Report Overview

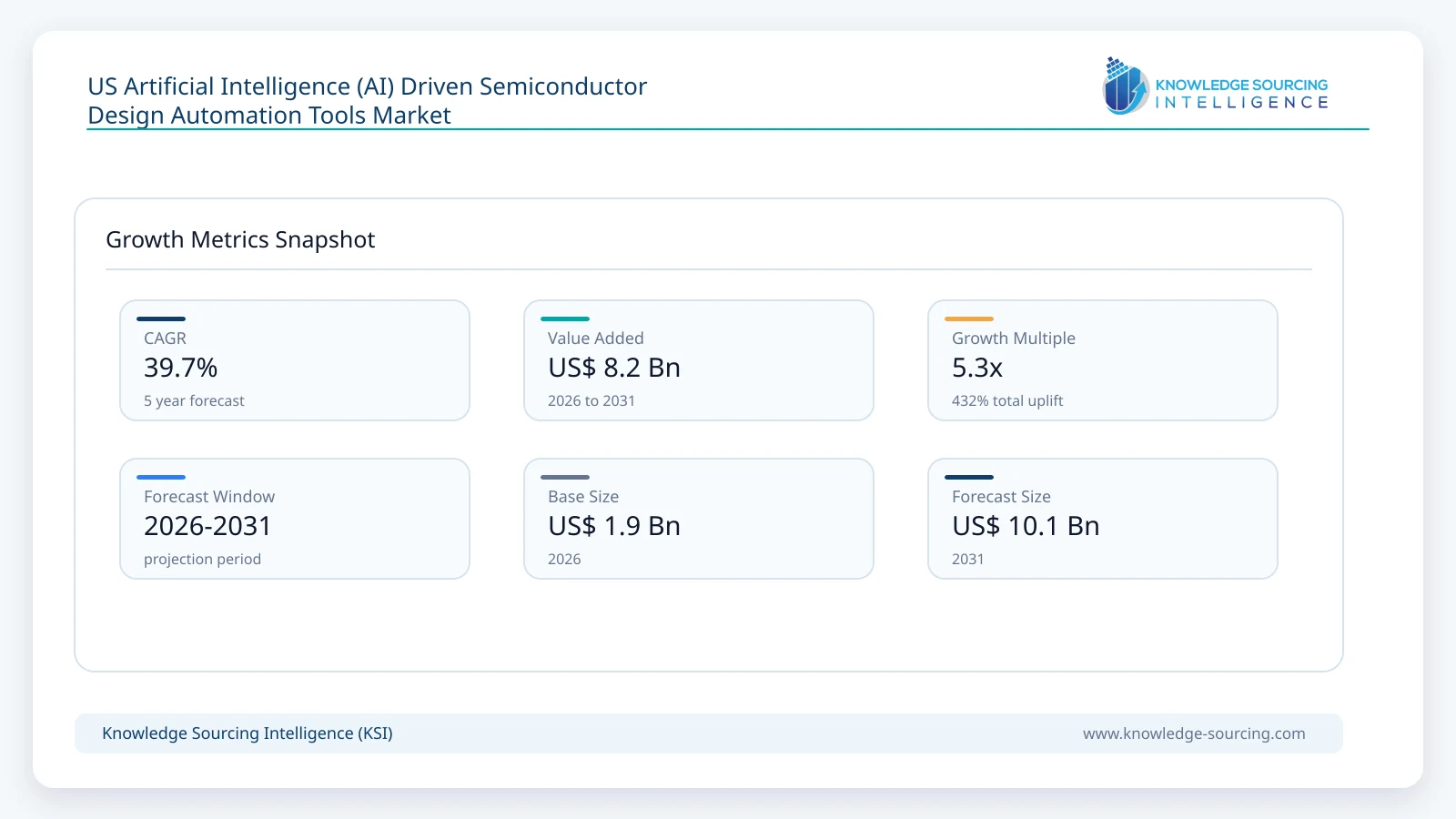

The US AI-Driven Semiconductor Design Automation Tools Market is forecast to grow at a CAGR of 39.7%, reaching USD 10.1 billion in 2031 from USD 1.9 billion in 2026.

Highlights:

- 1Rising semiconductor design complexity across advanced process nodes remains the primary catalyst for AI-enabled automation adoption.

- 2Verification and Simulation Tools represent one of the most commercially important areas because verification consumes a substantial share of semiconductor engineering resources.

- 3North America benefits from strong semiconductor research funding, advanced design ecosystems, and expanding domestic manufacturing investments.

- 4Generative AI and large language models are being integrated into engineering workflows to automate scripting, documentation, debugging, and design assistance.

- 5Government semiconductor manufacturing incentives and national technology policies encourage greater investment in domestic chip design capabilities.

- 6Competition increasingly depends on AI model performance, workflow integration, cloud deployment flexibility, and ecosystem partnerships rather than software functionality alone.

The US Artificial Intelligence (AI) Driven Semiconductor Design Automation Tools market comprises software platforms and intelligent design engines that apply artificial intelligence across integrated circuit (IC) development workflows, including logic synthesis, physical implementation, verification, simulation, testing, and design optimization. These tools assist semiconductor companies in reducing design complexity, improving engineering productivity, accelerating tape-outs, and achieving power, performance, and area (PPA) targets. They are increasingly embedded within electronic design automation (EDA) environments used for advanced-node semiconductor development.

Demand for AI-enabled design automation tools is being shaped by the rising complexity of semiconductor architectures and the growing number of chips designed for artificial intelligence computing, automotive electronics, telecommunications infrastructure, aerospace systems, industrial automation, and defense applications. Advanced process nodes require significantly more verification cycles, larger design datasets, and tighter manufacturing constraints than previous generations. AI-assisted workflows enable engineering teams to identify design bottlenecks earlier, optimize placement and routing decisions, and automate repetitive engineering tasks that traditionally required substantial manual intervention.

Procurement decisions are largely driven by integrated device manufacturers (IDMs), fabless semiconductor firms, semiconductor foundries, and specialized design service providers. Buyers increasingly evaluate AI-driven design platforms based on measurable improvements in design closure, verification efficiency, engineering productivity, interoperability with existing EDA environments, cloud scalability, cybersecurity capabilities, and support for advanced manufacturing nodes. Organizations also assess vendor roadmaps for generative AI capabilities, explainable AI functions, and compatibility with heterogeneous computing architectures.

The competitive structure remains concentrated around established EDA vendors while newer AI-focused software developers introduce specialized solutions for verification automation, chip reliability monitoring, and design optimization. Collaboration between EDA providers, semiconductor manufacturers, cloud infrastructure providers, and AI hardware developers continues to shape technology development. As semiconductor product cycles shorten and chip complexity increases, AI-assisted automation has become an operational requirement rather than an experimental capability for many advanced semiconductor design organizations.

Market Drivers

Rising design complexity across advanced semiconductor nodes

Modern semiconductor products integrate billions of transistors while supporting AI acceleration, high-speed connectivity, advanced memory architectures, and heterogeneous computing. Engineering teams face greater challenges in timing closure, signal integrity, thermal optimization, and verification coverage. AI-driven design automation tools analyze extensive design datasets to recommend optimized implementation strategies and reduce engineering iterations.

Commercially, this allows semiconductor companies to shorten development cycles and improve resource utilization. Vendors continue investing in AI-assisted optimization algorithms that address increasingly sophisticated design challenges for advanced-node manufacturing.

Expansion of domestic semiconductor manufacturing initiatives

Federal semiconductor manufacturing incentives have encouraged investments in fabrication facilities, advanced packaging, research centers, and semiconductor workforce development throughout the United States. Increased domestic production capacity also expands demand for sophisticated design tools capable of supporting next-generation chip development.

Chip designers increasingly procure software platforms that integrate AI throughout front-end and back-end design processes, helping organizations align product development schedules with expanding manufacturing capacity.

Growing adoption of cloud-based semiconductor design environments

Semiconductor verification workloads require considerable computing resources. Cloud infrastructure enables engineering organizations to scale simulation capacity without maintaining equivalent on-premise hardware investments.

AI-driven cloud platforms further improve computational efficiency by dynamically allocating computing resources, optimizing simulation schedules, and prioritizing engineering workloads. Procurement increasingly favors solutions that combine cloud scalability with enterprise security and regulatory compliance.

Increasing demand for AI processors across multiple industries

The expansion of data centers, autonomous vehicles, edge computing, telecommunications infrastructure, healthcare equipment, and defense electronics has accelerated demand for specialized semiconductor devices.

These application-specific requirements create more customized chip architectures, increasing the need for intelligent design automation capable of handling unique design constraints. Software vendors respond by expanding AI capabilities across architecture exploration, verification, and physical implementation workflows.

Market Restraints and Challenges

High implementation costs for enterprise-scale deployment

Comprehensive AI-driven EDA environments require software licensing, computing infrastructure, AI model training, workflow integration, and employee training. Smaller semiconductor firms may find enterprise deployments financially challenging, particularly when expected productivity gains require organizational process changes.

Vendors increasingly offer modular licensing models and cloud subscriptions to reduce initial investment requirements.

Limited availability of experienced semiconductor AI specialists

Successful deployment depends not only on software but also on engineers capable of interpreting AI-generated recommendations and integrating them into established design methodologies.

Competition for semiconductor design talent remains intense, increasing recruitment costs and extending implementation timelines. Organizations therefore invest in workforce development alongside software procurement.

Data confidentiality and intellectual property protection

Semiconductor design files represent highly valuable intellectual property. Companies remain cautious regarding cloud-based AI systems handling proprietary design information, particularly when external AI models are involved.

Software suppliers address these concerns through confidential computing technologies, secure deployment options, access controls, encryption, and enterprise governance frameworks.

Integration with existing design ecosystems

Large semiconductor organizations often operate mature EDA environments accumulated over many years. Replacing established workflows introduces operational risk and potential productivity disruptions.

Consequently, buyers prioritize AI platforms that integrate with existing verification, simulation, synthesis, and physical implementation tools instead of requiring complete workflow replacement.

Major Segment Analysis

Verification and Simulation Tools

Verification and Simulation Tools represent one of the most commercially influential segments because verification activities account for a substantial proportion of semiconductor development time and engineering expenditure. As integrated circuits become increasingly complex, identifying functional defects before fabrication becomes both technically demanding and financially critical.

Engineering organizations seek AI-assisted verification platforms capable of automatically generating test cases, identifying coverage gaps, prioritizing simulation workloads, and predicting potential design failures. Machine learning algorithms improve regression testing efficiency while reducing unnecessary computational workloads.

Competitive differentiation within this segment depends on verification accuracy, scalability across large designs, compatibility with multiple semiconductor architectures, and integration with established EDA workflows. Vendors also compete by incorporating generative AI assistants that simplify scripting, debug analysis, and documentation generation for engineering teams.

Commercially, improvements in verification efficiency directly reduce project schedules and lower the risk of expensive silicon re-spins. These measurable productivity gains support continued investment despite relatively high software acquisition costs.

Competitive Landscape

Competition combines established electronic design automation providers with specialized AI software developers addressing specific stages of semiconductor design. Vendors compete by improving AI algorithm accuracy, expanding automation across design workflows, supporting advanced manufacturing nodes, and integrating cloud-native deployment capabilities.

Partnerships with semiconductor manufacturers, foundries, cloud computing providers, and processor developers have become central to product development strategies. Suppliers also invest heavily in generative AI integration, reinforcement learning optimization, and explainable AI capabilities to improve engineering confidence and workflow transparency.

Competitive positioning increasingly depends on measurable productivity improvements, interoperability with existing semiconductor design environments, enterprise cybersecurity capabilities, and support for collaborative engineering across geographically distributed design teams.

Major companies operating in the market include Synopsys, Inc., Cadence Design Systems, Inc., Siemens EDA (Siemens AG), Ansys, Inc., Arm Limited, Silvaco Group, Inc., Keysight Technologies, Inc., proteanTecs Ltd., ChipAgents, and NVIDIA Corporation.

Recent Developments

March 2026: Synopsys expanded generative AI capabilities across its electronic design automation portfolio to automate engineering workflows and improve design productivity. Commercial relevance: supports faster semiconductor development and broader AI integration across customer environments.

September 2025: Cadence Design Systems introduced additional AI-driven enhancements for digital implementation and verification solutions supporting advanced semiconductor node development. Commercial relevance: improves engineering efficiency and strengthens AI-enabled design automation capabilities.

Regulatory and Policy Environment

Government semiconductor policy plays an important role in shaping investment decisions across the United States. Federal initiatives supporting domestic semiconductor manufacturing, advanced packaging, research infrastructure, and workforce development encourage greater investment in semiconductor design capabilities.

Compliance requirements related to export controls, cybersecurity, trusted semiconductor supply chains, and intellectual property protection influence software procurement decisions. Organizations developing chips for defense and critical infrastructure applications frequently require secure design environments that satisfy government security standards.

Industry standards for semiconductor design interoperability, verification methodologies, functional safety, and manufacturing compatibility also affect software development priorities. Vendors continue aligning AI-enabled capabilities with established engineering standards to support enterprise adoption without disrupting validated design processes.

Outlook and Strategic Implications

Over the forecast period, AI will become progressively integrated throughout semiconductor engineering rather than functioning as a standalone software feature. Procurement strategies will increasingly evaluate measurable engineering productivity improvements, automation accuracy, cloud deployment flexibility, and secure enterprise integration instead of isolated AI functionality.

Investment priorities are expected to concentrate on generative AI engineering assistants, reinforcement learning optimization, intelligent verification automation, cloud-native simulation platforms, and AI-supported design exploration. Buyers will continue demanding transparent AI recommendations that engineers can validate before implementation.

Competition is expected to extend beyond software functionality toward broader ecosystem integration involving semiconductor manufacturers, cloud infrastructure providers, AI hardware developers, and research organizations. Companies capable of delivering interoperable, secure, and scalable AI-assisted engineering environments are likely to strengthen their competitive position.

Despite challenges associated with implementation costs, workforce availability, and intellectual property protection, AI-driven semiconductor design automation is expected to become an essential capability for organizations seeking shorter development cycles, higher design quality, and greater engineering efficiency in increasingly sophisticated semiconductor programs.

US AI-Driven Semiconductor Design Automation Tools Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 1.9 billion |

| Total Market Size in 2031 | USD 10.1 billion |

| Forecast Unit | Billion |

| Growth Rate | 39.7% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Tool Type, Technology, Deployment Mode, Application, End User |

| Companies |

|

Market Segmentation

By Tool Type

By Technology

By Deployment Mode

By Application

By End User

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter's Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. US ARTIFICIAL INTELLIGENCE (AI)-DRIVEN SEMICONDUCTOR DESIGN AUTOMATION TOOLS MARKET BY TOOL TYPE

5.1. Introduction

5.2. Front-End Design Tools

5.3. Back-End (Physical Design) Tools

5.4. Verification and Simulation Tools

5.5. Testing and Validation Tools

6. US ARTIFICIAL INTELLIGENCE (AI)-DRIVEN SEMICONDUCTOR DESIGN AUTOMATION TOOLS MARKET BY TECHNOLOGY

6.1. Introduction

6.2. Machine Learning (ML)

6.3. Deep Learning

6.4. Reinforcement Learning

6.5. Generative AI and Large Language Models (LLMs)

7. US ARTIFICIAL INTELLIGENCE (AI)-DRIVEN SEMICONDUCTOR DESIGN AUTOMATION TOOLS MARKET BY DEPLOYMENT MODE

7.1. Introduction

7.2. On-Premise

7.3. Cloud-Based

8. US ARTIFICIAL INTELLIGENCE (AI)-DRIVEN SEMICONDUCTOR DESIGN AUTOMATION TOOLS MARKET BY APPLICATION

8.1. Introduction

8.2. Application-Specific Integrated Circuit (ASIC) Design

8.3. System-on-Chip (SoC) Design

8.4. Field-Programmable Gate Array (FPGA) Design

8.5. Analog and Mixed-Signal IC Design

9. US ARTIFICIAL INTELLIGENCE (AI)-DRIVEN SEMICONDUCTOR DESIGN AUTOMATION TOOLS MARKET BY END USER

9.1. Introduction

9.2. Integrated Device Manufacturers (IDMs)

9.3. Fabless Semiconductor Companies

9.4. Semiconductor Foundries

9.5. Semiconductor Design Service Providers

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. Synopsys, Inc.

11.2. Cadence Design Systems, Inc.

11.3. Siemens EDA (Siemens AG)

11.4. Ansys, Inc.

11.5. Arm Limited

11.6. Silvaco Group, Inc.

11.7. Keysight Technologies, Inc.

11.8. proteanTecs Ltd.

11.9. ChipAgents

11.10. NVIDIA Corporation

12. APPENDIX

12.1. Currency

12.2. Assumptions

12.3. Base and Forecast Years Timeline

12.4. Key Benefits for Stakeholders

12.5. Research Methodology

12.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations