Report Overview

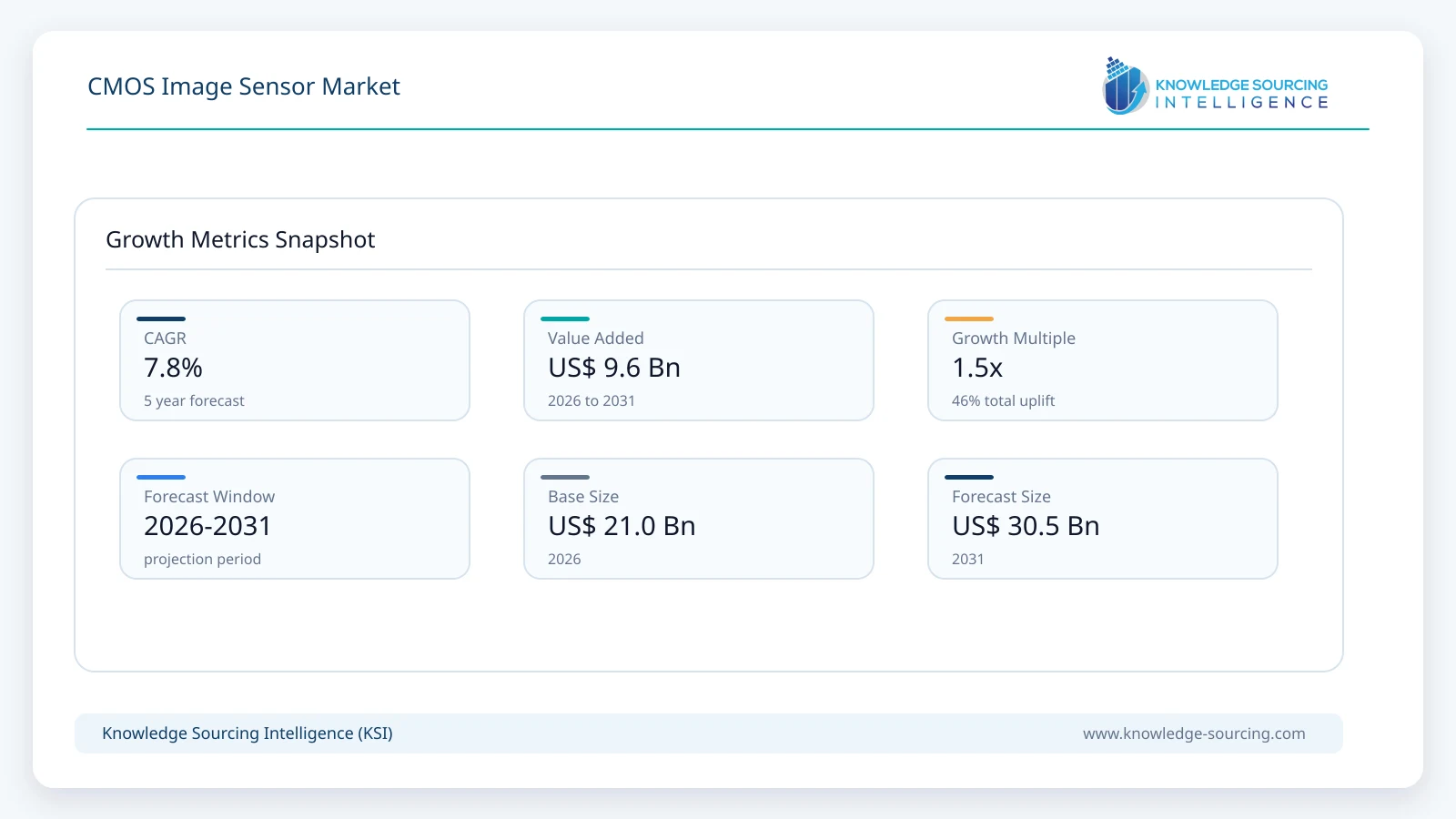

The CMOS Image Sensor market is forecast to grow at a CAGR of 7.8%, reaching approximately USD 30.52 billion in 2031 from USD 20.96 billion in 2026.

Highlights:

- 1Edge AI IntegrationThe requirement for real-time latency in autonomous systems is driving the integration of neural processing units (NPUs) into stacked CIS designs.

- 2Automotive Safety MandatesNew vehicle safety regulations are increasing the average camera count per vehicle, which directly multiplies the volume demand for automotive-grade sensors.

- 3Smartphone Pixel RaceConsumer demand for optical-quality zoom in mobile form factors is pushing manufacturers to release 200MP+ sensors with advanced pixel-binning capabilities.

- 4Industrial AutomationMachine vision requirements for high-speed inspection are shifting demand toward large-format global shutter sensors that support 100+ FPS output.

The CMOS image sensor market operates as a critical sub-sector of the global semiconductor industry, defined by high capital intensity and rapid iterative cycles in pixel miniaturization. Primary demand drivers include the mandatory integration of Advanced Driver Assistance Systems (ADAS) in the automotive sector and the proliferation of multi-camera arrays in premium mobile devices. Regulatory influences, specifically automotive safety mandates in the European Union and North America, are forcing a shift toward global shutter technology to eliminate motion artifacts in high-speed sensing. Strategic importance centers on the "imaging-to-sensing" pivot, where the ability to process data on-chip determines a manufacturer's position in the AI-driven edge computing ecosystem.

Market Dynamics

Drivers

ADAS Proliferation: Regulatory bodies are mandating features like automated emergency braking and lane-keep assist, which rely on continuous visual input. This mandate is forcing automotive OEMs to integrate between 6 and 12 high-resolution sensors per vehicle to achieve 360-degree coverage.

5G-Enabled Mobile Video: High-bandwidth 5G networks are encouraging the consumption of high-definition video content and real-time streaming. Smartphone manufacturers are responding by adopting larger 1-inch format sensors to improve low-light video performance and dynamic range.

Miniaturized Medical Imaging: The healthcare sector is demanding higher-resolution visual data for minimally invasive surgeries and endoscopy. Manufacturers are developing sub-1mm CMOS sensors that enable high-definition visualization within the human body while maintaining low thermal signatures.

Smart City Infrastructure: Urban centers are deploying massive networks of intelligent surveillance cameras for traffic management and public safety. These systems are shifting toward BSI sensors with integrated infrared (IR) capabilities to ensure consistent object recognition in variable lighting conditions.

-

Restraints and Opportunities

Wafer Supply Constraints: The complexity of 3D-stacking requires multiple specialized wafer starts per finished sensor, which increases the burden on global foundry capacity. This constraint is leading to periodic supply imbalances, particularly for 300mm wafers used in high-end mobile and automotive production.

Signal-to-Noise Ratios: As pixel sizes shrink below 0.6 micrometers, thermal noise is increasingly compromising image clarity. This physical limitation is creating an opportunity for "pixel-binning" technologies and AI-based denoising algorithms to maintain signal integrity in compact sensor formats.

Global Shutter Adoption: Traditional rolling shutters create "jello" effects in high-speed industrial environments, which limit the accuracy of automated inspection. The shift toward global shutter architectures is opening significant opportunities in high-speed machine vision and drone-based delivery systems.

Spectral Expansion: Demand is growing for sensors that can perceive beyond the visible spectrum into Short-Wave Infrared (SWIR) and Near-Infrared (NIR). This expansion is enabling new applications in moisture detection for precision agriculture and non-destructive testing in semiconductor manufacturing.

Supply Chain Analysis

The CMOS image sensor supply chain is characterized by a high degree of vertical integration among top-tier players who control both design and fabrication. Raw material procurement focuses on high-purity silicon wafers and specialized chemicals for color filter arrays (CFA) and micro-lens layers. Foundry utilization is currently prioritizing 300mm lines for stacked BSI production, as this process allows for the separate optimization of the photodiode and the logic layers.

Infrastructure constraints are emerging at the back-end assembly and test (OSAT) stage, where the precision required for mounting large-format sensors is exceeding current capacity. Logistics providers are adapting to the high sensitivity of these components by implementing vibration-controlled and temperature-monitored shipping environments. The geopolitical focus on semiconductor sovereignty is prompting companies to diversify their manufacturing footprints, with new fab investments occurring in Europe and North America to serve local automotive and industrial clusters.

Government Regulations

Agency/Body | Regulation/Mandate | Impact on Demand |

European Commission | General Safety Regulation (GSR) | Mandates Intelligent Speed Assistance (ISA) and driver drowsiness monitoring, increasing internal-cabin camera demand. |

US NHTSA | FMVSS 111 (Rear Visibility) | Ensures 100% integration of backup cameras in new vehicles, sustaining high-volume demand for entry-level CMOS sensors. |

ECHA (EU) | PFAS Restriction Proposal | Forces a material shift in sensor coatings and clean-room chemicals, impacting supply chain cost structures. |

China MIIT | Intelligent Connected Vehicles (ICV) Roadmap | Accelerates the adoption of Level 3 autonomy, driving demand for high-dynamic-range (HDR) automotive sensors. |

Key Developments

May 2026: Sony Semiconductor Solutions announced a joint venture with TSMC to co-develop next-generation image sensors at Sony’s Kumamoto plant. This partnership aims to maintain Sony’s global dominance against growing competition from Samsung.

April 2026: Samsung Electronics announced the expansion of its 200MP sensor customer base, targeting flagship smartphone design wins for the second half of the year.

November 2025: Sony Semiconductor Solutions released a 200-megapixel image sensor for mobile applications featuring built-in AI technology to enhance high-powered zoom capabilities.

September 2025: Sony Semiconductor Solutions introduced an industry-leading global shutter CMOS image sensor for industrial use, achieving 105-effective megapixels and 100 FPS output.

Market Segmentation

By Technology

The market structure is defined by the coexistence of Front-Side Illumination (FSI) and Back-Side Illumination (BSI) technologies. FSI architecture remains the standard for cost-sensitive applications like entry-level security cameras and low-cost consumer electronics. However, the limitation of FSI lies in the metal wiring layer, which blocks a portion of the incoming light and reduces quantum efficiency.

BSI technology is currently dominating the high-end mobile and automotive sectors by inverting the sensor structure to place the photodiodes closer to the light source. This shift is enabling the development of smaller pixels without sacrificing signal-to-noise ratios. Stacked BSI variants are now emerging as the primary growth engine, as they allow for the integration of dedicated memory and logic layers. This structural outcome enables real-time high-dynamic-range (HDR) processing and "always-on" sensing capabilities, which are essential for facial recognition and gesture control in mobile devices.

By Image Processing

Traditional 2D image processing remains the cornerstone of standard photographic and surveillance applications. These sensors capture intensity and color information to reconstruct flat images. However, demand is shifting toward 3D sensing technologies, including Time-of-Flight (ToF) and Structured Light. This shift is occurring because 2D data is insufficient for advanced spatial computing and autonomous navigation tasks.

3D image processing enables the sensor to calculate the depth and volume of objects in real-time. This capability is driving the adoption of CMOS sensors in augmented reality (AR) headsets and warehouse robotics. The integration of 3D processing on-chip is reducing the computational load on the main system processor, which lowers overall power consumption. Consequently, the market is seeing a trend where 3D-capable sensors are becoming a standard requirement for premium smartphones to support secure biometric authentication and professional-grade portrait effects.

By End-User

The consumer electronics segment serves as the historical volume anchor for the CMOS market. High-resolution multi-camera arrays in smartphones are maintaining a steady demand for both primary high-resolution sensors and auxiliary wide-angle or macro units. In the automotive sector, demand is intensifying as manufacturers transition from simple rearview cameras to complex ADAS suites.

The security and surveillance industry is currently upgrading from analog to high-definition IP cameras, which requires sensors with superior low-light performance and integrated motion detection. Healthcare is emerging as a high-value niche, where the need for disposable endoscopy sensors is driving the production of ultra-compact CMOS units. Aerospace and defense applications are shifting toward sensors with high radiation tolerance and the ability to operate in extreme temperature ranges. This diversified end-user base is insulating the market from downturns in any single consumer-facing segment.

Regional Analysis

The Asia-Pacific region is maintaining its position as the dominant market for CMOS image sensors due to its massive electronics manufacturing ecosystem. China is currently leading in the consumption of sensors for smartphone assembly and electric vehicle production. The region is benefiting from a dense supply chain that includes major foundries in Taiwan and assembly hubs in Southeast Asia. Domestic manufacturers in China are increasing their production capacity for mid-range sensors, which is putting pricing pressure on established global players in the consumer electronics space.

North America is exhibiting a demand profile centered on high-value automotive and industrial applications. The region is seeing a surge in demand for sensors that support Level 3 and Level 4 autonomous driving systems. US-based automotive OEMs are prioritizing sensors with high dynamic range and global shutter capabilities to meet stringent safety standards. Furthermore, the North American healthcare market is driving the adoption of high-end CMOS sensors for robotic-assisted surgery and diagnostic imaging, where precision and data integrity are paramount.

The European market is defined by its strong industrial automation and automotive sectors. German and French automotive manufacturers are integrating high-resolution vision systems to comply with the European General Safety Regulation. This regulation is forcing a structural shift toward internal cabin monitoring sensors and advanced blind-spot detection. Europe is also a center for the development of "smart factory" infrastructure, where high-speed machine vision sensors are becoming a standard component of automated production lines. The region is emphasizing environmental sustainability, which is encouraging manufacturers to develop low-power sensors that minimize the carbon footprint of data centers and edge devices.

In the Middle East and Africa, demand is being driven by large-scale smart city projects and critical infrastructure security. Urban developments in the Gulf region are deploying high-definition surveillance networks that require sensors capable of operating in high-glare and high-temperature environments. South America is seeing a gradual increase in CMOS demand as Brazil and Argentina expand their local electronics assembly and automotive production capabilities. These emerging markets are currently focusing on entry-level and mid-range sensors, though the transition toward connected vehicle infrastructure is expected to shift demand toward higher-grade components by 2031.

Competitive Landscape

Company List:

Sony Semiconductor Solutions Corporation

Samsung Electronics Co., Ltd.

OmniVision Technologies, Inc.

onsemi

STMicroelectronics

SK Hynix Inc.

Sharp Corporation

Panasonic Corporation

Canon Inc.

Fujifilm Corporation

Company Profiles:

Sony Semiconductor Solutions Corporation

Sony is strategically distinct due to its absolute leadership in stacked BSI technology and its control over the premium mobile sensor market. The company is currently shifting its focus toward "Sensing-at-the-Edge," where it integrates AI processing capabilities directly onto its IMX series sensors. This move is reducing the data transfer requirements for external processors and enabling faster object recognition in autonomous systems. Sony is maintaining its competitive edge by investing in large-format sensors for professional photography and high-speed global shutter units for industrial automation.

Samsung Electronics Co., Ltd.

Samsung is strategically distinct for its vertical integration and its ability to leverage advanced foundry nodes for pixel miniaturization. The company is currently leading the "high-pixel" race by mass-producing 200MP sensors with 0.6µm pixel sizes. This strategy is satisfying the mobile industry's demand for ultra-high-resolution imaging in compact form factors. Samsung is also expanding its "ISOCELL" technology to the automotive sector, where it is developing specialized sensors for ADAS that prioritize high dynamic range and flicker reduction for LED traffic sign recognition.

STMicroelectronics

STMicroelectronics is strategically distinct for its focus on specialized imaging solutions for the automotive and industrial sectors. The company is currently leveraging its own wafer fabs in France to produce high-performance CMOS sensors tailored for driver monitoring and occupancy detection. STMicroelectronics is also a leader in Time-of-Flight (ToF) technology, which is seeing rapid adoption in smart home devices and gesture-based interfaces. By focusing on niche, high-reliability applications, the company is avoiding the direct price competition seen in the high-volume smartphone market.

Analyst View

The CMOS image sensor market is transitioning from a component-level business to a system-on-chip ecosystem. Manufacturers that successfully integrate AI and 3D sensing will capture the highest value in the automotive and industrial segments through 2031.

CMOS Image Sensor Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 20.96 billion |

| Total Market Size in 2031 | USD 30.52 billion |

| Forecast Unit | Billion |

| Growth Rate | 7.8% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Technology, Image Processing, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Technology

- Front Side Illumination (FSI)

- Back Side Illumination (BSI)

By Image Processing

- 3D

- 2D

By End User

- Consumer Electronics

- Security and Surveillance

- Automotive

- Healthcare

- Aerospace and Defence

- Others

By Geography

- North America

- USA

- Canada

- Mexico

- Others

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Others

- Middle East and Africa

- Saudi Arabia

- Israel

- Others

- Asia Pacific

- China

- Japan

- South Korea

- India

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Currency

1.5. Assumptions

1.6. Base and Forecast Years Timeline

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Secondary Sources

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1. Market Segmentation

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Porter's Five Forces Analysis

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Power of Buyers

4.5.3. Threat of New Entrants

4.5.4. Threat of Substitutes

4.5.5. Competitive Rivalry in the Industry

4.6. Life Cycle Analysis - Regional Snapshot

4.7. Market Attractiveness

5. CMOS IMAGE SENSOR MARKET BY TECHNOLOGY

5.1. Front Side Illumination (FSI)

5.2. Back Side Illumination (BSI)

6. CMOS IMAGE SENSOR MARKET BY IMAGE PROCESSING

6.1. 3D

6.2. 2D

7. CMOS IMAGE SENSOR MARKET BY END USER

7.1. Consumer Electronics

7.2. Security and Surveillance

7.3. Automotive

7.4. Healthcare

7.5. Aerospace and Defence

7.6. Others

8. CMOS IMAGE SENSOR MARKET BY GEOGRAPHY

8.1. North America

8.1.1. USA

8.1.2. Canada

8.1.3. Mexico

8.1.4. Others

8.2. South America

8.2.1. Brazil

8.2.2. Argentina

8.2.3. Others

8.3. Europe

8.3.1. Germany

8.3.2. France

8.3.3. United Kingdom

8.3.4. Italy

8.3.5. Others

8.4. Middle East and Africa

8.4.1. Saudi Arabia

8.4.2. Israel

8.4.3. Others

8.5. Asia Pacific

8.5.1. China

8.5.2. Japan

8.5.3. South Korea

8.5.4. India

8.5.5. Others

9. COMPETITIVE INTELLIGENCE

9.1. Company Benchmarking and Analysis

9.2. Recent Investments and Deals

9.3. Strategies of Key Players

10. COMPANY PROFILES

10.1. Sony Semiconductor Solutions Corporation

10.2. Samsung Electronics Co., Ltd.

10.3. OmniVision Technologies, Inc.

10.4. onsemi

10.5. STMicroelectronics

10.6. SK Hynix Inc.

10.7. Sharp Corporation

10.8. Panasonic Corporation

10.9. Canon Inc.

10.10. Fujifilm Corporation

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations