Report Overview

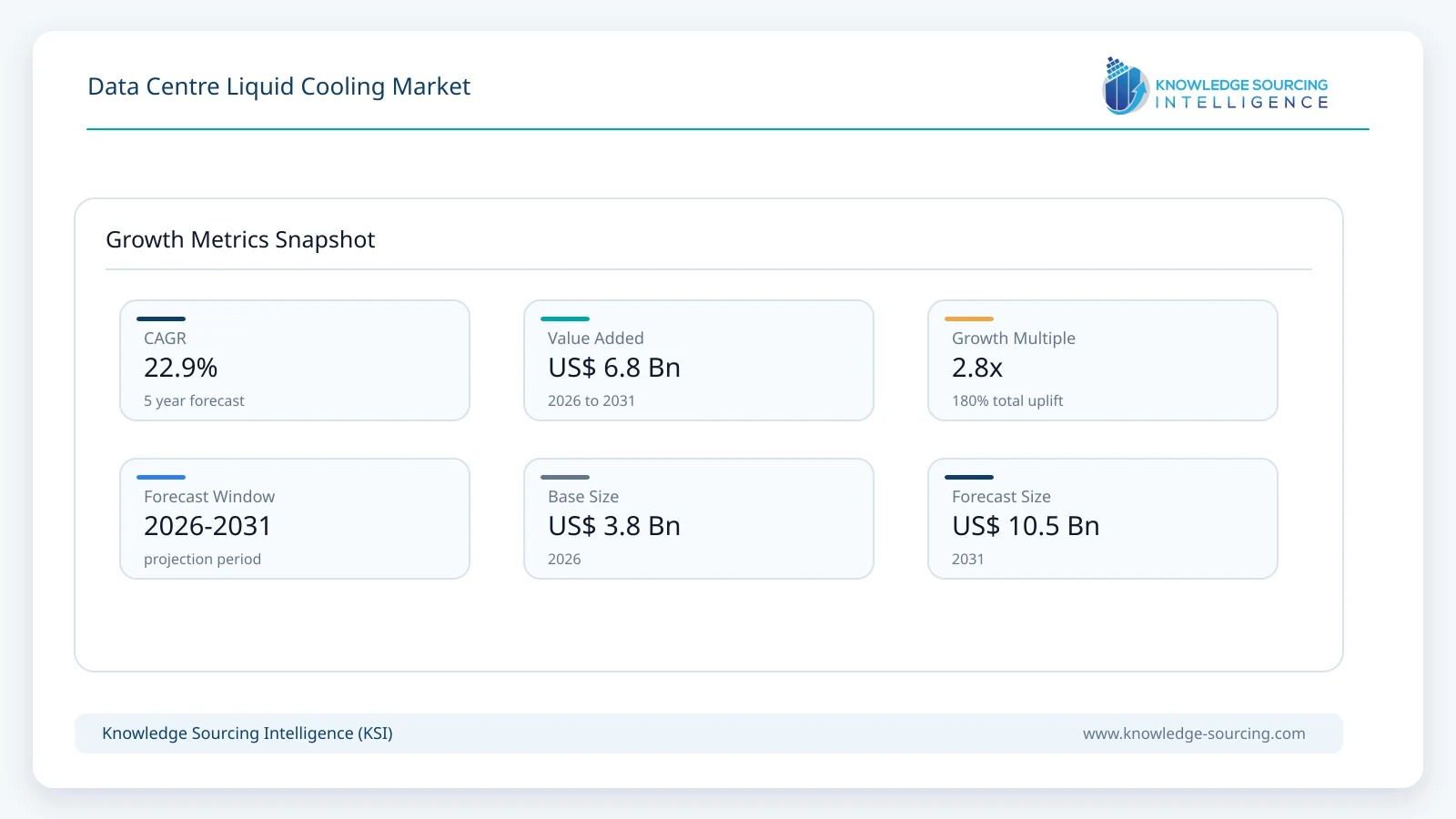

The Data Centre Liquid Cooling Market is expected to grow at a CAGR of 22.87% from USD 3.75 billion in 2026 to USD 10.50 billion by 2031.

Highlights:

- 1Growing deployment of AI servers and GPU clusters is accelerating investment in liquid cooling infrastructure.

- 2Cold plate coolingremains one of the most commercially adopted technologies because it integrates with existing server architectures while supporting higher rack densities.

- 3Asia Pacific continues to represent an important investment destination due to large-scale hyperscale data centre construction and semiconductor manufacturing expansion.

- 4Integration of intelligent thermal monitoring software is improving predictive maintenance and operational efficiency.

- 5Energy efficiency regulations and sustainability targets are encouraging operators to reduce cooling-related electricity consumption.

- 6Competition increasingly depends on engineering capability, system integration expertise, and lifecycle service offerings rather than hardware pricing alone.

The data centre liquid cooling market comprises hardware, software, and specialized services designed to remove heat from high-density computing infrastructure using liquid-based thermal management technologies. These solutions include immersion cooling, cold plate cooling, and hybrid liquid cooling systems that support servers, graphics processing units (GPUs), artificial intelligence (AI) accelerators, high-performance computing (HPC) clusters, and advanced storage platforms. Compared with conventional air cooling, liquid cooling offers higher heat transfer efficiency, enabling operators to accommodate rising rack power densities while reducing energy consumption associated with cooling infrastructure.

Commercial demand is being reshaped by the rapid deployment of AI training clusters, enterprise AI inference infrastructure, hyperscale cloud expansion, and scientific computing environments. Modern processors are generating thermal loads that exceed the practical limits of traditional air-cooling systems, particularly in facilities where rack densities are approaching or surpassing 50–100 kW. Data centre operators are therefore evaluating cooling technologies not only on acquisition cost but also on lifecycle operating expenses, cooling efficiency, water consumption, equipment reliability, and compatibility with future processor generations.

Procurement decisions increasingly involve collaboration between IT infrastructure teams, facilities managers, sustainability departments, and finance executives. Buyers seek cooling platforms that integrate with existing mechanical infrastructure while minimizing disruption during deployment. Compatibility with server manufacturers, modular installation capability, monitoring software, maintenance support, and long-term service agreements have become important purchasing criteria. Large cloud providers and colocation operators typically negotiate multi-year procurement contracts that combine hardware supply with engineering services and performance guarantees.

Demand is also supported by growing pressure to improve data centre energy efficiency. Governments and regulators continue to promote lower carbon emissions and better utilization of electricity resources. Since cooling systems account for a substantial share of overall facility power consumption, liquid cooling is becoming part of broader efficiency improvement programs. Operators are increasingly measuring investments against power usage effectiveness (PUE), operational resilience, and long-term infrastructure scalability rather than focusing solely on upfront capital expenditure.

The industry structure combines established electrical and thermal management suppliers with specialist liquid cooling technology developers. Competition extends beyond cooling hardware into software for thermal monitoring, predictive maintenance, intelligent coolant management, and integrated infrastructure management. Engineering services, installation expertise, and long-term maintenance capabilities have become important competitive differentiators because customers increasingly require turnkey deployment rather than standalone equipment purchases.

Growth opportunities extend across multiple industries including banking and financial services, healthcare, manufacturing, telecommunications, education, government, and media. Enterprises deploying AI-enabled applications, digital twins, advanced analytics, and large-scale virtualization are creating sustained demand for cooling systems capable of supporting higher computational densities without major increases in facility footprint.

Market Drivers

Expansion of AI and High-Density Computing Infrastructure

Artificial intelligence training, machine learning, and high-performance computing require processors with substantially higher thermal design power than conventional enterprise servers. GPU-intensive workloads generate concentrated heat that challenges conventional air cooling systems. Consequently, hyperscale cloud providers, research institutions, financial organizations, and technology companies are investing in liquid cooling architectures capable of supporting future processor roadmaps. Suppliers are responding by expanding direct-to-chip cooling platforms, immersion systems, and integrated rack-level thermal management solutions, creating additional opportunities across hardware and engineering services.

Rising Focus on Data Centre Energy Efficiency

Electricity costs represent a major operating expense for data centre owners. Cooling infrastructure accounts for a considerable proportion of facility energy consumption, making efficiency improvements financially attractive. Liquid cooling enables higher heat removal efficiency, reducing dependence on energy-intensive mechanical cooling equipment. Buyers increasingly evaluate procurement proposals using total cost of ownership, operational efficiency, and expected reductions in facility power consumption rather than initial purchase price alone. Vendors therefore compete by demonstrating measurable improvements in energy performance and operating economics.

Growth in Hyperscale and Colocation Facilities

Cloud service providers and colocation operators continue expanding regional capacity to support enterprise cloud migration, AI services, streaming applications, and digital business operations. New facilities are increasingly designed for higher rack densities than previous generations, making liquid cooling an important design consideration. Engineering firms, cooling technology providers, and infrastructure suppliers benefit from larger project sizes, long-term maintenance agreements, and standardized deployment across multiple facilities.

Sustainability Commitments Supporting Cooling Modernization

Corporate sustainability targets are influencing infrastructure investment decisions. Many enterprise operators and hyperscale providers have established carbon reduction objectives alongside commitments to improve resource efficiency. Liquid cooling technologies contribute by lowering electricity demand for thermal management and enabling better utilization of available data centre space. Procurement teams increasingly include environmental performance metrics alongside technical specifications during vendor evaluation.

Market Restraints and Challenges

High Initial Capital Investment

Liquid cooling installations generally require specialized infrastructure, plumbing systems, coolant distribution units, and engineering expertise. Existing facilities may also require modifications before deployment. Smaller enterprises often postpone adoption because financial returns depend on workload density and long-term utilization rates. Vendors address this challenge through modular systems, phased deployment strategies, and lifecycle service contracts that reduce implementation complexity.

Limited Retrofit Compatibility

Many operational data centres were originally designed for conventional air cooling. Retrofitting liquid cooling into these facilities can involve structural modifications, equipment relocation, and temporary operational disruption. This complexity increases project costs and lengthens procurement cycles. Suppliers therefore increasingly develop hybrid cooling solutions that integrate with existing environments while allowing gradual migration toward higher-density architectures.

Skills and Maintenance Requirements

Liquid cooling systems require personnel with expertise in coolant management, leak detection, thermal monitoring, and specialized maintenance procedures. Some organizations lack internal technical resources to manage these systems effectively. This has increased demand for managed maintenance contracts, remote monitoring services, and vendor-certified engineering support.

Supply Chain Complexity for Specialized Components

Cold plates, pumps, heat exchangers, precision connectors, dielectric fluids, and monitoring equipment rely on specialized manufacturing capabilities. Supply disruptions or extended lead times may delay project execution and increase procurement costs. Manufacturers are mitigating these risks through supplier diversification, regional manufacturing expansion, and strategic inventory management.

Major Segment Analysis

Cold Plate Cooling Leads Commercial Deployments

Cold plate cooling represents one of the most commercially important technologies because it provides an effective balance between cooling performance, infrastructure compatibility, and deployment flexibility. Rather than immersing complete servers in dielectric fluid, cold plate systems remove heat directly from processors and other high-power components while allowing organizations to retain familiar server architectures.

Demand is strongest among hyperscale cloud operators, enterprise AI deployments, financial institutions, and research organizations that require increased computing density without replacing existing operational models. Buyers prefer solutions compatible with established server platforms and existing data centre management processes. This reduces deployment risk while supporting future processor upgrades.

Competition within this segment increasingly depends on thermal efficiency, coolant distribution design, monitoring software integration, ease of maintenance, and compatibility with processors from multiple hardware vendors. Suppliers also differentiate through engineering services, installation support, and performance guarantees. As processor power consumption continues to increase, cold plate cooling is expected to remain an important revenue contributor across both new construction and selected retrofit projects.

Regional Analysis

North America

North America remains a major market due to extensive hyperscale cloud infrastructure, AI investment, advanced semiconductor development, and strong enterprise technology spending. The United States accounts for most regional demand, supported by cloud service providers, financial institutions, research laboratories, and technology companies investing in next-generation computing infrastructure. Procurement decisions emphasize operational efficiency, scalability, and sustainability performance. Canada also attracts investment because of expanding cloud infrastructure and comparatively favorable climate conditions for data centre operations.

Europe

European demand is influenced by stringent environmental objectives, energy efficiency initiatives, and continued digital infrastructure investment. Operators increasingly evaluate cooling technologies based on lifecycle emissions and electricity consumption. Countries including Germany, France, Spain, and the United Kingdom continue expanding colocation capacity while integrating higher-density computing environments. Regulatory compliance and sustainability reporting influence procurement decisions more strongly than in many other regions.

Asia Pacific

Asia Pacific represents the fastest-expanding regional opportunity owing to sustained investments in hyperscale data centres, semiconductor manufacturing, AI development, and cloud infrastructure. China, Japan, India, South Korea, Taiwan, and Indonesia continue expanding digital infrastructure to support enterprise cloud adoption and growing internet usage. Buyers increasingly prioritize scalable cooling technologies capable of supporting future AI workloads while maintaining energy efficiency. Regional manufacturing capabilities also strengthen equipment availability and supply chain resilience.

Middle East & Africa

Investment in cloud infrastructure, digital government initiatives, and smart city programs is creating demand for advanced cooling technologies. Countries including Saudi Arabia, the UAE, and Israel continue expanding data centre capacity to support regional digital services. High ambient temperatures increase the importance of efficient thermal management, making liquid cooling attractive for selected high-density facilities despite relatively smaller market size.

South America

Brazil leads regional demand through expanding cloud services, financial sector digitalization, and enterprise modernization initiatives. Argentina and other regional markets continue investing in localized data centre infrastructure to improve digital service delivery. Economic uncertainty and infrastructure investment constraints remain important considerations, although demand for efficient cooling technologies is gradually increasing among larger commercial operators.

Competitive Landscape

The competitive environment includes diversified power infrastructure manufacturers, thermal management specialists, server vendors, and engineering solution providers. Competition increasingly extends beyond equipment supply toward integrated cooling ecosystems that combine hardware, software, digital monitoring, engineering services, installation, and long-term maintenance.

Suppliers differentiate themselves through thermal efficiency, compatibility with emerging AI hardware, modular deployment capability, monitoring software, and service network coverage. Strategic partnerships between cooling technology developers, server manufacturers, semiconductor companies, and colocation providers are strengthening integrated solution offerings. Geographic expansion, localized manufacturing, and technical support capabilities continue influencing purchasing decisions, particularly for multinational cloud providers deploying standardized infrastructure across multiple regions.

Companies operating in this market include Airedale International Air Conditioning Ltd., IBM Corporation, Fujitsu Limited, Eaton Corporation plc, Vertiv Group Corp., Hewlett Packard Enterprise Development LP, Schneider Electric SE, Boyd Corporation, Alfa Laval AB, and JETCOOL Technologies Inc.

Recent Developments

March 2026: Accelsius introduced the NeuCool® IR150, the industry's first integrated in-rack two-phase liquid cooling system with 150 kW cooling capacity, targeting AI and high-performance computing data centre deployments.

March 2026: Alfa Laval launched FreeWaterLoop, an integrated liquid-based external cooling system combining heat exchangers, pumps, and filtration to improve energy efficiency and support high-density computing in modern data centres.

February 2026: Schneider Electric inaugurated its Motivair liquid cooling solutions factory in Bengaluru, India, establishing its first Indian manufacturing site for liquid cooling systems to support AI-ready, high-density data centres.

January 14, 2026: Vertiv introduced new Vertiv™ MegaMod™ HDX configurations, integrating direct-to-chip liquid cooling with modular AI infrastructure, supporting deployments up to 10 MW and rack densities exceeding 100 kW per rack.

Regulatory and Policy Environment

Energy efficiency regulations, environmental reporting requirements, and sustainability commitments increasingly influence cooling infrastructure investments. Data centre operators monitor energy performance indicators such as Power Usage Effectiveness (PUE) while aligning facilities with national energy efficiency policies. Standards developed by organizations including ASHRAE provide guidance for thermal management, equipment operating conditions, and liquid cooling implementation.

Environmental regulations affecting refrigerants, electricity consumption, and emissions reporting also influence procurement decisions. Government programs supporting digital infrastructure, cloud computing, AI development, and semiconductor manufacturing indirectly stimulate investment in advanced cooling technologies. Compliance requirements related to operational reliability, occupational safety, water management, and environmental performance are encouraging adoption of modern thermal management systems with comprehensive monitoring capabilities.

Outlook and Strategic Implications

The commercial outlook for the data centre liquid cooling market will be shaped by continued increases in processor power consumption, expansion of AI infrastructure, and greater emphasis on operational efficiency. Procurement strategies are expected to shift toward standardized liquid cooling architectures capable of supporting multiple generations of computing equipment with minimal facility modification.

Investment priorities will increasingly emphasize modular deployments, integrated monitoring software, predictive maintenance capabilities, and lifecycle service agreements. Buyers are expected to evaluate suppliers based on technical integration capability, engineering expertise, operational support, and long-term reliability rather than equipment cost alone.

Competition will continue moving toward complete infrastructure solutions that integrate thermal management with power distribution, rack systems, automation, and facility monitoring. Companies capable of delivering scalable, energy-efficient platforms supported by global service networks are likely to strengthen their competitive positions. Although capital investment requirements and retrofit complexity remain important constraints, sustained expansion of AI computing, hyperscale cloud infrastructure, and enterprise digital workloads will continue supporting long-term demand for liquid cooling technologies across global data centre markets.

Data Centre Liquid Cooling Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 3.75 billion |

| Total Market Size in 2031 | USD 10.5 billion |

| Forecast Unit | Billion |

| Growth Rate | 22.87% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Enterprise Size, Cooling Technology, End User, Industry Vertical, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

- Hardware

- Software

- Services

By Enterprise Size

- Small Enterprises

- Medium Enterprises

- Large Enterprises

By Cooling Technology

- Immersion Cooling

- Cold Plate Cooling

- Others

By End User

- Colocation Service Providers

- Cloud Service Providers

- Enterprises

- Others

By Industry Vertical

- Banking and Financial Services

- Manufacturing

- Healthcare

- IT & Telecommunications

- Education

- Government

- Media and Entertainment

- Others

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Taiwan

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

2. RESEARCH METHODOLOGY

2.1. Research Data

2.2. Research Design

2.3. Validation

3. EXECUTIVE SUMMARY

3.1. Research Highlights

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

5. DATA CENTER LIQUID COOLING MARKET BY COMPONENT

5.1. Introduction

5.2. Hardware

5.3. Software

5.4. Services

6. DATA CENTER LIQUID COOLING MARKET BY ENTERPRISE SIZE

6.1. Introduction

6.2. Small Enterprises

6.3. Medium Enterprises

6.4. Large Enterprises

7. DATA CENTER LIQUID COOLING MARKET BY COOLING TECHNOLOGY

7.1. Introduction

7.2. Immersion Cooling

7.3. Cold Plate Cooling

7.4. Others

8. DATA CENTER LIQUID COOLING MARKET BY END USER

8.1. Introduction

8.2. Colocation Service Providers

8.3. Cloud Service Providers

8.4. Enterprises

8.5. Others

9. DATA CENTER LIQUID COOLING MARKET BY INDUSTRY VERTICAL

9.1. Introduction

9.2. Banking and Financial Services

9.3. Manufacturing

9.4. Healthcare

9.5. IT & Telecommunications

9.6. Education

9.7. Government

9.8. Media and Entertainment

9.9. Others

10. DATA CENTER LIQUID COOLING MARKET BY GEOGRAPHY

10.1. Introduction

10.2. North America

10.2.1. USA

10.2.2. Canada

10.2.3. Mexico

10.3. South America

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Others

10.4. Europe

10.4.1. Germany

10.4.2. France

10.4.3. United Kingdom

10.4.4. Spain

10.4.5. Others

10.5. Middle East and Africa

10.5.1. Saudi Arabia

10.5.2. UAE

10.5.3. Israel

10.5.4. Others

10.6. Asia Pacific

10.6.1. China

10.6.2. Japan

10.6.3. India

10.6.4. South Korea

10.6.5. Indonesia

10.6.6. Taiwan

10.6.7. Others

11. COMPETITIVE ENVIRONMENT AND ANALYSIS

11.1. Major Players and Strategy Analysis

11.2. Emerging Players and Market Lucrativeness

11.3. Mergers, Acquisitions, Agreements, and Collaborations

11.4. Vendor Competitiveness Matrix

12. COMPANY PROFILES

12.1. Airedale International Air Conditioning Ltd.

12.2. IBM Corporation

12.3. Fujitsu Limited

12.4. Eaton Corporation plc

12.5. Vertiv Group Corp.

12.6. Hewlett Packard Enterprise Development LP

12.7. Schneider Electric SE

12.8. Boyd Corporation

12.9. Alfa Laval AB

12.10. JETCOOL Technologies Inc.

Navigate

Trusted by the world's leading organizations