Report Overview

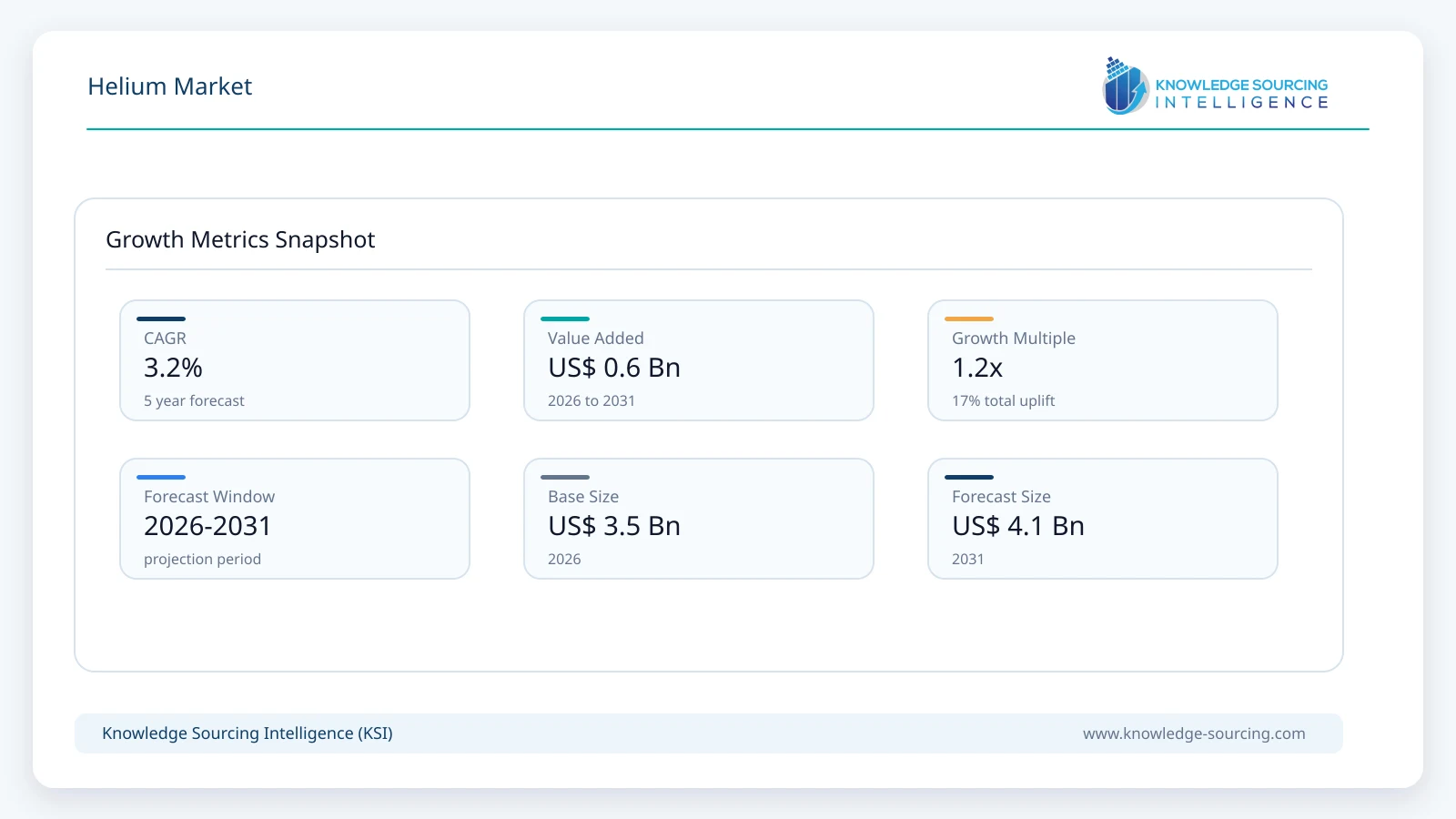

The Helium market is forecast to grow at a CAGR of 3.2%, reaching USD 4.1 billion in 2031 from USD 3.5 billion in 2026.

Highlights:

- 1Rising semiconductor fabrication capacity and expanding MRI installations continue to support long-term helium consumption.

- 2Liquid helium for cryogenic applications remains among the most commercially important product categories because of its limited substitutes.

- 3Asia Pacific represents an important demand center owing to electronics manufacturing expansion and healthcare infrastructure investment.

- 4Helium recovery, recycling, and purification technologies are gaining commercial importance as buyers seek greater supply security.

- 5Government oversight of strategic helium resources, industrial gas handling, and export policies continues to influence supply availability.

- 6Competition increasingly depends on production diversity, logistics capabilities, long-term contracts, and technical service rather than pricing alone.

The helium market comprises the production, purification, liquefaction, storage, transportation, and distribution of helium supplied in gaseous and liquid forms for industrial, scientific, medical, and aerospace applications. Unlike most industrial gases, helium is a finite natural resource recovered primarily as a by-product of natural gas processing where economically recoverable concentrations are present. This unique supply structure distinguishes helium from other industrial gases and places considerable emphasis on resource availability, purification infrastructure, and long-term supply contracts.

Demand is primarily generated by industries where helium's exceptionally low boiling point, chemical inertness, low density, and high thermal conductivity cannot be substituted without affecting performance or regulatory compliance. Healthcare organizations procure liquid helium for magnetic resonance imaging (MRI) systems, while semiconductor manufacturers require ultra-high-purity helium for wafer fabrication, leak detection, and advanced process control. Aerospace and defense organizations purchase helium for pressurization, purging, testing, and launch operations, whereas manufacturers rely on helium for specialized welding and quality assurance applications.

Purchasing decisions are increasingly influenced by supply reliability rather than price alone. Industrial consumers have experienced multiple supply disruptions over the past decade due to maintenance outages, geopolitical developments, and production constraints at major helium-producing facilities. Consequently, buyers are diversifying procurement sources, negotiating longer-term agreements, and investing in helium recovery and recycling systems to reduce exposure to supply volatility. These procurement strategies are reshaping commercial relationships throughout the supply chain.

Industry economics are determined by limited upstream production, specialized cryogenic infrastructure, transportation logistics, and purification capabilities. Liquid helium distribution requires sophisticated insulated containers and dedicated logistics networks, creating high entry barriers for new suppliers. Integrated industrial gas companies therefore maintain competitive advantages through global production portfolios, distribution assets, and long-standing customer relationships across multiple industrial sectors.

Technological developments within semiconductor manufacturing, quantum computing research, superconducting technologies, and advanced healthcare infrastructure continue to reinforce helium demand. At the same time, producers are investing in new extraction projects, purification facilities, and recycling technologies to improve supply resilience. Expansion of liquefaction capacity near producing regions also supports international trade while reducing transportation inefficiencies.

Commercial activity increasingly reflects a balance between supply security, purity requirements, operational efficiency, and sustainability objectives. Organizations that previously viewed helium as a commodity now evaluate suppliers based on technical support, delivery reliability, inventory management, and recovery solutions. These evolving purchasing priorities continue to influence investment decisions throughout the helium value chain.

Market Drivers

Expansion of Semiconductor Manufacturing

Semiconductor fabrication facilities require ultra-high-purity helium for wafer cooling, leak detection, plasma processing, and equipment maintenance. As manufacturers invest in advanced process nodes and larger fabrication capacity, helium consumption increases alongside production volumes. Procurement teams prioritize consistent purity specifications, uninterrupted deliveries, and technical support because production interruptions carry substantial financial consequences. Industrial gas suppliers continue expanding purification capacity and regional distribution networks to support these customer requirements.

Growing Healthcare Investment

The continued installation of MRI systems across developed and emerging healthcare markets supports liquid helium demand. Although modern MRI equipment incorporates helium conservation technologies, superconducting magnets continue to require highly reliable cryogenic cooling. Hospitals and diagnostic imaging providers increasingly evaluate lifecycle operating costs alongside supply continuity, encouraging suppliers to provide inventory management, refill scheduling, and recovery services as part of commercial agreements.

Rising Aerospace and Space Launch Activity

Government space agencies, commercial launch providers, and defense organizations utilize helium for pressurization, purging, testing, and propulsion-related operations. Increased launch frequency and satellite deployment programs have strengthened procurement requirements for high-quality helium. Suppliers capable of maintaining dependable deliveries under strict technical specifications gain competitive advantages within these specialized applications.

Industrial Quality Assurance and Manufacturing Requirements

Manufacturers across automotive, electronics, refrigeration, and energy industries rely on helium leak detection to improve product reliability and regulatory compliance. Increasing emphasis on manufacturing precision encourages investment in advanced testing systems where helium remains the preferred tracer gas because of its physical properties. Equipment suppliers and industrial gas providers continue collaborating to improve testing efficiency while minimizing helium consumption.

Market Restraints and Challenges

Limited Natural Resource Availability

Commercial helium production depends on relatively few natural gas reservoirs containing economically recoverable helium concentrations. New supply projects require substantial capital investment and extended development timelines, limiting the industry's ability to respond quickly to sudden demand increases. This constraint contributes to periodic supply shortages and pricing variability across downstream markets.

Supply Chain Disruptions and Geopolitical Exposure

Helium production remains concentrated within a limited number of producing countries. Maintenance shutdowns, geopolitical tensions, transportation disruptions, or export restrictions can significantly affect international availability. Large industrial consumers increasingly mitigate these risks through supplier diversification, strategic inventory planning, and recycling investments, although smaller buyers often have fewer procurement options.

High Logistics and Storage Costs

Liquid helium transportation requires specialized cryogenic containers, continuous temperature control, and dedicated distribution infrastructure. Transportation expenses increase substantially over long distances, particularly where regional storage capacity is limited. These logistical requirements raise delivered costs and influence purchasing decisions, especially in geographically distant markets.

Technological Efforts to Reduce Helium Consumption

Equipment manufacturers continue developing helium-efficient MRI systems, improved leak detection methods, and recycling technologies. Although these innovations improve operational efficiency and reduce waste, they may moderate consumption growth on a per-unit basis. Helium suppliers therefore increasingly focus on value-added services and integrated supply solutions rather than volume expansion alone.

Major Segment Analysis

Among all applications, cryogenics represents the most commercially significant segment because helium is uniquely capable of maintaining extremely low temperatures required by superconducting technologies. No practical alternative currently provides equivalent performance across MRI systems, nuclear magnetic resonance equipment, particle accelerators, quantum computing research, and various scientific laboratories.

Demand originates primarily from hospitals, research institutions, semiconductor research facilities, and national laboratories where uninterrupted cryogenic performance directly affects operational continuity. Buyers emphasize purity, delivery reliability, storage efficiency, and technical support rather than selecting suppliers solely on price. This purchasing behavior favors companies with extensive cryogenic logistics capabilities and established distribution infrastructure.

Commercial competition within this segment increasingly extends beyond helium supply. Providers differentiate themselves through inventory monitoring, recovery systems, maintenance services, and technical consulting designed to reduce helium losses throughout equipment operation. These service offerings strengthen long-term customer relationships while improving revenue stability through recurring contracts.

As investment continues in quantum technologies, advanced healthcare infrastructure, and scientific research facilities, cryogenic applications are expected to remain a strategic revenue contributor for helium suppliers over the forecast period.

Regional Analysis

North America

North America maintains an important position within the helium market because of established production assets, advanced healthcare infrastructure, aerospace programs, and semiconductor manufacturing investments. Demand is supported by MRI installations, defense applications, scientific research institutions, and expanding domestic semiconductor fabrication projects. Buyers increasingly prioritize supply diversification following previous market disruptions.

Europe

European demand is driven by healthcare services, industrial manufacturing, automotive engineering, scientific research, and electronics production. Environmental efficiency initiatives encourage greater adoption of helium recovery systems across industrial facilities and research laboratories. Limited domestic production increases reliance on imported supplies, making procurement resilience an important commercial consideration.

Asia Pacific

Asia Pacific represents the largest demand center for helium consumption due to extensive semiconductor manufacturing, electronics production, healthcare expansion, and industrial development. China, Japan, South Korea, and India continue investing in semiconductor fabrication capacity and advanced manufacturing, supporting sustained procurement of high-purity helium. Regional buyers increasingly seek long-term contracts to strengthen supply security amid global market fluctuations.

Middle East & Africa

The Middle East contributes both as a production region and a growing consumption market. Investments in natural gas processing and export infrastructure strengthen regional supply capabilities, while healthcare modernization and industrial diversification create additional domestic demand. African consumption remains comparatively limited but gradually expands alongside healthcare infrastructure and industrial investment.

Competitive Landscape

The helium market exhibits relatively high concentration because upstream resource ownership, purification technology, liquefaction infrastructure, and global logistics networks require substantial capital investment. Competition involves securing reliable production sources, expanding distribution capabilities, and providing specialized technical services rather than competing exclusively through pricing.

Leading companies including Air Liquide, Air Products and Chemicals, Inc., Linde plc, Messer SE & Co. KGaA, Matheson Tri-Gas, Inc., Iwatani Corporation, Nippon Sanso Holdings Corporation, Gulf Cryo S.A.L., Exxon Mobil Corporation, Gazprom PJSC, QatarEnergy LNG, and Total Helium Ltd. compete through diversified production portfolios, geographic expansion, strategic supply agreements, purification technologies, and customer-focused service models.

Suppliers increasingly strengthen competitive positioning by investing in helium recovery technologies, expanding cryogenic logistics infrastructure, securing long-term production agreements, and supporting customers with inventory optimization and engineering expertise. Geographic diversification of production assets also reduces exposure to localized operational disruptions.

Recent Developments

June 2026: Blue Star Helium Ltd. confirmed continued advancement of its U.S. helium commercialization strategy, highlighting recent Galactica/Pegasus and Voyager discovery successes while progressing additional production and exploration activities across its Colorado helium portfolio.

June 2026: The Government of Saskatchewan completed its first-ever Crown public offering for helium and associated gases on June 22, 2026, awarding 15 exploration permits to Millennium Land Ltd. across more than 267,000 hectares, strengthening future helium supply development.

May 2026: QatarEnergy LNG advanced additional helium production capacity associated with LNG infrastructure expansion, strengthening future export availability and supporting long-term international supply reliability. Commercial relevance: enhances global supply diversification.

Regulatory and Policy Environment

The helium market operates within a regulatory framework covering natural resource development, industrial gas safety, transportation, environmental compliance, and export controls. National mining and energy authorities regulate upstream extraction activities, while industrial gas handling follows occupational safety requirements governing storage, transportation, and workplace operations.

Medical applications must comply with healthcare equipment regulations governing MRI systems and cryogenic installations. Semiconductor manufacturing facilities also operate under strict quality management standards requiring consistent gas purity and traceability. International transportation of cryogenic materials follows hazardous materials regulations that establish packaging, labeling, and operational safety requirements.

Government support for semiconductor manufacturing, scientific research infrastructure, healthcare modernization, and space exploration indirectly strengthens helium demand through expanded investment in helium-intensive applications. Environmental policies additionally encourage adoption of recovery and recycling technologies that reduce resource losses while improving operational efficiency.

Outlook and Strategic Implications

Between 2026 and 2031, commercial priorities within the helium market are expected to center on supply diversification, infrastructure investment, and resource efficiency. Semiconductor manufacturing expansion, healthcare modernization, aerospace activity, and scientific research will continue supporting demand for high-purity helium despite ongoing efforts to improve consumption efficiency.

Industrial buyers are expected to increase investment in recycling systems, digital inventory monitoring, and long-term procurement agreements to reduce operational risk associated with supply disruptions. Suppliers capable of integrating production, purification, logistics, and technical services will be better positioned to secure long-duration customer relationships.

Upstream investment in new helium extraction projects and processing facilities will remain important for improving market balance, although project development timelines suggest supply additions will occur gradually. Companies with geographically diversified production portfolios are likely to demonstrate stronger resilience against geopolitical and operational disruptions.

Future competition will increasingly depend on operational reliability, technical expertise, recovery solutions, and supply chain resilience rather than commodity pricing. Organizations that successfully combine secure resource access with efficient logistics and customer-focused engineering services are expected to strengthen their commercial position as procurement strategies continue to prioritize long-term supply assurance.

Helium Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 3.5 billion |

| Total Market Size in 2031 | USD 4.1 billion |

| Forecast Unit | Billion |

| Growth Rate | 3.2% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Form, Product Type, Application, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Form

By Product Type

By Application

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Definition

2.2. Market Size & Growth Outlook

2.3. Geopolitical Risks

2.3.1. Sanctions & Shipping Disruptions

2.3.2. Production Reserves

2.3.3. Supply Security & Trade Routes

3. BUSINESS LANDSCAPE

3.1. Policies and Regulations

3.2. Pricing Benchmark

3.3. Import/Export Analysis

3.4. Middle East Geopolitical Impact on Helium Supply

3.4.1. U.S. Domestic Supply Chain Bottlenecks

3.4.2. Qatar and Middle East Logistics Constraints

3.4.3. Algerian and Russian Export Route Interruptions

4. SUPPLY CHAIN ANALYSIS

5. HELIUM DEMAND BY FORM

5.1. Introduction

5.2. Gas

5.3. Liquid

6. HELIUM DEMAND BY PRODUCT TYPE

6.1. Introduction

6.2. Merchant/Industrial Helium

6.3. Packaged Helium

7. HELIUM DEMAND BY APPLICATION

7.1. Introduction

7.2. Cryogenics

7.3. Leak Detection

7.4. Welding

7.5. Pressurization & Purging

7.6. Breathing Mixes

7.7. Others

8. HELIUM DEMAND BY END-USER

8.1. Introduction

8.2. Aerospace & Defense

8.3. Electronics & Semiconductor

8.4. Healthcare

8.5. Power & Energy

8.6. Manufacturing

8.7. Others

9. HELIUM DEMAND BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. USA

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. Germany

9.4.2. France

9.4.3. United Kingdom

9.4.4. Russia

9.4.5. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. Algeria

9.5.3. Qatar

9.5.4. Others

9.6. Asia Pacific

9.6.1. China

9.6.2. Japan

9.6.3. South Korea

9.6.4. India

9.6.5. Others

10. COMPANY PROFILES

10.1. Air Liquide

10.2. Air Products and Chemicals, Inc.

10.3. Linde plc

10.4. Messer SE & Co. KGaA

10.5. Matheson Tri-Gas, Inc.

10.6. Iwatani Corporation

10.7. Nippon Sanso Holdings Corporation

10.8. Gulf Cryo S.A.L.

10.9. Exxon Mobil Corporation

10.10. Gazprom PJSC

10.11. QatarEnergy LNG

10.12. Total Helium Ltd.

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key Benefits to the Stakeholders

11.5. Research Methodology

11.6. Abbreviations

Navigate

Trusted by the world's leading organizations