Report Overview

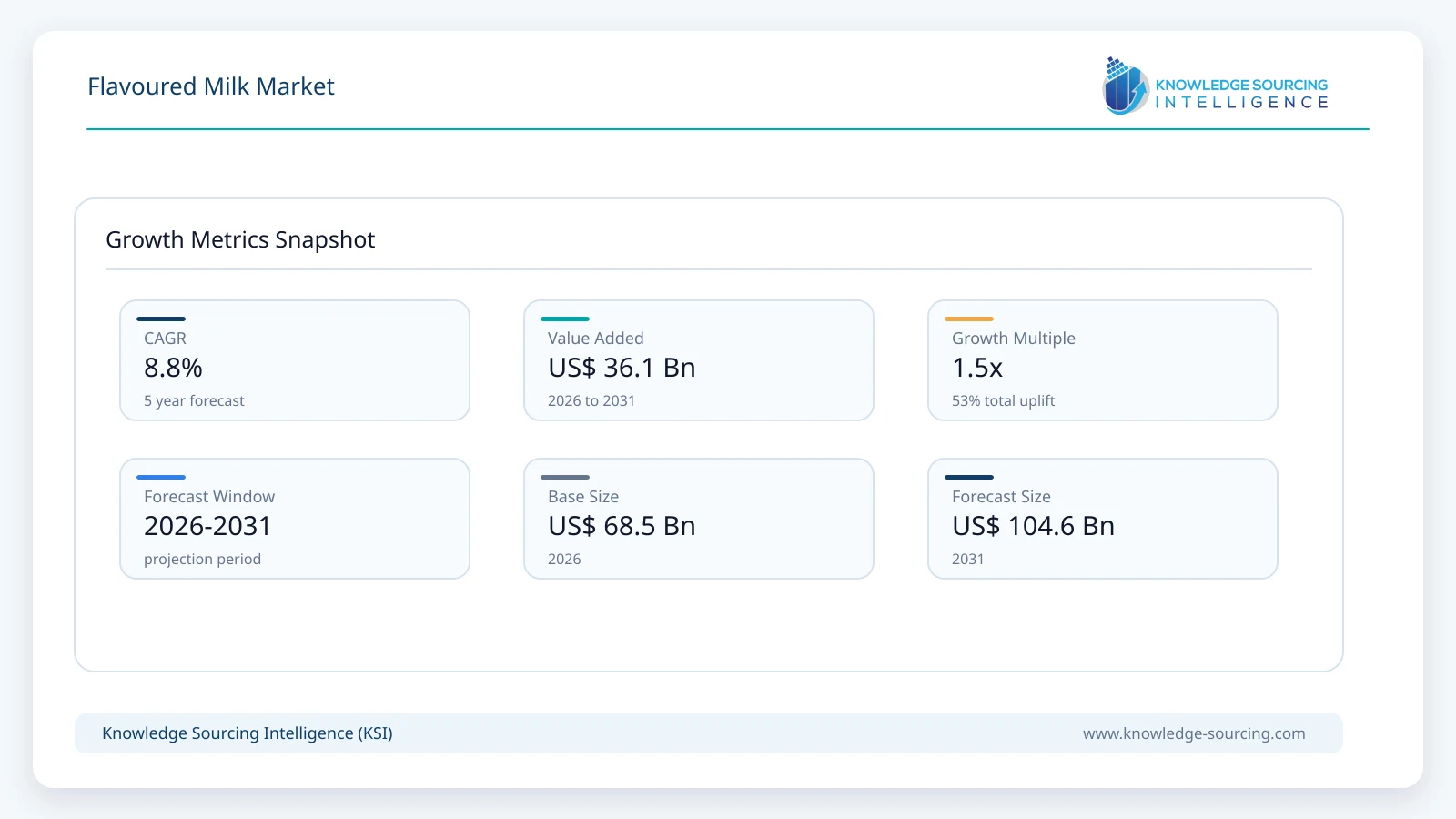

The Global Flavoured Milk market is forecast to grow at a CAGR of 8.8%, reaching USD 104.6 billion in 2031 from USD 68.5 billion in 2026.

Highlights:

- 1Manufacturers are introducing innovative and explosive flavour profiles to meet evolving consumer preferences.

- 2Companies are developing functional flavoured milk products to boost immunity and improve gut health.

- 3Millennials are driving demand for ethnic-inspired and sustainable flavoured milk variants globally.

- 4Brands are expanding distribution channels while launching low-sugar and plant-based flavoured milk options.

Flavored milk is a sweetened dairy beverage made from milk, sugar, and taste profiles, and occasionally, food coloring is also used in its production. It can be offered as a pasteurized, refrigerated product or as an ultra-high-temperature treated product that does not need to be refrigerated. It can also be produced at home and in restaurants by combining flavorings with milk or as a pre-packed product on grocery aisles.

Globally, manufacturers in the flavored milk industry offer new and innovative flavored items to assist the rising demand for creative flavors as customer preferences shift. This incorporates developing flavors that are popular in the region, offering fruit-flavored variations to appeal to younger customers, and presenting flavored milk with increased functional quality. Individuals are seeking to augment their diets with immune-boosting nutrients and enhance their gastrointestinal health by adding fortified dairy products and alternatives with functional claims.

Simultaneously, customers are increasingly drawn to functional items positioned to assist them in relaxing, sleeping better, and boosting their mood to cope with persistent uncertainty, worry, and anxiety, which results in rising consumer demand for functional flavoured milk. Moreover, rising health consciousness has led companies to launch low-sugar or sugar-free alternatives in the flavoured milk category.

Flavoured Milk Market Drivers

Growing demand for new innovative and explosive flavour profiles is augmenting the demand for flavoured milk products

Millennials are demanding ethnic-inspired flavour profiles in flavoured milk products. Such products not only satisfy their taste senses but also provide them with the opportunity to discover another culture and tradition. Shortcakes, figs, pear, tres leeches, thai chili, and pandan are increasingly used in flavoured milk as Asian, Mediterranean, and Latin American flavours combine well with dairy.

Besides, plant-based milk items have prospered in the market exponentially in recent years. Plant-based flavored milk products face fresh competition as they develop new flavours and ingredients. Animal-free dairy milk is developed from whey proteins generated by cellular agriculture globally. This sort of milk is lactose-free and cholesterol-free. The rising number of vegetarian and vegan populations is one of the essential components driving the expansion of plant-based flavored milk. In 2022, the Dutch dairy brand Chocomel possessed by FrieslandCampina, introduced the vegan version of its tremendously well-known chocolate milk in the UK.

Millennials as the targeted audience will bolster the flavoured milk market expansion.

Flavored milk companies have continued introducing new beverages for the millennial demographic. This beverage sector always seeks novel and intriguing flavours and sustainable ones since they are passionate about environmental concerns and enjoy diversity. For instance, in March 2023, DARI® launched MOO'V™, an ultra-filtered, lactose-free, whole-milk beverage in three satisfying flavors. This lactose-free, high-protein, low-sugar beverage offers optimized nutritional benefits for kids. It uses natural flavors to enhance the milk's taste, eliminating the need for additional sugar or added colors. MOO'V™ is a trailblazer in the dairy industry.

Growing accessibility of diverse distribution channels is anticipated to propel the global demand for the flavoured milk market

Supermarkets have traditionally held the significant and most established market share of flavoured milk. Besides, convenience stores cater to impulse purchases and typically offer a smaller selection of flavoured milk options than supermarkets. Other distribution channels include vending machines, gas stations, and diverse alternative retail stores, giving additional options for consumers to get flavoured milk on the go and single-serve choices for travelers.

Specialist stores with outlets specializing in health food, organic items, or dairy items provide a niche market for flavoured milk customers and key market players' expansion. Moreover, online retail channels are seeing an essential rise, giving convenient access to flavored milk products and a possibly broader number of brands and flavours to choose from compared to brick-and-mortar stores.

Flavoured Milk Market Restraints:

Price volatility can be a major hindrance in the flavoured milk market expansion.

Despite its growth potential, the flavoured milk market experiences a few challenges that prevent broader adoption. One challenge is the perception among people that flavoured milk may be costlier than plain milk or alternative refreshments, especially for consumers careful of their budgets.

Furthermore, mounting public well-being concerns regarding sugar consumption, especially among children, provoke guardians to look for healthier beverage alternatives over sugary flavored milk. Besides, the rising demand for clean-label items containing recognizable and natural ingredients can discourage customers from flavoured milk being seen as excessively processed products.

Flavoured Milk Market Geographical Outlook:

APAC is anticipated to hold a significant share of the flavoured milk market.

Asia Pacific region is expected to hold a significant market share in flavoured milk. This region will experience rapid expansion throughout the projection period due to increasing demand for new and innovative flavour profiles for milk products. Flavored milk is in high demand in countries such as India, South Korea, and China.

This region's market is also growing due to the increasing millennial population as well as changing eating habits and rising demand for healthy beverages. In addition, the prevalence of major market players such as Amul, Nestle, Danone, and others also spurs the growth of flavoured milk in this region. The region is also experiencing various launches from niche brands with specialty products and giving tough competition to bigger well-established brands.

Flavoured Milk Market Recent Developments

May 2024- European dairy cooperative Arla Foods partnered with snack company Mondel?z International to produce, distribute, and market chocolate milk under the Milka brand in Germany, Austria, and Poland. The partnership focused on extending Arla Foods' portfolio by leveraging the robust brand recognition and buyer devotion of Milka, leveraging its dairy advancement and quality skill to secure a rise within the mature chocolate milk lineup products.

January 2024- Chartwells K12 launched its Hot Chocolate Milk concept in over 55 pilot schools across the US. The concept offers students a cup of comforting hot chocolate milk served during breakfast and lunch, with various toppings available for customization.

April 2023 - Bega Group launched lactose-free versions of its Dare, Big M, and Dairy Farmers Classic lines. Lactose-free versions included Dare's best-selling double espresso and lactose-free chocolate-flavored milk from Dairy Farmers Classic and Big M.

Flavoured Milk Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 68.5 billion |

| Total Market Size in 2031 | USD 104.6 billion |

| Forecast Unit | Billion |

| Growth Rate | 8.8% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Distribution Channel, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

- Dairy-Based

- Plant-Based

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Stores

- Online Retail Stores

- Other Distribution Channels

By Geography

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- UK

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Thailand

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. FLAVOURED MILK MARKET BY TYPE

5.1. Introduction

5.2. Dairy-Based

5.3. Plant-Based

6. FLAVOURED MILK MARKET BY DISTRIBUTION CHANNEL

6.1. Introduction

6.2. Supermarkets/Hypermarkets

6.3. Convenience Stores

6.4. Specialist Stores

6.5. Online Retail Stores

6.6. Other Distribution Channels

7. FLAVOURED MILK MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. By Type

7.2.2. By Distribution Channel

7.2.3. By Country

7.2.3.1. USA

7.2.3.2. Canada

7.2.3.3. Mexico

7.3. South America

7.3.1. By Type

7.3.2. By Distribution Channel

7.3.3. By Country

7.3.3.1. Brazil

7.3.3.2. Argentina

7.3.3.3. Others

7.4. Europe

7.4.1. By Type

7.4.2. By Distribution Channel

7.4.3. By Country

7.4.3.1. Germany

7.4.3.2. France

7.4.3.3. UK

7.4.3.4. Spain

7.4.3.5. Others

7.5. Middle East and Africa

7.5.1. By Type

7.5.2. By Distribution Channel

7.5.3. By Country

7.5.3.1. Saudi Arabia

7.5.3.2. UAE

7.5.3.3. Israel

7.5.3.4. Others

7.6. Asia Pacific

7.6.1. By Type

7.6.2. By Distribution Channel

7.6.3. By Country

7.6.3.1. China

7.6.3.2. Japan

7.6.3.3. India

7.6.3.4. South Korea

7.6.3.5. Indonesia

7.6.3.6. Thailand

7.6.3.7. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Nestle S.A

9.2. The Hershey Company

9.3. The Farmer's Cow

9.4. Oakhurst

9.5. Dean Food Company

9.6. Fairlife, LLC

9.7. Saputo Inc

9.8. Agropur Dairy Cooperative

9.9. Mondelz International

9.10. The Kraft Heinz Company

9.11. Danone

Navigate

Trusted by the world's leading organizations