Report Overview

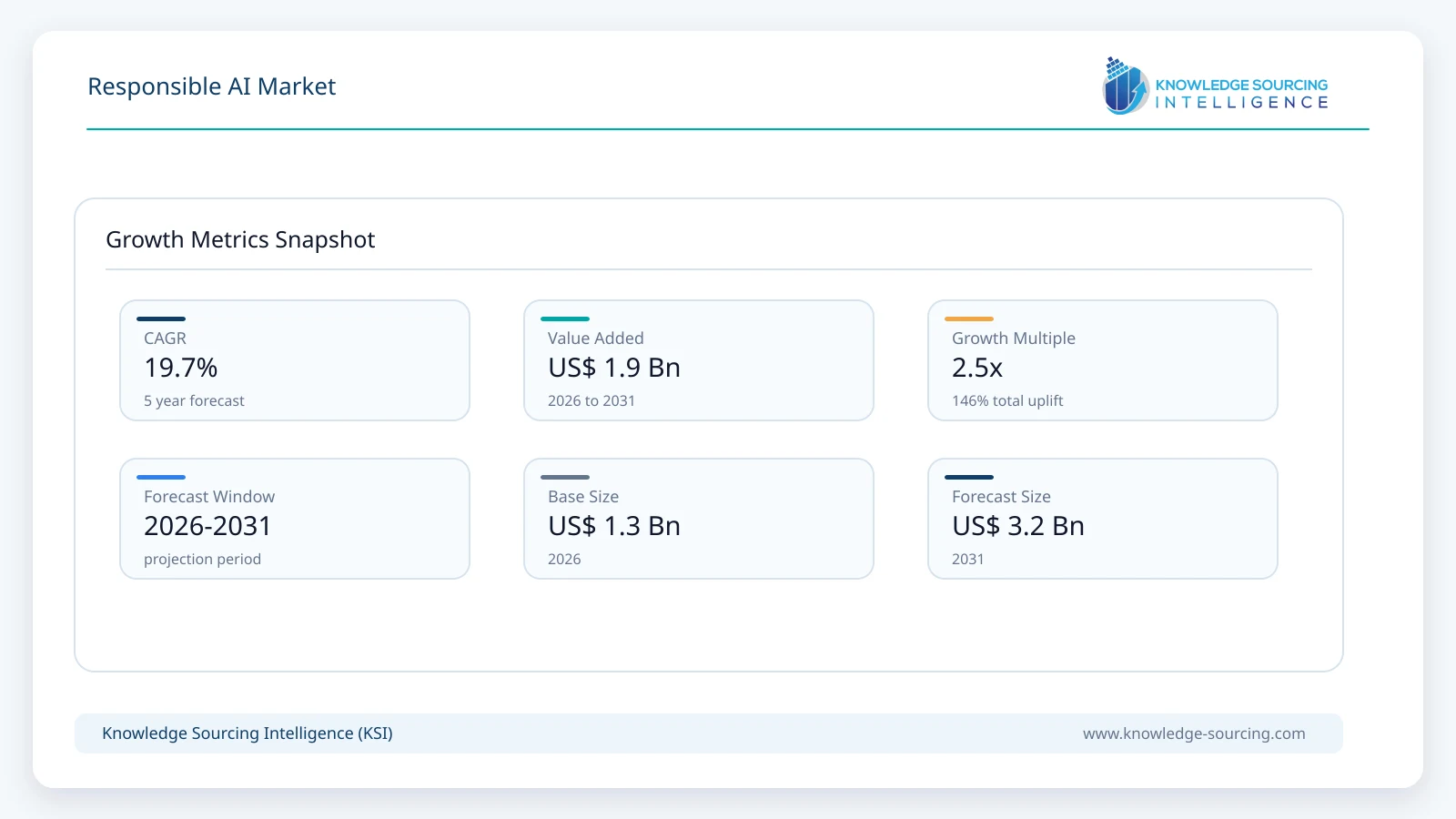

The Responsible AI Market is forecast to grow at a CAGR of 19.7%, reaching USD 3.2 billion in 2031 from USD 1.3 billion in 2026.

Highlights:

- 1Largest End-UserThe Banking, Financial Services, and Insurance (BFSI) sector represents the largest end-user segment due to the critical nature of credit scoring and fraud detection models, which must meet stringent anti-discrimination laws.

- 2Regulatory ImpactThe extraterritorial application of the EU AI Act has forced global firms to adopt standardized auditing protocols, directly increasing the demand for third-party compliance services and certification tools.

- 3Regional LeaderNorth America maintains the leading market position, driven by the early adoption of the NIST AI Risk Management Framework (AI RMF) and significant private sector investment in AI safety research by firms such as Anthropic and Microsoft.

- 4Technology TransitionThere is a significant transition toward "Constitutional AI," where models are trained to adhere to a predefined set of principles (a constitution) to evaluate and refine their own outputs without constant human intervention.

Structural demand for Responsible AI is primarily driven by the institutionalization of risk management within enterprise operations. Organizations are no longer viewing AI ethics as a branding exercise but as a fundamental requirement for operational continuity. This shift is catalyzed by high-profile instances of algorithmic failure and the subsequent litigation or regulatory penalties that follow. Industry dependency factors are heavily tied to the financial services, healthcare, and public sectors, where automated decisions directly impact human rights, financial health, and social equity. As these sectors increasingly rely on Large Language Models (LLMs) and agentic systems, the demand for governance-by-design has moved from a peripheral concern to a core architectural requirement.

The technological advancement of the artificial intelligence industry is increasingly defined by the shift toward real-time observability and automated policy enforcement during runtime operations. Conventional GRC (Governance, Risk, and Compliance) frameworks are being enhanced or substituted by AI-native solutions that can continuously detect model drift, bias, and performance anomalies across evolving datasets. In addition, the growing significance of Responsible AI is reinforced by its ability to strengthen consumer confidence and trust. As digital awareness expands, users are more inclined to adopt systems that offer transparent and understandable decision-making processes. As a result, the movement toward “Trustworthy AI” is emerging as a key competitive advantage, encouraging leading technology companies to integrate transparency mechanisms and robust safety controls throughout their product development lifecycles.

Market Dynamics

Market Drivers

Growth of Agentic AI Systems: As businesses transition from simple chatbots to semi-autonomous agents capable of task delegation, the complexity of managing "agentic drift" drives demand for advanced monitoring and accountability platforms.

Public Sector Digital Transformation: Governments worldwide are adopting AI for social services and law enforcement, necessitating "Black Box" transparency tools to ensure that public-sector automation remains contestable and fair.

Standardization of AI Auditing: The release of international standards such as ISO/IEC 42001 (Artificial Intelligence Management System) provides a benchmark for organizations to demonstrate compliance, fueling the demand for professional auditing and consulting services.

Market Restraints and Opportunities

Global Regulatory Fragmentation: Differing standards between the United States, Europe, and Asia Pacific create a complex compliance environment that can stifle innovation for smaller firms unable to afford multi-jurisdictional legal and technical audits.

Skills Shortage in AI Ethics: A critical lack of professionals who possess both technical data science skills and legal/ethical expertise limits the ability of firms to operationalize governance frameworks effectively.

Innovation vs. Safety Trade-off: Intense competitive pressure to release "Frontier Models" quickly can lead to the deprioritization of safety testing, though this increasingly represents a long-term reputational and legal risk.

Emerging Market Potential for Bias Mitigation: The high prevalence of diverse demographics in emerging markets like India and Brazil offers a significant opportunity for the development of localized bias-mitigation tools that handle multilingual and multicultural data nuances.

Supply Chain Analysis

The supply chain for the Responsible AI market is highly integrated with the broader AI development stack but features a unique layer of specialized "safety and trust" providers. At the base are the compute providers (GPU manufacturers) and cloud infrastructure leaders who are increasingly embedding "Responsible AI" hubs into their platforms to retain enterprise clients. Above this layer sit the model developers who provide the foundational "Constitutional" logic and safety-aligned models. The downstream layer consists of specialized software vendors offering "plug-and-play" bias detection, explainability, and auditing tools that sit on top of third-party models.

Production concentration is currently high, with a few major hyperscalers controlling the primary governance platforms. This concentration creates a dependency risk, as changes in the base provider's safety policies can disrupt the entire downstream governance workflow. However, an emerging "open-source safety" movement is gaining traction, providing developers with free tools for model evaluation and red-teaming. The regional risk exposure is centered on the availability of high-quality, "clean" datasets for training, with increasing pressure on the supply chain to provide data provenance and lineage tracking to ensure intellectual property and privacy rights are respected.

Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

Europe | EU AI Act (2024/1689) | Mandates strict conformity assessments for "High-Risk" AI; imposes fines up to €35M or 7% of turnover for non-compliance. |

United States | NIST AI Risk Management Framework (AI RMF) | Provides a voluntary but widely adopted standard for identifying and managing AI risks; influences federal procurement requirements. |

United States | Executive Order 14110 (Safe, Secure, and Trustworthy AI) | Requires developers of the most powerful AI systems to share safety test results and other critical information with the government. |

International | ISO/IEC 42001 | The world’s first AI management system standard; enables organizations to certify their AI governance processes for global trade. |

Key Developments

June 2026: At the Hamburg Sustainability Conference 2026, UNDP, the International Chamber of Commerce (ICC), and the German Federal Ministry for Economic Cooperation and Development (BMZ) advanced the Hamburg Declaration on Responsible AI for the SDGs, expanding industry commitments and reviewing implementation progress.

May 2026: Pope Leo XIV, together with Anthropic co-founder Christopher Olah, launched the encyclical Magnifica Humanitas, emphasizing responsible AI, protection of human dignity, and ethical governance of artificial intelligence amid accelerating global AI adoption.

February 2026: The IndiaAI Mission officially released the AI Compendium during the India AI Impact Summit 2026, showcasing verified real-world AI applications and responsible AI implementation practices across priority sectors to support trustworthy AI adoption.

December 2025: IBM rolls out watsonx.governance 2.1 to accelerate responsible AI workflows. IBM announced the general availability of watsonx.governance 2.1, enhancing governance automation, risk assessment, and ethical AI monitoring across model lifecycles.

December 2025: HCLTech joins AI Verify Foundation to advance Responsible AI. HCLTech joined the AI Verify Foundation, committing to global trustworthy AI practices aligned with international AI governance principles and frameworks.

Market Segmentation

By Component: Software Tools and Platforms

The software segment is the primary engine of market growth, comprising standalone bias-detection tools, explainability dashboards, and end-to-end governance platforms. The need for "automated transparency" in complex neural networks drives this demand. As organizations scale their AI deployments, manual auditing becomes unfeasible, necessitating software that can provide continuous, real-time monitoring of model behavior. This segment is characterized by high R&D investment as vendors seek to create tools that can support diverse AI architectures, including both proprietary and open-source models.

By End-User: BFSI

The BFSI sector remains the leading end-user of Responsible AI solutions due to the high-stakes nature of its operations. Financial institutions are under intense pressure to explain why an AI system denied a loan or flagged a transaction as fraudulent. Consequently, demand in this segment is focused on "Explainability-as-a-Service" and bias mitigation to prevent disparate impact on protected classes. The structural demand is reinforced by sector-specific regulations (e.g., Fair Lending acts) that require documented proof of non-discrimination in automated systems.

By Deployment: Cloud

Cloud-based deployment offers significant operational advantages, particularly for Small and Medium Enterprises (SMEs) that lack the infrastructure to host complex governance frameworks locally. Cloud providers like AWS and Azure offer integrated "Responsible AI" suites that simplify evidence collection for audits and provide scalable monitoring capabilities. This model allows for rapid updates to governance tools as new regulations emerge, ensuring that firms remain compliant without significant hardware investment.

Regional Analysis

North America

North America is the dominant region, characterized by a mature ecosystem of AI safety labs and tech giants. The voluntary but pervasive adoption of the NIST AI RMF across federal and commercial sectors drives this demand. The presence of leading innovators like Alphabet and Anthropic ensures that the region remains at the forefront of "Frontier AI" safety research. Furthermore, the U.S. executive branch’s focus on AI security and trustworthiness has institutionalized Responsible AI within the national defense and intelligence supply chains.

Europe

The European market is the global regulator of the "Responsible AI" space. The enforcement of the EU AI Act has created an immediate and non-negotiable demand for compliance software and professional services. European companies are leading the "Governance-by-Design" transition, as the cost of failure is legally prohibitive. The industrial base is focused on specialized sectors like manufacturing and healthcare, where the integration of AI must meet the continent's high standards for digital sovereignty and human-centric design.

Asia Pacific

The Asia Pacific region, led by China and India, is experiencing rapid growth in Responsible AI adoption. China’s specific regulations regarding recommendation algorithms and generative AI have forced a rapid shift toward transparency in its massive consumer tech sector. In India, the market is driven by the "AI for All" initiative, which emphasizes inclusive and ethical AI growth. The regional demand is increasingly focused on localized bias mitigation to handle the vast linguistic and cultural diversity of the population.

List of Companies

Accenture plc

Amazon Web Services, Inc. (AWS)

SAP SE

IBM

Fair Isaac Corporation (FICO)

Alphabet Inc.

Salesforce, Inc.

Microsoft Corporation

Anthropic PBC

Intel Corporation

IBM

IBM occupies a leading position in the Responsible AI market through its "watsonx.governance" platform, which automates model risk management and compliance tracking. The company’s strategy is built on the "Principles for Trust and Transparency," which emphasize that the purpose of AI is to augment, not replace, human intelligence. IBM’s competitive advantage lies in its deep consulting expertise, allowing it to provide end-to-end governance frameworks tailored to highly regulated industries like banking and healthcare. Its technological differentiation is highlighted by its "Granite" models, recognized for their high levels of transparency and alignment with safety ethics.

Microsoft Corporation

Microsoft’s strategy in the Responsible AI space is centered on "Shared Responsibility," where it provides customers with the tools and transparency documents needed to build their own compliant systems. The company has integrated responsible AI guardrails directly into its Azure AI and Copilot ecosystems. Microsoft’s competitive advantage is its massive scale and its ability to influence global standards through its annual Transparency Reports. By offering tools like "Fairlearn" and "InterpretML," Microsoft empowers developers to measure and mitigate bias, reinforcing its position as a key infrastructure provider for trustworthy enterprise AI.

Fair Isaac Corporation (FICO)

FICO is a specialized leader in the Responsible AI market, particularly within the financial sector. The company’s strategy focuses on "Applied Intelligence," utilizing its extensive patent portfolio, which includes over 230 active patents, to solve critical challenges in bias detection and fraud prevention. FICO’s competitive advantage is its established trust with thousands of financial institutions worldwide that use the FICO Platform for decisioning. Its technology differentiation lies in its "Latent-Space Misalignment" measures and real-time concept drift algorithms, which ensure that machine learning models remain aligned with business and ethical requirements throughout their lifecycle.

Analyst View

Global regulatory enforcement and the rise of autonomous agentic systems are structurally accelerating demand for Responsible AI. While fragmented international standards present operational hurdles, the shift toward real-time, automated governance is establishing trust as a primary competitive advantage.

Responsible AI Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 1.3 billion |

| Total Market Size in 2031 | USD 3.2 billion |

| Forecast Unit | Billion |

| Growth Rate | 19.7% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Deployment, End-User, Geography |

| Companies |

|

Market Segmentation

By Component

By Deployment

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. RESPONSIBLE AI MARKET BY COMPONENT

5.1. Introduction

5.2. Software Tools and Platforms

5.3. Services

6. RESPONSIBLE AI MARKET BY DEPLOYMENT

6.1. Introduction

6.2. On-Premises

6.3. Cloud

7. RESPONSIBLE AI MARKET BY END-USER

7.1. Introduction

7.2. Healthcare

7.3. BFSI

7.4. Government and Public Sector

7.5. Automotive Industry

7.6. IT and Telecommunication

7.7. Others

8. RESPONSIBLE AI MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Component

8.2.2. By Deployment

8.2.3. By End-User

8.2.4. By Country

8.2.4.1. United States

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Component

8.3.2. By Deployment

8.3.3. By End-User

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Component

8.4.2. By Deployment

8.4.3. By End-User

8.4.4. By Country

8.4.4.1. United Kingdom

8.4.4.2. Germany

8.4.4.3. France

8.4.4.4. Spain

8.4.4.5. Others

8.5. Middle East and Africa

8.5.1. By Component

8.5.2. By Deployment

8.5.3. By End-User

8.5.4. By Country

8.5.4.1. Saudi Arabia

8.5.4.2. UAE

8.5.4.3. Others

8.6. Asia Pacific

8.6.1. By Component

8.6.2. By Deployment

8.6.3. By End-User

8.6.4. By Country

8.6.4.1. Japan

8.6.4.2. China

8.6.4.3. India

8.6.4.4. South Korea

8.6.4.5. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Accenture plc

10.2. Amazon Web Services, Inc.

10.3. SAP SE

10.4. IBM

10.5. Fair Isaac Corporation (FICO)

10.6. Alphabet Inc.

10.7. Salesforce, Inc.

10.8. Microsoft Corporation

10.9. Anthropic PBC

10.10. Intel Corporation

11. RESEARCH METHODOLOGY

List of Figures

List of Tables

Navigate

Trusted by the world's leading organizations