Report Overview

Semiconductor Manufacturing Material Market Size:

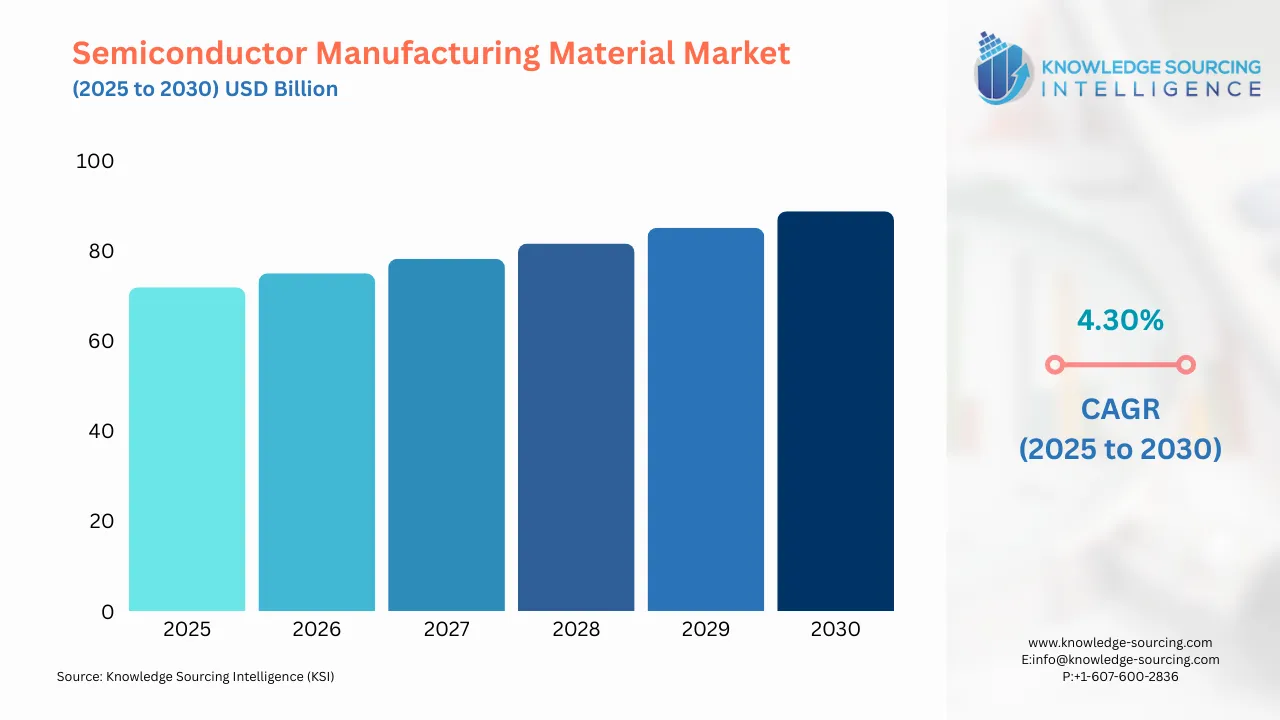

The Semiconductor Manufacturing Material Market is expected to grow from US$71.890 billion in 2025 to US$88.749 billion in 2030, at a CAGR of 4.30%.

Highlights:

- 1Increasing consumer electronics demandis driving growth in semiconductor manufacturing materials.

- 2Growing IoT and AI adoptionis boosting need for advanced semiconductor materials.

- 3North Americais leading the semiconductor material market with strong innovation.

- 4Advancing 5G technologyis fueling demand for high-performance manufacturing materials.

- 5Rising automotive sectoris enhancing the use of semiconductors and packaging materials.

- 6Expanding government investmentsare supporting domestic semiconductor material production.

- 7Strengthening R&D initiativesis promoting innovative materials for semiconductor manufacturing.

Advancements in materials and fabrication techniques have prompted a shift in the semiconductor industry away from inflexible substrates towards more adaptable options such as plastic materials and paper. The miniaturization of advanced material manufacturing has increased the need for new and innovative manufacturing materials in the projected period. This transition towards flexible substrates has given rise to a multitude of devices, including but not limited to light-emitting diodes, solar cells, and transistors.

Semiconductor Manufacturing Material Market Growth Drivers:

Increasing demand for end-user industries

The increasing demand for consumer electronics is one of the major reasons propelling the semiconductor manufacturing material industry in the forecast period. Companies are adding new and developed products to their production line, which are equipped with technologies such as the Internet of Things (IoT), and various end-user industries are adopting the use of advanced consumer electronic products for optimal operation. The increasing development of IoT technologies such as NB-IoT and Cat-M, which primarily consist of wide-area cases, is one of the reasons pushing the semiconductor manufacturing material market in an upward direction. Moreover, in countries such as China, where automotive manufacturing is done heavily, the consumption of such material is increasing, which is increasing the semiconductor manufacturing materials demand.

Increasing investments

According to the Semiconductor Industry Association, the Chinese semiconductor industry is investing large sums in CAPEX, that is, funds used by companies to acquire, upgrade, or maintain their assets. As per the above data, in 2021, Chinese CAPEX companies invested US$12.3 billion, which increased to US$15.3 billion in 2022. The increasing demand for manufacturing facilities and the growing need for semiconductors in the consumer electronics industry and the automobile industry are pushing the semiconductor manufacturing material market in the projected period.

Semiconductor Manufacturing Material Market Geographical Outlook:

North American semiconductor manufacturing market is anticipated to propel

The bolstering growth for semiconductor manufacturing material is fueled by its pivotal role in enabling technological advancements and innovation across various industries, including electronics, telecommunications, automotive, and healthcare. The region is further segmented into the USA, Canada, and Mexico. The United States is expected to hold a substantial share of the semiconductor manufacturing material industry, strongly influenced by increasing demand for high-performance semiconductors for emerging technologies like 5G, artificial intelligence, and electric vehicles, as well as government support for domestic semiconductor production. The market in Canada is expected to witness significant growth driven by a combination of factors, including a thriving technology sector, increased investment in research and development, and a focus on sustainable semiconductor production practices.

The United States is anticipated to be the fastest-growing country in the North American region

The increasing demand for cutting-edge technologies, such as 5G, artificial intelligence, and the Internet of Things (IoT), has created a strong need for advanced semiconductor materials. These materials are essential for developing faster, more efficient, and smaller electronic components to power these technologies. For example, in February 2023, Transcelestial received a $10 million funding injection to enhance laser technology, facilitating the advancement of internet infrastructure in both Asia and the United States. The U.S. government has recognized the importance of semiconductor manufacturing to national security and economic competitiveness. Initiatives like the CHIPS Act of 2022 (Creating Helpful Incentives to Produce Semiconductors for America) have provided financial incentives and funding for semiconductor research, development, and domestic production. This support has encouraged investments from both the public and private sectors.

Continuous research and development in the United States

The USA is at the forefront of semiconductor innovation, with many leading semiconductor companies and research institutions located in the country. Continuous research and development efforts have led to the creation of new materials, manufacturing processes, and semiconductor designs, further driving growth in the sector. For instance, in September 2023, the U.S. National Science Foundation revealed 24 research and educational initiatives, backed by a $45.6 million investment, which includes contributions from the "CHIPS and Science Act of 2022." These projects aim to accelerate advancements in semiconductor technology, manufacturing, and workforce development. The NSF Future of Semiconductors (FuSe) program supports these initiatives through a collaborative effort involving NSF and four corporations: Ericsson, IBM, Intel, and Samsung.

Growth in the USA semiconductor industry

In 2021, the U.S. semiconductor industry made a significant contribution to the Gross Value Added (GVA) to GDP, with a total of $277 billion. This comprised direct GVA of $96.1 billion, indirect GVA of $85.6 billion, and induced GVA of $95.3 billion. This robust performance of the semiconductor industry reflects its integral role in the U.S. economy. The substantial GVA underscores the significance of the semiconductor manufacturing material market in the USA, as the industry relies heavily on advanced materials and technologies to maintain its growth and economic impact, showcasing the close interdependence between the two sectors in driving technological innovation and economic progress.

Semiconductor Manufacturing Material Market Key Developments:

October 2025: Applied Materials (AMAT) launched next-gen manufacturing systems, including the Centura Xtera Epi System, enabling void-free, uniform epitaxial layers for advanced logic nodes (2 nm/GAA), a key advance in epitaxial material deposition.

October 2025: Applied Materials also introduced the PROVision 10 eBeam Metrology System, offering sub-nanometer resolution metrology for complex 3D chips and packaging, a key support system for advanced materials layers (epi, deposition, interconnect) in next-gen semiconductors.

April 2025: Linde plc announced it will build and operate an eighth on-site air separation unit at Samsung Electronics’s Pyeongtaek semiconductor complex to expand the supply of ultra-high-purity specialty/process gases (N2, O2, Ar, H2), critical for wafer fabrication, etching, cleaning, and other material-sensitive steps.

List of Top Semiconductor Manufacturing Material Companies:

Shin-Etsu Chemical Co., Ltd.

SUMCO Corporation

BASF SE

JSR Corporation

Linde plc

Semiconductor Manufacturing Material Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2025 | USD 71.890 billion |

| Total Market Size in 2030 | USD 88.749 billion |

| Forecast Unit | Billion |

| Growth Rate | 4.30% |

| Study Period | 2020 to 2030 |

| Historical Data | 2020 to 2023 |

| Base Year | 2024 |

| Forecast Period | 2025 – 2030 |

| Segmentation | Material Type, Application, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Semiconductor Manufacturing Material Market Segmentation:

By Material Type

Wafer/Substrate Materials

Photoresists & Ancillary Materials

Chemical Materials

Specialty Gases

Metals & Alloys

Dielectric & Insulating Materials

Packaging Materials

By Application

Front-End of Line (FEOL)

Back-End of Line (BEOL)

Packaging

Assembly & Testing

By End-User

Consumer Electronics

Automotive Electronics

Industrial Automation

Telecommunications

Healthcare & Medical Devices

Aerospace & Defense

Data Centers & Cloud Infrastructure

Others

By Geography

Americas

Europe, Middle East and Africa

Asia Pacific

Our Best-Performing Industry Reports:

Market Segmentation

By Material Type

By Application

By End-user Industry

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. SEMICONDUCTOR MANUFACTURING MATERIAL MARKET BY MATERIAL TYPE

5.1. Introduction

5.2. Wafer/Substrate Materials

5.3. Photoresists & Ancillary Materials

5.4. Chemical Materials

5.5. Specialty Gases

5.6. Metals & Alloys

5.7. Dielectric & Insulating Materials

5.8. Packaging Materials

6. SEMICONDUCTOR MANUFACTURING MATERIAL MARKET BY APPLICATION

6.1. Introduction

6.2. Front-End of Line (FEOL)

6.3. Back-End of Line (BEOL)

6.4. Packaging

6.5. Assembly & Testing

7. SEMICONDUCTOR MANUFACTURING MATERIAL MARKET BY END-USER INDUSTRY

7.1. Introduction

7.2. Consumer Electronics

7.3. Automotive Electronics

7.4. Industrial Automation

7.5. Telecommunications

7.6. Healthcare & Medical Devices

7.7. Aerospace & Defense

7.8. Data Centers & Cloud Infrastructure

7.9. Others

8. SEMICONDUCTOR MANUFACTURING MATERIAL MARKET BY GEOGRAPHY

8.1. Introduction

8.2. Americas

8.2.1. USA

8.2.2. Others

8.3. Europe, Middle East and Africa

8.3.1. Germany

8.3.2. France

8.3.3. United Kingdom

8.3.4. Others

8.4. Asia Pacific

8.4.1. China

8.4.2. South Korea

8.4.3. Japan

8.4.4. Taiwan

8.4.5. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Shin-Etsu Chemical Co., Ltd.

10.2. SUMCO Corporation

10.3. BASF SE

10.4. JSR Corporation

10.5. Linde plc

10.6. Tokyo Ohka Kogyo Co., Ltd.

10.7. Showa Denko Materials Co., Ltd.

10.8. DuPont de Nemours, Inc.

10.9. Sumitomo Chemical Co., Ltd.

10.10. Indium Corporation

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key benefits for the stakeholders

11.5. Research Methodology

11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations