Report Overview

Scar Treatment Market Size:

The Scar Treatment Market will surge from USD 17.112 billion in 2025 to USD 25.096 billion by 2030, fueled by a 7.96% compound annual growth rate (CAGR).

Highlights:

- 1Acne scars dominate due to high global prevalence, driving demand for topical treatments.

- 2North America leads with advanced healthcare; Asia Pacific grows fastest due to aesthetic awareness.

- 3Topical products lead treatment types; innovations like Silagen’s 2023 gel enhance efficacy.

- 4High costs of laser therapies and limited OTC evidence restrain market growth.

The scar treatment market represents a rapidly growing segment of the global healthcare and aesthetics industry, addressing the medical and cosmetic needs associated with scarring from injuries, surgeries, burns, and skin conditions such as acne. Scars, formed during the body’s natural healing process, can impact physical appearance, psychological well-being, and, in severe cases, functional mobility.

The scar treatment market is a dynamic segment within dermatology aesthetics, focusing on innovative scar revision market solutions. Advances in wound healing solutions drive effective therapies for cosmetic scar removal, addressing both aesthetic and functional concerns. The skin repair market is expanding with non-invasive treatments like lasers, microneedling, and topical formulations, catering to diverse scar types, including post-surgical scar management. Growing consumer demand for minimally invasive procedures and improved skin outcomes fuels market growth. As technologies evolve, industry experts see significant potential in personalized, high-efficacy treatments that enhance patient satisfaction and quality of life in scar management.

The market offers diverse solutions, including topical products, laser therapies, and injectable treatments, tailored to various scar types such as keloid, contracture, hypertrophic, and acne scars. With technological advancements, increasing aesthetic awareness, and a rising incidence of skin-related conditions, the scar treatment market is experiencing significant expansion, serving consumers across hospitals, clinics, pharmacies, and online platforms.

Scar Treatment Market Overview:

Scarring occurs when fibrous tissue replaces normal skin following trauma, surgery, or dermatological conditions. The scar treatment market addresses both aesthetic and functional concerns through a variety of products and procedures. It is segmented by scar type (keloid, contracture, hypertrophic, and acne scars), treatment type (topical products, laser treatments, and injectables), end-user (hospitals, clinics, pharmacies, and drug stores), distribution channel (online and offline), and geography (North America, South America, Europe, Middle East and Africa, and Asia Pacific). Each segment caters to specific consumer needs, with adoption rates influenced by technological innovation, accessibility, and regional preferences.

The global scar treatment market is projected to grow at a compound annual growth rate (CAGR) of approximately 8-10% through the late 2020s, driven by increasing demand for effective scar management solutions. This growth is fueled by advancements in treatment technologies, rising aesthetic consciousness, and the growing prevalence of skin injuries and conditions. The market is further supported by the development of innovative products, such as advanced topical formulations and laser systems, which improve treatment outcomes and patient satisfaction.

Scar Treatment Market Trends:

The scar treatment market is evolving with personalized scar therapy, tailoring solutions to individual skin types and scar characteristics. Minimally invasive scar treatments, such as laser therapy and microneedling, dominate due to their efficacy and reduced downtime. Home-use scar devices, like silicone patches and LED tools, are gaining popularity, driven by consumer aesthetic awareness. Tele-dermatology scar assessment enables remote consultations, enhancing accessibility. Evidence-based scar care, supported by clinical studies, ensures reliable outcomes, boosting trust among professionals. These trends reflect a shift toward patient-centric, accessible, and scientifically validated approaches, reshaping the landscape of scar management.

Scar Treatment Market Segment Analysis:

By Scar Type

The market is segmented into keloid scars, contracture scars, hypertrophic scars, and acne scars, each requiring distinct treatment approaches.

-

Keloid Scars: These are raised, proliferative scars that extend beyond the original wound due to excessive collagen production. They are more common in individuals with darker skin tones and often result from burns, surgery, or minor injuries. Keloid scars are challenging to treat due to their high recurrence rates, driving demand for specialized therapies like corticosteroid injections and laser treatments.

-

Contracture Scars: Typically caused by burns, contracture scars lead to skin tightening, which can restrict movement and cause functional impairments. Treatments such as surgical revision, laser therapy, and physical therapy are used to restore mobility and improve appearance, particularly for burn survivors.

-

Hypertrophic Scars: These raised scars remain within the boundaries of the original wound and are often caused by trauma or surgery. They are less severe than keloids but can cause discomfort and aesthetic concerns. Common treatments include silicone-based products, laser therapies, and injectables, with a growing preference for non-invasive options.

-

Acne Scars: Atrophic acne scars, characterized by pitted or depressed skin, are highly prevalent, especially among adolescents and young adults. These scars result from acne, chickenpox, or other inflammatory skin conditions. Topical products dominate treatment due to their accessibility, while laser therapies are increasingly used for severe cases.

By Treatment Type

The market is divided into topical products, laser treatments, and injectables, each addressing different scar types and consumer preferences.

-

Topical Products: This segment includes creams, gels, silicone sheets, and other over-the-counter (OTC) or prescription products. Topical treatments are popular for their affordability, ease of use, and availability, particularly for acne and hypertrophic scars. Recent advancements, such as silicone gels with growth factors, have improved their effectiveness.

-

Laser Treatments: Laser therapies, such as fractional CO2 lasers and pulsed-dye lasers, are gaining traction for their ability to treat deeper scars like keloids and contractures. These treatments promote collagen remodeling and improve scar texture and color, making them a preferred choice in clinical settings.

-

Injectables: Injectables, including corticosteroids, hyaluronic acid, and 5-fluorouracil, are used primarily for keloid and hypertrophic scars. They reduce inflammation and promote scar flattening, offering targeted solutions for raised scars.

By End-User

The market is segmented into hospitals, clinics, and pharmacies/drug stores, reflecting the diverse settings where scar treatments are accessed.

-

Hospitals: Hospitals lead this segment due to their advanced infrastructure, access to laser technologies, and capability to perform surgical scar revisions. They primarily serve patients with severe scars, such as contractures and keloids.

-

Clinics: Dermatology and aesthetic clinics offer specialized treatments like laser therapy and injectables, catering to consumers seeking professional care for cosmetic concerns.

-

Pharmacies & Drug Stores: This segment is critical for distributing OTC topical products, appealing to consumers with mild scars who prefer self-treatment.

By Distribution Channel

The market is split into online and offline channels, reflecting evolving consumer purchasing behaviors.

-

Online: E-commerce platforms have expanded access to scar treatment products, especially OTC topical solutions. Online channels offer convenience and variety, appealing to younger, digitally savvy consumers.

-

Offline: Retail pharmacies and drug stores remain a key channel, particularly for prescription products and in regions with limited internet access.

Scar Treatment Market Geographical Outlook:

The scar treatment market is analyzed across North America, South America, Europe, the Middle East and Africa, and Asia Pacific, with distinct regional trends.

-

North America (US, Canada, Mexico): North America dominates the market, driven by advanced healthcare systems, high consumer awareness, and the presence of key industry players. The US is the largest contributor, with strong demand for laser treatments and injectables due to the high prevalence of acne and surgical scars. The FDA’s clearance of Cynosure’s PicoSure Pro laser for scar treatment in 2024 has further strengthened the region’s market.

-

Asia Pacific (China, Japan, India, South Korea, Thailand, Indonesia, Others): Asia Pacific is the fastest-growing region, fueled by rising disposable incomes, increasing aesthetic awareness, and a high incidence of acne and trauma-related scars. China and India are key markets, with a 2023 study in the Asian Journal of Dermatology reporting a 6.8% prevalence of acne scars in China. Innovations like Singapore’s A*STAR-developed microneedle patches for scar treatment in 2024 are driving regional growth.

Scar Treatment Market Growth Drivers:

-

Increasing Prevalence of Skin Conditions: The rising incidence of acne, burns, and trauma-related injuries drives demand. WHO data indicates that burns affect approximately 11 million people annually, many requiring scar treatment.

-

Growing Aesthetic Awareness: Global emphasis on physical appearance, amplified by social media, boosts demand for scar treatments, particularly among younger demographics.

-

Technological Innovations: Advances in laser technologies (e.g., Cynosure’s PicoSure Pro) and topical formulations (e.g., Silagen’s 2023 silicone gel) enhance treatment outcomes, driving market growth.

-

Rise in Surgical Procedures: Increasing cosmetic and reconstructive surgeries globally heighten the need for post-surgical scar management, particularly through topical products and laser therapies.

Scar Treatment Market Restraints:

-

High Costs of Advanced Treatments: Laser therapies and injectables are costly, limiting accessibility in low-income regions and among price-sensitive consumers.

-

Limited Efficacy of OTC Products: Many topical products lack robust clinical evidence, which can undermine consumer confidence and slow market growth.

-

Shortage of Skilled Professionals: The lack of trained dermatologists in some regions restricts the adoption of advanced treatments like laser therapy.

Scar Treatment Market Key Developments:

-

2023: Silagen introduced an advanced silicone gel with enhanced hydration properties for hypertrophic and keloid scar treatment.

-

2024: Cynosure’s PicoSure Pro laser received FDA clearance for acne scar and wrinkle treatment, offering improved precision and efficacy.

-

2024: Singapore’s A*STAR developed microneedle patches for scar treatment, delivering active ingredients directly to scar tissue.

List of Top Scar Treatment Companies:

- CCA Industries, Inc.

- Cynosure, Inc.

- Smith & Nephew plc

- Sientra, Inc.

- Lumenis

Segmentation

- By Scar Type

- Keloid Scars

- Contracture Scars

- Hypertrophic Scars

- Acne Scars

- Burn Scars

- Post-Surgical Scars

- Others

- By Treatment Type

- Silicone-based Products

- Sheets

- Gels

- Topicals Creams & Ointments

- Surgical & Procedural Treatments

- Laser Therapy

- Microneedling

- Cryotherapy

- Chemical Peels

- Injectables

- Steroid Injections

- Fillers

- Silicone-based Products

- By End-User

- Hospitals & Clinics

- Retail

- Medical Spas

- By Distribution Channel

- Online

- Offline

- Hospital Pharmacies

- Retail

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Others

- Middle East & Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- Japan

- China

- India

- South Korea

- Taiwan

- Others

- North America

Scar Treatment Market Scope:

| Report Metric | Details |

|---|---|

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Report Metric | Details |

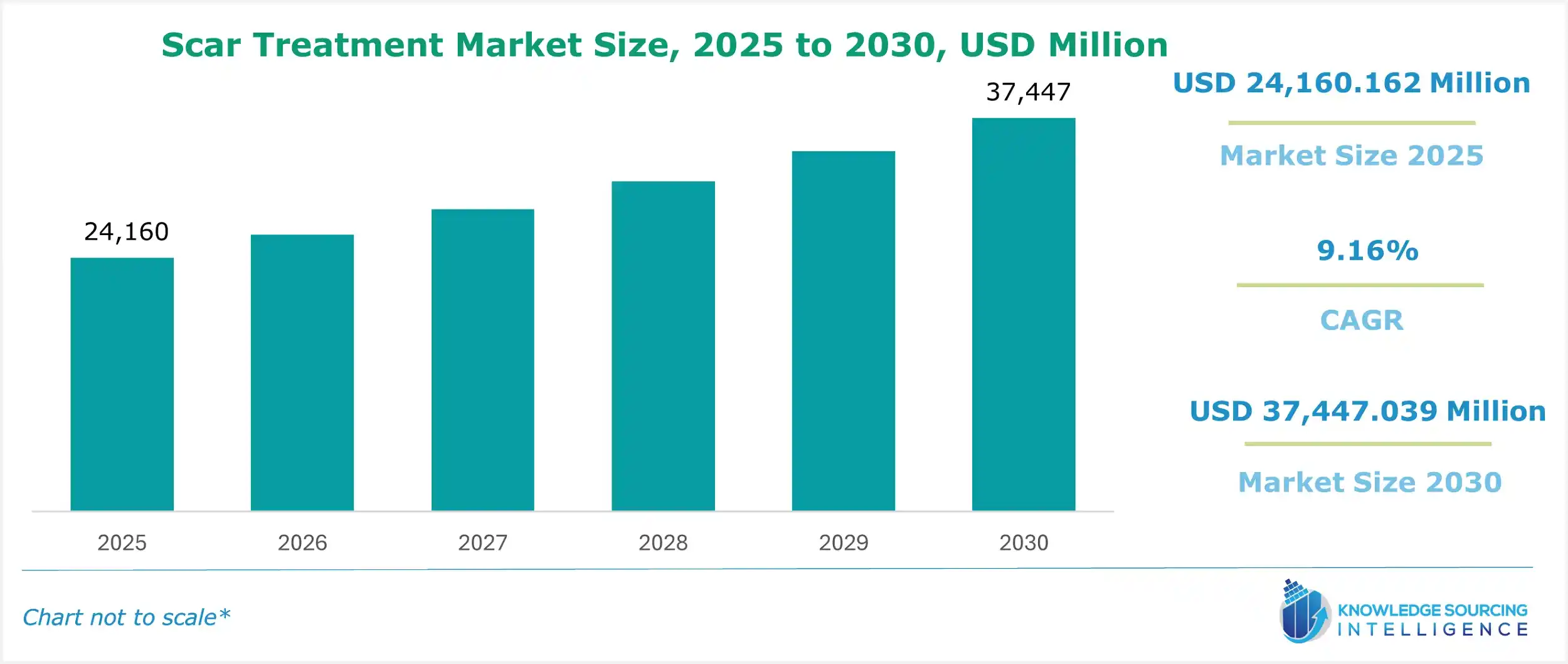

| Scar Treatment Market Size in 2025 | USD 24,160.162 million |

| Scar Treatment Market Size in 2030 | USD 37,447.039 million |

| Growth Rate | CAGR of 9.16% |

| Study Period | 2020 to 2030 |

| Historical Data | 2020 to 2023 |

| Base Year | 2024 |

| Forecast Period | 2025 – 2030 |

| Forecast Unit (Value) | USD Million |

| Segmentation |

|

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| List of Major Companies in Scar Treatment Market |

|

| Customization Scope | Free report customization with purchase |

Our Best-Performing Industry Reports:

Market Segmentation

By Scar Type

By Treatment Type

By End-user

By Distribution Channel

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. SCAR TREATMENT MARKET BY SCAR TYPE

5.1. Introduction

5.2. Keloid Scars

5.3. Contracture Scars

5.4. Hypertrophic Scars

5.5. Acne Scars

5.6. Burn Scars

5.7. Post-Surgical Scars

5.8. Others

6. SCAR TREATMENT MARKET BY TREATMENT TYPE

6.1. Introduction

6.2. Silicone-based Products

6.2.1. Sheets

6.2.2. Gels

6.3. Topicals Creams & Ointments

6.4. Surgical & Procedural Treatments

6.4.1. Laser Therapy

6.4.2. Microneedling

6.4.3. Cryotherapy

6.4.4. Chemical Peels

6.5. Injectables

6.5.1. Steroid Injections

6.5.2. Fillers

7. SCAR TREATMENT MARKET BY END-USER

7.1. Introduction

7.2. Hospitals & Clinics

7.3. Retail

7.4. Medical Spas

8. SCAR TREATMENT MARKET BY DISTRIBUTION CHANNEL

8.1. Introduction

8.2. Online

8.3. Offline

8.3.1. Hospital Pharmacies

8.3.2. Retail

9. SCAR TREATMENT MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. By Scar Type

9.2.2. By Treatment Type

9.2.3. By End-User

9.2.4. By Distribution Channel

9.2.5. By Country

9.2.5.1. United States

9.2.5.2. Canada

9.2.5.3. Mexico

9.3. South America

9.3.1. By Scar Type

9.3.2. By Treatment Type

9.3.3. By End-User

9.3.4. By Distribution Channel

9.3.5. By Country

9.3.5.1. Brazil

9.3.5.2. Argentina

9.3.5.3. Others

9.4. Europe

9.4.1. By Scar Type

9.4.2. By Treatment Type

9.4.3. By End-User

9.4.4. By Distribution Channel

9.4.5. By Country

9.4.5.1. United Kingdom

9.4.5.2. Germany

9.4.5.3. France

9.4.5.4. Italy

9.4.5.5. Others

9.5. Middle East & Africa

9.5.1. By Scar Type

9.5.2. By Treatment Type

9.5.3. By End-User

9.5.4. By Distribution Channel

9.5.5. By Country

9.5.5.1. Saudi Arabia

9.5.5.2. UAE

9.5.5.3. Others

9.6. Asia Pacific

9.6.1. By Scar Type

9.6.2. By Treatment Type

9.6.3. By End-User

9.6.4. By Distribution Channel

9.6.5. By Country

9.6.5.1. Japan

9.6.5.2. China

9.6.5.3. India

9.6.5.4. South Korea

9.6.5.5. Taiwan

9.6.5.6. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. CCA Industries, Inc.

11.2. Cynosure Lutronic

11.3. Smith & Nephew plc

11.4. Lumenis

11.5. Merz Pharma

11.6. Sonoma Pharmaceuticals, Inc.

11.7. NewMedical Technology, Inc.

11.8. Bausch Health Companies Inc.

11.9. BirchBioMed

11.10. Perrigo Company plc

11.11. Stratpharma

11.12. Mölnlycke Health Care AB

11.13. Alliance Pharma

12. RESEARCH METHODOLOGY

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations