Report Overview

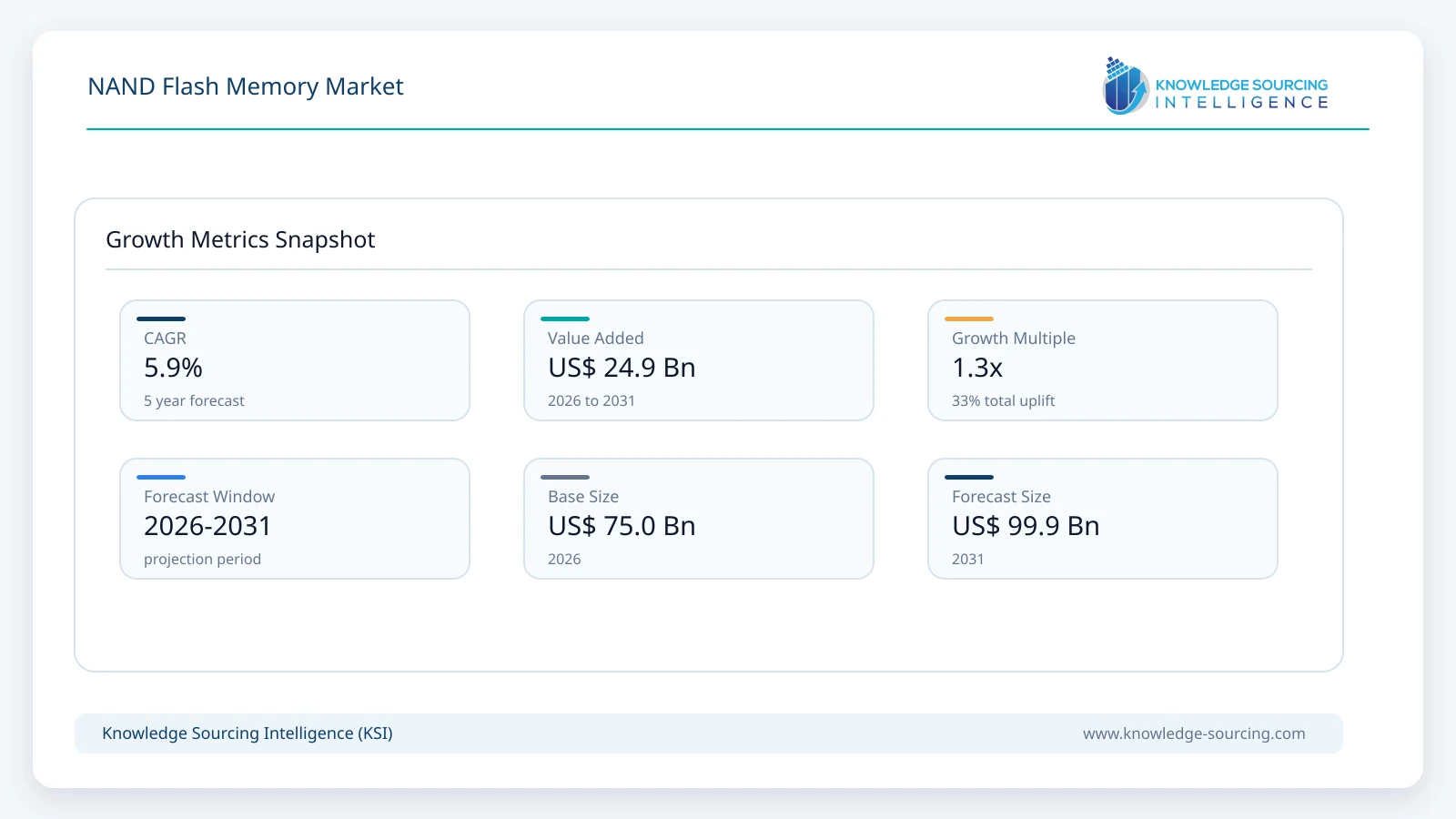

The NAND Flash Memory market is forecast to grow at a CAGR of 5.9%, reaching USD 99.89 billion in 2031 from USD 75.01 billion in 2026.

Highlights:

- 1AI Training IntensificationThe rapid expansion of Large Language Model (LLM) training is surging the demand for high-throughput NVMe SSDs to minimize data latency during GPU processing cycles.

- 2Smartphone Density InflationMobile original equipment manufacturers (OEMs) are steadily increasing base storage configurations to 256GB and 512GB to accommodate local AI inference and high-resolution media capture.

- 33D Scaling AccelerationManufacturers are aggressively adopting multi-stack wafer bonding techniques to achieve layer counts beyond 300, which effectively lowers the cost-per-bit for mass-market storage.

- 4Industrial Edge ProliferationThe rollout of standalone 5G networks is driving the integration of high-endurance NAND into autonomous vehicles and smart factory robotics for real-time edge analytics.

The global NAND flash memory market operates as a foundational pillar of the modern digital economy. The demand drivers are shifting toward high-capacity enterprise SSDs as hyperscale data centers redesign storage hierarchies to support AI training clusters. This transition increases the dependency on 3D NAND technology, which enables vertical cell stacking to bypass the physical density constraints of traditional 2D structures. Regulatory influence, particularly through the U.S. CHIPS Act and evolving export controls, is actively reshaping the geographic distribution of manufacturing capacity. Strategic importance remains high as NAND flash is increasingly viewed as a critical sovereign asset for maintaining technological parity in semiconductor fabrication and data sovereignty.

Market Dynamics

Drivers

Hyperscale Capital Expenditure: Cloud service providers are significantly increasing their procurement of high-density QLC SSDs to support the massive data ingestion requirements of generative AI workloads.

Enterprise Storage Modernization: Traditional hard disk drive (HDD) infrastructures are facing a widespread replacement cycle as enterprises prioritize the superior IOPS and power efficiency of all-flash arrays.

Automotive Electrification: The shift toward Software-Defined Vehicles (SDVs) is creating a new demand layer for automotive-grade NAND to support advanced driver-assistance systems (ADAS) and high-resolution cockpit mapping.

Content Creation Volume: The explosion of 4K and 8K video content across social media platforms is forcing consumer device manufacturers to adopt higher-capacity TLC NAND modules to maintain user experience.

Restraints and Opportunities

Raw Material Price Volatility: Fluctuations in the cost of critical chemicals and gases used in high-aspect-ratio etching processes are creating margin pressures for top-tier memory fabricators.

Export Control Constraints: Expanding trade restrictions on advanced semiconductor manufacturing equipment are limiting the ability of certain regions to transition toward sub-200-layer 3D NAND production.

QLC Endurance Optimization: The inherent endurance trade-offs in Quad-Level Cell technology are providing a massive opportunity for controller manufacturers to develop advanced error correction code (ECC) algorithms.

Sustainability Mandates: Increasing regulatory pressure to reduce the carbon footprint of data centers is driving a demand shift toward ultra-low-power NAND architectures that reduce thermal management costs.

Supply Chain Analysis

The NAND flash supply chain is undergoing a structural realignment as geopolitical tensions force a shift from concentrated production toward regionalized resilience. Silicon wafer production remains the primary upstream constraint, with high-purity chemicals and specialized lithography tools acting as secondary bottlenecks. Fabrication facilities (Fabs) are increasingly adopting "Wafer-on-Wafer" and "Xtacking" methodologies to integrate CMOS logic and NAND arrays separately, which optimizes performance but adds complexity to the assembly and test phase. Downstream, the transition toward proprietary controller development by hyperscalers is bypassing traditional module integrators, allowing for deeper vertical integration. Supply chain actors are currently focusing on diversifying their sourcing of neon and hexafluorobutadiene to mitigate potential disruptions in Eastern Europe and Asia. This regionalization is resulting in higher capital intensity as companies build redundant capacity in North America and Europe to comply with new government subsidy requirements.

Government Regulations

Agency/Regulation | Impact on NAND Flash Market |

U.S. CHIPS and Science Act | Funding is incentivizing domestic production of advanced 3D NAND while prohibiting recipients from expanding high-end capacity in specific foreign jurisdictions. |

EU Chips Act | Regulatory frameworks are streamlining the approval process for "first-of-a-kind" semiconductor facilities to secure European data infrastructure. |

ECHA (REACH) | Restrictions on PFAS (Per- and polyfluoroalkyl substances) are forcing manufacturers to research alternative materials for cooling and etching processes. |

China Integrated Circuit Industry Fund | State-led capital is accelerating the development of domestic 3D NAND stacking technologies to achieve self-sufficiency in enterprise storage. |

Key Developments

July 2026: Kioxia and Sandisk announced the start of production of their 10th-generation 3D BiCS FLASH™ memory at the Kitakami Fab2 facility, introducing their latest high-performance NAND technology utilizing advanced CBA (CMOS directly Bonded to Array) architecture.

April 2026: SK Hynix commenced shipping its PQC21 client SSD, marking the industry's first commercial use of 321-layer QLC NAND technology, specifically designed to enhance AI PC storage performance.

January 2026: Micron Technology announced a US$24 billion investment to expand its Singapore NAND manufacturing campus, adding approximately 700,000 square feet of cleanroom space to strengthen advanced NAND flash production capacity for future AI and enterprise storage demand.

Market Segmentation

By Type

Single-Level Cell (SLC) NAND remains the gold standard for high-reliability industrial and automotive applications. Industrial manufacturers are consistently choosing SLC for mission-critical boot code storage due to its superior cell endurance and temperature resilience. Demand is shifting toward high-density SLC variations as embedded systems integrate more complex operating kernels. This shift is putting pressure on legacy 2D production lines, which are often the only source for these specialized chips. Manufacturers are responding by porting SLC designs to modern 3D processes to maintain cost-competitiveness. The outcome is a bifurcated market where high-margin SLC serves the automotive sector while TLC dominates the high-volume consumer segment.

Triple-Level Cell (TLC) acts as the primary volume driver in the global NAND ecosystem. Consumer electronics OEMs are integrating TLC modules into nearly all mid-to-high range smartphones and laptops. Demand is currently accelerating for 232-layer TLC as the price-per-gigabyte reaches parity with older 128-layer designs. This technological leap is straining existing etching capacities at major fabrication sites. Fabrication leads are increasing their capital investment in high-aspect-ratio (HAR) tools to sustain these stacking trends. TLC is maintaining its structural dominance as the most balanced architecture for general-purpose computing.

By Structure

3D NAND represents the most commercially important segment because it enables significantly higher storage density than conventional planar NAND while reducing the cost per stored bit. By stacking memory cells vertically, manufacturers can increase capacity without proportionally increasing chip size, making 3D NAND the preferred technology for enterprise SSDs, cloud data centers, smartphones, and high-performance computing applications.

Demand is driven by hyperscale cloud operators, enterprise storage vendors, consumer electronics manufacturers, and automotive OEMs requiring high-capacity storage with improved reliability and energy efficiency. Buyers increasingly evaluate suppliers based on endurance, input/output performance, power efficiency, and long-term product availability rather than acquisition cost alone.

Competition within the 3D NAND segment is shaped by layer-count innovation, manufacturing yield, controller integration, firmware optimization, and advanced packaging technologies. Manufacturers capable of scaling production while maintaining consistent quality and competitive pricing are better positioned to secure long-term supply agreements with global OEMs, cloud service providers, and enterprise storage vendors.

By Application

The Smartphone application segment remains the largest single consumer of NAND bits globally. Mobile consumers are demanding larger on-device storage to accommodate high-definition video and generative AI apps. Demand is shifting toward UFS 4.0 and UFS 5.0 interfaces that utilize high-speed TLC NAND. This requirement is forcing smartphone brands to increase their procurement of high-layer-count 3D chips. Memory vendors are prioritizing high-density mobile packages to capture the premium handset market. Smartphones are continuing to act as the primary stabilizer for NAND market cycles.

Solid State Drives (SSDs) are witnessing a structural surge in the enterprise and data center categories. Hyperscale data centers are replacing traditional mechanical drives with high-capacity QLC SSDs to support high-speed data retrieval for AI training. Demand is shifting toward 64TB and 128TB enterprise drives as storage density becomes a critical competitive factor. This volume shift is creating a shortage of specialized high-speed NAND controllers. Controller manufacturers are ramping up production of PCIe Gen 5 and Gen 6 compatible chips. SSDs are becoming the central focus of NAND manufacturers' long-term profitability strategies.

Regional Analysis

North America is maintaining its position as a primary demand center for high-end NAND flash due to the concentration of hyperscale cloud providers and AI research firms. U.S.-based technology giants are aggressively procuring high-density SSDs to build out the next generation of generative AI clusters. Demand is shifting toward domestically produced memory modules as the CHIPS Act begins to influence procurement policies. This shift is forcing global manufacturers to accelerate their facility expansions in states like Idaho and New York. Semiconductor leads are responding by establishing dedicated enterprise storage support teams within the region. North America remains the critical proving ground for PCIe Gen 6 and high-layer-count 3D architectures.

Asia Pacific is functioning as both the largest production hub and the fastest-growing consumer market for NAND flash. China, South Korea, and Taiwan are continuing to dominate the manufacturing landscape, with massive fabrication clusters in Hwaseong, Pyeongtaek, and Hefei. Demand is rising across the region as local smartphone brands and electric vehicle manufacturers integrate higher storage capacities. This growth is attracting increased investment in local memory packaging and testing facilities to shorten supply chains. Regional governments are offering significant tax incentives to attract 300-layer-plus production technology. Asia Pacific is sustaining its role as the global engine for NAND bit growth and consumer demand.

Europe is carving out a specialized niche in the NAND market, focused on automotive-grade and industrial-strength storage solutions. The region's strong automotive manufacturing base is demanding high-endurance flash to support the rollout of Level 3 and Level 4 autonomous driving features. Demand is shifting toward localized supply chains as the EU Chips Act encourages the development of European semiconductor resilience. This trend is putting pressure on traditional Asian suppliers to establish European-based distribution and customization centers. Logistics and quality assurance teams are responding by implementing stricter "zero-defect" protocols for automotive memory. Europe is emerging as the strategic leader in high-reliability and extended-temperature NAND applications.

Competitive Landscape

Samsung Electronics Co., Ltd.

KIOXIA Corporation

Micron Technology, Inc.

SK hynix Inc.

SanDisk Corporation

Solidigm

Yangtze Memory Technologies Co., Ltd. (YMTC)

GigaDevice Semiconductor Inc.

Winbond Electronics Corporation

ATP Electronics, Inc.

Company Profiles

Samsung Electronics Co., Ltd

Samsung is maintaining its leadership by utilizing its massive scale and vertical integration to pioneer the "V-NAND" transition. The company is currently deploying its 9th-generation V-NAND, which utilizes a "double-stack" structure to achieve industry-leading bit density. Demand is shifting toward Samsung's 128TB enterprise SSDs as hyperscalers seek to consolidate their data center footprints. Samsung is responding by repurposing legacy DRAM lines to increase its NAND output in response to the 2026 supply crunch. The company remains the primary setter of market pricing and technological benchmarks.

Micron Technology, Inc

Micron is strategically distinct due to its aggressive pursuit of layer-count leadership and its early adoption of CMOS-under-Array (CuA) architecture. The company is successfully mass-producing 232-layer NAND, which provides a significant footprint advantage for mobile and laptop manufacturers. Demand is shifting toward Micron's high-bandwidth storage solutions as AI edge devices require faster data access. Micron is responding by building new "mega-fabs" in the United States to align with government security requirements. This geographic diversification is positioning Micron as the preferred partner for Western government and enterprise clients.

SK Hynix Inc.

SK Hynix is strategically distinct through its "4D NAND" approach, which integrates the peripheral circuitry under the cell array to maximize wafer efficiency. The company's acquisition of Intel's NAND business (Solidigm) has provided it with a dominant position in the high-density QLC enterprise SSD market. Demand is surging for SK Hynix's specialized AI storage modules that sit adjacent to high-speed memory clusters. The company is responding by prioritizing "zero-capacity" inventory management to maintain high average selling prices. SK Hynix is successfully pivoting from a consumer-focused vendor to an enterprise storage powerhouse.

Analyst View

The NAND flash market is currently transitioning from a commodity-driven cycle to a high-value infrastructure cycle. Structural shortages in 2026 are forcing long-term strategic partnerships between hyperscalers and memory fabricators to ensure AI deployment timelines remain on track.

NAND Flash Memory Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 75.01 billion |

| Total Market Size in 2031 | USD 99.89 billion |

| Forecast Unit | Billion |

| Growth Rate | 5.9% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Structure, Application, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

By Structure

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. NAND FLASH MEMORY MARKET BY TYPE

5.1. Introduction

5.2. Single-Level Cell (SLC)

5.3. Multi-Level Cell (MLC)

5.4. Triple-Level Cell (TLC)

5.5. Quad-Level Cell (QLC)

6. NAND FLASH MEMORY MARKET BY STRUCTURE

6.1. Introduction

6.2. 2D NAND

6.3. 3D NAND

7. NAND FLASH MEMORY MARKET BY APPLICATION

7.1. Introduction

7.2. Smartphones

7.3. Solid-State Drives (SSDs)

7.4. Memory Cards

7.5. Tablets

7.6. Other Applications

8. NAND FLASH MEMORY MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. United States

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Argentina

8.3.3. Others

8.4. Europe

8.4.1. Germany

8.4.2. France

8.4.3. United Kingdom

8.4.4. Spain

8.4.5. Others

8.5. Middle East and Africa

8.5.1. Saudi Arabia

8.5.2. United Arab Emirates

8.5.3. Others

8.6. Asia Pacific

8.6.1. China

8.6.2. India

8.6.3. Japan

8.6.4. South Korea

8.6.5. Indonesia

8.6.6. Thailand

8.6.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Samsung Electronics Co., Ltd.

10.2. KIOXIA Corporation

10.3. Micron Technology, Inc.

10.4. SK hynix Inc.

10.5. SanDisk Corporation

10.6. Solidigm

10.7. Yangtze Memory Technologies Co., Ltd. (YMTC)

10.8. GigaDevice Semiconductor Inc.

10.9. Winbond Electronics Corporation

10.10. ATP Electronics, Inc.

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations