Report Overview

Semiconductor CVD Equipment Market Size:

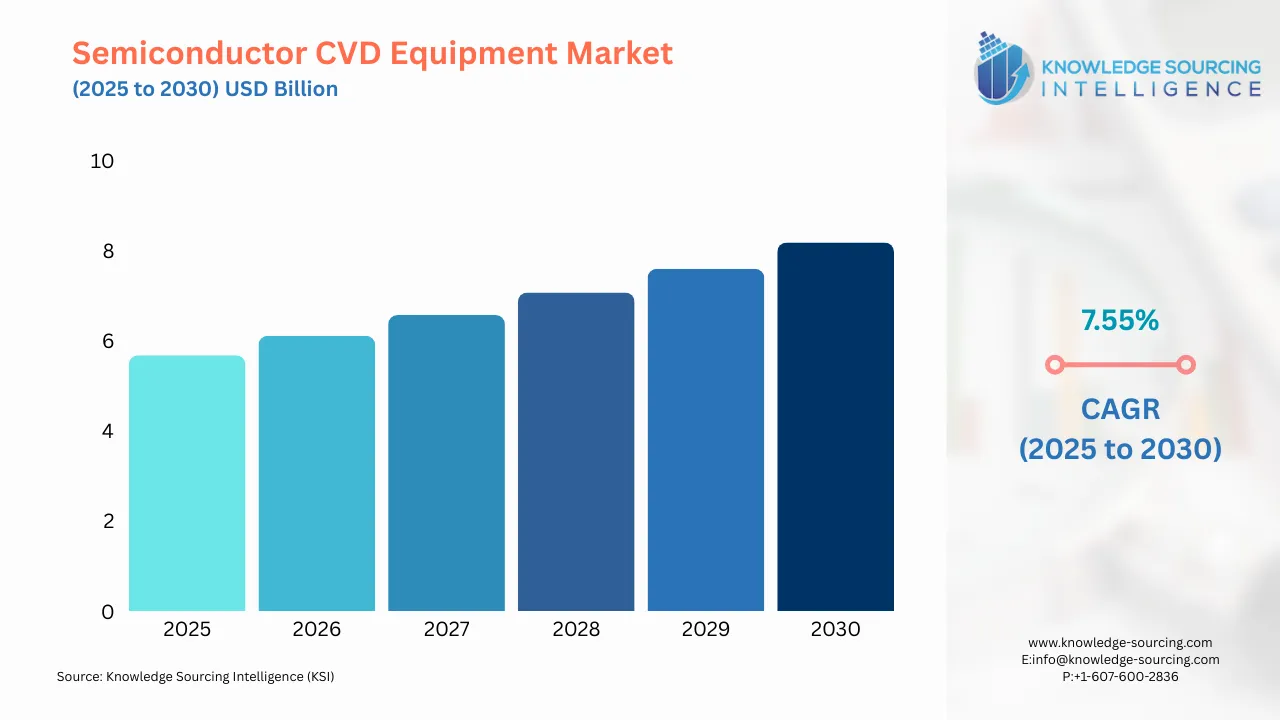

Semiconductor CVD Equipment Market, at a 7.55% CAGR, is projected to increase from USD 5.683 billion in 2025 to USD 8.179 billion in 2030.

Highlights:

- 1Increasing electronics demandis driving growth in the semiconductor CVD equipment market.

- 2Growing AI and IoT adoptionis boosting the need for advanced CVD solutions.

- 3Asia Pacificis leading the CVD equipment market with robust manufacturing.

- 4Advancing solar cell productionis fueling demand for CVD deposition systems.

- 5Rising government investmentsare supporting semiconductor CVD equipment expansion.

- 6Expanding microelectronics sectoris enhancing the use of precision CVD technologies.

- 7Strengthening environmental regulationspromotes sustainable CVD chemical processes.

Semiconductor CVD Equipment Market Trends:

Chemical vapour deposition is a technique that uses a chemical reaction that occurs on or near a substrate surface to deposit a solid substance from a vapour (CVD). The performance of the CVD method in semiconductor manufacturing processes is improved by the use of CVD equipment. In most cases, chemical vapour deposition is utilised to produce conformal coatings and change substrate surfaces in ways that are not possible with conventional surface modification techniques. For creating materials with atomically thin layers, CVD is particularly helpful. Solar cells in particular have been shown to encourage development and are anticipated to have significant potential over the upcoming years. The demand for solar photovoltaic cells is rising due to the depletion of conventional energy sources and rising greenhouse gas emissions, which is anticipated to accelerate the expansion of the CVD industry.

The key drivers of the expansion of the CVD equipment market are rigorous rules controlling the use of Cr6 for electroplating, faster growth in the semiconductor, LED, and storage device sectors, and increased consumer demand for items made of microelectronics. Thin films and semiconductor production both heavily rely on the Chemical Vapour Deposition (CVD) method. Other important market growth accelerators include the expanding semiconductor industry, rising semiconductor equipment investment, and advancements in semiconductor equipment.

Chemical vapour deposition is commonly used in the production of solar cells. As solar module prices fall in the future years, it is projected that the market for solar panels will grow. The decrease is a result of increased material efficiency, production optimisation, and economies of scale. They react or deteriorate when they cross or come into contact with a heated substrate, resulting in the deposition of a solid phase on the substrate.

Semiconductor CVD Equipment Market Growth Drivers:

- Demand for Consumer Electronics and Microelectronics Will Rise, Fueling the Market

The market for chemical vapour deposition might be boosted by semiconductor device makers increasing their manufacturing capacity in response to the demand for semiconductor ICs. (Memory Manufacturers are not included). A conventional IDM manufactures, designs, and owns its line of branded chips. An increase in consumer expenditure on electronics is driving up demand for semiconductors and microelectronics. The market for chemical vapour deposition is likely to increase as a result of the increasing demand for semiconductor fabrication throughout the forecast period.

- Various initiatives by the government to fuel the market for semiconductor CVD equipment.

Advancements in the microelectronics sector are being actively watched by governments and industry stakeholders because they can both stifle and expand the Internet of Things market. The government hosted a meeting in September 2021 with 50 leaders from the European and global semiconductor sectors to entice them to invest in Germany by providing a financial incentive. To enhance market penetration, businesses in the sector are concentrating on mergers and acquisitions, joint ventures, new launches, and regional growth. For example, in July 2022, ASM International NV introduced a new 300 mm vertical batch for LPCVD and ALD. The new system will offer cutting-edge support for applications involving memory and logic/foundry.

Semiconductor CVD Equipment Market Geographical Outlook:

- Asia Pacific is projected to be the prominent market shareholder in the semiconductor CVD equipment market and is anticipated to continue throughout the forecast period.

With its diverse production facilities, the Asia Pacific area has great potential for the development of consumer electronics and semiconductor-related goods. In the next years, it is anticipated that the specific region will have the greatest market share in the market for semiconductor CVD equipment.

The expansion of the regional market is being driven by the development of the electronics and semiconductor industries, particularly in China. The increase in industrialization and the number of end-user industries and businesses in developing nations like China and India offered vast untapped potential. The area is expected to increase significantly throughout the projected period as a result of the mere presence of expanding economies and the expansion of the electronics sector.

Semiconductor CVD Equipment Market Key Developments:

- November 2025: Veeco Instruments received an order for its Propel®300 MOCVD System from a major GaN-on-Si power-semiconductor IDM for 300?mm GaN epitaxy.

- October 2025: Veeco launched the Lumina+ MOCVD System and secured a multi-tool order for high-volume compound-semiconductor production, strengthening its MOCVD tool footprint.

- October 2025: AIXTRON SE joined a new 300 mm GaN Power Electronics Program (with imec) with its Hyperion 300 mm GaN MOCVD System, a key step toward wide-bandgap GaN device manufacturing at 300 mm scale.

- February 2025: Lam Research unveiled its ALTUS® Halo ALD system, the industry’s first atomic-layer deposition tool for molybdenum metallization, enabling low-resistivity, void-free metal films for advanced logic and memory devices.

List of Top Semiconductor CVD Equipment Companies:

- Aixtron SE

- ASM International

- CVD Equipment Corporation

- Oxford Instruments PLC

- Lam Research Corporation

Semiconductor CVD Equipment Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 5.683 billion |

| Total Market Size in 2031 | USD 8.179 billion |

| Growth Rate | 7.55% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Application, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Semiconductor CVD Equipment Market Segmentation:

- SEMICONDUCTOR CVD EQUIPMENT MARKET BY TYPE

- Plasma Enhanced Chemical Vapour Deposition

- Metal Organic Chemical Vapour Deposition

- Atmospheric Pressure Chemical Vapour Deposition

- Low-Pressure Chemical Vapour Deposition

- Others

- SEMICONDUCTOR CVD EQUIPMENT MARKET BY APPLICATION

- Wafer Foundries

- Memory Manufacturers

- Integrated Device Manufacturers

- SEMICONDUCTOR CVD EQUIPMENT MARKET BY GEOGRAPHY

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Thailand

- Others

- North America

Our Best-Performing Industry Reports:

Market Segmentation

By Type

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. SEMICONDUCTOR CVD EQUIPMENT MARKET BY TYPE

5.1. Introduction

5.2. Plasma Enhanced Chemical Vapour Deposition

5.3. Metal Organic Chemical Vapour Deposition

5.4. Atmospheric Pressure Chemical Vapour Deposition

5.5. Low-Pressure Chemical Vapour Deposition

5.6. Others

6. SEMICONDUCTOR CVD EQUIPMENT MARKET BY APPLICATION

6.1. Introduction

6.2. Wafer Foundries

6.3. Memory Manufacturers

6.4. Integrated Device Manufacturers

7. SEMICONDUCTOR CVD EQUIPMENT MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. USA

7.2.2. Canada

7.2.3. Mexico

7.3. South America

7.3.1. Brazil

7.3.2. Argentina

7.3.3. Others

7.4. Europe

7.4.1. Germany

7.4.2. France

7.4.3. United Kingdom

7.4.4. Spain

7.4.5. Others

7.5. Middle East and Africa

7.5.1. Saudi Arabia

7.5.2. UAE

7.5.3. Others

7.6. Asia Pacific

7.6.1. China

7.6.2. India

7.6.3. Japan

7.6.4. South Korea

7.6.5. Indonesia

7.6.6. Thailand

7.6.7. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Aixtron SE

9.2. ASM International

9.3. CVD Equipment Corporation

9.4. Oxford Instruments PLC

9.5. Lam Research Corporation

9.6. Ulvac Inc

9.7. Veeco Instruments Inc

9.8. Vapour Technologies Inc

9.9. Eugene Technology

9.10. Wonik IPS

10. APPENDIX

10.1. Currency

10.2. Assumptions

10.3. Base and Forecast Years Timeline

10.4. Key benefits for the stakeholders

10.5. Research Methodology

10.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations