Report Overview

The global private cloud automation market is anticipated to expand at a high CAGR during the forecast period.

Highlights:

- 1Rising enterprise demand for infrastructure standardisation and operational efficiency is strengthening investment in private cloud automation.

- 2Cloud orchestration and automation solutions represent one of the most commercially important product categories because they coordinate complex enterprise workloads.

- 3North America remains a major revenue contributor owing to mature enterprise IT infrastructure and sustained investment in hybrid cloud environments.

- 4AI-assisted infrastructure management and policy-based automation are improving operational visibility and reducing administrative workloads.

- 5Data protection regulations and cybersecurity compliance requirements continue to influence purchasing decisions across regulated industries.

- 6Competition increasingly centres on platform interoperability, automation depth, hybrid cloud integration, and enterprise support capabilities.

The private cloud automation market comprises software platforms and professional services that automate the provisioning, configuration, orchestration, monitoring, governance, and lifecycle management of private cloud infrastructure. These solutions enable enterprises to standardise IT operations, reduce manual intervention, improve infrastructure utilisation, and support application deployment across virtualised and hybrid environments. Automation spans infrastructure provisioning, configuration management, workload orchestration, backup scheduling, disaster recovery, and DevOps workflows, allowing organisations to operate private cloud environments with greater consistency and operational control.

Demand for private cloud automation continues to expand as enterprises seek to modernise data centre operations while retaining direct control over sensitive workloads. Organisations operating in regulated industries such as banking, healthcare, government, and critical infrastructure often prioritise private cloud environments because they provide greater visibility over security policies, compliance requirements, and data residency obligations. As application portfolios become more distributed and software deployment cycles shorten, IT teams require automation platforms that reduce operational complexity without compromising governance.

Buyer priorities have shifted beyond infrastructure virtualisation toward policy-driven automation, workload consistency, and operational resilience. Procurement decisions increasingly evaluate interoperability with existing enterprise platforms, integration with Kubernetes environments, Infrastructure-as-Code (IaC) frameworks, security monitoring tools, and multi-vendor infrastructure. Enterprises also assess long-term support capabilities, API maturity, licensing flexibility, and compatibility with hybrid cloud architectures before selecting automation platforms.

Industry structure reflects collaboration between infrastructure vendors, enterprise software providers, cloud platform suppliers, and systems integration firms. Software vendors generate recurring revenue through platform subscriptions, enterprise licences, and lifecycle management services, while consulting and implementation partners support migration planning, workflow design, integration, and operational optimisation. Service revenues remain closely tied to complex enterprise deployments that require customised automation policies and legacy infrastructure integration.

Revenue expansion is supported by enterprise investment in application modernisation, software-defined infrastructure, AI-assisted IT operations, and compliance automation. Organisations continue replacing isolated management tools with integrated automation platforms capable of managing compute, storage, networking, and security functions through unified policy engines. Adoption is particularly evident among enterprises operating large private data centres where manual infrastructure administration increases operational costs and deployment delays.

Market Drivers

Growing enterprise adoption of hybrid IT architectures

Many organisations now operate applications across on-premises infrastructure, private clouds, and selected public cloud services. This operating model creates management complexity that cannot be efficiently addressed through manual administration. Private cloud automation platforms simplify workload deployment, infrastructure provisioning, and lifecycle management through unified orchestration policies. Enterprises purchasing these solutions seek operational consistency rather than simply reducing labour costs. Vendors have responded by expanding hybrid cloud management capabilities that integrate virtual machines, containers, storage systems, and network resources through common automation frameworks.

Expansion of regulatory compliance requirements

Financial institutions, healthcare providers, defence organisations, and government agencies face strict requirements governing data protection, auditability, and operational resilience. Automated configuration management reduces human error while maintaining documented compliance procedures. Buyers increasingly value automation tools capable of enforcing security policies, maintaining configuration baselines, and generating compliance reports. Suppliers therefore compete by embedding governance controls, identity management integration, and policy enforcement into automation platforms rather than offering standalone orchestration capabilities.

Enterprise investment in DevOps and application delivery

Software development teams require infrastructure that can be provisioned quickly without compromising operational governance. Automation platforms supporting CI/CD pipelines accelerate application deployment while maintaining standardised infrastructure configurations. Organisations adopting DevOps practices increasingly procure infrastructure automation alongside application development tools. Software vendors continue integrating Kubernetes, GitOps, and Infrastructure-as-Code capabilities to support enterprise development environments with shorter release cycles.

Rising operational costs within enterprise data centres

Labour-intensive infrastructure management remains costly for organisations operating large server estates. Manual provisioning, software updates, configuration changes, and disaster recovery testing require skilled personnel and introduce operational risk. Automation improves resource utilisation while reducing repetitive administrative tasks. Enterprises evaluating automation platforms frequently compare expected operational savings, infrastructure availability improvements, and reduced deployment times when determining investment priorities.

Market Restraints and Challenges

Complex integration with legacy infrastructure

Many enterprises continue operating heterogeneous infrastructure assembled over several technology generations. Legacy hardware, proprietary applications, and customised operational processes complicate automation deployment. Integration projects often require extensive systems engineering and workflow redesign, increasing implementation costs and extending project timelines. Service providers mitigate these challenges through phased deployment strategies and customised migration planning.

Shortage of automation and cloud operations expertise

Successful automation requires knowledge spanning cloud architecture, scripting, security, networking, and infrastructure engineering. Many organisations face shortages of professionals capable of designing enterprise-wide automation policies. Skills constraints may delay implementation or limit automation to selected workloads rather than enterprise-wide deployment. Vendors increasingly provide low-code automation interfaces, predefined templates, and managed services to address workforce limitations.

Security concerns associated with automated infrastructure

Automation platforms often possess privileged access across enterprise infrastructure. Any security weakness within automation workflows can affect multiple systems simultaneously. Organisations therefore conduct extensive security assessments before deployment, increasing procurement cycles. Suppliers invest heavily in identity management integration, privileged access controls, encryption, and continuous monitoring to strengthen buyer confidence.

Budget constraints for large-scale infrastructure modernisation

Although automation reduces operational expenditure over time, initial investment may include software licensing, consulting, infrastructure upgrades, employee training, and application redesign. Organisations with constrained IT budgets frequently prioritise incremental deployment rather than enterprise-wide implementation. Flexible subscription licensing and modular platform deployment help suppliers broaden adoption among mid-sized enterprises.

Major Segment Analysis

Cloud Orchestration and Automation Solutions

Cloud orchestration and automation solutions represent one of the most commercially important segments because they coordinate infrastructure provisioning, application deployment, workload scheduling, policy enforcement, and lifecycle management through centralised automation engines. Large enterprises managing thousands of virtual machines, storage resources, and containerised applications depend on orchestration capabilities to maintain operational consistency across distributed environments.

Demand is strongest among organisations pursuing hybrid infrastructure strategies where multiple technologies must operate through unified governance frameworks. Buyers increasingly seek automation platforms capable of integrating virtual infrastructure, Kubernetes clusters, networking resources, security controls, and backup operations within a single management environment. Procurement decisions emphasise scalability, API compatibility, policy-based automation, analytics capabilities, and interoperability with existing enterprise management systems.

Competitive differentiation increasingly depends on workflow flexibility, AI-assisted operational recommendations, integration ecosystems, and enterprise support services. Suppliers offering broad infrastructure compatibility and extensive automation libraries strengthen customer retention because organisations prefer platforms that minimise future migration costs. As enterprises expand private cloud deployments alongside container-based applications, orchestration platforms continue generating substantial recurring software and services revenue.

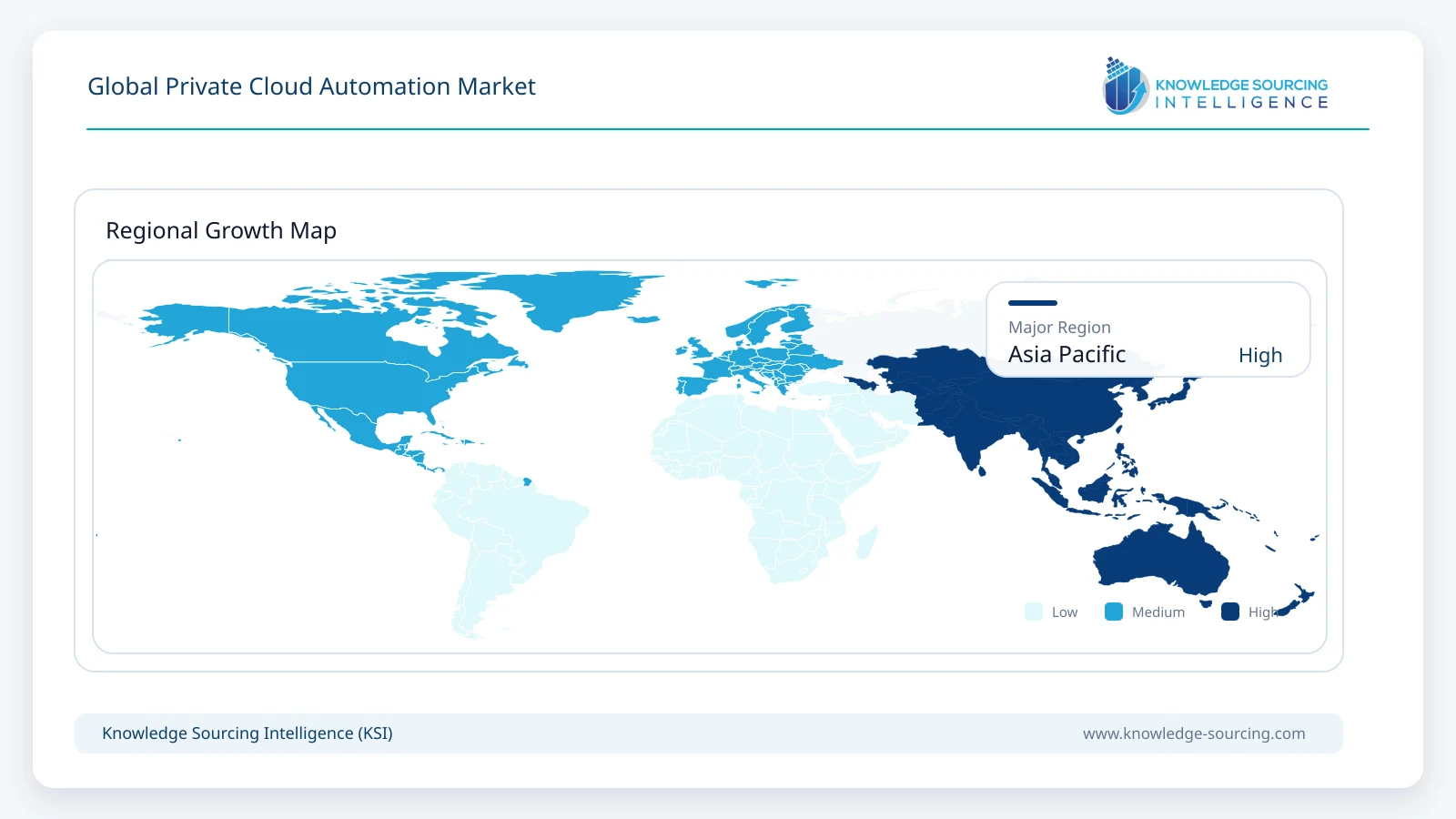

Regional Analysis

North America remains the largest commercial market due to extensive enterprise cloud investment, mature data centre infrastructure, and strong adoption among financial services, healthcare, telecommunications, and government organisations. Organisations continue modernising private infrastructure while integrating hybrid cloud operations. Strict cybersecurity requirements further encourage investment in automation platforms capable of improving governance and operational consistency.

Europe demonstrates sustained demand supported by stringent privacy regulations, industrial digitalisation programmes, and enterprise investment in secure cloud infrastructure. Financial institutions, manufacturers, and public sector organisations prioritise automation solutions that support compliance with European data protection requirements while improving infrastructure efficiency. Local data residency considerations continue supporting private cloud investment.

Asia Pacific presents substantial long-term opportunities as enterprises modernise IT infrastructure across manufacturing, banking, telecommunications, and public administration. Countries including China, Japan, India, South Korea, and Southeast Asian economies continue expanding enterprise cloud adoption while investing in domestic data centre capacity. Cost sensitivity remains important, encouraging phased automation deployment supported by implementation partners.

Middle East and Africa benefit from government investment in national digital infrastructure, smart government initiatives, financial sector modernisation, and expanding regional data centres. Adoption varies across countries according to enterprise cloud maturity, workforce availability, and investment capacity. Public sector procurement increasingly supports secure private cloud environments for critical workloads.

South America continues adopting private cloud automation within banking, telecommunications, retail, and energy industries. Organisations seek operational efficiency while modernising ageing infrastructure. Economic uncertainty and budget constraints may slow enterprise-wide deployments, although automation investments remain justified where operational resilience and regulatory compliance are business priorities.

Competitive Landscape

Competition is characterised by enterprise platform capabilities rather than price alone. Suppliers including Oracle Corporation, Microsoft Corporation, Dell Technologies Inc., Red Hat, Inc. (IBM), Cisco Systems, Inc., Google LLC, and VMware LLC (Broadcom) compete through integrated automation ecosystems supporting infrastructure management, orchestration, container platforms, security, and hybrid cloud operations.

Competitive positioning depends on enterprise interoperability, lifecycle management capabilities, automation depth, ecosystem partnerships, and professional services. Vendors continue strengthening relationships with systems integrators, managed service providers, and enterprise software partners to accelerate implementation. Geographic expansion increasingly focuses on regional cloud infrastructure, customer support capability, and industry-specific compliance solutions.

Recent Developments

April 2026: Microsoft Corporation expanded automation capabilities across its hybrid cloud management portfolio with additional AI-assisted infrastructure management features. Commercial relevance: supports enterprise operational efficiency and automated policy enforcement.

April 2026: Nutanix announced that its upcoming enterprise platform will deliver a secure virtualization foundation integrating Kubernetes services and automated infrastructure operations, enabling simplified management of AI-ready private cloud deployments.

February 2026: HPE expanded its cloud portfolio with automation capabilities enabling service providers to modernize private cloud environments, reduce dependence on legacy hypervisors and accelerate deployment of AI-driven managed services through centralized lifecycle management.

November 2025: Red Hat, Inc. (IBM) announced expanded automation capabilities for enterprise hybrid cloud environments through enhancements to its Ansible Automation Platform. Commercial relevance: improves large-scale infrastructure standardisation and operational consistency.

Regulatory and Policy Environment

Regulatory compliance substantially influences procurement decisions within the private cloud automation market. Data protection legislation, including the EU General Data Protection Regulation (GDPR), requires organisations to maintain appropriate technical controls over personal information. Automation platforms assist compliance by enforcing standardised security configurations, audit logging, and controlled infrastructure changes.

Cybersecurity frameworks published by organisations such as the U.S. National Institute of Standards and Technology (NIST), ISO/IEC 27001 information security standards, and national critical infrastructure guidance increasingly shape enterprise infrastructure policies. Government cloud adoption programmes also encourage secure automation practices through procurement requirements covering identity management, encryption, access control, and operational resilience.

Enterprises operating regulated infrastructure increasingly require automation platforms capable of supporting continuous compliance monitoring, documented change management, vulnerability remediation, and disaster recovery testing. Suppliers therefore invest heavily in governance capabilities alongside operational automation.

Outlook and Strategic Implications

Investment over the next several years is expected to prioritise policy-driven automation, AI-assisted operations, infrastructure standardisation, and hybrid cloud management rather than standalone infrastructure management tools. Enterprise buyers are likely to consolidate fragmented operational platforms into integrated automation environments supporting virtual infrastructure, containers, storage, networking, and security operations.

Procurement decisions will increasingly evaluate interoperability, security certification, operational analytics, vendor support quality, and integration with Infrastructure-as-Code frameworks. Organisations are also expected to expand investment in automation supporting compliance reporting, operational resilience, and disaster recovery readiness as regulatory oversight continues strengthening.

Competitive conditions will continue favouring suppliers capable of delivering comprehensive enterprise ecosystems rather than isolated automation functions. Partnerships with systems integrators, managed service providers, and enterprise software vendors are expected to remain important channels for customer acquisition and deployment success. Risks include persistent skills shortages, integration complexity, cybersecurity threats, and constrained enterprise IT budgets. Nevertheless, enterprises seeking greater operational efficiency, governance consistency, and infrastructure resilience are expected to sustain long-term investment in private cloud automation platforms.

Private Cloud Automation Market Scope

| Report Metric | Details |

|---|---|

| Forecast Unit | Billion |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, End-User Industry, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

By End-user Industry

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter's Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. GLOBAL PRIVATE CLOUD AUTOMATION MARKET BY COMPONENT

5.1. Introduction

5.2. Solutions

5.2.1. Cloud Orchestration and Automation

5.2.2. Configuration Management Automation

5.2.3. Infrastructure Provisioning Automation

5.2.4. Cloud Migration Automation

5.2.5. Backup and Disaster Recovery Automation

5.2.6. DevOps and CI/CD Automation

5.3. Services

5.3.1. Consulting Services

5.3.2. Implementation and Integration Services

5.3.3. Support and Maintenance Services

6. GLOBAL PRIVATE CLOUD AUTOMATION MARKET BY END-USER INDUSTRY

6.1. Introduction

6.2. BFSI

6.3. IT and Telecommunications

6.4. Manufacturing

6.5. Healthcare and Life Sciences

6.6. Government and Public Sector

6.7. Retail and E-commerce

6.8. Energy and Utilities

6.9. Transportation and Logistics

6.10. Education

6.11. Others

7. GLOBAL PRIVATE CLOUD AUTOMATION MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. United States

7.2.2. Canada

7.2.3. Mexico

7.3. South America

7.3.1. Brazil

7.3.2. Argentina

7.3.3. Others

7.4. Europe

7.4.1. United Kingdom

7.4.2. Germany

7.4.3. France

7.4.4. Italy

7.4.5. Spain

7.4.6. Others

7.5. Middle East and Africa

7.5.1. Saudi Arabia

7.5.2. United Arab Emirates

7.5.3. Others

7.6. Asia Pacific

7.6.1. China

7.6.2. Japan

7.6.3. India

7.6.4. South Korea

7.6.5. Taiwan

7.6.6. Thailand

7.6.7. Indonesia

7.6.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Oracle Corporation

9.2. Microsoft Corporation

9.3. Dell Technologies Inc.

9.4. Red Hat, Inc. (IBM)

9.5. Cisco Systems, Inc.

9.6. Google LLC

9.7. VMware LLC (Broadcom)

10. APPENDIX

10.1. Currency

10.2. Assumptions

10.3. Base and Forecast Years Timeline

10.4. Key Benefits for Stakeholders

10.5. Research Methodology

10.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations