Report Overview

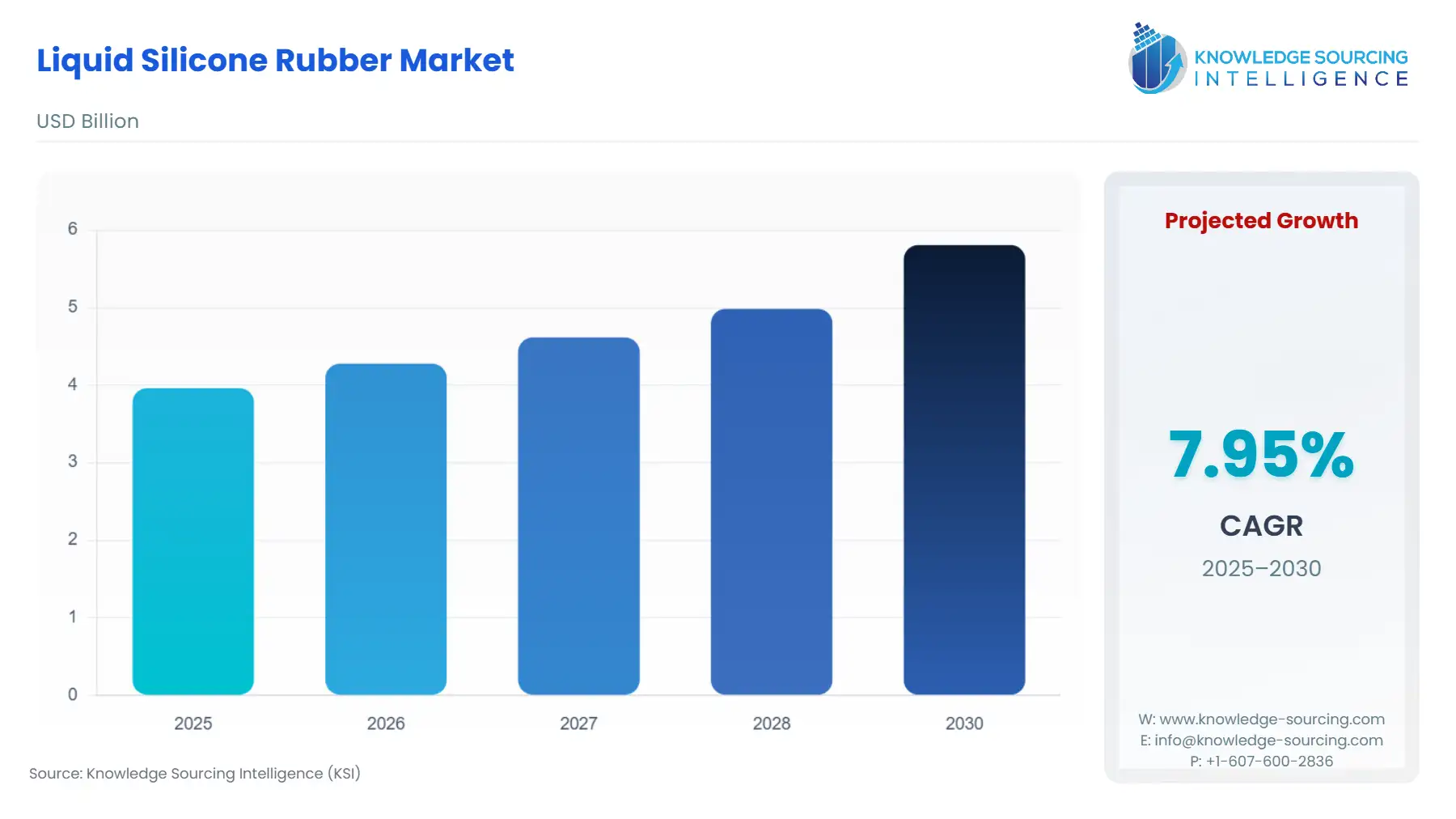

The liquid silicone rubber market is projected to grow at a CAGR of 7.95% over the forecast period, increasing from US$3.96 billion in 2025 to US$5.81 billion by 2030.

Highlights:

- 1The Dow Chemical Company

- 2Elkem Silicones (China National Bluestar Group)

- 3Wacker Chemie AG

Liquid Silicone Rubber Market Trends:

The liquid silicone rubber market is witnessing significant growth during the mentioned timeframe. The growing demand from the automotive industry, particularly electric vehicles, and healthcare, is the major factor propelling the market to grow. Its growing usage in consumer goods and electronics is also driving the market to expand.

Liquid silicone rubber is a two-component system where long polysiloxane chains are reinforced with specially treated silica. It is a biocompatible silicone that can be molded and formed into solid forms for various applications. It has several advantages, such as being highly biocompatible, which drives its increasing usage in applications such as organ parts or prostheses. It is also durable, ensuring long-term stability and chemical resistance. It is also compatible with a wide spectrum of temperatures, from -60 °C to +250 °C, maintaining its high-performance mechanical properties at all times. Additionally, its electrical properties make it ideal for insulation and precise conductivity protection.

Liquid silicone rubber Market Overview & Scope:

The liquid silicone rubber market is segmented by:

Grade Type: The liquid silicone rubber market, by grade type, is segmented into food, medical and industrial. Food-grade liquid silicone rubber is estimated to grow at a robust rate due to its demand, as it is safe and non-toxic. Apart from this, medical-grade liquid silicone is growing at a fast rate due to the demand for biocompatible materials in medical devices, implants, and wearables. As the healthcare industry continues to advance with increasingly sophisticated medical technologies, the demand for safe and durable materials for long-term implantation and use in medical devices fuels the development of the LSR market. In line with this, as per CMS, U.S. healthcare spending grew 7.5 percent in 2023, reaching $4.9 trillion or $14,570 per person.

Industry Vertical: The liquid silicone rubber market, by industry vertical, is segmented into consumer electronics, automotive, healthcare, and others. The development of the liquid silicone rubber (LSR) market for the automotive market is being spearheaded by fast growth in electric vehicles (EVs) and rising electronics content. EVs need high-performing materials to handle extreme temperatures, have superior sealing, and provide electrical insulation all of which LSR excels. As per IEA, in 2023, approximately 14 million electric cars were sold, of which ninety-five percent found consumers in Europe, China, and the United States. Compared to 2022, this figure showed a 35% increase, with 3.5 million more registered EVs. The IEA data further represented that the sale of electric cars rose from 13.7 million in 2023 to account for 16.6 million units by 2024.

Application: The liquid silicone rubber market, by application, is segmented into moldings, coatings, and industrial. The molding segment dominates the market for its usage in automotive, medical, and electronics.

Region: The Asia-Pacific region is expected to dominate the regional liquid silicone rubber market. The demand for liquid silicone rubber in the area is rapidly increasing due to the presence of the world's major consumers, such as China and India.

Top Trends Shaping the Liquid Silicone Rubber Market

1. Automotive Industry Adoption

The automotive sector remains a driving factor behind LSR market growth, particularly with the shift towards electric and hybrid vehicles. LSR's thermal stability, flexibility, and weather resistance make it a superior material for under-the-hood applications such as seals, gaskets, and vibration-damping components. In electric vehicles (EVs), where effective thermal management and sealing against moisture and dust are essential, LSR is gaining increased application in battery enclosures and electronic parts. Moreover, as cars become increasingly technologically advanced with features such as autonomous driving and intelligent interiors, the demand for tough, safe, and reliable materials such as LSR is growing at a fast pace.

2. Advancements in Manufacturing Technologies

Manufacturing technological advances, more so in liquid injection molding (LIM) and 3D printing, are transforming the design and manufacture of LSR products. LIM technology makes it possible to produce very accurate, robotized manufacturing of complex, detailed pieces with minimal scrap, improving efficiency and scalability. Moreover, the advent of 3D printing using LSR materials is providing new applications in rapid prototyping and customized manufacturing, particularly in healthcare and electronic applications. These developments reduce the cost of production, enhance product uniformity, and facilitate more design flexibility, thus enhancing LSR's use in a wide range of industries.

Liquid Silicone Rubber Market Growth Drivers vs. Challenges:

Drivers:

Growing Electricity Demand: The rapid expansion of the electric vehicle (EV) market is one of the primary drivers fueling demand for liquid silicone rubber. As global automakers shift toward cleaner, energy-efficient technologies, there is increasing demand for liquid silicone rubber to meet the needs of electric vehicles, such as lightweight products for reducing the vehicle weight, heat-resistant products for its components for withstanding the high temperatures of electric vehicles, and others.

As there is increasing adoption of EVs and increasing focus on governments on EVs for a cleaner environment, the market for liquid silicone rubber is growing robustly. As per the data by the International Energy Agency, the global sales of electric cars reached 14 million in 2923, which was 3.5 million higher than in 2023. This totaled 40 million in 2023, which was 4.9 million in 2018, 9.1 million in 2020 and 28.1 million in 2022. IEA estimates that more than one in five new cars sold in 2024 will be electric, and will continue to grow by 2030, for the cleaner energy goals of countries to align with sustainability due to climate change.

Expanding Medical Applications: The increasing application of liquid silicone rubber (LSR) in medical devices is a key growth driver, driven by the superior biocompatibility, chemical stability, and bacterial resistance of the material. LSR is widely preferred for producing critical medical devices like catheters, infusion pumps, prosthetics, pacemaker parts, and implantable devices, where safety and reliability are of utmost importance. Its resistance to sterilization procedures such as autoclaving, gamma radiation, and ethylene oxide sterilization without deterioration makes it a perfect material in healthcare environments that require high standards of hygiene and performance.

Liquid Silicone Rubber Market Regional Analysis:

North America: The North American liquid silicone rubber market, country-wise, is segmented into the United States, Canada, and Mexico. Several influential growth drivers are driving the U.S. LSR market. The healthcare industry is a prime driver, tapping into LSR's biocompatibility, optical clarity, and resistance to bacterial growth for application in implants, medical devices, and other important uses. The automotive industry, on the other hand, is also making a strong contribution to growth, since LSR's elasticity, heat stability, and resilience are critical in sophisticated gaskets, seals, and parts, particularly with escalating motor vehicle manufacturing and the movement toward electric vehicles (EVs).

In 2022, new U.S light vehicle sales were 11.5 million units, with the production of 4.9 million vehicles in 2023 as per Autos Drive America. The shift toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) will further boost LSR use, given its superior electrical insulation, flame retardancy, and environmental resilience. Moreover, heavy investments in automotive R&D will foster the development of specialized LSR grades tailored to evolving industry needs, including low-temperature curing and enhanced adhesion.

Liquid Silicone Rubber Market Regional Analysis:

Product Innovation: In February 2024, at Silicone Expo Europe, the WACKER Group showcased silicone-based product solutions for specific industrial sectors. The focus is on silicone gels for wound care, non-posturing liquid silicone rubber for the food industry and medical technology, and self-adhesive liquid silicone rubber grades that adhere to polycarbonate and other high-performance plastics.

Liquid Silicone Rubber Market Scope:

| Report Metric | Details |

|---|---|

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Companies |

|

Report Metric | Details |

Liquid Silicone Rubber Market Size in 2025 | US$3.962 billion |

Liquid Silicone Rubber Market Size in 2030 | US$5.808 billion |

Growth Rate | CAGR of 7.95% |

Study Period | 2020 to 2030 |

Historical Data | 2020 to 2023 |

Base Year | 2024 |

Forecast Period | 2025 – 2030 |

Forecast Unit (Value) | USD Billion |

Segmentation |

|

Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

List of Major Companies in the Liquid Silicone Rubber Market | |

Customization Scope | Free report customization with purchase |

Liquid Silicone Rubber Market Segmentation:

By Grade Type

Food

Medical

Industrial

By Industry Vertical

Consumer Electronics

Automotive

Healthcare

Others

By Application

Injection Molding Components

Seals & Gaskets

Medical Devices & Implants

Electrical Insulation

Coatings & Encapsulation

Others

By Region

North America

USA

Canada

Mexico

South America

Brazil

Argentina

Others

Europe

Germany

France

United Kingdom

Spain

Others

Middle East and Africa

Saudi Arabia

UAE

Israel

Others

Asia Pacific

China

Japan

India

South Korea

Indonesia

Taiwan

Others

Market Segmentation

By Grade Type

By Industry Vertical

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL ADVANCEMENTS

5. LIQUID SILICONE RUBBER MARKET BY GRADE TYPE

5.1. Introduction

5.2. Food

5.3. Medical

5.4. Industrial

6. LIQUID SILICONE RUBBER MARKET BY INDUSTRY VERTICAL

6.1. Introduction

6.2. Consumer Electronics

6.3. Automotive

6.4. Healthcare

6.5. Others

7. LIQUID SILICONE RUBBER MARKET BY APPLICATION

7.1. Introduction

7.2. Injection Molding Components

7.3. Seals & Gaskets

7.4. Medical Devices & Implants

7.5. Electrical Insulation

7.6. Coatings & Encapsulation

7.8. Others

8. LIQUID SILICONE RUBBER MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. USA

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Argentina

8.3.3. Others

8.4. Europe

8.4.1. United Kingdom

8.4.2. Germany

8.4.3. France

8.4.4. Spain

8.4.5. Others

8.5. Middle East and Africa

8.5.1. Saudi Arabia

8.5.2. UAE

8.5.3. Others

8.6. Asia Pacific

8.6.1. China

8.6.2. Japan

8.6.3. India

8.6.4. South Korea

8.6.5. Taiwan

8.6.6. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. The Dow Chemical Company

10.2. KCC Corporation

10.3. Elkem Silicones (China National Bluestar Group)

10.4. Wacker Chemie AG

10.5. Avantor Inc.

10.6. Stockwell Elastomerics Inc.

10.7. Reiss Manufacturing Inc.

10.8. SIMTEC Silicone Parts LLC

10.9. Nano Tech Chemical Brothers Pvt. Ltd.

10.10. Shin-Etsu Chemical Co., Ltd.

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key Benefits for the Stakeholders

11.5. Research Methodology

11.6. Abbreviations

Navigate

Trusted by the world's leading organizations