Report Overview

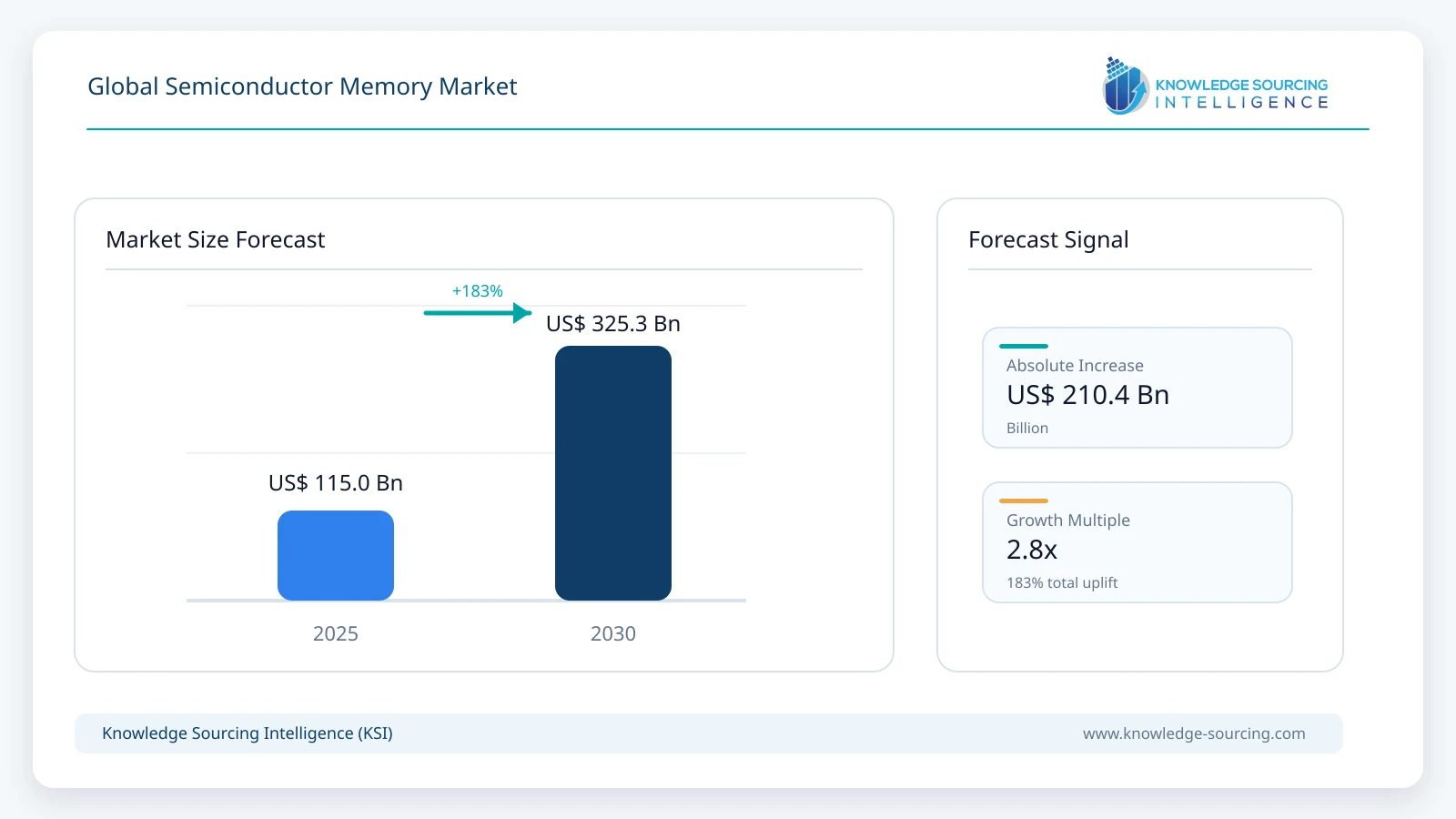

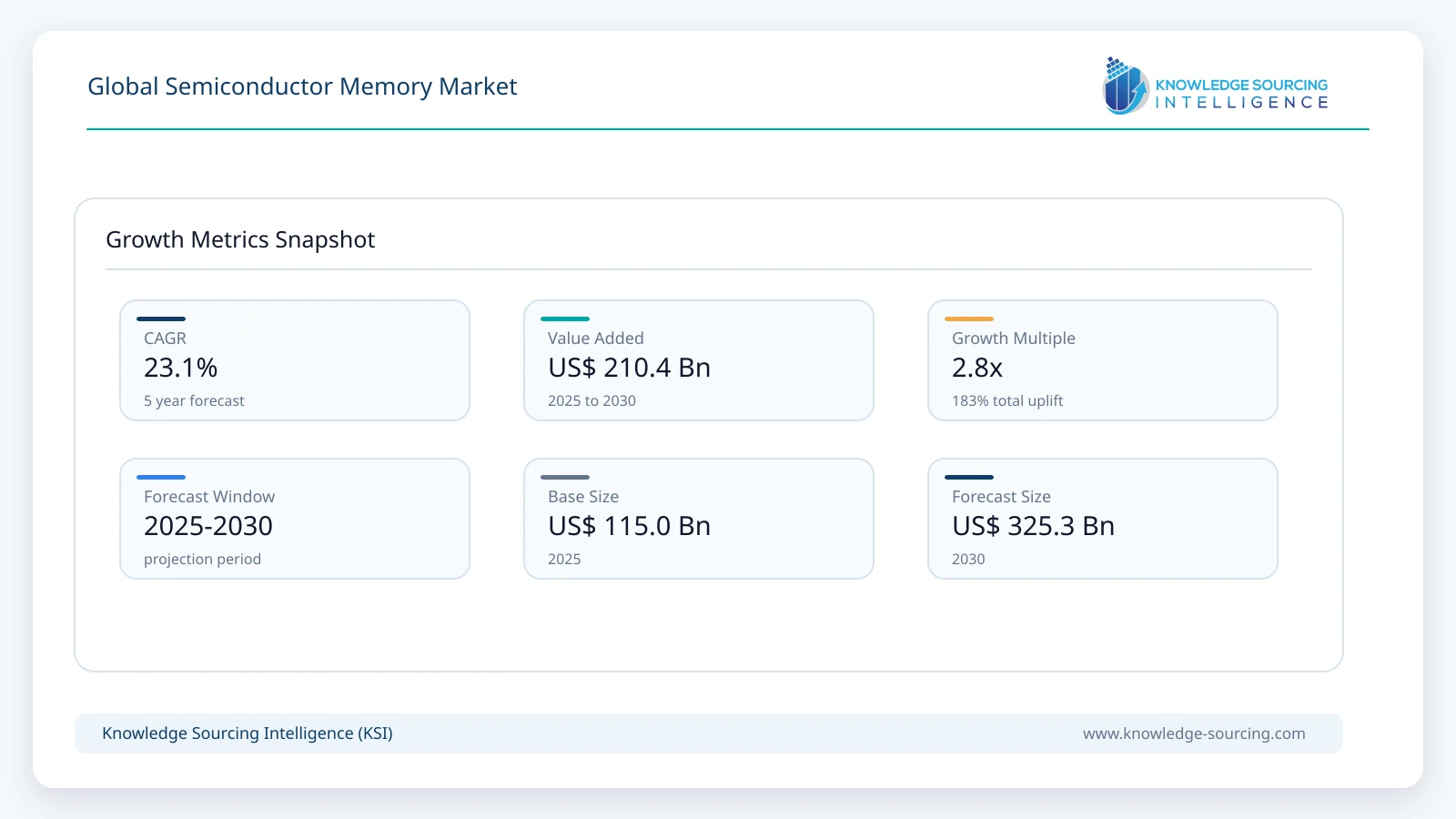

The semiconductor memory market is forecast to grow at a CAGR of 22.98%, reaching USD 398.24 billion in 2031 from USD 141.56 billion in 2026.

Highlights:

- 1Growing investment in artificial intelligence infrastructure is increasing procurement of high-capacity and high-bandwidth semiconductor memory.

- 2DRAM remains the commercially dominant product category because of its essential role in computing, servers, smartphones, and AI processors.

- 3Asia Pacific represents the largest production and consumption hub due to concentrated semiconductor manufacturing capacity and electronics assembly.

- 4Automotive electrification and advanced driver assistance systems are expanding demand for automotive-grade memory qualified under stringent reliability standards.

- 5Government semiconductor manufacturing incentive programs are reshaping investment decisions and regional supply chain diversification.

- 6Competition increasingly depends on manufacturing technology, packaging capability, long-term supply assurance, and product qualification rather than pricing alone.

The semiconductor memory market comprises integrated circuits designed to store digital information for processing, temporary caching, and long-term data retention across electronic systems. It includes volatile memory technologies such as DRAM and SRAM, alongside non-volatile memory technologies including NAND Flash, NOR Flash, and EEPROM. These memory devices form the foundation of computing platforms, mobile devices, enterprise servers, networking infrastructure, industrial automation equipment, connected vehicles, and embedded electronic systems. Demand for semiconductor memory is closely linked to semiconductor production cycles, digital infrastructure investment, and device replacement trends rather than consumer electronics shipments alone.

Purchasing decisions are increasingly influenced by memory density, bandwidth, power efficiency, endurance, reliability, and supply continuity. Original equipment manufacturers (OEMs), cloud service providers, automotive manufacturers, telecommunications equipment vendors, and industrial automation companies are prioritizing long-term supply agreements with qualified memory suppliers to reduce procurement risk following recent semiconductor supply disruptions. Buyers are also evaluating total ownership costs, firmware support, qualification timelines, and product longevity, particularly in automotive and industrial applications where components remain in production for several years.

Industry economics are shaped by substantial capital expenditure requirements, continuous process-node migration, and cyclical pricing. Memory fabrication facilities require multibillion-dollar investments, creating high barriers to entry and reinforcing the dominance of established manufacturers. At the same time, artificial intelligence computing, cloud infrastructure expansion, high-performance computing, and advanced driver assistance systems are changing demand patterns toward higher-capacity and higher-bandwidth memory products. These applications generate stronger value per device than traditional consumer electronics, encouraging suppliers to prioritize premium memory solutions over commodity offerings.

Another defining characteristic of the market is the increasing integration between memory design, controller technologies, packaging innovations, and manufacturing efficiency. Advanced packaging methods, including stacked memory architectures and high-bandwidth memory integration, have become important differentiators for suppliers serving AI accelerators and data center processors. Consequently, competition extends beyond manufacturing scale to engineering capabilities, process technology, ecosystem partnerships, and customer qualification expertise.

Market Drivers

Expansion of Artificial Intelligence and Cloud Computing Infrastructure

Artificial intelligence workloads require substantially greater memory bandwidth and capacity than conventional computing applications. Large language models, inference engines, and AI training clusters consume advanced DRAM and high-performance memory modules capable of supporting parallel processing architectures. Cloud service providers continue expanding hyperscale facilities to accommodate enterprise AI adoption, resulting in higher procurement volumes for enterprise memory solutions.

Memory manufacturers are responding by increasing investments in advanced DRAM technologies, packaging innovations, and production capacity for premium memory products. This shift improves average selling prices while reducing dependence on highly cyclical consumer electronics demand.

Growth in Automotive Electronics Content

Modern vehicles incorporate increasing amounts of semiconductor memory to support infotainment systems, digital instrument clusters, telematics, advanced driver assistance systems, battery management systems, and autonomous driving platforms. Automotive applications require memory components capable of operating under extended temperature ranges with long qualification cycles.

Automotive manufacturers prioritize supplier reliability, functional safety compliance, and guaranteed product availability over several years. These procurement requirements encourage memory suppliers to establish dedicated automotive product portfolios with extended lifecycle support.

Continued Expansion of Enterprise Data Centers

Enterprise digitalization, hybrid cloud adoption, and data-intensive workloads continue driving investments in servers and storage infrastructure. Higher processor core counts require larger memory configurations to maximize computing efficiency and application performance.

Enterprise customers increasingly evaluate energy efficiency alongside memory capacity, as electricity consumption represents a significant operational cost within data centers. Suppliers therefore compete through improved power efficiency and thermal performance in addition to density improvements.

Industrial Automation and Embedded Systems Development

Industrial manufacturers continue integrating sensors, edge computing platforms, robotics, and machine control systems across production facilities. These applications require dependable memory products with extended operating life, resistance to harsh environments, and consistent availability.

Industrial buyers generally avoid frequent component redesigns, creating demand for suppliers capable of maintaining production over extended periods while providing firmware compatibility and technical support.

Market Restraints and Challenges

Cyclical Memory Pricing

Semiconductor memory remains susceptible to supply-demand imbalances that produce substantial price fluctuations. Capacity expansion often precedes periods of oversupply, compressing margins across commodity memory products. Conversely, unexpected demand increases can tighten supply and elevate prices.

These cycles complicate production planning for manufacturers and procurement budgeting for OEMs. Many buyers now diversify suppliers and negotiate longer-term contracts to reduce pricing volatility.

High Manufacturing Capital Requirements

Advanced memory fabrication requires continuous investment in lithography, wafer processing equipment, cleanroom infrastructure, and research and development. Escalating capital intensity limits new market entrants and raises financial risk associated with technology transitions.

Manufacturers increasingly pursue government incentives, strategic partnerships, and phased capacity expansion to improve investment returns while maintaining competitiveness.

Geopolitical and Supply Chain Risks

Semiconductor manufacturing remains geographically concentrated, exposing the market to trade restrictions, export controls, logistics disruptions, and geopolitical uncertainty. Restrictions affecting semiconductor equipment or advanced technology transfers can influence production planning and customer sourcing strategies.

Large buyers are therefore adopting multi-region procurement strategies while governments promote domestic semiconductor manufacturing capabilities to improve supply resilience.

Technology Migration Complexity

Transitioning to smaller process technologies and advanced memory architectures introduces engineering complexity and qualification challenges. Customers in automotive and industrial markets require extensive validation before adopting new memory generations, extending commercialization timelines.

Suppliers mitigate these risks through collaborative development programs, comprehensive qualification testing, and expanded technical support during customer design cycles.

Major Segment Analysis

DRAM

DRAM represents the most commercially important segment because it serves virtually every modern computing platform requiring high-speed working memory. Personal computers, enterprise servers, smartphones, graphics processors, AI accelerators, networking equipment, and industrial computing platforms all depend on DRAM to deliver processing performance.

Demand is increasingly shifting toward premium DRAM solutions optimized for artificial intelligence infrastructure and high-performance computing. Enterprise customers prioritize bandwidth, latency, thermal efficiency, and scalability rather than simply memory capacity. These purchasing criteria support stronger margins than commodity consumer applications.

Competition within DRAM centers on manufacturing efficiency, process technology leadership, packaging innovation, and production scale. Long-term customer relationships are especially important because qualification requirements for servers and enterprise computing platforms involve extensive validation before commercial deployment. Suppliers capable of combining technology leadership with stable production capacity are better positioned to secure multi-year procurement agreements with hyperscale operators and enterprise OEMs.

Commercially, DRAM generates substantial industry revenue because higher-performance configurations command premium pricing while serving expanding AI infrastructure investments worldwide. Continued processor performance improvements are expected to sustain demand for advanced DRAM products throughout the forecast period.

Regional Analysis

North America

North America remains a major demand center driven by hyperscale cloud providers, semiconductor design companies, enterprise computing infrastructure, defense electronics, and advanced automotive development. Government semiconductor manufacturing incentives are encouraging additional fabrication investments and supply chain localization. Buyers increasingly emphasize supply security and long-term sourcing reliability.

Europe

European demand is supported by automotive manufacturing, industrial automation, telecommunications infrastructure, and aerospace applications. Regulatory emphasis on digital sovereignty and semiconductor manufacturing resilience encourages investment in regional semiconductor ecosystems. However, relatively limited domestic memory fabrication capacity continues to create import dependence for many applications.

Asia Pacific

Asia Pacific represents both the largest manufacturing base and the largest consumption region. China, South Korea, Taiwan, and Japan collectively account for substantial semiconductor fabrication, electronics assembly, and consumer electronics production. Strong regional supplier networks, advanced manufacturing capabilities, and government industrial policies reinforce the region's strategic importance. Continued investment in semiconductor fabrication facilities supports long-term production capacity expansion.

Middle East & Africa and South America

These regions primarily represent demand markets rather than manufacturing centers. Telecommunications modernization, digital infrastructure projects, industrial automation, and consumer electronics imports contribute to memory consumption. Growth opportunities exist as governments invest in digital economies and enterprise technology adoption, although local semiconductor manufacturing remains limited.

Competitive Landscape

The semiconductor memory market exhibits a concentrated competitive structure characterized by high capital requirements and substantial technological barriers. Samsung Electronics Co., Ltd., SK hynix Inc., Micron Technology, Inc., Kioxia Holdings Corporation, Western Digital Corporation, Intel Corporation, Winbond Electronics Corporation, Nanya Technology Corporation, Macronix International Co., Ltd., ATP Electronics, and Alliance Memory, Inc. compete across different memory technologies, application segments, and geographic markets.

Competition extends beyond production capacity to manufacturing process leadership, product reliability, packaging innovation, customer qualification expertise, and supply assurance. Suppliers continue strengthening strategic partnerships with processor manufacturers, cloud service providers, automotive OEMs, and industrial equipment companies to secure long-term business. Geographic diversification of manufacturing operations and investment in advanced fabrication technologies remain central competitive priorities.

Recent Developments

March 2026: Samsung Electronics unveiled its HBM4E memory at NVIDIA GTC 2026, while confirming mass production of HBM4 for NVIDIA's Vera Rubin platform, delivering up to 11.7 Gbps performance and showcasing next-generation AI memory solutions.

March 2026: SK hynix showcased its latest AI memory portfolio at Mobile World Congress (MWC) 2026 in Barcelona, highlighting advanced HBM, LPDDR, automotive, and enterprise memory solutions while strengthening collaborations with global mobile industry partners.

February 2026: Samsung Electronics began mass production of its latest high-bandwidth memory generation designed for AI computing platforms. The development strengthens supply capability for expanding AI server deployments.

Regulatory and Policy Environment

Government industrial policy has become an important factor influencing semiconductor memory investment decisions. Semiconductor incentive programs in the United States, European Union, Japan, South Korea, and other economies seek to strengthen domestic manufacturing capacity and reduce dependence on concentrated supply chains.

Export control regulations affecting advanced semiconductor equipment and certain memory technologies influence manufacturing strategies, technology collaboration, and international supply chains. Companies must continuously monitor compliance requirements governing technology transfers and international sales.

Automotive applications require compliance with established quality and reliability standards, while industrial customers often require extensive qualification testing before product approval. Environmental regulations governing chemical handling, emissions, water usage, and manufacturing sustainability also affect fabrication operations and capital investment planning.

Outlook and Strategic Implications

Over the next five years, procurement priorities are expected to continue shifting toward higher-value memory products supporting artificial intelligence, cloud infrastructure, automotive electronics, and industrial computing. These applications provide stronger revenue opportunities than traditional commodity consumer markets while requiring closer technical collaboration between suppliers and customers.

Investment activity is likely to remain concentrated in advanced fabrication facilities, packaging technologies, and manufacturing automation capable of improving yield and production efficiency. Supply chain diversification will continue influencing location decisions for future manufacturing capacity as governments pursue greater semiconductor resilience.

Competitive differentiation will increasingly depend on manufacturing technology, engineering expertise, customer qualification capability, and long-term supply assurance rather than production volume alone. Suppliers that successfully combine advanced memory performance with reliable global manufacturing networks will be positioned to strengthen relationships with enterprise, automotive, and industrial customers.

Despite continuing exposure to pricing cycles, geopolitical uncertainty, and capital intensity, the semiconductor memory market is expected to benefit from sustained investment in artificial intelligence infrastructure, connected devices, enterprise computing, and intelligent industrial systems. These structural demand drivers support continued innovation and strategic investment across the semiconductor memory value chain.

Semiconductor Memory Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 141.56 billion |

| Total Market Size in 2031 | USD 398.24 billion |

| Forecast Unit | Billion |

| Growth Rate | 22.98% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Industry Vertical, Geography |

| Geographical Segmentation | Americas, Europe Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

- DRAM

- NAND Flash

- NOR Flash

- SRAM

- EEPROM

By Industry Vertical

- Consumer Electronics

- IT & Telecommunications

- Automotive

- Industrial

- Enterprise & Data Centers

- Others

By Geography

- Americas

- United States

- Canada

- Brazil

- Others

- Europe, Middle East and Africa

- Germany

- United Kingdom

- France

- Netherlands

- Others

- Asia-Pacific

- China

- Japan

- South Korea

- Taiwan

- Others

Geographical Segmentation

Americas, Europe Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits for the Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

3.2. Analyst View

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

5. SEMICONDUCTOR MEMORY MARKET BY TYPE

5.1. Introduction

5.2. DRAM

5.3. NAND Flash

5.4. NOR Flash

5.5. SRAM

5.6. EEPROM

6. SEMICONDUCTOR MEMORY MARKET BY INDUSTRY VERTICAL

6.1. Introduction

6.2. Consumer Electronics

6.3. IT & Telecommunications

6.4. Automotive

6.5. Industrial

6.6. Enterprise & Data Centers

6.7. Others

7. SEMICONDUCTOR MEMORY MARKET BY GEOGRAPHY

7.1. Americas

7.1.1. United States

7.1.2. Canada

7.1.3. Brazil

7.1.4. Others

7.2. Europe, Middle East and Africa

7.2.1. Germany

7.2.2. United Kingdom

7.2.3. France

7.2.4. Netherlands

7.2.5. Others

7.3. Asia-Pacific

7.3.1. China

7.3.2. Japan

7.3.3. South Korea

7.3.4. Taiwan

7.3.5. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. Samsung Electronics Co., Ltd.

9.2. SK hynix Inc.

9.3. Micron Technology, Inc.

9.4. Kioxia Holdings Corporation

9.5. Western Digital Corporation

9.6. Intel Corporation

9.7. Winbond Electronics Corporation

9.8. Nanya Technology Corporation

9.9. Macronix International Co., Ltd.

9.10. ATP Electronics

9.11. Alliance Memory, Inc.

Navigate

Trusted by the world's leading organizations