Report Overview

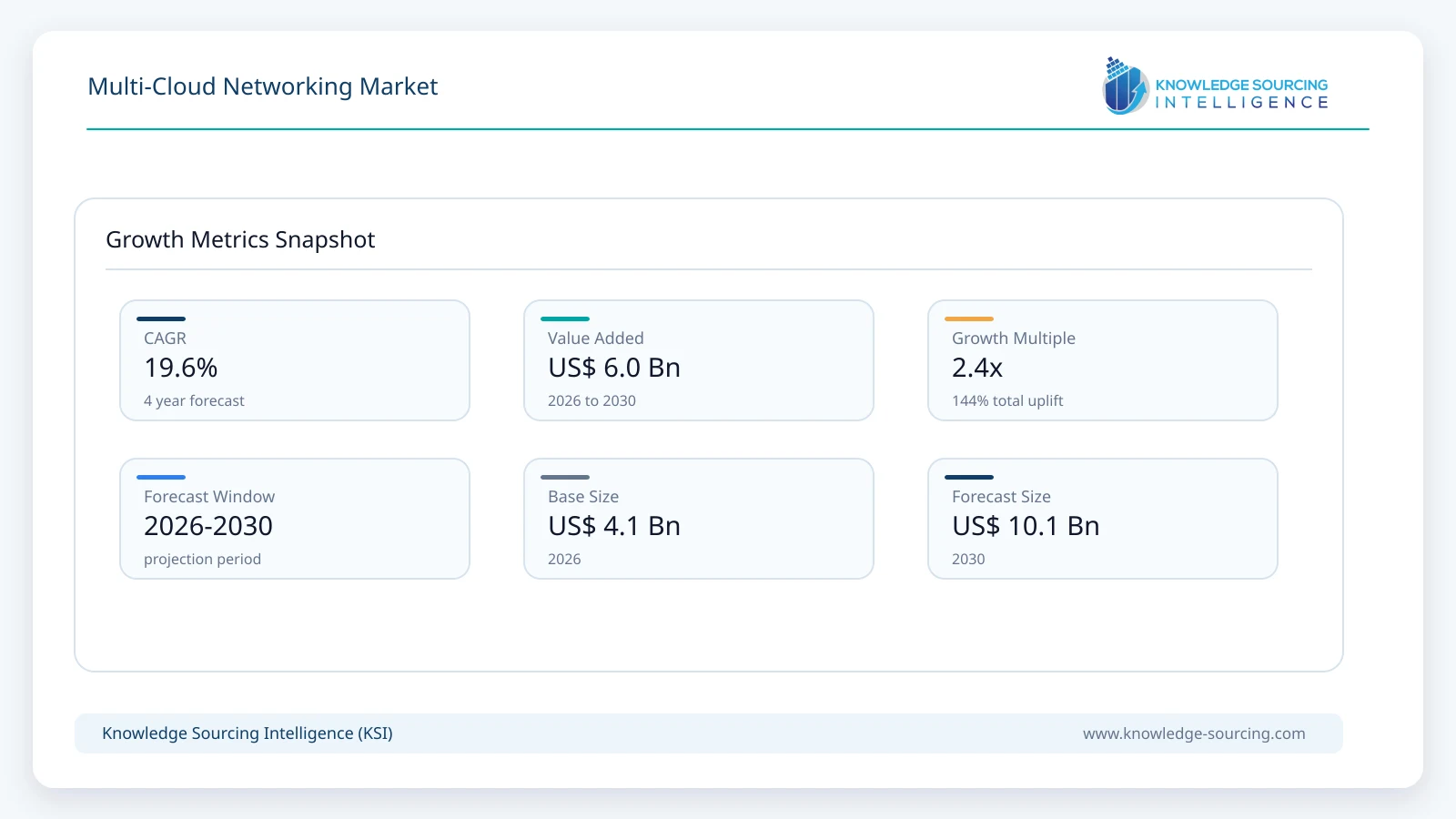

The Multi-Cloud Networking Market is forecast to grow at a CAGR of 19.57%, reaching USD 10.12 billion in 2031 from USD 4.14 billion in 2026.

Highlights:

- 1Data Sovereignty Mandates the Control PlaneRegulatory fragmentation, epitomized by the U.S. DOJ’s Final Rule on bulk sensitive data transfers (2025) and GDPR, directly mandates the adoption of Multi-Cloud Networking Solutions to enforce data locality and consistent policy across disparate global cloud regions.

- 2Security Centralization is the Core ImperativeThe inherent complexity of managing disparate, cloud-native security controls across multiple hyperscalers (AWS, Azure, Google) drives demand for a unified, centralized Solution for network security, exemplified by the growth of distributed cloud firewalls and Zero Trust models.

- 3Large Enterprises Dominate Strategic ProcurementLarge Enterprises constitute the majority of market value, as their high sunk cost in legacy infrastructure and their complex application portfolios necessitate high-cost, high-value Services for seamless, secure Hybrid Cloud migration and operations.

- 4The Rise of Cloud-Native Workloads Accelerates SegmentationThe mainstream adoption of containerization (Kubernetes) and microservices creates a new layer of network complexity, driving demand for specialized, Software-Defined overlay networking technologies that provide L3-L7 policy enforcement at the workload level across clouds.

The Multi-Cloud Networking (MCN) market is a fundamental enabler of modern digital transformation, emerging as the critical control layer atop the infrastructure-as-a-service (IaaS) providers. Enterprises are no longer questioning the shift to cloud, but rather the optimal strategy for leveraging best-of-breed services from hyper-scale providers while mitigating the operational complexity and vendor lock-in that multi-cloud adoption introduces. MCN solutions, which encompass abstracting cloud-native networking constructs into a unified, programmable, and security-focused fabric, are transitioning from a niche requirement for high-tech firms to a core architectural imperative for global Large Enterprises across verticals like BFSI and Healthcare. This market’s value proposition is centered on delivering centralized visibility, consistent security policy, and simplified operations across otherwise siloed public, private, and hybrid cloud environments.

Multi-Cloud Networking Market Analysis

Growth Drivers

The primary growth driver is the non-negotiable requirement for regulatory compliance and risk mitigation. New government mandates on data sovereignty and cross-border data transfer, such as the EU's GDPR and the stringent US DOJ rules on bulk sensitive data (2025), compel Large Enterprises to implement a unified MCN Solution. This technology allows them to geographically segment sensitive data and consistently enforce localized access policies across disparate cloud regions. Furthermore, the inherent complexity of managing multiple, distinct cloud-native network architectures creates substantial operational friction. MCN provides a layer of abstraction and automation, directly reducing the operational expenditure and technical skill requirements associated with multi-cloud management, thereby accelerating enterprise migration to a multi-vendor strategy.

Challenges and Opportunities

A key challenge is the substantial skills gap within enterprise IT departments, particularly in technologically developing geographies. The complex integration of cloud-native APIs, network overlays, and distributed security requires advanced technical expertise, leading to high initial deployment costs and slower adoption among Small and Medium enterprises. This constraint, however, yields a significant opportunity for the Services segment of the market. The high complexity creates sustained demand for premium managed services, consulting, and advanced training (e.g., vendor-specific certifications). Providers that offer a Solution wrapped in simplified, subscription-based managed Services can capture substantial value by offloading the operational burden from the enterprise, positioning themselves as indispensable partners rather than mere technology vendors.

Supply Chain Analysis

The Multi-Cloud Networking market supply chain is fundamentally intangible, focusing on software development and deployment rather than physical logistics. Key production hubs are concentrated in regions with high-density software engineering talent, primarily North America (US) and, increasingly, India and Europe. The supply chain complexity centers on three core dependencies: reliable access to highly skilled network software engineers; continuous integration with the rapidly evolving Application Programming Interfaces (APIs) of the major hyperscalers (AWS, Microsoft, Alphabet); and the intellectual property licensing agreements that underpin the software-defined networking stack. Logistical complexity is limited to licensing delivery and software updates, which are handled via digital distribution, making the supply chain highly resilient but dependent on maintaining the technical integrity and API compatibility of the core Solutions.

Government Regulations

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

United States | DOJ Final Rule Regulating Bulk Sensitive Data Transfers (2025) | Mandates Data Residency Enforcement: The Final Rule restricts or prohibits the transfer/access of certain bulk US sensitive personal data and government-related data to foreign entities/countries of concern. This directly increases demand for Multi-Cloud Networking Solutions with granular, centralized policy enforcement capabilities (e.g., GeoBlocking, real-time data flow analysis) to prove compliance and prevent non-compliant cross-border data movements. |

European Union | General Data Protection Regulation (GDPR) / European Data Protection Board (EDPB) | Drives Consistent Security and Control: GDPR mandates strict controls over the storage and processing of EU citizens' personal data, imposing significant fines for non-compliance. This accelerates the adoption of MCN platforms that provide a consistent security perimeter, robust encryption, and unified data classification across public cloud regions, allowing enterprises to demonstrate legal control over EU data residing in non-EU clouds. |

China | Cybersecurity Law (CSL) and Data Security Law (DSL) / Cyberspace Administration of China (CAC) | Increases Demand for Localized and Segregated Architectures: The CSL and DSL require critical information infrastructure operators (CIIO) to store certain data locally and mandate security assessments for cross-border transfers. This regulatory environment fuels demand for multi-cloud solutions that facilitate localized, segregated public cloud deployments and provide high-performance connectivity between in-country public clouds and private data center resources. |

Multi-Cloud Networking Market Segment Analysis

By Component: Solutions

The Solutions segment, comprising the core software-defined networking (SDN) platform, security modules, and orchestration tools, is the foundational revenue driver of the MCN market. The key growth driver is the urgent need for Operational Consistency and Centralized Control. Enterprises, particularly those using Hybrid Cloud deployments, face systemic challenges in managing disparate routing, visibility, and security tools provided natively by AWS, Azure, and Google. The MCN Solution abstracts these complexities into a single, programmable control plane. This abstraction simplifies operations, enables unified policy application (e.g., consistent IP addressing schemes and Zero Trust models across clouds), and significantly reduces the operational expenditure associated with specialized, multi-vendor certification for network personnel, creating a measurable ROI that accelerates procurement.

By Industry Vertical: BFSI

The BFSI (Banking, Financial Services, and Insurance) sector is a high-value, early-adopter vertical for MCN, driven primarily by the twin mandates of High Resilience and Regulatory Scrutiny. Financial institutions require near-zero downtime and must comply with industry-specific regulations that mandate strict disaster recovery (DR) protocols, such as storing critical data in physically separated, redundant environments. A multi-cloud architecture is the most reliable way to achieve this geo-redundancy and avoid single-vendor outages. Consequently, demand for MCN Solutions in BFSI is propelled by the need to provision high-speed, secure, and fully automated connectivity between primary and failover sites hosted on different cloud providers (e.g., workload active-active across AWS and Azure), which ensures business continuity and satisfies the stringent demands of financial regulators worldwide.

Multi-Cloud Networking Market Geographical Analysis

US Market Analysis (North America)

The US market acts as the global innovation hub and largest consumer of Multi-Cloud Networking, fueled by the presence of the major hyperscalers and a massive, early-adopter population of cloud-native enterprises. The local factor impacting demand is the Convergence of Security and Networking. Stringent US regulations (e.g., those governing sensitive government-related data access) and the prevalence of sophisticated cyber threats compel enterprises to prioritize MCN platforms that embed Zero Trust security, distributed firewalling, and threat intelligence directly into the network fabric, driving high-value demand for Solutions over basic connectivity.

Brazil Market Analysis (South America)

Brazil represents the largest and most dynamic market in South America, where demand for MCN is driven by Economic Resilience and Regulatory Fragmentation. The country’s high interest rates, currency volatility, and evolving data protection laws (LGPD, the Brazilian equivalent of GDPR) compel enterprises to adopt multi-cloud strategies to secure favorable pricing models and hedge against the risks of vendor lock-in with a single cloud provider. This accelerates demand for MCN Services that can ensure LGPD compliance while maintaining efficient, low-latency connectivity across domestic and international public cloud regions for optimized application delivery.

Germany Market Analysis (Europe)

Germany's market is characterized by a strong manufacturing base (Industry 4.0) and an uncompromising focus on Data Sovereignty and Operational Technology (OT) Security. The need for MCN is propelled by the need to integrate geographically distributed, often sensitive OT data from factory floors (Private Cloud/Edge) with public cloud-based analytics platforms. The strict compliance environment stemming from GDPR and national cyber security requirements means German companies seek MCN Solutions that can enforce deterministic data residency policies and extend the Zero Trust model from the corporate network into the public cloud infrastructure.

Saudi Arabia Market Analysis (Middle East & Africa)

The Saudi Arabian market is driven by immense, state-backed investment in digital transformation and Vision 2030 initiatives, focusing on large-scale public cloud adoption. The local factor is the Sovereign Cloud Imperative. The government and large state-owned enterprises are establishing local hyperscaler regions, which creates a compulsory demand for MCN Solutions to facilitate secure, high-performance interconnection between these new local cloud regions and existing international cloud deployments. Demand is highest for Services that enable rapid, compliant workload migration while ensuring adherence to emerging data localization requirements.

China Market Analysis (Asia-Pacific)

The Chinese market is heavily influenced by the Complex Regulatory Environment and Digital Ecosystem Fragmentation. The CSL and DSL require specific data categories to be processed within the mainland, necessitating multi-cloud designs that integrate a China-based cloud presence with global operations. This regulatory constraint drives demand for MCN Solutions capable of providing a high-performance, resilient, and secure connection across the Great Firewall and between disparate global cloud environments, with an emphasis on local compliance for data routing and encryption.

Multi-Cloud Networking Market Competitive Environment and Analysis

The MCN competitive landscape is highly polarized, featuring legacy networking incumbents and disruptive software-centric specialists. The market is defined by the tension between the "big three" hyperscalers, who offer native but siloed networking tools, and third-party vendors who provide the necessary, overarching control plane. Success is determined by the ability to offer a unified, code-driven fabric that provides the security, visibility, and automation lacking in the cloud providers’ fragmented native toolsets.

Cisco Systems, Inc.

Cisco leverages its dominant position in enterprise networking and security to strategically position its MCN offerings (e.g., Cisco Multicloud Defense) as an extension of established on-premises infrastructure. Its strategy centers on providing a consistent policy and operational model from the data center edge to the multi-cloud environment. Key products focus on multi-cloud security and networking, including high-performance cloud routing and a unified security platform that extends familiar perimeter defenses into the cloud. This positioning appeals strongly to Large Enterprises that prioritize integrating their existing Cisco investments and seeking an enterprise-grade, single-vendor accountability model for their entire network footprint.

Aviatrix, Inc.

Aviatrix is a pure-play, software-defined MCN provider focused on creating a consistent, abstraction layer, or "Intelligent Cloud Network," above the native APIs of the major hyperscalers. Its strategic positioning is built on providing a networking and security fabric that delivers enterprise-class features, like High-Performance Encryption, Distributed Cloud Firewall, and Advanced Visibility, that are difficult or impossible to achieve using native cloud constructs alone. Aviatrix targets customers with highly complex, business-critical Multi-Cloud or Hybrid Cloud deployments that require the highest levels of security, operational simplicity, and cross-cloud consistency, making its Solutions an immediate purchase for technically demanding BFSI and IT and Telecom firms.

Alphabet Inc. (Google)

Alphabet Inc. (Google), through its Google Cloud Platform (GCP) and networking portfolio, competes by emphasizing a cloud-native, API-centric approach and leveraging its global network infrastructure. Google’s strategic positioning often focuses on high-performance workloads, advanced AI/ML capabilities, and a developer-friendly environment. Key services, such as their virtual private cloud (VPC) capabilities and specialized networking tools, are designed to natively integrate with their advanced services. While their core offerings are specific to GCP, the company actively engages in partnerships and service enhancements to ensure seamless, low-latency interoperability, particularly for customers prioritizing Data Analytics and cloud-native application development across multiple clouds.

Multi-Cloud Networking Market Developments

July 2026: Lumen Technologies completed its acquisition of Alkira on July 7, 2026, combining Alkira's cloud-native networking platform with Lumen's programmable network to simplify enterprise connectivity across multi-cloud, hybrid cloud, and AI workloads.

June 2026: Cisco unveiled Cisco Cloud Control on June 2, 2026, introducing a unified platform that centralizes networking, security, observability, and AI-driven operations across hybrid and multi-cloud environments through its AgenticOps operating model.

March 2026: Alkira launched the Alkira Connect Partner Program, enabling system integrators, managed service providers, and cloud partners to accelerate multi-cloud networking deployments, AI infrastructure modernization, and enterprise network transformation services.

November 2025: Aviatrix launched its Zero Trust for Workloads product line, extending pervasive cross-cloud runtime enforcement into the application layer for containers and serverless functions. This new offering directly addresses the security gaps introduced by modern cloud-native architectures, driving demand for fine-grained security Solutions.

Multi-Cloud Networking Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 4.14 billion |

| Total Market Size in 2030 | USD 10.12 billion |

| Forecast Unit | Billion |

| Growth Rate | 19.57% |

| Study Period | 2021 to 2030 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2030 |

| Segmentation | Component, Enterprise Size, Deployment Model, Industry Vertical, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

By Enterprise Size

By Deployment Model

By Industry Vertical

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. MULTI-CLOUD NETWORKING MARKET BY COMPONENT

5.1. Introduction

5.2. Solutions

5.3. Services

6. MULTI-CLOUD NETWORKING MARKET BY ENTERPRISE SIZE

6.1. Introduction

6.2. Small and Medium-sized Enterprises (SMEs)

6.3. Large Enterprises

7. MULTI-CLOUD NETWORKING MARKET BY DEPLOYMENT MODEL

7.1. Introduction

7.2. Public Cloud

7.3. Private Cloud

7.4. Hybrid Cloud

8. MULTI-CLOUD NETWORKING MARKET BY INDUSTRY VERTICAL

8.1. Introduction

8.2. BFSI

8.3. IT and Telecom

8.4. Healthcare

8.5. Retail and E-commerce

8.6. Manufacturing

8.7. Government and Public Sector

8.8. Others

9. MULTI-CLOUD NETWORKING MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. United States

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. United Kingdom

9.4.2. Germany

9.4.3. France

9.4.4. Spain

9.4.5. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. United Arab Emirates

9.5.3. Others

9.6. Asia Pacific

9.6.1. China

9.6.2. Japan

9.6.3. India

9.6.4. South Korea

9.6.5. Australia

9.6.6. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. Microsoft Corporation

11.2. Amazon Web Services, Inc.

11.3. Oracle Corporation

11.4. Google Cloud (Alphabet Inc.)

11.5. Cisco Systems, Inc.

11.6. Equinix, Inc.

11.7. Aviatrix, Inc.

11.8. Prosimo Inc.

11.9. Tata Communications Limited

11.10. Hewlett Packard Enterprise Company

12. APPENDIX

12.1. Currency

12.2. Assumptions

12.3. Base and Forecast Years Timeline

12.4. Key Benefits for Stakeholders

12.5. Research Methodology

12.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations