Report Overview

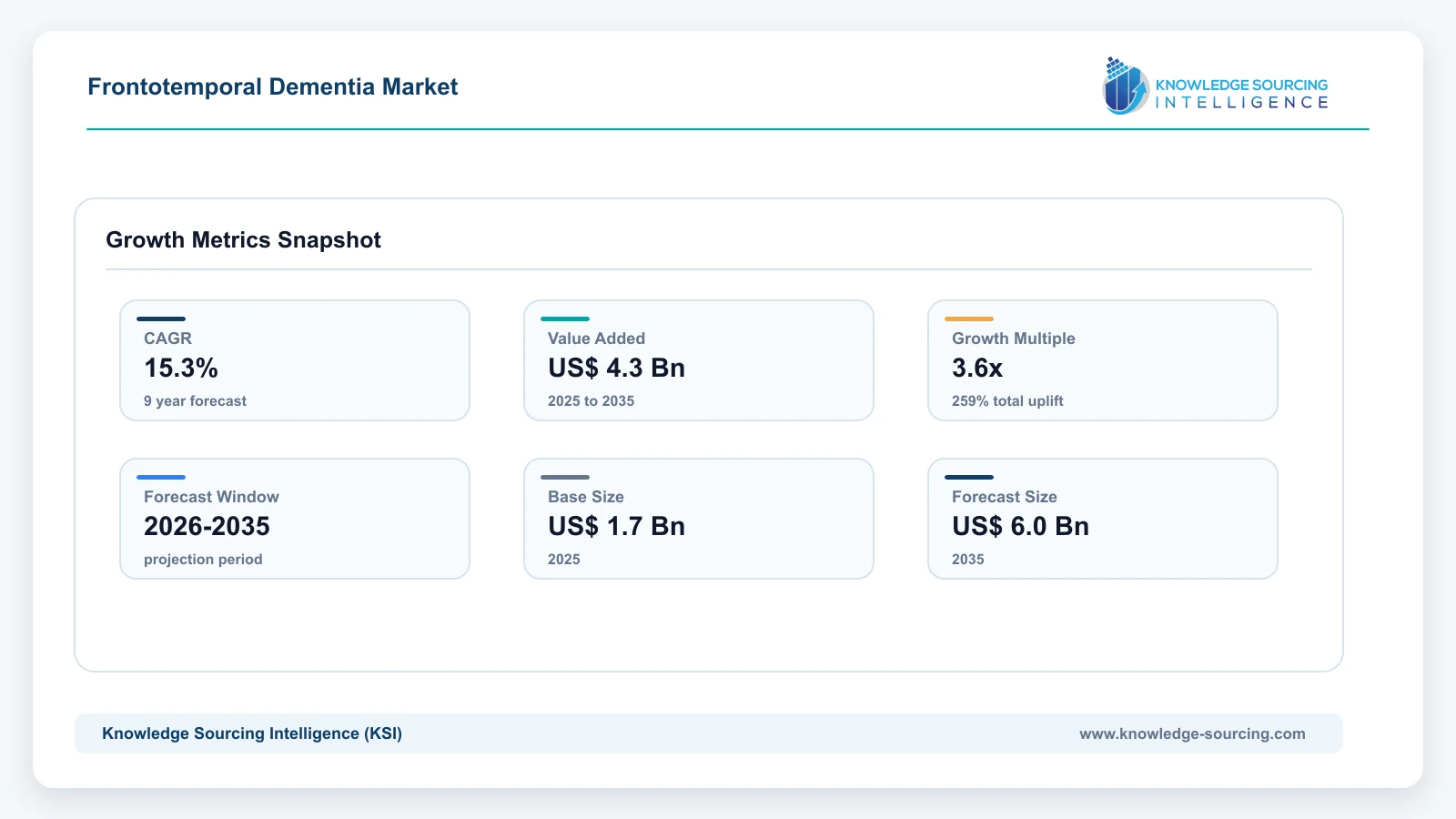

The Frontotemporal Dementia Market is predicted to grow at a CAGR of 15.3% from USD 1.66 Billion in 2026 to USD 5.96 Billion in 2031.

Highlights:

- 1Expanded genetic testing is increasing identification of hereditary FTD populations, which strengthens demand for targeted therapies.

- 2Precision medicine programs are advancing because broad neurodegenerative approaches have demonstrated limited success.

- 3Gene therapy development is accelerating, which is increasing investment in genetically characterized patient populations.

- 4Biomarker-driven clinical studies are expanding because developers require objective disease progression measurements.

Demand within the FTD market originates from progressive neurodegeneration that causes behavioral, language, and executive function impairment. Earlier recognition is increasing because awareness among neurologists, psychiatrists, and dementia specialists continues expanding. Diagnostic complexity remains a major constraint because symptoms frequently overlap with psychiatric disorders and other forms of dementia. Healthcare systems are strengthening specialist referral pathways to improve diagnostic accuracy. The treatment market therefore increasingly depends on earlier patient identification and genetic characterization.

Regulatory agencies are supporting rare neurological disease development because treatment options remain limited. Clinical development increasingly depends on biomarker validation, which creates demand for natural history studies and genetically defined patient registries. Research institutions are expanding precision medicine initiatives to support therapeutic development. This infrastructure growth strengthens future treatment adoption opportunities.

Market Dynamics

Market Drivers

Expansion of Genetic Diagnosis: Genetic characterization enables precise identification of disease-causing mutations. Testing utilization is increasing because hereditary forms of FTD are becoming easier to recognize. Limited awareness continues restricting diagnosis in many healthcare systems. Clinical centers are expanding genetic counseling and testing programs to address this challenge. Precision treatment development therefore becomes increasingly feasible.

Demand for Disease-Modifying Therapies: Symptomatic management does not alter underlying neurodegeneration. Patient advocacy organizations are increasing pressure for transformative treatment options. Clinical development remains difficult because disease progression varies substantially across patient populations. Developers are integrating biomarkers and genetic stratification into trial designs to improve development efficiency. Innovation therefore increasingly focuses on biologically validated targets.

Growth of Biomarker-Based Development: Traditional clinical endpoints require extended observation periods. Biomarker adoption is increasing because developers seek earlier indicators of therapeutic activity. Validation requirements continue creating development complexity. Research organizations are expanding longitudinal biomarker studies to strengthen regulatory confidence. Drug development therefore becomes increasingly data driven.

Regulatory Support for Rare Neurological Disorders: Rare disease frameworks create incentives for innovation. Sponsors are increasingly pursuing orphan drug and expedited development pathways. Scientific uncertainty remains a challenge because disease biology continues evolving. Regulatory agencies are encouraging early engagement with developers. Development timelines therefore become more predictable.

Market Restraints

Clinical endpoint variability limits confidence in therapeutic efficacy assessments.

Small genetically defined patient populations restrict recruitment speed.

High development costs create substantial financial risk for sponsors.

Market Opportunities

Progranulin Restoration Therapies: Reduced progranulin levels drive disease in FTD-GRN populations. Interest is increasing because genetic causality provides strong biological validation. Clinical proof remains limited. Developers are refining restoration strategies through antibodies and gene therapies. Targeted intervention therefore remains a major opportunity.

Gene Therapy Expansion: One-time treatment approaches offer potential long-term benefit. Investment is increasing because durable biological correction may improve outcomes. Manufacturing complexity remains significant. Companies are optimizing delivery platforms. Gene therapy therefore continues attracting strategic interest.

RNA Therapeutics: Gene regulation approaches enable targeted intervention. Research activity is increasing because RNA technologies support precision medicine. Delivery challenges remain important. Technology platforms are improving tissue targeting capabilities. Clinical applicability therefore expands.

Disease & Epidemiology Analysis

FTD creates significant healthcare burden because progressive neuronal loss causes irreversible cognitive and functional decline. Earlier diagnosis is increasing as awareness programs and genetic testing become more widely available. Diagnostic delays remain common because behavioral symptoms frequently resemble psychiatric disorders. Healthcare providers are adopting multidisciplinary assessment models to improve identification. The diagnosed treatment-eligible population therefore continues expanding.

Behavioral variant FTD remains the largest diagnosed subgroup because behavioral symptoms often prompt medical evaluation. Recognition is increasing among specialists as diagnostic frameworks improve. Disease heterogeneity continues complicating therapeutic development. Researchers are focusing on genetically defined populations to reduce variability. Precision medicine therefore becomes increasingly relevant.

Treatment Guidelines Landscape

Treatment Component | Current Practice |

Initial Evaluation | Neurological and neuropsychological assessment |

Structural Imaging | MRI |

Functional Imaging | FDG-PET when appropriate |

Genetic Assessment | Recommended for familial cases |

Market Segmentation

By Mechanism of Action

Progranulin deficiency directly contributes to FTD-GRN pathology. Development activity is increasing because the target possesses strong genetic validation. Clinical uncertainty remains after mixed outcomes from some antibody programs. Companies are expanding gene replacement and protein restoration approaches. The segment therefore remains a central focus of innovation.

Tau-targeted therapies continue attracting interest because tau pathology contributes to several FTD subtypes. Translational challenges remain significant because clinical efficacy has proven difficult to demonstrate. Developers are refining anti-tau antibodies and gene regulation strategies to improve target engagement. Precision biomarker use is increasing to support patient selection. Tau modulation therefore remains an important component of the emerging treatment landscape.

Neuroinflammation modulators are gaining prominence because microglial dysfunction influences disease progression. Research activity is increasing as immune-mediated mechanisms become better understood. Biological complexity continues creating development risk. Companies are pursuing selective immune pathway modulation to improve therapeutic specificity. Neuroimmune interventions therefore represent a growing area of innovation.

By Modality

Monoclonal antibody development remains active because biologics provide selective target engagement. Development activity expanded as progranulin restoration and neuroimmune modulation gained importance. Blood-brain barrier limitations continue constraining efficacy. Companies are improving molecular engineering strategies to enhance central nervous system penetration. Antibody-based therapies therefore remain a key modality within the pipeline.

Gene therapies are attracting increasing investment because they offer the potential for long-term correction of underlying genetic defects. Manufacturing complexity and delivery challenges remain substantial barriers. Developers are advancing viral vector technologies to improve precision targeting. Clinical programs increasingly focus on genetically defined patient populations. Gene therapy therefore continues emerging as one of the most promising modalities in FTD treatment development.

RNA therapeutics are advancing because they provide highly specific gene regulation capabilities. Delivery limitations continue affecting development feasibility. Platform innovation is improving tissue targeting and therapeutic durability. Researchers are expanding investigation of antisense oligonucleotides and RNA interference technologies. RNA-based interventions therefore are becoming increasingly relevant to future treatment strategies.

By Innovation Category

First-in-class assets continue attracting attention because they target previously unaddressed biological pathways. Scientific uncertainty remains elevated due to limited historical precedent. Developers are emphasizing biomarker validation to strengthen confidence in target engagement. Precision patient selection is becoming increasingly important for development success. Innovation therefore increasingly centers on genetically characterized disease populations.

Platform-based innovation is expanding because companies seek scalable approaches across multiple neurodegenerative diseases. Development strategies increasingly leverage shared delivery technologies and biomarker frameworks. Regulatory expectations continue evolving as novel modalities mature. Clinical programs are integrating translational evidence earlier in development. Platform technologies therefore are becoming critical competitive differentiators.

Regional Analysis

North America

North America leads FTD research and treatment development because advanced neuroscience infrastructure supports rare disease innovation. Genetic diagnosis rates are increasing as specialist centers expand testing programs. Recruitment challenges persist because eligible patient populations remain relatively small. Sponsors are strengthening academic partnerships to improve trial enrollment. Clinical development activity therefore remains concentrated within the region.

Europe

Europe benefits from strong academic collaboration and multinational research networks. Demand for targeted therapies is increasing because hereditary FTD awareness continues expanding. Reimbursement differences between countries influence access to specialized diagnostics. Research institutions are strengthening genomic medicine initiatives to improve patient stratification. Clinical recruitment therefore benefits from broader diagnostic capabilities.

Asia Pacific

Asia Pacific is becoming increasingly important because healthcare systems are expanding neurological research capabilities. Genetic diagnosis remains comparatively underdeveloped in several countries. Academic institutions are increasing investment in molecular neuroscience research. International developers are expanding regional trial activity to diversify recruitment. The region therefore continues gaining strategic importance.

Rest of the World

Emerging markets continue facing specialist infrastructure limitations. Awareness is increasing through educational initiatives and international collaboration. Diagnostic barriers remain substantial. Healthcare providers are strengthening referral pathways to improve patient identification. Market readiness therefore gradually improves despite ongoing constraints.

Regulatory Landscape

Regulatory agencies increasingly support rare neurological disease development because treatment options remain limited. Expedited pathways are becoming more relevant as precision medicine programs advance. Clinical uncertainty still requires strong evidence generation. Developers are engaging regulators earlier in development programs. Regulatory predictability therefore continues improving.

Gene therapy oversight remains a major focus because long-term safety monitoring is essential. Sponsors are expanding post-treatment follow-up programs. Manufacturing consistency remains a regulatory priority. Guidance frameworks continue evolving to accommodate novel technologies. Development standards therefore become increasingly mature.

Pipeline Analysis

The FTD pipeline increasingly concentrates on progranulin restoration and gene replacement because these mechanisms target well-characterized disease biology. Antibody-based approaches initially attracted attention due to their scalability. Mixed clinical outcomes have shifted focus toward genetic correction strategies. Developers are increasingly prioritizing durable biological interventions. Pipeline composition therefore continues moving toward advanced precision therapies.

Gene therapy programs remain among the most visible development efforts because they seek to address underlying genetic causes rather than downstream symptoms. Clinical evaluation remains ongoing. Long-term efficacy and safety continue requiring validation. Developers are expanding biomarker integration to strengthen development decisions. Pipeline momentum therefore remains strong.

Reimbursement Landscape

Current reimbursement primarily supports diagnosis and symptomatic management because disease-modifying therapies remain unavailable. Coverage for genetic testing is expanding as precision medicine becomes more important. Budget constraints continue affecting access decisions. Payers are evaluating long-term economic implications of advanced therapies. Future reimbursement frameworks therefore are likely to depend heavily on demonstrated clinical benefit and durability.

Competitive Landscape

Alector

Alector differentiates itself through neuroimmunology-focused research. The company is emphasizing mechanisms that influence neurodegeneration and immune system interactions. Clinical development activities are supporting broader understanding of FTD biology. Biomarker integration remains a central component of its strategy. This focus positions the company as an important contributor to precision neurodegenerative medicine.

GSK

GSK maintains a strategic position through neuroscience collaborations and global development capabilities. The company is leveraging extensive clinical infrastructure to support neurodegenerative disease programs. Partnership-driven approaches strengthen access to emerging technologies. Development expertise supports large-scale clinical execution. GSK therefore remains a significant participant in future therapeutic advancement.

Passage Bio

Passage Bio focuses on genetic neurological disorders. Its strategy emphasizes gene therapy approaches that address underlying disease mechanisms rather than symptomatic management. Clinical development increasingly centers on genetically validated targets. Specialized expertise supports precision medicine initiatives. The company therefore remains strongly aligned with evolving treatment trends.

Denali Therapeutics

Denali Therapeutics concentrates on neurodegeneration with a strong emphasis on translational science. The company is developing approaches intended to improve therapeutic delivery into the central nervous system. Scientific innovation focuses on overcoming biological barriers. Precision targeting remains a strategic priority. This approach supports future participation in advanced neurological therapies.

Takeda

Takeda contributes substantial neurological research expertise. Its development capabilities support participation in rare disease and neurodegenerative therapeutic programs. Global infrastructure enables broad research collaboration. Scientific investment continues supporting innovation efforts. Takeda therefore maintains relevance within the evolving treatment landscape.

Prevail Therapeutics

Prevail Therapeutics focuses on gene therapy innovation. The company is pursuing genetically defined patient populations where precision medicine strategies may improve outcomes. Targeted intervention remains central to development efforts. Genetic disease expertise supports long-term innovation. The company therefore aligns closely with emerging therapeutic trends.

Vesper Bio

Vesper Bio emphasizes progranulin-related disease mechanisms. The company is developing targeted approaches intended to address biological pathways linked to FTD. Scientific focus remains concentrated on genetically validated targets. Development efforts seek to improve disease modification potential. This specialization strengthens its position within the emerging therapy ecosystem.

AviadoBio

AviadoBio focuses on gene therapy technologies designed for neurodegenerative diseases. Strategic differentiation stems from targeted delivery approaches and rare disease specialization. Clinical programs increasingly emphasize genetic correction strategies. Precision medicine remains central to development priorities. The company therefore occupies a prominent position within the gene therapy segment.

Strategic Insights and Future Market Outlook

The FTD market increasingly favors genetically targeted interventions because broad neurodegenerative approaches have produced inconsistent outcomes. Patient identification is improving through expanded genetic testing programs. Small patient populations continue constraining recruitment. Developers are building global trial networks to improve efficiency. Precision medicine therefore becomes increasingly practical.

Gene therapy investment continues rising because durable biological correction offers a compelling treatment rationale. Long-term efficacy remains uncertain. Developers are generating increasing biomarker evidence to strengthen confidence in therapeutic activity. The evidence base therefore continues expanding.

Future competitive positioning will depend heavily on clinical validation of targeted mechanisms. Regulatory support remains favorable. Development risk continues influencing investment decisions. Companies capable of demonstrating durable disease modification are likely to shape the next phase of FTD market evolution.

The future FTD market is moving toward earlier diagnosis, biomarker-guided intervention, and genetically defined patient management. Development challenges remain substantial, yet continued advances in gene therapy, RNA therapeutics, and precision neuroscience are strengthening the likelihood that disease-modifying treatment options will emerge during the forecast period.

Frontotemporal Dementia Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 1.66 Billion |

| Total Market Size in 2035 | USD 5.96 Billion |

| Forecast Unit | USD Billion |

| Growth Rate | 15.3% |

| Study Period | 2021 to 2035 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2035 |

| Segmentation | Mechanism of Action, Modality, Innovation Category, Geography |

| Geographical Segmentation | North America, Latin America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

Mechanism of Action

Modality

Innovation Category

Geography

Geographical Segmentation

North America, Latin America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. EXECUTIVE SUMMARY

1.1 Report Scope and Objectives

1.2 Frontotemporal Dementia Emerging Therapies Market Snapshot

1.3 Key Pipeline Intelligence Highlights

1.4 Major Innovation Trends

1.5 Emerging Therapeutic Modalities Overview

1.6 Clinical Development Outlook

1.7 Competitive Intelligence Summary

1.8 Risk-Adjusted Opportunity Assessment

1.9 Future Commercial and Clinical Outlook

2. PIPELINE OVERVIEW

2.1 Frontotemporal Dementia Therapeutic Landscape Overview

2.1.1 Disease Background

2.1.2 Current Standard of Care

2.1.3 Approved Therapy Landscape

2.1.4 Unmet Treatment Need Assessment

2.2 Emerging Therapy Pipeline Snapshot

2.2.1 Total Active Pipeline Assets

2.2.2 Active versus Discontinued Programs

2.2.3 Historical Pipeline Evolution

2.2.4 Development Stage Distribution

2.3 Pipeline Maturity Assessment

2.3.1 Early-Stage Asset Concentration

2.3.2 Mid-Stage Development Strength

2.3.3 Late-Stage Development Readiness

2.3.4 Historical Advancement Trends

2.4 Innovation Ecosystem Overview

2.4.1 Industry-Sponsored Programs

2.4.2 Academic Research Programs

2.4.3 Foundation-Supported Initiatives

2.4.4 Public–Private Collaborations

3. DISEASE AND UNMET NEED ANALYSIS

3.1 Frontotemporal Dementia Disease Overview

3.1.1 Behavioral Variant Frontotemporal Dementia (bvFTD)

3.1.2 Primary Progressive Aphasia (PPA)

3.1.3 Genetic Frontotemporal Dementia

3.1.4 FTD with Motor Neuron Disease

3.2 Disease Burden Assessment

3.2.1 Clinical Burden

3.2.2 Economic Burden

3.2.3 Caregiver Burden

3.2.4 Quality-of-Life Impact

3.3 Current Treatment Limitations

3.3.1 Symptomatic Management Constraints

3.3.2 Lack of Disease-Modifying Therapies

3.3.3 Diagnostic Challenges

3.3.4 Genetic Subpopulation Challenges

3.4 Emerging Therapy Opportunity Areas

3.4.1 Progranulin Restoration

3.4.2 Tau Modulation

3.4.3 TDP-43 Targeting

3.4.4 Neuroinflammation Regulation

3.4.5 Gene Replacement Strategies

3.4.6 RNA-Based Therapeutics

4. MECHANISM AND MODALITY LANDSCAPE

4.1 Mechanism of Action Clustering

4.1.1 Progranulin Restoration Therapies

4.1.1.1 Sortilin Inhibition

4.1.1.2 Progranulin Augmentation

4.1.1.3 GRN Gene Replacement

4.1.2 Tau-Targeted Therapies

4.1.2.1 Anti-Tau Antibodies

4.1.2.2 Tau Aggregation Inhibitors

4.1.2.3 Tau Gene Regulation Approaches

4.1.3 Neuroinflammation Modulators

4.1.3.1 Microglial Pathway Modulators

4.1.3.2 Innate Immune Regulators

4.1.3.3 Neuroimmune Signaling Targets

4.1.4 TDP-43 Pathway Modulators

4.1.4.1 Protein Homeostasis Approaches

4.1.4.2 Aggregation Prevention Strategies

4.1.5 Genetic and RNA-Based Therapies

4.1.5.1 Gene Replacement Technologies

4.1.5.2 Antisense Oligonucleotides

4.1.5.3 RNA Interference Platforms

4.2 Modality Analysis

4.2.1 Small Molecules

4.2.2 Monoclonal Antibodies

4.2.3 Gene Therapies

4.2.4 RNA Therapies

4.2.5 Other Advanced Modalities

4.3 Innovation Assessment

4.3.1 First-in-Class Emerging Assets

4.3.2 Best-in-Class Development Strategies

4.3.3 Platform-Based Innovation

4.3.4 Precision Medicine Trends

4.3.5 Biomarker-Driven Development Trends

5. CLINICAL DEVELOPMENT INTELLIGENCE

5.1 Clinical Trial Landscape Overview

5.1.1 Historical Trial Activity

5.1.2 Active Trial Distribution

5.1.3 Trial Initiation Trends

5.1.4 Trial Completion Trends

5.2 Trial Design Benchmarking

5.2.1 Sample Size Benchmarking

5.2.2 Primary Endpoint Benchmarking

5.2.3 Secondary Endpoint Benchmarking

5.2.4 Biomarker Endpoint Utilization

5.2.5 Trial Duration Benchmarking

5.3 Recruitment Intelligence

5.3.1 Enrollment Trends

5.3.2 Recruitment Challenges

5.3.3 Genetic Population Recruitment Analysis

5.3.4 Global Recruitment Patterns

5.4 Success and Failure Analysis

5.4.1 Historical Success Rates

5.4.2 Clinical Failure Drivers

5.4.3 Trial Discontinuation Trends

5.4.4 Endpoint Achievement Analysis

6. PIPELINE SEGMENTATION ANALYSIS

6.1 Pipeline by Development Phase

6.1.1 Preclinical Pipeline

6.1.1.1 Asset Count

6.1.1.2 Mechanism Distribution

6.1.1.3 Developer Participation

6.1.2 Phase I Pipeline

6.1.2.1 Asset Count

6.1.2.2 Safety Evaluation Trends

6.1.2.3 Biomarker Integration

6.1.3 Phase II Pipeline

6.1.3.1 Asset Count

6.1.3.2 Proof-of-Concept Assessment

6.1.3.3 Development Risks

6.1.4 Phase III Pipeline

6.1.4.1 Asset Count

6.1.4.2 Pivotal Study Assessment

6.1.4.3 Regulatory Readiness

6.1.5 Filed and Under Review Assets

6.1.5.1 Regulatory Status Review

6.1.5.2 Approval Readiness Assessment

6.2 Pipeline by Mechanism of Action

6.3 Pipeline by Modality

6.4 Pipeline by Genetic Target

6.5 Pipeline by Developer Type

7. EMERGING THERAPY ASSET INTELLIGENCE PROFILES

7.1 Latozinemab (AL001)

7.1.1 Developer Profile (Alector / GSK)

7.1.2 Molecule Overview

7.1.3 Mechanism of Action

7.1.4 Clinical Development History

7.1.5 Trial Design Assessment

7.1.6 Regulatory Status

7.1.7 Clinical Outcome Analysis

7.1.8 Probability of Success Assessment

7.1.9 Future Development Outlook

7.2 AVB-101

7.2.1 Developer Profile (AviadoBio)

7.2.2 Gene Therapy Platform

7.2.3 Mechanism of Action

7.2.4 Clinical Development Status

7.2.5 ASPIRE-FTD Trial Analysis

7.2.6 Regulatory Designations

7.2.7 Risk Assessment

7.2.8 Commercial Opportunity

7.3 PBFT02

7.3.1 Developer Profile (Passage Bio)

7.3.2 AAV Gene Therapy Technology

7.3.3 Mechanism of Action

7.3.4 Clinical Progress Review

7.3.5 Biomarker Evaluation

7.3.6 Development Challenges

7.3.7 Future Outlook

7.4 TPN-101

7.4.1 Developer Profile (Transposon Therapeutics)

7.4.2 Molecule Overview

7.4.3 Mechanism of Action

7.4.4 Clinical Development Status

7.4.5 Trial Assessment

7.4.6 Strategic Outlook

8. PROBABILITY OF SUCCESS AND RISK ANALYSIS

8.1 Clinical Transition Probability Modeling

8.1.1 Preclinical-to-Phase I Probability

8.1.2 Phase I-to-Phase II Probability

8.1.3 Phase II-to-Phase III Probability

8.1.4 Phase III-to-Approval Probability

8.2 Risk-Adjusted Pipeline Assessment

8.2.1 Asset Risk Weighting

8.2.2 Mechanism-Based Risk Analysis

8.2.3 Platform Technology Risk

8.2.4 Regulatory Risk Analysis

8.3 Attrition Intelligence

8.3.1 Historical Attrition Rates

8.3.2 Neurodegeneration Benchmark Comparison

8.3.3 FTD-Specific Failure Patterns

8.4 Scenario Analysis

8.4.1 Base Case Scenario

8.4.2 Optimistic Scenario

8.4.3 Conservative Scenario

9. LAUNCH TIMELINE AND COMMERCIAL POTENTIAL

9.1 Expected Approval Timeline Assessment

9.2 Launch Sequence Forecasting

9.3 Competitive Entry Timing

9.4 Adoption Curve Assessment

9.5 Market Access Preparedness

9.6 Peak Sales Opportunity Analysis

9.7 Probability-Weighted Revenue Modeling

9.8 Genetic Subpopulation Opportunity Assessment

10. COMPETITIVE PIPELINE LANDSCAPE

10.1 Pipeline Strength Ranking

10.2 Company-Wise Asset Concentration

10.3 Development Stage Leadership Analysis

10.4 Innovation Leadership Assessment

10.5 Leader versus Challenger Positioning

10.6 Company Intelligence Profiles

10.6.1 Alector

10.6.2 GSK

10.6.3 AviadoBio

10.6.4 Passage Bio

10.6.5 Transposon Therapeutics

10.6.6 Denali Therapeutics

10.6.7 Takeda

10.6.8 Prevail Therapeutics

10.6.9 Vesper Bio

10.6.10 Eli Lilly and Company

11. GEOGRAPHIC ANALYSIS

11.1 North America

11.2 Europe

11.3 Asia-Pacific

11.4 Latin America

11.5 Middle East & Africa

12. KEY COUNTRIES ANALYSIS

12.1 United States

12.2 Canada

12.3 Germany

12.4 United Kingdom

12.5 France

12.6 Italy

12.7 Spain

12.8 China

12.9 Japan

12.10 India

12.11 South Korea

12.12 Australia

12.13 Brazil

12.14 Mexico

12.15 Saudi Arabia

12.16 South Africa

13. DEALS AND INVESTMENT LANDSCAPE

13.1 Licensing Transactions

13.1.1 Regional Licensing Deals

13.1.2 Global Licensing Agreements

13.2 Co-Development Partnerships

13.2.1 Strategic Collaborations

13.2.2 Research Alliances

13.3 Mergers and Acquisitions

13.3.1 Pipeline Asset Acquisitions

13.3.2 Platform Acquisitions

13.4 Funding Landscape

13.4.1 Venture Capital Funding

13.4.2 Private Equity Activity

13.4.3 Public Financing Events

13.4.4 Foundation and Non-Profit Funding

14. FUTURE OUTLOOK AND STRATEGIC INSIGHTS

14.1 Future Pipeline Evolution

14.2 Emerging Mechanism Trends

14.3 Gene Therapy Outlook

14.4 RNA Therapeutics Outlook

14.5 Precision Medicine Evolution

14.6 Biomarker Integration Outlook

14.7 Regulatory Environment Evolution

14.8 Competitive Landscape Forecast

14.9 Strategic Recommendations for Developers

14.10 Strategic Recommendations for Investors

14.11 Long-Term Probability-Adjusted Opportunity Outlook

15. METHODOLOGY AND DATA FRAMEWORK

15.1 Research Methodology

15.2 Data Sources and Validation Framework

15.3 Clinical Trial Registry Review Methodology

15.4 Asset Inclusion and Exclusion Criteria

15.5 Phase Classification Methodology

15.6 Mechanism Classification Framework

15.7 Probability Modeling Methodology

15.8 Revenue Forecasting Framework

15.9 Competitive Benchmarking Methodology

15.10 Limitations and Assumptions

15.11 Glossary of Terms

15.12 Abbreviations

Navigate

Trusted by the world's leading organizations