Report Overview

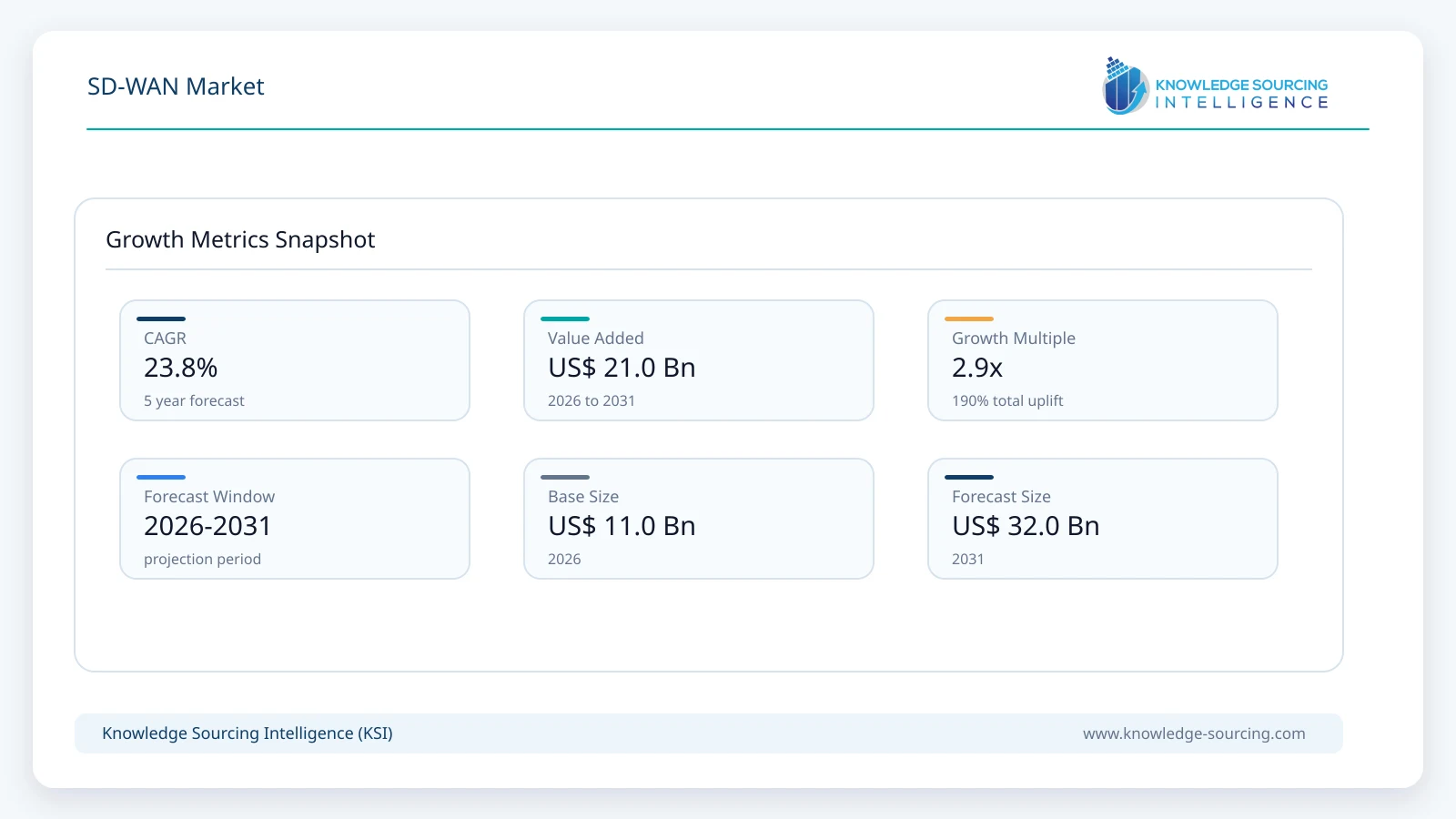

The SD-WAN Market is forecast to grow at a CAGR of 23.75%, reaching USD 32.03 billion in 2031 from USD 11.04 billion in 2026.

Highlights:

- 1Increasing enterprise cloud adoption remains the primary catalyst for SD-WAN deployment worldwide.

- 2Cloud-based SD-WANrepresents the leading deployment segment because it supports distributed enterprise applications and hybrid work environments.

- 3North America remains the largest regional market owing to high cloud adoption, advanced enterprise networking infrastructure, and early technology implementation.

- 4Integration of SD-WAN with SASE and zero-trust security architectures is influencing enterprise procurement strategies.

- 5Government cybersecurity initiatives and data protection regulations continue encouraging investment in secure network infrastructure.

- 6Competition is driven by network performance, integrated security, cloud interoperability, centralized management, and managed service capabilities.

The Software-Defined Wide Area Network (SD-WAN) market comprises software-driven networking solutions that centrally manage and optimize enterprise connectivity across branch offices, data centers, cloud environments, and remote users. SD-WAN separates the network control plane from underlying transport infrastructure, enabling organizations to intelligently route application traffic over broadband, MPLS, LTE, and 5G networks based on performance, security, and business policies. The technology has become a core component of enterprise network modernization as organizations expand cloud adoption, hybrid work environments, and distributed business operations.

Enterprise demand is being driven by the need to improve application performance while reducing dependence on traditional MPLS-based wide area networks. Organizations across banking, healthcare, manufacturing, retail, government, and telecommunications increasingly require secure connectivity between geographically dispersed locations without significantly increasing network operating costs. Procurement decisions are influenced by cloud integration capabilities, embedded cybersecurity functions, centralized management, scalability, application visibility, interoperability with existing infrastructure, and vendor support services.

Cloud migration has fundamentally changed enterprise traffic patterns. Applications that were previously hosted within centralized corporate data centers are now distributed across public cloud, private cloud, and Software-as-a-Service (SaaS) environments. According to the European Union Agency for Cybersecurity (ENISA), secure cloud connectivity and resilient enterprise networking have become essential priorities as organizations continue expanding digital services and cloud infrastructure.

Growing internet usage further strengthens the business case for SD-WAN deployment. According to the International Telecommunication Union (ITU), approximately 5.8 billion people, or about 68% of the global population, were using the internet by the end of 2024. Expanding digital connectivity is increasing enterprise dependence on cloud applications, remote collaboration platforms, and distributed IT infrastructure, all of which require intelligent traffic management and secure network connectivity.

Organizations are also consolidating networking and cybersecurity investments. SD-WAN increasingly serves as the networking foundation for Secure Access Service Edge (SASE) architectures by integrating traffic optimization with firewall, secure web gateway, zero-trust access, and threat protection capabilities. This convergence allows enterprises to simplify infrastructure management while improving security across branch offices and remote work environments.

Market Drivers

Accelerating Enterprise Cloud Migration

Organizations continue migrating enterprise applications from on-premise data centers to public cloud, hybrid cloud, and Software-as-a-Service platforms. Traditional WAN architectures often struggle to support increasing cloud traffic efficiently because they rely on centralized routing models that introduce latency and reduce application performance.

SD-WAN enables direct cloud connectivity while dynamically selecting optimal network paths based on application requirements and real-time network conditions. Enterprises benefit from improved user experience, greater operational flexibility, and reduced dependence on expensive dedicated circuits.

Growth of Hybrid Work and Distributed Enterprises

The expansion of hybrid work has increased demand for secure connectivity between headquarters, branch offices, cloud platforms, and remote employees. Organizations require networking solutions capable of maintaining consistent application performance regardless of user location.

SD-WAN provides centralized policy management and intelligent traffic routing while supporting secure access to cloud applications. Enterprises increasingly consider integrated networking and security capabilities when selecting vendors to simplify network operations and improve workforce productivity.

Increasing Adoption of Secure Access Service Edge (SASE)

Organizations are increasingly integrating SD-WAN with cloud-delivered cybersecurity services to improve network protection and simplify infrastructure management. Secure Access Service Edge combines SD-WAN with firewall-as-a-service, zero-trust network access, secure web gateways, and cloud access security broker capabilities.

According to the U.S. National Institute of Standards and Technology (NIST), zero-trust principles continue gaining importance as organizations protect distributed users, cloud resources, and enterprise applications.

Vendors continue expanding integrated networking and security platforms that reduce operational complexity while strengthening enterprise cybersecurity.

Increasing Network Modernization Investments

Enterprises continue replacing legacy networking infrastructure with software-defined solutions capable of supporting automation, analytics, and centralized policy management. Modern SD-WAN platforms improve network visibility, simplify branch deployment, and reduce operational costs through centralized orchestration.

Telecommunications providers and managed service companies are also expanding SD-WAN offerings to address increasing enterprise demand for managed connectivity solutions across multiple geographic regions.

Market Restraints and Challenges

Complexity of Legacy Network Integration

Many organizations operate hybrid networking environments consisting of legacy routers, MPLS infrastructure, multiple cloud platforms, and various security solutions. Integrating SD-WAN into these environments often requires significant planning, network redesign, and interoperability testing.

Large enterprises frequently adopt phased migration strategies to minimize operational disruption while maintaining business continuity.

Cybersecurity and Data Protection Concerns

Although SD-WAN improves network visibility and security capabilities, organizations remain concerned about protecting sensitive enterprise data across distributed cloud environments. Financial institutions, healthcare providers, and government agencies require compliance with stringent cybersecurity regulations before implementing new networking technologies.

Vendors continue investing in integrated encryption, identity management, zero-trust architectures, and advanced threat detection to address these concerns.

Skills Shortage and Deployment Complexity

Successful SD-WAN implementation requires expertise in networking, cloud architecture, cybersecurity, and application optimization. Organizations lacking experienced IT personnel may face longer deployment timelines and increased dependence on managed service providers.

Suppliers increasingly provide professional services, automation tools, and centralized management platforms that simplify implementation and reduce operational complexity.

Major Segment Analysis

Cloud Deployment

Cloud deployment represents the leading segment within the SD-WAN market because enterprises increasingly operate business applications across multiple public cloud providers, private cloud environments, and Software-as-a-Service platforms. Traditional network architectures often create inefficient traffic routing patterns that reduce application performance and increase operational costs.

Cloud-based SD-WAN enables organizations to establish direct and secure connectivity to cloud workloads while dynamically optimizing application traffic based on latency, bandwidth availability, and business priorities. Enterprises benefit from faster deployment, simplified scalability, centralized management, and reduced dependence on dedicated networking hardware.

Demand is particularly strong among multinational corporations, financial institutions, retailers, healthcare providers, and technology companies operating geographically distributed business locations. Buyers prioritize integrated security capabilities, multi-cloud compatibility, application visibility, automation, and seamless interoperability with existing enterprise infrastructure.

Competition within this segment centers on network performance, security integration, cloud-native architecture, centralized orchestration, artificial intelligence-assisted network analytics, and managed service capabilities. Vendors capable of combining SD-WAN with comprehensive SASE platforms, automation, and global cloud connectivity are expected to maintain stronger competitive positions as enterprises continue modernizing network infrastructure during the forecast period.

Regional Analysis

North America

North America represents the largest regional market for SD-WAN owing to high cloud adoption, mature enterprise networking infrastructure, and widespread implementation of hybrid work models. Organizations across the United States and Canada continue replacing legacy WAN architectures with software-defined solutions that improve application performance and network visibility. Financial institutions, healthcare providers, retailers, and government agencies are major buyers because they operate geographically distributed locations that require secure, centralized network management. Regulatory requirements related to cybersecurity and data protection also encourage investment in integrated networking and security platforms. The region benefits from the presence of leading SD-WAN vendors, managed service providers, and hyperscale cloud operators, accelerating technology adoption across enterprises of all sizes.

Europe

European enterprises continue investing in SD-WAN to support cloud migration while complying with strict cybersecurity and data privacy regulations. Germany, the United Kingdom, France, and Spain remain important markets due to their strong manufacturing, financial services, telecommunications, and public sector industries. Organizations increasingly evaluate SD-WAN platforms based on security integration, automation capabilities, and interoperability with multi-cloud environments. Demand is further supported by enterprise modernization initiatives and increasing adoption of Secure Access Service Edge (SASE) architectures. Procurement decisions typically emphasize compliance with the General Data Protection Regulation (GDPR) and resilience against cyber threats.

Asia Pacific

Asia Pacific is expected to record the fastest expansion during the forecast period as enterprises increase investments in cloud infrastructure, broadband connectivity, and digital business operations. China, India, Japan, South Korea, Indonesia, and Thailand continue expanding enterprise networks across manufacturing, banking, telecommunications, retail, and government sectors. According to the International Telecommunication Union (ITU), Asia accounts for the largest share of global internet users, supporting sustained demand for scalable enterprise networking solutions. Governments across the region are also investing in digital infrastructure and cloud adoption, encouraging enterprises to modernize branch connectivity while improving cybersecurity.

Middle East & Africa and South America

The Middle East is witnessing increasing SD-WAN adoption as governments pursue economic diversification and smart infrastructure initiatives. Saudi Arabia and the UAE continue investing in cloud computing, digital government services, and secure enterprise connectivity. South America, led by Brazil and Argentina, is gradually adopting SD-WAN as organizations modernize branch networks and reduce dependence on traditional MPLS services. Although investment levels remain lower than those of North America and Europe, increasing cloud adoption and managed network services are expected to improve regional demand over the forecast period.

Competitive Landscape

The SD-WAN market is characterized by competition among networking infrastructure vendors, cybersecurity providers, cloud networking specialists, and managed service companies. Vendors differentiate themselves through software functionality, integrated security, centralized orchestration, artificial intelligence-assisted network analytics, cloud interoperability, application visibility, and managed service capabilities.

Companies including Cisco Systems, Broadcom (VMware SD-WAN), Fortinet, Versa Networks, Hewlett Packard Enterprise, Palo Alto Networks, Juniper Networks, Cato Networks, Nokia, Aryaka Networks, and Citrix (Cloud Software Group) continue expanding integrated networking and security portfolios to address enterprise demand for unified network management. Competition has shifted beyond traditional WAN optimization toward comprehensive SASE platforms that combine SD-WAN, zero-trust access, secure web gateways, firewall services, and cloud-delivered security within a single architecture.

Strategic partnerships with telecommunications operators, cloud service providers, and system integrators remain important because many enterprise customers prefer managed SD-WAN services rather than deploying and operating complex network infrastructure independently. Vendors also continue investing in automation, artificial intelligence, and centralized policy management to simplify enterprise network operations across hybrid cloud environments.

Recent Developments

June 2026: Cisco released software fixes for Cisco Catalyst SD-WAN Manager to remediate CVE-2026-20262, an actively exploited vulnerability affecting the SD-WAN management platform, and urged customers to upgrade immediately to protected software releases.

March 2026: Cisco announced that Orange Business certified Cisco Catalyst SD-WAN with Integrated Next-Generation Firewall (NGFW) for its Flexible SD-WAN managed service, enabling integrated networking and security for enterprise branch deployments without additional security appliances.

Regulatory and Policy Environment

The SD-WAN market is influenced by cybersecurity regulations, data privacy requirements, cloud security standards, and critical infrastructure protection policies. Organizations deploying SD-WAN solutions must comply with industry-specific regulations governing network security, encryption, identity management, and protection of sensitive business information.

In the United States, the National Institute of Standards and Technology (NIST) provides cybersecurity guidance through the Cybersecurity Framework and Zero Trust Architecture, both of which influence enterprise network modernization and secure remote access strategies. These frameworks encourage organizations to implement continuous authentication, segmentation, and risk-based access controls across distributed enterprise networks.

Within Europe, the Network and Information Systems Directive (NIS2) and the General Data Protection Regulation (GDPR) require many organizations operating essential and digital services to strengthen cybersecurity governance, incident reporting, and protection of personal data. These regulatory requirements encourage investment in secure networking technologies capable of providing centralized policy enforcement, encryption, and network visibility.

Governments across Asia Pacific and the Middle East continue promoting national digital infrastructure, cloud adoption, and cybersecurity modernization through public investment programs and regulatory initiatives. As enterprises increasingly migrate mission-critical workloads to cloud environments, compliance requirements are expected to remain an important factor influencing SD-WAN procurement decisions.

Outlook and Strategic Implications

Between 2026 and 2031, enterprise investment is expected to focus on unified networking platforms that combine SD-WAN, cloud connectivity, artificial intelligence, automation, and integrated cybersecurity. Organizations are moving away from isolated networking products toward platforms capable of supporting distributed users, multi-cloud environments, Internet of Things deployments, and edge computing through centralized policy management.

Procurement strategies will increasingly prioritize operational simplicity, cloud-native architecture, application visibility, zero-touch deployment, and embedded security rather than standalone network connectivity. Large enterprises are expected to expand managed SD-WAN adoption to reduce operational complexity, while small and medium-sized enterprises will seek subscription-based solutions that minimize upfront infrastructure investment.

Competition is likely to intensify as networking vendors, cybersecurity companies, telecommunications providers, and cloud platform operators continue integrating networking and security capabilities into unified SASE platforms. Artificial intelligence-assisted network operations, predictive analytics, automated policy optimization, and improved application performance monitoring will become important differentiators among vendors.

Potential risks include evolving cybersecurity threats, integration challenges within legacy enterprise environments, regulatory changes, and shortages of skilled networking professionals. Despite these challenges, continued cloud migration, hybrid work adoption, enterprise digital infrastructure investment, and increasing demand for secure distributed connectivity are expected to support sustained commercial opportunities for SD-WAN providers throughout the 2026 to 2031 forecast period.

SD-WAN Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 11.04 billion |

| Total Market Size in 2031 | USD 32.03 billion |

| Forecast Unit | Billion |

| Growth Rate | 23.75% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Deployment, Enterprise Size, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Deployment

By Enterprise Size

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. SD-WAN MARKET BY DEPLOYMENT

5.1. Introduction

5.2. Cloud

5.3. On-Premise

5.4. Hybrid

6. SD-WAN MARKET BY ENTERPRISE SIZE

6.1. Introduction

6.2. Small and Medium Enterprises (SMEs)

6.3. Large Enterprises

7. SD-WAN MARKET BY END-USER

7.1. Introduction

7.2. BFSI

7.3. IT & Telecommunications

7.4. Healthcare

7.5. Retail

7.6. Manufacturing

7.7. Government

7.8. Education

7.9. Others

8. SD-WAN MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Deployment

8.2.2. By Enterprise Size

8.2.3. By End-User

8.2.4. By Country

8.2.4.1. USA

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Deployment

8.3.2. By Enterprise Size

8.3.3. By End-User

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Deployment

8.4.2. By Enterprise Size

8.4.3. By End-User

8.4.4. By Country

8.4.4.1. Germany

8.4.4.2. France

8.4.4.3. United Kingdom

8.4.4.4. Spain

8.4.4.5. Others

8.5. Middle East and Africa

8.5.1. By Deployment

8.5.2. By Enterprise Size

8.5.3. By End-User

8.5.4. By Country

8.5.4.1. Saudi Arabia

8.5.4.2. UAE

8.5.4.3. Others

8.6. Asia Pacific

8.6.1. By Deployment

8.6.2. By Enterprise Size

8.6.3. By End-User

8.6.4. By Country

8.6.4.1. China

8.6.4.2. India

8.6.4.3. Japan

8.6.4.4. South Korea

8.6.4.5. Indonesia

8.6.4.6. Thailand

8.6.4.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Cisco Systems, Inc.

10.2. Broadcom Inc. (VMware SD-WAN)

10.3. Fortinet, Inc.

10.4. Versa Networks, Inc.

10.5. Hewlett Packard Enterprise

10.6. Palo Alto Networks, Inc.

10.7. Juniper Networks, Inc.

10.8. Cato Networks Ltd.

10.9. Nokia Corporation

10.10. Aryaka Networks, Inc.

10.11. Citrix Systems, Inc. (Cloud Software Group)

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base Year and Forecast Period

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations