Report Overview

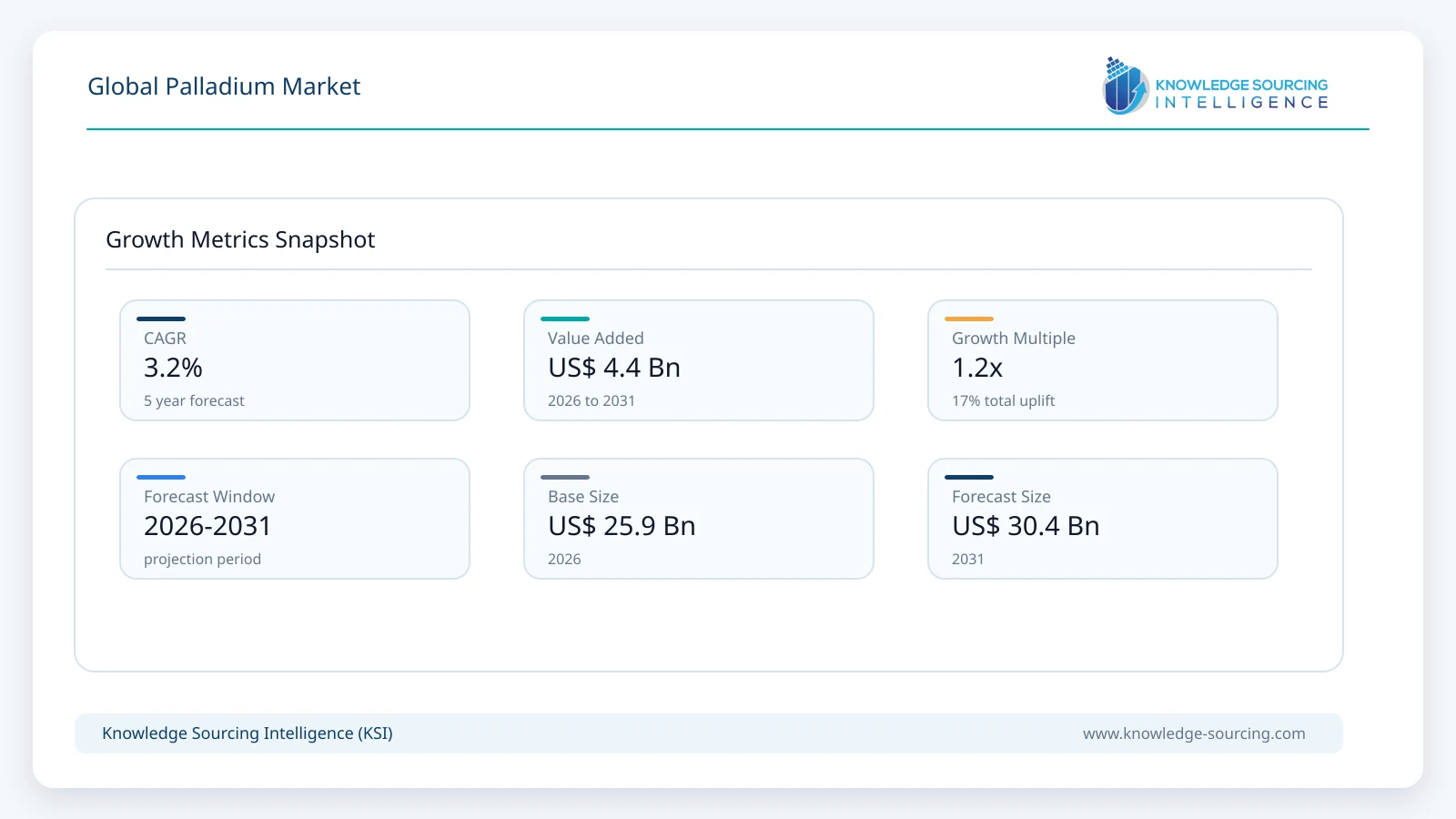

The global Palladium market is forecast to grow at a CAGR of 3.2%, reaching USD 30.38 billion in 2031 from USD 25.95 billion in 2026.

Highlights:

- 1Automotive catalysts represent the primary commercial application for palladium due to emission-control requirements for gasoline-powered vehicles.

- 2Supply concentration in Russia and South Africa creates procurement concerns related to geopolitical risks and mining disruptions.

- 3Recycling is becoming an important supply source as industries seek greater material security and lower environmental impact.

- 4Electronics manufacturers use palladium in multilayer ceramic capacitors, plating materials, and specialized components requiring conductivity and durability.

- 5Hydrogen purification applications are creating additional interest in palladium-based membrane technologies.

- 6Producers and refiners compete through supply reliability, refining capability, recycling infrastructure, and customer-specific material solutions.

The global palladium market covers the extraction, refining, processing, and commercial distribution of palladium in forms including powder, sponge, compounds, and refined metal. Palladium is a platinum group metal (PGM) valued for its catalytic properties, corrosion resistance, electrical conductivity, and ability to absorb hydrogen. The metal serves critical industrial applications across automotive emissions control, chemical processing, electronics manufacturing, hydrogen purification, electroplating, healthcare, and jewelry.

Automotive catalysts remain the largest demand application for palladium because gasoline-powered vehicles use palladium-based catalytic converters to reduce harmful emissions such as carbon monoxide, hydrocarbons, and nitrogen oxides. Regulatory requirements for lower vehicle emissions continue to influence procurement decisions among automobile manufacturers and catalytic converter producers. The International Platinum Group Metals Association (IPA) identifies automotive catalysts as a major industrial application for platinum group metals due to their role in emission-control technologies.

The market structure is influenced by a concentrated supply base. Palladium production is geographically limited, with Russia and South Africa representing major sources of primary supply. According to the United States Geological Survey (USGS), global palladium mine production remains concentrated among a small number of producing countries, creating sensitivity to geopolitical conditions, labor disruptions, energy costs, and mining investment cycles. Buyers typically prioritize supply reliability, metal purity, recycling capability, and long-term supplier relationships when sourcing palladium.

Demand patterns are changing as automotive manufacturers adjust their catalyst requirements in response to vehicle technology shifts. The increasing adoption of battery electric vehicles reduces demand for internal combustion engine catalysts, while hybrid vehicles continue requiring emission-control systems. This transition is influencing purchasing strategies among automakers and catalyst manufacturers, who are balancing near-term regulatory requirements with long-term technology changes.

Recycling has become an important part of the palladium supply chain. Secondary recovery from spent automotive catalysts, electronic components, and industrial materials helps reduce dependence on mined supply. Refiners and industrial users increasingly consider recycled palladium availability, recovery efficiency, and environmental performance when planning procurement strategies.

Market Drivers

Emission Regulations Supporting Automotive Catalyst Demand

Strict vehicle emission standards remain a primary demand driver for palladium because automakers require catalytic materials capable of meeting regulatory limits for exhaust pollutants. Governments across major automotive markets continue strengthening emission regulations, requiring manufacturers to improve combustion efficiency and exhaust treatment systems.

Automotive companies, catalyst manufacturers, and metal refiners form the primary buyer chain for palladium used in catalytic converters. Procurement decisions depend on metal availability, price stability, catalyst performance, and compliance requirements. Companies supplying palladium-based catalyst materials continue investing in refining capacity, recycling operations, and technical support to maintain stable industrial supply.

The commercial implication is that regulatory changes directly influence palladium consumption patterns. While electric vehicle adoption affects long-term automotive demand, hybrid vehicle production and emission standards continue supporting near-term industrial requirements.

Growth of Electronics Manufacturing Applications

Palladium is used in electronics because of its electrical conductivity, chemical stability, and resistance to oxidation. The metal is incorporated into multilayer ceramic capacitors, connectors, electrode materials, and plating applications used in consumer electronics, industrial equipment, and automotive electronics.

Electronics manufacturers purchase palladium-based materials based on consistency, purity levels, processing compatibility, and supply reliability. As electronic systems become more complex, manufacturers require materials that maintain performance under higher operating temperatures and demanding conditions.

Suppliers are responding by improving powder production technologies, refining processes, and customized material formulations. These developments support demand from electronics producers seeking reliable precious metal inputs for advanced components.

Expansion of Palladium Recycling Infrastructure

Recycling has become a major factor influencing palladium availability and pricing. Spent automotive catalysts contain recoverable platinum group metals, making recycling economically attractive for refiners and material processors. Secondary supply reduces pressure on mining operations while providing additional material security for industrial users.

Companies involved in refining and recycling invest in recovery technologies, collection networks, and processing facilities to improve metal recovery rates. This creates additional revenue opportunities throughout the value chain while helping manufacturers manage exposure to primary supply fluctuations.

Demand from Hydrogen and Industrial Applications

Palladium’s ability to selectively absorb and separate hydrogen supports its use in hydrogen purification membranes and specialized industrial processes. Although these applications currently represent a smaller share of total palladium demand compared with automotive catalysts, interest in hydrogen-related technologies has encouraged research and commercial development.

Industrial users evaluate palladium-based hydrogen technologies based on separation efficiency, material durability, cost considerations, and system performance. Growth in hydrogen infrastructure investment could create additional demand opportunities for specialized palladium applications during the forecast period.

Market Restraints and Challenges

Automotive Transition Toward Battery Electric Vehicles

The shift toward battery electric vehicles creates a long-term challenge for palladium demand because fully electric vehicles do not require catalytic converters. Automakers are increasing investment in electrification strategies, which may reduce future dependence on palladium-based emission systems.

Mining companies, refiners, and catalyst producers face uncertainty regarding long-term demand planning. Companies are addressing this challenge through recycling investments, diversification into other platinum group metals, and development of alternative industrial applications.

Price Volatility and Supply Concentration

Palladium prices are sensitive to geopolitical conditions, mining disruptions, currency movements, and changes in automotive demand. Since primary production is concentrated among a limited number of countries, unexpected supply interruptions can affect availability and procurement costs.

Manufacturers using palladium must manage inventory levels, supplier diversification, and contractual arrangements to reduce exposure to price fluctuations. Refiners and industrial suppliers increasingly emphasize recycling capacity and flexible sourcing strategies.

Competition from Alternative Materials

Automotive catalyst manufacturers continue evaluating platinum substitution because platinum can replace palladium in some gasoline catalyst applications. Price differences between platinum and palladium influence material selection decisions among catalyst producers.

This substitution pressure affects palladium demand forecasts and encourages producers to improve cost efficiency and develop specialized applications where palladium maintains technical advantages.

Major Segment Analysis

Automotive Catalysts

Automotive catalysts represent the most commercially important segment of the palladium market due to the metal’s effectiveness in controlling emissions from gasoline engines. Vehicle manufacturers and catalyst suppliers rely on palladium-based formulations to meet emission standards established by transportation authorities worldwide.

Demand is closely linked to global vehicle production, gasoline engine penetration, hybrid vehicle adoption, and regulatory requirements. Although battery electric vehicles reduce future catalyst demand, hybrid vehicles continue requiring emission-control systems, maintaining industrial relevance for palladium during the forecast period.

Buyers prioritize catalyst performance, material availability, price stability, and compliance with environmental regulations. Automotive catalyst manufacturers compete through research into catalyst formulations, metal loading optimization, recycling efficiency, and supply agreements with automakers.

The revenue importance of this segment extends beyond primary palladium sales because it supports related activities including refining, catalyst manufacturing, recycling, and precious metal recovery. Companies with integrated supply chains are better positioned to manage changing automotive demand conditions.

Regional Analysis

North America

North America represents an important palladium consumption region due to its large automotive manufacturing base, emissions regulations, and advanced electronics industry. The United States remains a major market for automotive catalyst demand because vehicle manufacturers must comply with federal and state emission standards.

The Environmental Protection Agency (EPA) continues implementing vehicle emission regulations that influence catalyst technology requirements. Automotive manufacturers and suppliers evaluate palladium procurement based on regulatory compliance, supply security, and cost management.

Recycling infrastructure is also well established in North America, supporting secondary palladium recovery from spent automotive catalysts and industrial materials. However, future demand depends on the pace of vehicle electrification and changes in domestic automotive production.

Europe

Europe remains an important palladium market because of strict vehicle emission standards and established automotive manufacturing capabilities. Germany, France, the United Kingdom, and other European markets maintain strong demand from automotive original equipment manufacturers and catalyst suppliers.

The European Union’s emission regulations continue influencing material requirements for vehicle manufacturers. Companies operating in Europe increasingly evaluate supply chain transparency, responsible sourcing, and environmental performance when purchasing precious metals.

The region also faces long-term demand uncertainty due to accelerated electric vehicle adoption policies, which may reduce conventional catalyst requirements over time.

Asia Pacific

Asia Pacific is a major consumption and manufacturing region supported by automotive production, electronics manufacturing, and industrial processing activities. China, Japan, South Korea, and India represent important markets due to large vehicle manufacturing industries and extensive electronics supply chains.

China’s automotive sector remains a major consumer of palladium-based catalysts, while Japan and South Korea contribute demand through advanced electronics and industrial applications. Regional buyers prioritize reliable supply arrangements due to exposure to global precious metal price fluctuations.

Mining and refining activities in Asia Pacific are comparatively limited compared with major producing regions, making imports and recycling important components of regional supply strategies.

Competitive Landscape

The palladium market has a concentrated supply structure because primary production depends on a limited number of mining regions and specialized refining capabilities. Competition extends across mining companies, precious metal refiners, chemical suppliers, and advanced material manufacturers. Companies compete through access to mineral resources, refining capacity, recycling infrastructure, product purity, customer relationships, and technical expertise.

The major companies operating in the palladium value chain include MMC Norilsk Nickel, Sibanye-Stillwater Limited, Impala Platinum Holdings Limited, Northam Platinum Holdings Limited, Anglo American plc, Johnson Matthey, Merck KGaA (Sigma-Aldrich), Thermo Fisher Scientific, Heraeus, Valterra Platinum, and Heeger Materials Inc. Their activities cover different stages of the value chain, from mining and refining to specialty chemical production and industrial material supply.

Mining companies differentiate through reserve quality, production scale, operational efficiency, and geographic diversification. Producers with integrated refining operations can manage processing activities internally and provide greater supply reliability to industrial customers. South African and Russian producers remain strategically important because of their contribution to global palladium supply.

Refining and specialty material suppliers compete through processing technology, recycling capability, and customized product development. Companies supplying palladium powders, compounds, and other refined materials serve electronics manufacturers, chemical companies, research institutions, and industrial users requiring specific purity levels and particle characteristics.

Recycling has become an important competitive factor because secondary palladium recovery provides an alternative supply source for industrial buyers. Companies with established collection networks and refining infrastructure can recover palladium from spent automotive catalysts and industrial waste streams, improving supply flexibility.

Strategic partnerships between mining companies, refiners, automotive suppliers, and technology providers influence market positioning. These collaborations help companies secure long-term supply arrangements, improve recovery rates, and develop materials suited for changing industrial requirements.

Recent Developments

April 2026: Nornickel opened the world’s first dedicated palladium laboratory in Moscow on 14 April 2026 to accelerate research, material development, and commercialization of new palladium-based technologies.

May 2025: Johnson Matthey continued expanding its focus on sustainable technologies and precious metal recovery solutions through its advanced materials and recycling activities. The company’s strategy supports industrial customers seeking improved resource efficiency and recycled precious metal supply.

Regulatory and Policy Environment

The palladium market is influenced by regulations covering vehicle emissions, mining operations, responsible sourcing, environmental protection, and industrial safety. Automotive emission standards remain one of the most important regulatory factors because they determine the quantity and type of catalyst materials required by vehicle manufacturers.

In the United States, the Environmental Protection Agency (EPA) establishes vehicle emission standards that affect catalytic converter technology requirements. Regulations requiring lower pollutant emissions encourage automotive manufacturers to maintain efficient catalyst systems for internal combustion and hybrid vehicles.

In Europe, vehicle emission policies under the European Union framework influence palladium demand through increasingly strict limits on exhaust emissions. The European Commission’s regulations encourage manufacturers to reduce transportation-related emissions while supporting the transition toward lower-emission mobility solutions.

Mining regulations also influence palladium supply. Producers must comply with environmental permitting, land management requirements, occupational safety standards, and responsible mining principles. International frameworks such as the International Council on Mining and Metals (ICMM) encourage mining companies to improve environmental performance, community engagement, and responsible resource management.

Responsible sourcing requirements are becoming more important for industrial buyers, particularly electronics manufacturers and automotive companies. Procurement teams increasingly evaluate supplier transparency, environmental reporting, and traceability of precious metal inputs.

Recycling regulations and circular economy policies also support secondary palladium supply. Governments promoting resource efficiency encourage industries to recover and reuse precious metals, reducing dependence on newly mined resources.

Outlook and Strategic Implications

The palladium market between 2026 and 2031 will be shaped by the interaction between automotive technology changes, supply constraints, recycling expansion, and industrial demand diversification. Automotive catalysts are expected to remain the primary demand source, particularly because hybrid vehicles and existing gasoline vehicle production will continue requiring emission-control materials.

However, the increasing adoption of battery electric vehicles represents a structural challenge for long-term palladium consumption. Automakers are adjusting procurement strategies by evaluating catalyst material efficiency, platinum substitution opportunities, and alternative powertrain technologies. Suppliers must therefore monitor vehicle production trends and adapt their product portfolios accordingly.

Investment priorities across the palladium value chain are expected to focus on mining efficiency, recycling capacity, refining technology, and specialty material production. Recycling infrastructure will become more strategically important as companies seek additional supply sources and reduce exposure to primary mining volatility.

Technology development will influence demand from non-automotive sectors. Electronics, chemical processing, hydrogen purification, and advanced materials applications may provide additional opportunities for palladium suppliers. Companies producing high-purity powders, compounds, and engineered materials are positioned to serve specialized industrial applications where palladium’s physical and chemical properties remain valuable.

Procurement strategies are expected to emphasize supply security, price risk management, and supplier diversification. Industrial users may increase reliance on long-term agreements, recycling partnerships, and inventory management programs to reduce exposure to sudden supply disruptions.

The competitive environment will continue favoring companies with integrated operations covering mining, refining, recycling, and specialty material production. Producers with strong environmental practices and transparent supply chains are likely to maintain stronger relationships with automotive and industrial customers facing stricter sustainability requirements.

Key risks include accelerated electric vehicle adoption, prolonged palladium price weakness, substitution by alternative materials, and geopolitical disruptions affecting major producing regions. Companies that improve recycling capabilities, diversify end-use markets, and maintain operational efficiency will be better positioned to manage these pressures.

Overall, the palladium market will transition from a primarily automotive-driven commodity market toward a more balanced industrial materials market. The ability to provide reliable supply, recycled material solutions, and specialized palladium products will determine competitive positioning during the 2026–2031 forecast period.

Palladium Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 25.95 billion |

| Total Market Size in 2031 | USD 30.38 billion |

| Forecast Unit | Billion |

| Growth Rate | 3.2% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Form, Application, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Form

By Application

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET OVERVIEW

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

2.5. Market Size and Forecast

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Supply Chain Analysis

3.7. Pricing Trends

3.8. Raw Material and Mining Landscape

3.9. Policies and Regulations

3.10. Strategic Recommendations

4. TECHNOLOGICAL AND INNOVATION LANDSCAPE

4.1. Palladium Recycling Technologies

4.2. Automotive Catalyst Innovations

4.3. Hydrogen Purification Technologies

4.4. Palladium Substitution Trends

5. GLOBAL PALLADIUM MARKET BY FORM

5.1. Introduction

5.2. Palladium Powder

5.3. Palladium Sponge

5.4. Palladium Compounds

5.5. Palladium Metal

5.6. Others

6. GLOBAL PALLADIUM MARKET BY APPLICATION

6.1. Introduction

6.2. Automotive Catalysts

6.3. Chemical Catalysts

6.4. Electronics Components

6.5. Jewelry and Decorative Applications

6.6. Hydrogen Purification

6.7. Electroplating

6.8. Dental and Medical Applications

6.9. Others

7. GLOBAL PALLADIUM MARKET BY END-USER

7.1. Introduction

7.2. Automotive

7.3. Electronics and Electrical

7.4. Chemical Processing

7.5. Healthcare and Dental

7.6. Jewelry

7.7. Energy and Hydrogen

7.8. Others

8. GLOBAL PALLADIUM MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. USA

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Argentina

8.3.3. Others

8.4. Europe

8.4.1. Germany

8.4.2. France

8.4.3. United Kingdom

8.4.4. Russia

8.4.5. Spain

8.4.6. Others

8.5. Middle East and Africa

8.5.1. Saudi Arabia

8.5.2. UAE

8.5.3. Israel

8.5.4. Others

8.6. Asia Pacific

8.6.1. China

8.6.2. India

8.6.3. Japan

8.6.4. South Korea

8.6.5. Indonesia

8.6.6. Taiwan

8.6.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Production Capacity Analysis

9.4. Supplier Landscape Analysis

9.5. Mergers, Acquisitions, Partnerships, and Collaborations

9.6. Competitive Dashboard

10. COMPANY PROFILES

10.1. Merck KGaA (Sigma-Aldrich)

10.2. MMC Norilsk Nickel

10.3. Sibanye-Stillwater Limited

10.4. Impala Platinum Holdings Limited

10.5. Northam Platinum Holdings Limited

10.6. Anglo American plc

10.7. Johnson Matthey

10.8. Thermo Fisher Scientific

10.9. Heraeus

10.10. Valterra Platinum

10.11. Heeger Materials Inc.

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base Year and Forecast Period Timeline

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations