Report Overview

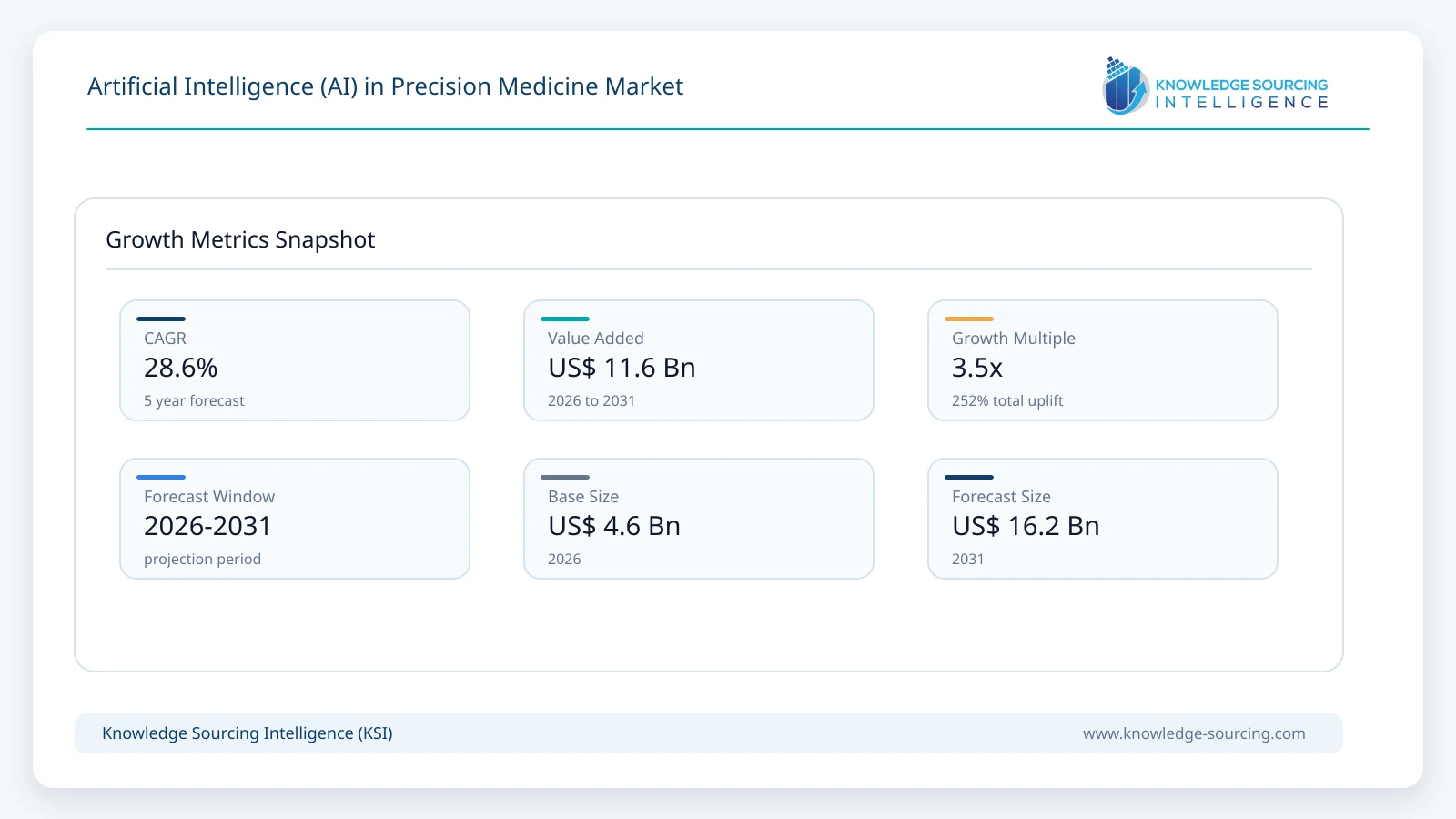

The AI in Precision Medicine Market is forecast to grow at a CAGR of 28.6%, reaching USD 16.2 billion in 2031 from USD 4.6 billion in 2026.

Highlights:

- 1Growing adoption of genomic sequencing and precision oncology is creating sustained demand for AI-enabled clinical interpretation platforms.

- 2Machine learning remains the leading technology segment due to its broad application across drug discovery, genomic analysis, and clinical decision support.

- 3North America represents the largest commercial opportunity owing to mature healthcare infrastructure, advanced genomics research, and strong private-sector investment.

- 4Integration of multimodal datasets, including genomic, imaging, pathology, and electronic health records, is becoming a major technology trend.

- 5Expanding regulatory guidance for AI-enabled medical software is improving commercialization pathways while increasing compliance requirements.

- 6Competition is increasingly centered on proprietary clinical datasets, validated algorithms, cloud infrastructure, and strategic healthcare partnerships.

Artificial Intelligence (AI) in Precision Medicine refers to the application of computational models that analyze genomic, clinical, imaging, molecular, and real-world patient data to support individualized disease prevention, diagnosis, treatment selection, and therapeutic development. The market extends across software platforms, cloud-based analytics, clinical decision support systems, genomic interpretation tools, and AI-enabled research applications used by pharmaceutical companies, biotechnology firms, hospitals, diagnostic laboratories, and academic institutions.

Commercial demand is primarily driven by the growing complexity of biological datasets and the need to improve decision-making throughout the healthcare value chain. Advances in next-generation sequencing, digital pathology, molecular diagnostics, and electronic health records have created large volumes of structured and unstructured data that exceed conventional analytical capabilities. AI technologies enable organizations to identify clinically relevant biomarkers, stratify patient populations, optimize clinical trial recruitment, and accelerate drug development while improving treatment selection for physicians.

Procurement priorities have shifted beyond algorithm accuracy toward platform interoperability, regulatory compliance, cybersecurity, explainable AI capabilities, and integration with existing laboratory information systems and hospital workflows. Buyers increasingly seek platforms capable of combining multimodal datasets rather than isolated analytical tools. Healthcare providers evaluate AI solutions based on clinical validation, workflow efficiency, reimbursement prospects, and compatibility with electronic medical record systems, while pharmaceutical companies prioritize scalable computing infrastructure capable of supporting biomarker discovery and precision clinical development.

The industry's commercial structure includes multinational technology companies, cloud computing providers, genomic diagnostics firms, AI software developers, and specialized precision medicine platform providers. Software generates the largest share of industry revenue because AI models can be deployed across existing healthcare infrastructure without extensive replacement of medical equipment. However, complementary investments in cloud computing capacity, secure data storage, sequencing technologies, and clinical validation services remain essential for successful implementation.

Investment activity continues to strengthen as governments expand national genomic medicine programs and pharmaceutical companies increase spending on AI-assisted research. Strategic collaborations between healthcare institutions, biotechnology firms, and cloud service providers are expanding access to high-quality clinical datasets required for model development. At the same time, increasing regulatory attention toward AI transparency, patient privacy, and clinical validation is influencing purchasing decisions across both developed and emerging healthcare systems.

Market Drivers

Expansion of Precision Oncology Programs

Cancer treatment continues to shift toward biomarker-guided therapies that require interpretation of increasingly complex molecular information. Hospitals, cancer centers, and pharmaceutical developers rely on AI to identify actionable genetic mutations, predict treatment response, and support personalized therapeutic decisions. This demand encourages technology suppliers to develop validated oncology-focused AI platforms with stronger clinical evidence, expanding commercial opportunities across diagnostics and pharmaceutical research.

Growth in Genomic Sequencing Volumes

National genome initiatives, declining sequencing costs, and broader clinical adoption of genomic testing have substantially increased the volume of genetic data requiring interpretation. Manual analysis cannot efficiently process this information within clinical timeframes. AI enables automated variant classification, disease association analysis, and clinical reporting, making genomic laboratories important purchasers of advanced analytical software. Vendors compete by improving interpretation accuracy, processing speed, and integration with laboratory workflows.

Rising Pharmaceutical Investment in AI-Enabled Drug Discovery

Drug development remains expensive and time intensive, increasing demand for technologies capable of improving research productivity. Pharmaceutical and biotechnology companies increasingly apply AI to identify therapeutic targets, discover biomarkers, optimize patient stratification, and predict clinical outcomes. These capabilities reduce unnecessary experimental activity while supporting precision medicine strategies that improve clinical trial success rates and accelerate commercialization.

Expansion of Real-World Health Data Utilization

Healthcare organizations are generating growing volumes of electronic medical records, imaging studies, pathology reports, and wearable device data. AI platforms capable of integrating these diverse information sources provide clinicians with more comprehensive patient assessments and generate valuable evidence for pharmaceutical research. This trend supports recurring software revenues and encourages long-term enterprise licensing agreements.

Market Restraints and Challenges

Limited Availability of High-Quality Clinical Data

AI performance depends heavily on diverse, accurately annotated datasets. Many healthcare organizations maintain fragmented databases with inconsistent coding standards and incomplete patient records. Data quality limitations reduce model accuracy and delay clinical deployment. Suppliers increasingly address this challenge through standardized data frameworks, collaborative research partnerships, and federated learning approaches that preserve patient privacy.

Regulatory Complexity for Clinical AI Applications

AI-based medical software must satisfy evolving regulatory expectations related to safety, transparency, validation, and post-market monitoring. Continuous learning algorithms create additional compliance challenges because model performance may change after deployment. These requirements increase development costs, extend commercialization timelines, and require substantial investment in quality management systems and clinical evidence generation.

Integration Challenges Within Healthcare Infrastructure

Hospitals frequently operate legacy information systems that complicate AI deployment across clinical workflows. Integration with laboratory systems, imaging platforms, genomic databases, and electronic health records often requires customized implementation services. Longer deployment periods increase procurement costs and may delay return on investment for healthcare providers.

Shortage of Specialized Workforce

Successful implementation requires professionals with expertise in bioinformatics, clinical genomics, artificial intelligence, regulatory compliance, and healthcare informatics. Many healthcare organizations face shortages of multidisciplinary talent capable of validating and operating advanced AI platforms. Vendors increasingly provide implementation support, clinician education, and managed services to reduce adoption barriers.

Major Segment Analysis

Machine Learning represents the most commercially important technology segment because it supports a broad range of precision medicine applications across research, diagnostics, and clinical practice. Unlike highly specialized analytical techniques, machine learning algorithms can process structured clinical records, genomic datasets, laboratory results, and imaging information simultaneously, enabling healthcare organizations to generate clinically meaningful insights from heterogeneous data sources.

Demand is strongest among pharmaceutical companies, genomic laboratories, and tertiary healthcare providers seeking scalable analytical platforms capable of supporting routine clinical operations as well as research programs. Buyers prioritize validated predictive performance, explainable model outputs, interoperability with existing systems, and continuous software updates supported by regulatory documentation.

Competition within this segment increasingly depends on access to proprietary datasets, algorithm validation across diverse patient populations, cloud computing efficiency, and integration capabilities. Companies capable of demonstrating measurable improvements in diagnostic accuracy, biomarker discovery, and treatment selection gain stronger commercial positioning. As reimbursement models gradually recognize AI-assisted clinical services, machine learning platforms are expected to generate recurring software subscription and enterprise licensing revenues, reinforcing their importance within the overall market.

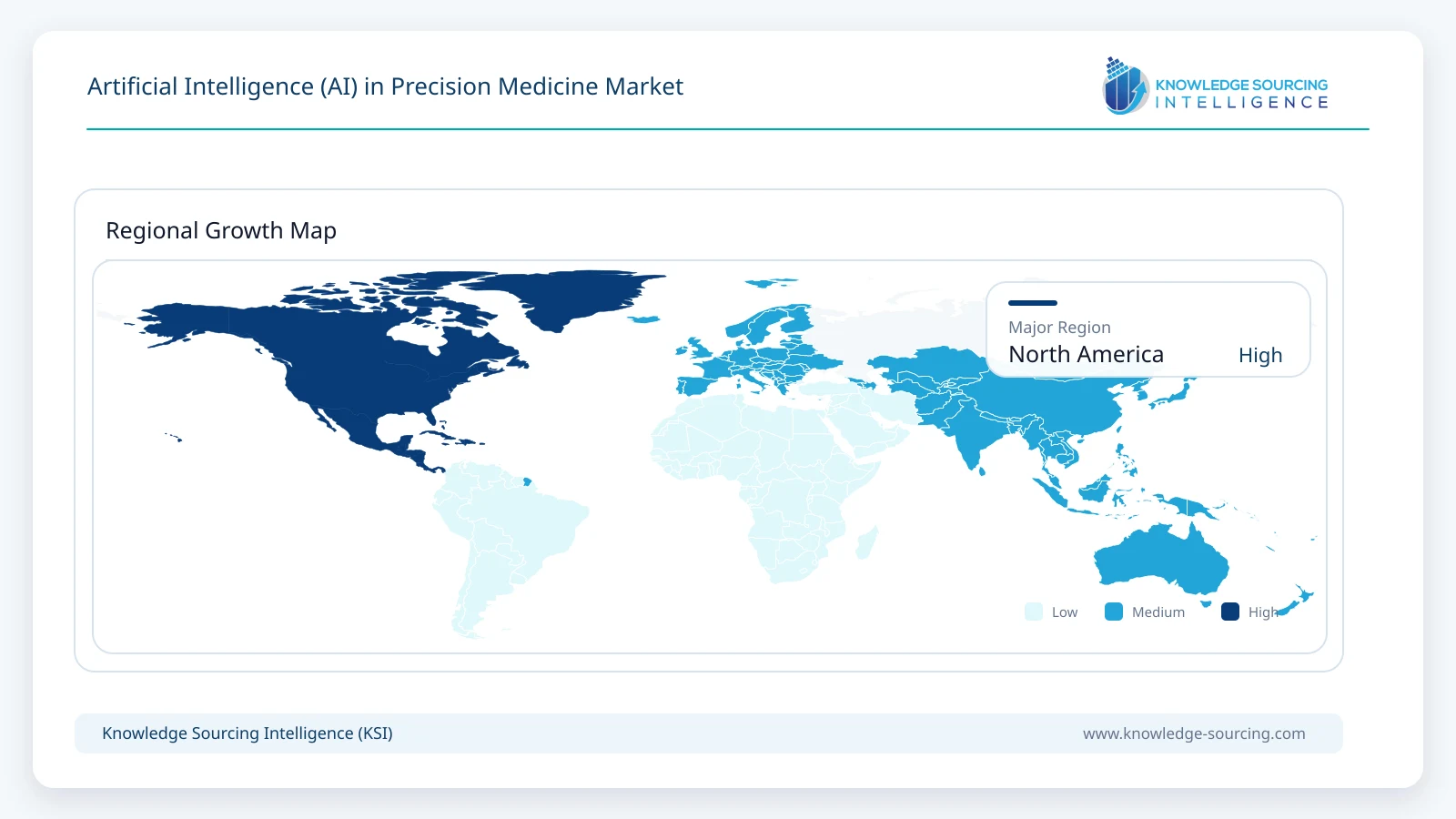

Regional Analysis

North America

North America maintains the largest market share due to substantial investment in genomic medicine, established digital healthcare infrastructure, and active participation from pharmaceutical companies and academic medical centers. The United States benefits from extensive precision oncology programs, advanced sequencing capabilities, and favorable private investment in AI-enabled healthcare technologies. Regulatory guidance for AI-based medical devices continues to evolve, encouraging commercialization while maintaining patient safety requirements.

Europe

European demand is supported by coordinated research initiatives, expanding genomic medicine programs, and increasing adoption of digital health technologies. National healthcare systems emphasize evidence-based implementation and data protection, encouraging suppliers to develop compliant AI solutions that satisfy privacy regulations. Collaborative research across universities, hospitals, and biotechnology companies supports continued innovation despite differences in reimbursement policies among member states.

Asia Pacific

Asia Pacific represents the fastest-expanding regional opportunity due to increasing healthcare expenditure, expanding biotechnology industries, and government-supported genomic research initiatives. China, Japan, South Korea, India, and Taiwan continue investing in precision healthcare infrastructure, sequencing capacity, and AI research. Growing patient populations and expanding hospital modernization programs create favorable conditions for broader commercial adoption, although infrastructure disparities remain across several developing economies.

Middle East & Africa

Healthcare modernization programs, national digital health strategies, and growing investment in specialized medical centers support gradual adoption across selected Middle Eastern countries. Saudi Arabia and the UAE continue expanding precision medicine capabilities through public-sector investment and international partnerships. Adoption across much of Africa remains constrained by limited sequencing infrastructure, workforce shortages, and healthcare funding limitations.

Competitive Landscape

Competition is characterized by a combination of global technology providers, cloud infrastructure companies, genomic diagnostics specialists, and precision medicine software developers. Companies including IBM Corporation, Google LLC (Alphabet Inc.), Microsoft Corporation, Amazon Web Services, NVIDIA Corporation, Tempus AI, Flatiron Health, Foundation Medicine, Illumina, and SOPHiA GENETICS compete through integrated technology ecosystems rather than standalone AI algorithms.

Competitive differentiation increasingly depends on proprietary clinical datasets, validated genomic interpretation capabilities, cloud computing performance, cybersecurity, regulatory readiness, and interoperability with healthcare information systems. Strategic partnerships between pharmaceutical companies, hospitals, research institutions, and cloud providers remain essential for acquiring high-quality training data and expanding commercial deployment. Geographic expansion increasingly targets healthcare systems investing in national genomics initiatives and digital health infrastructure.

Recent Developments

May 2026: Tempus AI launched the PRECISION Challenge, a national research initiative providing scientists access to its AI foundation models, multimodal datasets, funding, and computing infrastructure to accelerate precision medicine and oncology innovations.

February 2026: Merck and Mayo Clinic entered a research and development collaboration to apply artificial intelligence, multimodal clinical data, and genomics for AI-enabled drug discovery, disease understanding, and precision medicine research.

January 2026: Natera announced a collaboration with NVIDIA to develop multimodal AI foundation models for precision medicine, combining Natera's longitudinal genomic datasets with NVIDIA's AI computing infrastructure to advance personalized diagnostics and therapeutic decision-making.

Regulatory and Policy Environment

Regulatory oversight continues to evolve as AI becomes integrated into clinical decision-making. In the United States, the FDA regulates AI-enabled software intended for medical purposes under Software as a Medical Device (SaMD) frameworks while expanding guidance for adaptive machine learning technologies. European implementation is influenced by the Medical Device Regulation (MDR), In Vitro Diagnostic Regulation (IVDR), and the EU AI Act, which establish risk-based requirements for healthcare AI applications.

Data governance remains equally important. Compliance with HIPAA in the United States and GDPR across Europe significantly influences product architecture, cloud deployment strategies, and data-sharing agreements. National genomic medicine programs in several countries continue funding sequencing infrastructure and precision medicine research, creating additional opportunities for AI platform adoption while requiring strict adherence to cybersecurity, patient consent, and data governance standards.

Outlook and Strategic Implications

Commercial demand for AI in precision medicine is expected to remain closely linked to expansion in genomic testing, precision oncology, molecular diagnostics, and pharmaceutical research investment. Buyers are expected to prioritize enterprise platforms capable of integrating genomic, imaging, pathology, and clinical information within secure and interoperable environments rather than purchasing isolated analytical applications.

Technology suppliers will continue directing investment toward explainable AI, multimodal analytics, federated learning, and automated clinical reporting that satisfy evolving regulatory expectations. Procurement decisions will increasingly emphasize demonstrated clinical utility, reimbursement potential, cybersecurity, implementation support, and compatibility with existing healthcare infrastructure.

Competitive positioning will depend less on algorithm development alone and more on access to proprietary clinical datasets, validated healthcare partnerships, and scalable cloud infrastructure. Organizations capable of combining scientific credibility with regulatory compliance and operational integration are likely to strengthen their commercial position over the next five years, while participants unable to demonstrate measurable clinical and economic value may encounter slower adoption despite technological capability.

AI in Precision Medicine Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 4.6 billion |

| Total Market Size in 2031 | USD 16.2 billion |

| Forecast Unit | Billion |

| Growth Rate | 28.6% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Technology, Application, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Technology

- Machine Learning

- Deep Learning

- Natural Language Processing (NLP)

- Big Data Analytics

- Computer Vision

- Others

By Application

- Drug Discovery and Development

- Clinical Decision Support

- Oncology

- Genetic Testing

- Rare Diseases

- Infectious Diseases

- Others

By End-User

- Pharmaceutical and Biotechnology Companies

- Research Institutes and Academic Centers

- Healthcare Providers

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- Japan

- China

- India

- South Korea

- Indonesia

- Taiwan

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

2. RESEARCH METHODOLOGY

2.1. Research Data

2.2. Sources

2.3. Research Design

3. EXECUTIVE SUMMARY

3.1. Research Highlights

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter's Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

5. AI IN PRECISION MEDICINE MARKET BY TECHNOLOGY

5.1. Introduction

5.2. Machine Learning

5.3. Deep Learning

5.4. Natural Language Processing (NLP)

5.5. Big Data Analytics

5.6. Computer Vision

5.7. Others

6. AI IN PRECISION MEDICINE MARKET BY APPLICATION

6.1. Introduction

6.2. Drug Discovery and Development

6.3. Clinical Decision Support

6.4. Oncology

6.5. Genetic Testing

6.6. Rare Diseases

6.7. Infectious Diseases

6.8. Others

7. AI IN PRECISION MEDICINE MARKET BY END-USER

7.1. Introduction

7.2. Pharmaceutical and Biotechnology Companies

7.3. Research Institutes and Academic Centers

7.4. Healthcare Providers

7.5. Others

8. AI IN PRECISION MEDICINE MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. United States

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Argentina

8.3.3. Others

8.4. Europe

8.4.1. United Kingdom

8.4.2. Germany

8.4.3. France

8.4.4. Italy

8.4.5. Spain

8.4.6. Others

8.5. Middle East and Africa

8.5.1. Saudi Arabia

8.5.2. UAE

8.5.3. Others

8.6. Asia Pacific

8.6.1. Japan

8.6.2. China

8.6.3. India

8.6.4. South Korea

8.6.5. Indonesia

8.6.6. Taiwan

8.6.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Emerging Players and Market Lucrativeness

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Vendor Competitiveness Matrix

10. COMPANY PROFILES

10.1. IBM Corporation

10.2. Google LLC (Alphabet Inc.)

10.3. Microsoft Corporation

10.4. Amazon Web Services, Inc.

10.5. NVIDIA Corporation

10.6. Tempus AI, Inc.

10.7. Flatiron Health, Inc. (Roche Holding AG)

10.8. Foundation Medicine, Inc. (Roche Holding AG)

10.9. Illumina, Inc.

10.10. SOPHiA GENETICS SA

Navigate

Trusted by the world's leading organizations