Report Overview

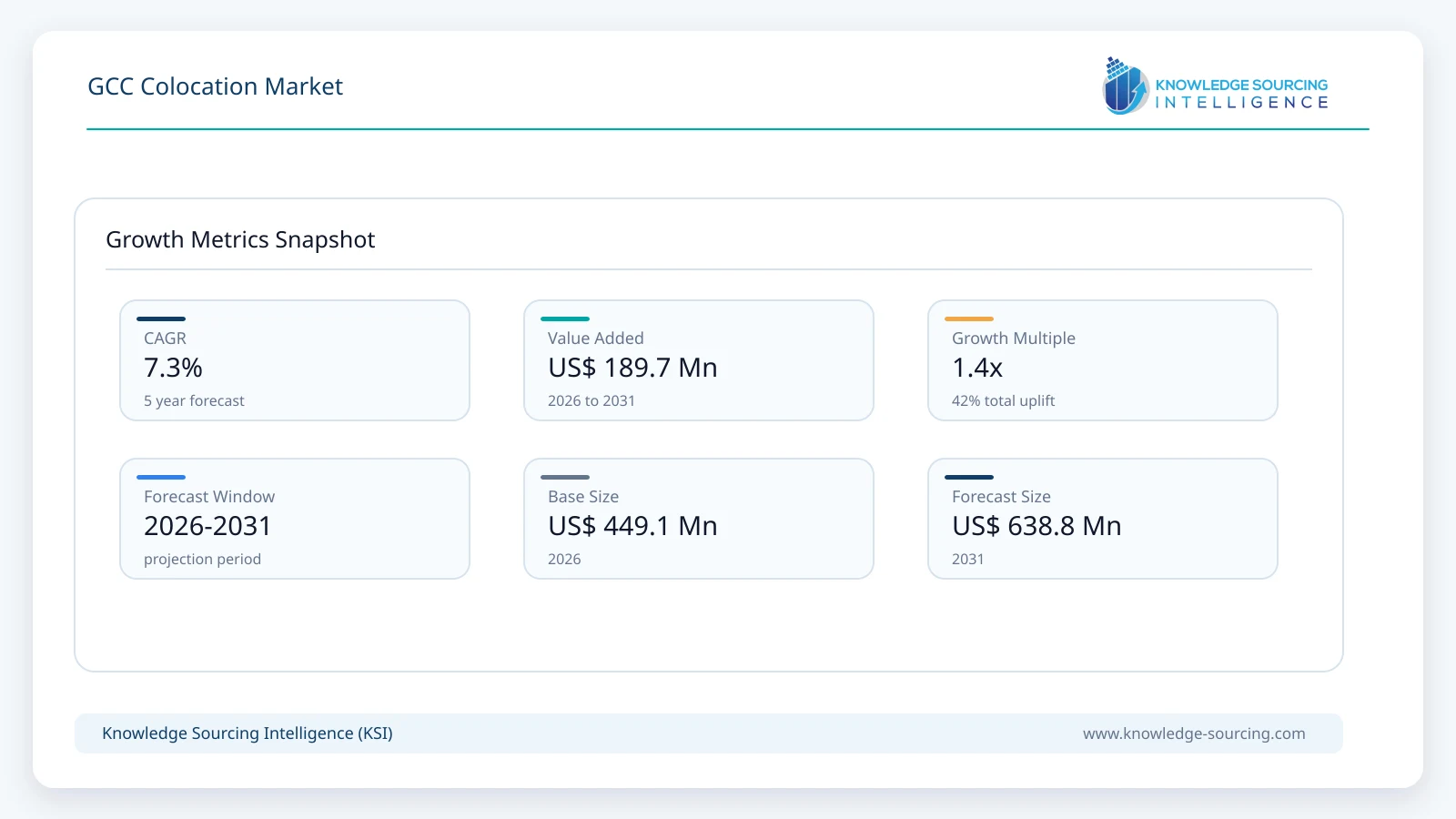

The GCC Colocation Market is forecast to grow at a CAGR of 7.30%, reaching USD 638.82 million in 2031 from USD 449.12 million in 2026.

Highlights:

- 1Government-led digital infrastructure programmes remain the primary catalyst supporting new colocation capacity across GCC countries.

- 2Retail colocation continues to attract broad enterprise demand from organisations seeking flexible infrastructure without major capital investment.

- 3Saudi Arabia and the UAE account for the largest pipeline of new carrier-neutral data centre developments.

- 4High-density computing and AI workloads are increasing demand for advanced cooling technologies and resilient power architecture.

- 5Data residency regulations and cybersecurity requirements encourage domestic hosting of critical workloads.

- 6Competition increasingly centres on interconnection ecosystems, sustainability credentials, service quality, and geographic expansion rather than pricing alone.

The GCC colocation market comprises third-party data centre facilities that provide rack space, power, cooling, physical security, and interconnection services for enterprise IT infrastructure. Organisations adopt colocation to reduce capital expenditure on in-house facilities while improving service continuity, scalability, regulatory compliance, and connectivity. Unlike conventional hosting, colocation enables customers to retain ownership of servers and storage systems while outsourcing facility operations to specialised providers.

Demand has shifted beyond traditional telecommunications customers. Financial institutions, hyperscale cloud providers, government agencies, healthcare organisations, energy companies, manufacturers, and digital commerce businesses are expanding their colocation footprint as workloads become more distributed and data residency obligations strengthen. Procurement decisions increasingly consider network density, carrier neutrality, energy efficiency, security certifications, disaster recovery capability, and proximity to major business districts.

Across the GCC, national economic diversification programmes have accelerated investment in digital infrastructure. Saudi Arabia's Vision 2030, the UAE Digital Government Strategy, Qatar National Vision 2030, and similar initiatives in Oman, Bahrain, and Kuwait encourage cloud adoption, artificial intelligence deployment, smart city programmes, and digital public services. These programmes create sustained demand for carrier-grade data centre capacity that can support both public and private sector digitalisation.

Buyer behaviour has also evolved. Large enterprises increasingly seek hybrid infrastructure strategies that combine public cloud services with dedicated colocation facilities. This approach enables organisations to manage latency-sensitive applications, confidential workloads, and regulatory requirements without maintaining expensive captive facilities. Service-level agreements, renewable energy availability, cybersecurity capabilities, and cross-connect ecosystems now carry greater weight during vendor selection than simple rack pricing.

Revenue generation within the market extends beyond cabinet rental. Providers increasingly differentiate through managed services, remote operations, network connectivity, disaster recovery support, and energy optimisation. The expansion of artificial intelligence applications, content delivery networks, edge computing, and enterprise cloud migration continues to broaden demand for high-density deployments requiring resilient power and advanced cooling infrastructure.

Market Drivers

Expansion of National Digital Infrastructure Programmes

Public investment remains one of the strongest demand generators for colocation services. Governments across the GCC continue expanding digital government platforms, smart city initiatives, digital identity programmes, and cloud-first policies. These projects require secure and highly available infrastructure capable of supporting national digital services. Colocation operators benefit because many government agencies prefer certified third-party facilities that satisfy operational resilience and security requirements while avoiding lengthy construction timelines associated with dedicated data centres.

Enterprise Migration Toward Hybrid IT Architectures

Large organisations increasingly balance public cloud adoption with privately managed infrastructure. Financial institutions, telecom operators, healthcare providers, and industrial companies continue relocating mission-critical applications into colocation facilities where they can access multiple cloud providers through low-latency connections. Buyers prioritise flexibility, compliance, and business continuity, encouraging operators to invest in richer connectivity ecosystems and managed infrastructure services.

Rising Demand for AI, Cloud, and Content Delivery Infrastructure

Artificial intelligence training, analytics platforms, streaming services, and digital commerce applications require substantial computing resources with dependable power availability. High-density server deployments place greater emphasis on cooling efficiency, power redundancy, and network performance. Colocation providers respond by expanding facilities capable of supporting higher rack densities and advanced thermal management systems, improving their ability to accommodate modern enterprise workloads.

Strengthening Data Sovereignty and Cybersecurity Requirements

Regulatory expectations surrounding sensitive information continue influencing infrastructure procurement decisions. Financial institutions, healthcare providers, government entities, and critical infrastructure operators increasingly require domestic hosting environments with recognised security certifications. Colocation providers meeting international operational standards gain competitive advantages as enterprises seek facilities capable of supporting compliance obligations without compromising operational efficiency.

Market Restraints and Challenges

High Capital Requirements for New Facilities

Modern colocation facilities require substantial upfront investment in land acquisition, electrical infrastructure, cooling systems, backup generation, physical security, and network connectivity. Rising construction costs and specialised equipment procurement extend project timelines while increasing financial exposure. Operators mitigate these challenges through phased development, strategic partnerships, and long-term customer commitments before commissioning additional capacity.

Power Availability and Energy Sustainability

Reliable electricity remains fundamental to colocation operations. Rapid increases in AI-related computing demand have elevated power density requirements beyond conventional enterprise workloads. Securing sufficient grid capacity while meeting sustainability objectives presents operational challenges, particularly for facilities pursuing renewable energy commitments. Operators increasingly incorporate energy-efficient cooling technologies and long-term renewable power agreements to manage operational costs.

Limited Availability of Highly Skilled Technical Personnel

Advanced data centre operations require specialists in electrical engineering, mechanical systems, cybersecurity, network operations, and facility management. Competition for experienced professionals remains intense across GCC markets as infrastructure investment accelerates. Companies address workforce constraints through technical training programmes, automation, remote monitoring platforms, and partnerships with technology vendors.

Procurement Complexity for Enterprise Customers

Selecting a colocation provider now involves evaluating security standards, network ecosystems, sustainability performance, service availability, compliance certifications, and future scalability. Procurement cycles have therefore become longer, particularly among highly regulated industries. Providers increasingly support buyers through consulting services, migration planning, and customised service agreements that reduce implementation risks.

Major Segment Analysis

Retail Colocation Represents the Largest Commercial Opportunity

Retail colocation continues to represent the most commercially significant segment because it serves organisations requiring scalable infrastructure without committing to large dedicated facilities. Customers typically lease cabinets, cages, or limited floor space while maintaining ownership of their computing equipment. This operating model appeals to enterprises undergoing cloud migration, application modernisation, disaster recovery planning, and regional expansion.

Demand originates from organisations with variable infrastructure requirements rather than hyperscale operators requiring entire facilities. Financial institutions, healthcare providers, software companies, logistics businesses, and government agencies value the flexibility to expand incrementally while maintaining operational control over hardware assets. This reduces capital expenditure and shortens deployment schedules.

Competition within retail colocation increasingly depends on connectivity ecosystems, managed support services, security certifications, and customer experience. Providers capable of delivering rapid deployment, remote hands support, carrier diversity, and direct cloud connectivity strengthen customer retention while generating recurring service revenues beyond space rental alone. The segment also provides greater customer diversification, reducing dependence on a limited number of hyperscale contracts.

Regional Analysis

Saudi Arabia represents the largest investment destination within the GCC colocation market, supported by substantial government expenditure on digital infrastructure, artificial intelligence initiatives, and cloud adoption under Vision 2030. Enterprise digitalisation, financial sector modernisation, and expanding industrial automation continue generating demand for secure carrier-neutral facilities.

The United Arab Emirates maintains one of the region's most mature colocation ecosystems. Strong international connectivity, favourable business regulations, and concentration of multinational enterprises encourage continuous investment in high-capacity data centres. Demand remains supported by financial services, aviation, logistics, media, and digital commerce sectors seeking regional infrastructure hubs.

Qatar continues expanding digital infrastructure following sustained investment in telecommunications and public sector digital services. National cloud initiatives and smart infrastructure projects contribute to steady enterprise demand for resilient hosting environments.

Kuwait, Oman, and Bahrain represent emerging opportunities where enterprise cloud adoption, financial sector modernisation, and government digital programmes are supporting additional colocation requirements. While overall capacity remains smaller than Saudi Arabia and the UAE, improving connectivity and policy support continue attracting infrastructure investment. Market expansion across these countries nevertheless depends on power availability, specialised workforce development, and continued enterprise adoption of outsourced infrastructure services.

Competitive Landscape

The GCC colocation market remains moderately concentrated, combining regional telecommunications operators with specialised data centre companies expanding across multiple countries. Competition increasingly reflects service quality rather than basic infrastructure availability.

Providers differentiate through geographic coverage, carrier neutrality, cloud interconnection capabilities, sustainability initiatives, operational certifications, and managed infrastructure services. Strategic partnerships with hyperscale cloud providers, telecommunications operators, and systems integrators strengthen customer acquisition by expanding connectivity options and simplifying hybrid cloud deployment.

Expansion strategies increasingly involve constructing large-scale campuses capable of supporting high-density computing while reserving land for future development. Companies also pursue operational efficiencies through advanced cooling technologies, AI-assisted facility monitoring, renewable energy integration, and automation. As enterprise customers demand consistent service across multiple GCC countries, regional presence has become an increasingly important competitive attribute.

The competitive environment includes Equinix, Inc., Khazna Data Centers, Gulf Data Hub, Moro Hub, center3, Ooredoo, Mobily, and e& (e& Enterprise), all competing through infrastructure scale, connectivity ecosystems, strategic partnerships, and regional expansion rather than price-led competition.

Recent Developments

April 2026: Edarat Communication and Information Technology Company announced a five-year colocation services contract with Edge Network Services Limited, strengthening enterprise data centre hosting capabilities in Saudi Arabia.

February 2026: ST Telemedia Global Data Centres India announced its fourth Chennai data centre launch and 45MW AI-ready Siruseri campus expansion, highlighting continued regional colocation infrastructure investments.

January 2026: Saudi Arabia’s Saudi Data and AI Authority (SDAIA) announced the launch of the Hexagon Data Center in Riyadh, a Tier IV facility designed to support advanced digital infrastructure and large-scale technology workloads.

Regulatory and Policy Environment

Government policy plays a central role in shaping the GCC colocation market. National digital economy strategies encourage cloud adoption while strengthening cybersecurity governance and domestic digital infrastructure investment. Public sector procurement increasingly favours facilities demonstrating recognised operational resilience, information security, and business continuity certifications.

Data protection regulations across GCC countries continue influencing infrastructure deployment decisions by requiring appropriate handling of sensitive government, healthcare, and financial information. Organisations operating critical infrastructure must satisfy sector-specific cybersecurity obligations alongside broader privacy requirements.

International standards such as ISO 27001 for information security management, ISO 22301 for business continuity, and recognised data centre operational certifications remain important procurement requirements. Environmental considerations are also receiving greater attention as operators pursue improved energy efficiency, water conservation, and lower carbon intensity in response to government sustainability programmes.

Outlook and Strategic Implications

The GCC colocation market is expected to benefit from sustained investment in cloud infrastructure, artificial intelligence deployment, enterprise digital services, and public sector modernisation over the coming years. Demand will increasingly originate from hybrid IT architectures requiring close integration between dedicated enterprise infrastructure and hyperscale cloud platforms.

Investment priorities are expected to favour high-density facilities capable of supporting AI workloads, advanced cooling technologies, renewable energy integration, and expanded interconnection ecosystems. Buyers will continue evaluating providers based on operational resilience, sustainability performance, compliance capabilities, and geographic coverage rather than facility space alone.

Procurement strategies are also becoming more sophisticated. Enterprises increasingly seek long-term infrastructure partners capable of supporting expansion across multiple GCC countries while maintaining consistent service quality. Providers offering integrated managed services, cloud connectivity, remote operations, and security capabilities are likely to strengthen customer retention and generate higher recurring revenues.

Competition is expected to intensify as new capacity enters the market. However, operators with established connectivity ecosystems, proven operational performance, strategic utility partnerships, and scalable development pipelines should remain well positioned. Potential risks include construction cost inflation, electricity constraints, evolving cybersecurity obligations, and continued competition for skilled technical personnel. Despite these considerations, the commercial outlook remains supported by structural demand for secure, scalable, and compliant digital infrastructure throughout the GCC region.

GCC Colocation Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 449.12 million |

| Total Market Size in 2031 | USD 638.82 million |

| Forecast Unit | Million |

| Growth Rate | 7.30% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Service Type, Industry Vertical, Country |

| Companies |

|

Market Segmentation

By Type

By Service Type

By Industry Vertical

By Country

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. GCC COLOCATION MARKET BY TYPE

5.1. Introduction

5.2. Retail Colocation

5.3. Wholesale Colocation

6. GCC COLOCATION MARKET BY SERVICE TYPE

6.1. Introduction

6.2. Power & Cooling Services

6.3. Networking Services

6.4. Security Services

6.5. Remote Hands Services

6.6. Monitoring & Management Services

7. GCC COLOCATION MARKET BY INDUSTRY VERTICAL

7.1. Introduction

7.2. Telecom and IT

7.3. Banking, Financial Services, and Insurance (BFSI)

7.4. Government and Public Sector

7.5. Healthcare

7.6. Energy & Utilities

7.7. Manufacturing

7.8. Media & Entertainment

7.9. E-commerce

7.10. Others

8. GCC COLOCATION MARKET BY COUNTRY

8.1. Introduction

8.2. Saudi Arabia

8.2.1. By Type

8.2.2. By Service Type

8.2.3. By Industry Vertical

8.3. United Arab Emirates (UAE)

8.3.1. By Type

8.3.2. By Service Type

8.3.3. By Industry Vertical

8.4. Qatar

8.4.1. By Type

8.4.2. By Service Type

8.4.3. By Industry Vertical

8.5. Kuwait

8.5.1. By Type

8.5.2. By Service Type

8.5.3. By Industry Vertical

8.6. Oman

8.6.1. By Type

8.6.2. By Service Type

8.6.3. By Industry Vertical

8.7. Bahrain

8.7.1. By Type

8.7.2. By Service Type

8.7.3. By Industry Vertical

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Equinix, Inc.

10.2. Khazna Data Centers

10.3. Gulf Data Hub

10.4. Moro Hub

10.5. center3

10.6. Ooredoo

10.7. Mobily

10.8. e& (e& Enterprise)

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations