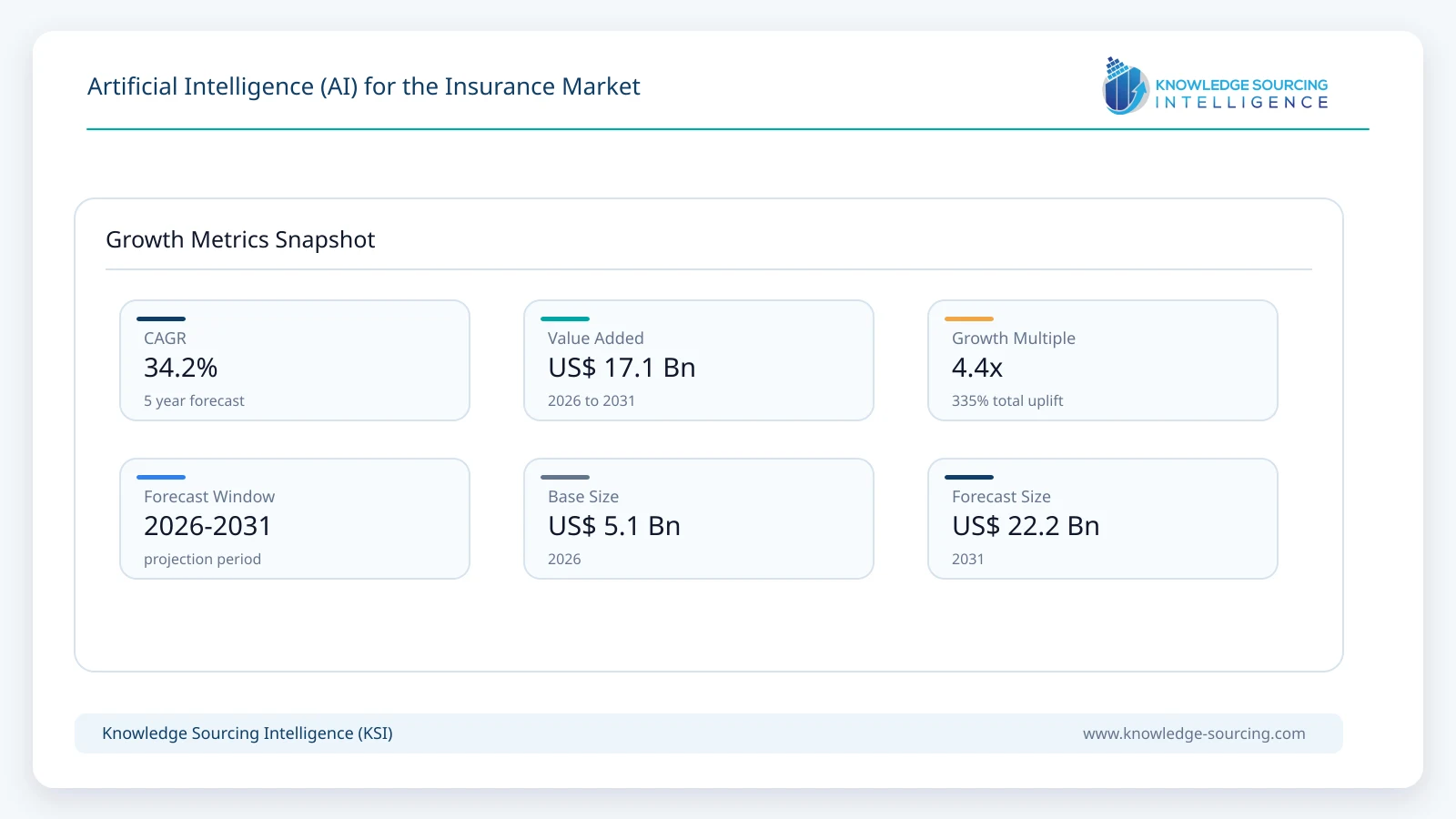

The global AI for Insurance market is forecast to grow at a CAGR of 34.2%, reaching USD 22.2 billion in 2031 from USD 5.1 billion in 2026.

Highlights:

- 1Insurers are deploying agentic AI systemsthat autonomously orchestrate complex workflows across claims processing, underwriting, and policy servicing, moving beyond simple automation to handle end-to-end tasks with minimal human intervention.

- 2AI-powered image recognition and anomaly detectionare transforming fraud identification in claims, enabling insurers to spot manipulated media and suspicious patterns more effectively while supporting human investigators on complex cases.

- 3Advanced AI enhances underwriting accuracyby rapidly analyzing unstructured data, medical records, and risk factors, resulting in more precise risk assessments and personalized policy offerings for customers.

- 4AI-driven chatbots and virtual assistantsare elevating customer service by delivering instant responses, automated claim updates, and tailored interactions, improving overall policyholder experience and operational efficiency.

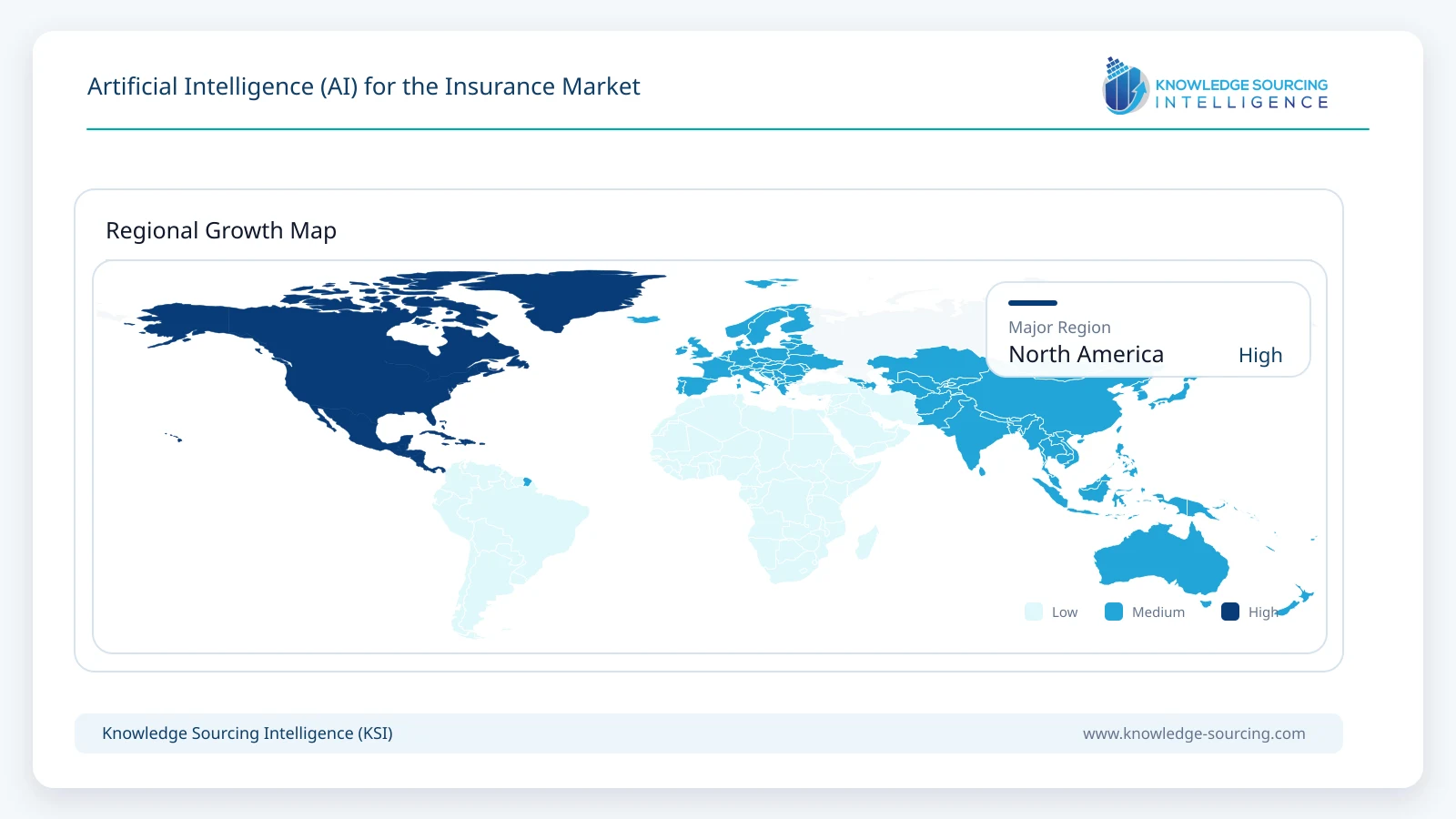

Asia-Pacific is the fastest-growing region due to rapid digital adoption, expanding insurance user base, and strong AI initiatives in countries like India and China.

The solutions segment is expected to be the fastest growing, as insurers increasingly adopt end-to-end AI platforms to automate core operations, enhance decision-making, and scale efficiently.

In 2025, cloud was the major segment by deployment mode, accounting for X% share by value, followed by on-premise, accounting for X% share in the same year.

Cloud deployment is witnessing the highest growth due to its scalability, cost-effectiveness, and ability to support real-time data processing and AI integration.

Generative AI is emerging as the fastest-growing technology segment, driven by its ability to automate content generation, improve customer interactions, and enhance underwriting and claims processes.

Market Dynamics

Drivers

Increasing Need for Operational Efficiency and Cost Reduction

The rising demand for operational efficiency and cost reduction is largely driven by the rapid growth in the number of insurance customers. This trend is significantly accelerating the adoption of Artificial Intelligence (AI) in the sector. The increase in the number of customers due to growing financial awareness, digital penetration, and wider access to insurance products is encouraging insurers to experience an enormous increase in the volume of policies, claims submissions, and customer interactions.

Through the year 2024-25 in India, the insurance segment issued 418.4 million policies, earned the premium income of ?11.93 trillion, made the payment of the claim amount of ?8.36 trillion, and reported the assets managed of ?74.44 trillion as on 31 March 2025.

The overall reinsurance market in India was numbered at ?1.12 lakh crore for the year 2024-25.

Trying to manage such a large scale with traditional, manual methods would be very inefficient, expensive, and could cause delays.

AI enables insurance companies to efficiently handle huge amounts of data and transactions by using automation to perform repetitive tasks like issuing policies, processing claims, and resolving customer questions.

Additionally, AI-powered chatbots and virtual assistants help manage the growing number of customer inquiries in real time, ensuring faster response rates and improved service quality.

Restraints and Opportunities

The laws and regulations involved in the insurance sector could hinder AI for insurance market expansion.

The insurance sector is very closely regulated, and the application of AI technology has to meet multiple laws. This can be quite difficult for insurance firms, sometimes involving a sizeable budget and overall investment. The insurance industry has been one of the slowest sectors in embracing new technology, and some companies tend to resist new technology and innovations. Moreover, while a trend towards more AI in the market is consistently growing, many traditional insurers appear to be prevaricating. At the same time, they assess how much such technology will cost and may expose them to financial risk

Key Developments

November 2025: Aon plc launches “Aon Claims Copilot”, an AI-enabled, integrated claims-advocacy and analytics platform, debuting in Germany in November 2025 and set for global expansion in 2026-27.

November 2025: Monetary Authority of Singapore (MAS) and the Financial Conduct Authority (FCA UK) announce a strategic partnership on AI in finance to enable cross-border testing of AI solutions, regulatory insight sharing, and responsible scaling of frontier models in banking and insurance.

October 2025: Zurich Insurance Group launches its new AI Lab, in partnership with ETH Zurich’s Agentic Systems Lab and the University of St. Gallen; the Lab aims to develop scalable AI solutions to address real-world insurance challenges and redefine what customers expect from insurers.

Market Segmentation

By Application: Fraud Detection

Application-wise, the Artificial Intelligence (AI) for Insurance market is segmented into fraud detection, risk analysis, customer service, claim assessment, and others. Risk analysis is expected to grow steadily, fueled by increasing emphasis of insurers towards accurate decision-making.

Ongoing progress in telematics and IoT device adoption, as well as advances in potential risk and data analysis, have provided new growth prospects for AI adoption in the insurance sector.

Strategic efforts to digitize financial operations, followed by improved preference for personalized insurance, have expanded the market landscape. The fraud detection segment is expected to show considerable growth, fueled by the progressing strength of false digital claims.

High prevalence of DDoS (Distributed Denial of Service) in the insurance sector has played a key role in adopting advanced concepts like AI for real-time detection.

Surge in fraudulent filing costing billions in losses to insurers has accelerated the demand for sophisticated AI-solutions in major regional markets with high prevalence. According to CIFAS “Fraudscape 2026”, nearly 242,000 identity fraud cases were recorded in the National Fraud Database, with insurance cases experiencing 26% growth.

With insurance enrollment witnessing steady growth, the preference for digital solutions to simplify unstructured data to overwhelm manual review is set to amplify market growth.

Global economies like China have emphasizes on adopting smart technologies to minimize fraudulent claims. In 2025, nearly 1,626 institutions in the economy were identified to be involved in medical insurance fraud.

The ongoing product innovations, such as the launch of Experian’s AI-powered “Transactions Forensics” on 22nd April 2026, enable financial service providers, including insurers, to prevent sophisticated financial crimes.

Regional Analysis

North America: the US

Standing at the forefront of global AI spending, the United States holds high potential for LLMs adoption in the insurance sector.

With high insurance enrollment, the emphasis on improving the technological framework with advanced algorithms to improve data analysis and anomaly detection is set to gain traction.

According to the Centers for Medicare & Medicaid Services (CMS), in the 2026 Open Enrollment Period (OEP), nearly 23.1million consumers were automatically enrolled in health insurance coverage, with 68% enrolled by the HealthCare.gov platform.

Research studies like the World Economic Forum’s “AI in Financial Services” have outlined the potential of large language models (LLMs) adoption to streamline automation and augmentation in the US insurance sector.

Major US-based insurance and financial service providers, namely Nationwide Mutual Insurance Company, investing billions to accelerate AI adoption, have amplified the market outlook.

Ongoing regulatory compliance to safeguard consumers’ interests, followed by the launch of generative AI tools like “Insurance Risk Suite AI Assistant” by global fintech players like FIS, has further paved the way for future market expansion.

List of Companies

SoundHound AI, Inc.

Microsoft Corporation

Amazon Web Services, Inc.

IBM Corporation

Avaamo, Inc.

Wipro Limited

Gradient AI

ZestyAI

Shift Technology

FurtherAI

Microsoft Corporation engages in the Artificial Intelligence (AI) in Insurance market primarily through its cloud and AI ecosystem, led by Microsoft Azure. The company provides scalable infrastructure, advanced analytics, and machine learning capabilities that enable insurers to modernize operations across underwriting, claims processing, fraud detection, and customer engagement. Through solutions such as Azure Machine Learning and Azure OpenAI Service, Microsoft supports the development of intelligent automation, predictive risk modeling, and conversational AI applications tailored to insurance workflows.

The company’s strategy focuses on expanding industry-specific cloud offerings, fostering partnerships with Insurtech firms, and delivering end-to-end digital transformation capabilities that enhance operational efficiency and customer experience across the insurance value chain.

Artificial Intelligence (AI) For Insurance Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 5.1 billion |

| Total Market Size in 2031 | USD 22.2 billion |

| Forecast Unit | Billion |

| Growth Rate | 34.2% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Application, Sector, Technology, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

By Deployment Mode

By Technology

By Insurance Type

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. ARTIFICIAL INTELLIGENCE (AI) FOR INSURANCE MARKET BY COMPONENT

5.1. Introduction

5.2. Solutions

5.3. Services

6. ARTIFICIAL INTELLIGENCE (AI) FOR INSURANCE MARKET BY DEPLOYMENT MODE

6.1. Introduction

6.2. Cloud

6.3. On-Premise

7. ARTIFICIAL INTELLIGENCE (AI) FOR INSURANCE MARKET BY TECHNOLOGY

7.1. Introduction

7.2. Machine Learning (ML)

7.3. Natural Language Processing (NLP)

7.4. Generative AI (GI)

7.5. Robotic Process Automation (RPA)

7.6. Others

8. ARTIFICIAL INTELLIGENCE (AI) FOR INSURANCE MARKET BY INSURANCE TYPE

8.1. Introduction

8.2. Life Insurance

8.3. Health Insurance

8.4. Title Insurance

8.5. Others

9. ARTIFICIAL INTELLIGENCE (AI) FOR INSURANCE MARKET BY APPLICATION

9.1. Introduction

9.2. Fraud Detection

9.3. Risk Analysis

9.4. Customer Service

9.5. Claims Assessment

9.6. Others

10. ARTIFICIAL INTELLIGENCE (AI) FOR INSURANCE MARKET BY GEOGRAPHY

10.1. Introduction

10.2. North America

10.2.1. By Component

10.2.2. By Deployment Mode

10.2.3. By Technology

10.2.4. By Insurance Type

10.2.5. By Application

10.2.6. By Country

10.2.6.1. USA

10.2.6.2. Canada

10.2.6.3. Mexico

10.3. South America

10.3.1. By Component

10.3.2. By Deployment Mode

10.3.3. By Technology

10.3.4. By Insurance Type

10.3.5. By Application

10.3.6. By Country

10.3.6.1. Brazil

10.3.6.2. Argentina

10.3.6.3. Others

10.4. Europe

10.4.1. By Component

10.4.2. By Deployment Mode

10.4.3. By Technology

10.4.4. By Insurance Type

10.4.5. By Application

10.4.6. By Country

10.4.6.1. Germany

10.4.6.2. France

10.4.6.3. United Kingdom

10.4.6.4. Spain

10.4.6.5. Others

10.5. Middle East and Africa

10.5.1. By Component

10.5.2. By Deployment Mode

10.5.3. By Technology

10.5.4. By Insurance Type

10.5.5. By Application

10.5.6. By Country

10.5.6.1. Saudi Arabia

10.5.6.2. UAE

10.5.6.3. Israel

10.5.6.4. Others

10.6. Asia Pacific

10.6.1. By Component

10.6.2. By Deployment Mode

10.6.3. By Technology

10.6.4. By Insurance Type

10.6.5. By Application

10.6.6. By Country

10.6.6.1. China

10.6.6.2. Japan

10.6.6.3. India

10.6.6.4. South Korea

10.6.6.5. Indonesia

10.6.6.6. Taiwan

10.6.6.7. Others

11. COMPETITIVE ENVIRONMENT AND ANALYSIS

11.1. Major Players and Strategy Analysis

11.2. Market Share Analysis

11.3. Mergers, Acquisitions, Agreements, and Collaborations

11.4. Competitive Dashboard

12. COMPANY PROFILES

12.1. SoundHound AI, Inc.

12.2. Microsoft Corporation

12.3. Amazon Web Services, Inc.

12.4. IBM Corporation

12.5. Avaamo, Inc.

12.6. Wipro Limited

12.7. Gradient AI

12.8. ZestyAI

12.9. Shift Technology

12.10. FurtherAI

12.11. Corgi Insurance

12.12. Guidewire Software, Inc.

12.13. Majesco

12.14. Duck Creek Technologies LLC

13. LIST OF FIGURES

14. LIST OF TABLES

Navigate

Trusted by the world's leading organizations