Report Overview

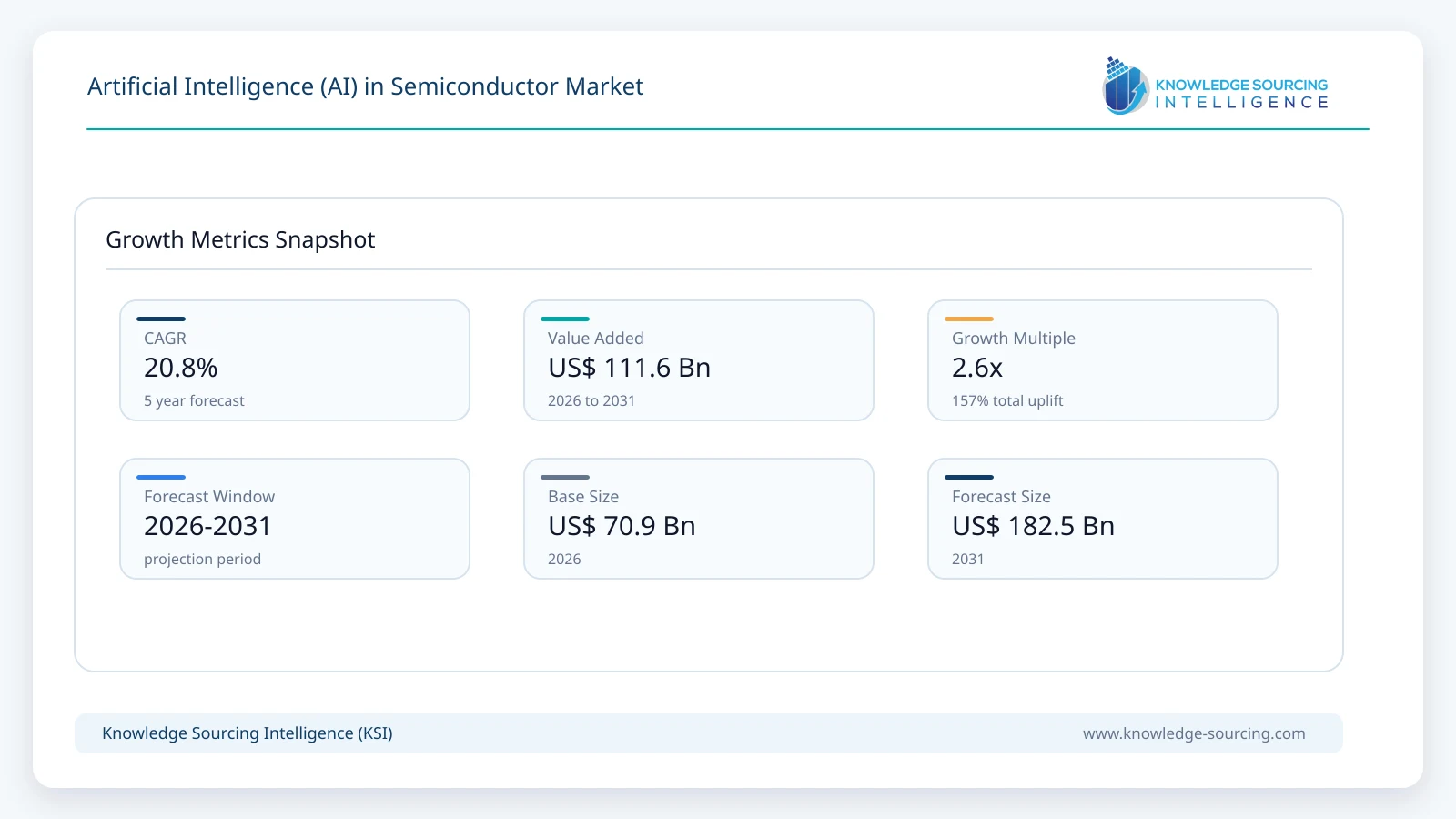

The global Artificial Intelligence (AI) in Semiconductor market is forecast to grow at a CAGR of 20.8%, reaching USD 182.54 billion in 2031 from USD 70.90 billion in 2026.

Highlights:

- 1Largest End-UserHyperscale data center operators dominate demand, as the requirements for training complex LLMs drive the purchase of high-performance GPUs and HBM, causing supply tightness for other consumer electronics.

- 2Regulatory ImpactGeopolitical export controls on advanced AI chips and lithography equipment have forced a fragmentation of global supply chains, increasing operational costs while incentivizing domestic manufacturing in non-traditional regions.

- 3Regional LeaderNorth America continues to lead in architectural design and R&D, while the Asia-Pacific region maintains dominance in high-volume back-end assembly, testing, and advanced packaging, creating a high degree of inter-regional dependency.

- 4Technology TransitionThe industry is moving from monolithic chip design to heterogeneous integration (chiplets/3D stacking) to overcome the limits of reticle size and thermal management, directly impacting current assembly and packaging capacities.

- 5Pricing SensitivityMemory components, particularly HBM, are experiencing extreme price volatility due to supply constraints, forcing a shift in bill-of-materials management for device manufacturers who are now prioritizing supply security over cost reduction.

The semiconductor industry is currently navigating a period of unprecedented expansion, primarily driven by the systemic requirement for AI compute capacity. Demand is no longer tethered to a single vertical; it is distributed across hyperscale cloud infrastructure, industrial automation, autonomous automotive systems, and consumer edge devices. This breadth of demand has decoupled the semiconductor market from historical boom-bust cycles, creating a more resilient, albeit constrained, growth trajectory. Dependency on AI-ready hardware has reached a critical threshold, where lack of access to specific high-performance chips, particularly those required for training Large Language Models (LLMs), directly limits organizational and national competitiveness.

Technological evolution is moving beyond simple process node shrinks toward heterogeneous integration and advanced packaging techniques like CoWoS (Chip-on-Wafer-on-Substrate). As Moore’s Law encounters physical and economic scaling limits, the industry is increasingly reliant on architectural innovation, specifically chiplets, to maintain the pace of performance improvement. Sustainability has transitioned from a corporate social responsibility metric to an operational necessity; as data centers reach gigawatt-scale requirements, "performance-per-watt" has become the primary competitive metric for chip designers and foundries.

Regulatory influence is profound. Governments in North America, Europe, and Asia are treating semiconductor manufacturing as a component of national security. Policies such as the U.S. CHIPS Act and India’s Semiconductor Mission 2.0 prioritize the reshoring of advanced manufacturing and the development of secure domestic supply chains. These regulatory frameworks are influencing where fabs are built and which organizations receive capital, thereby recalibrating global production concentration.

MARKET DYNAMICS

Market Drivers

Data Center Infrastructure Expansion: The continuous scale-up of hyperscale data centers necessitates high-density, AI-optimized compute, creating consistent long-term demand for accelerators that general-purpose CPUs cannot satisfy.

Edge AI Adoption: The migration of inference capabilities from the cloud to the device (Edge AI) is driving demand for low-power, high-efficiency processors in automotive, IoT, and industrial sectors, widening the market reach of AI-specific silicon.

Regulatory Reshoring Initiatives: Government subsidies for domestic semiconductor production are lowering the barrier to entry for new fab construction, increasing total global capacity, though this adds complexity to supply chain integration and workforce skilling.

Industrial Automation Demand: The integration of embodied AI and robotics in manufacturing requires specialized real-time processing silicon, which is driving a structural shift in the demand for industrial microcontrollers and neural processing units.

Market Restraints and Opportunities

Energy and Sustainability Challenges: High-performance AI chips generate significant thermal load; data centers are reaching the limits of power grid capacity, which may act as a physical ceiling for the continued deployment of power-hungry training clusters.

Supply Chain Chokepoints: Advanced packaging and lithography equipment (EUV) represent critical single points of failure in the global supply chain, where even minor geopolitical or logistical disruptions cause outsized delays in chip delivery.

Regulatory Compliance Costs: New sustainability-linked regulations, such as the EU Digital Product Passport, increase administrative and technical overhead for semiconductor firms, forcing investment in traceability rather than just performance.

Emerging Market Potential: Developing nations with strategic initiatives to build domestic chip-design talent and manufacturing capacity present opportunities for decentralized supply chain nodes, reducing reliance on single-country production hubs.

RAW MATERIAL AND PRICING ANALYSIS

The pricing of semiconductors is heavily influenced by the availability of high-purity raw materials, including neon gas, photoresists, and specialized silicon wafers. In 2026, the supply chain for these materials remains tight due to the rapid scaling of HBM production and 3nm/2nm fabrication requirements. The energy intensity of the fabrication process, specifically the use of ultrapure water and extreme ultraviolet (EUV) systems, has made the cost structure of chips sensitive to regional energy pricing. As foundries pass on these inflationary pressures, manufacturers are shifting toward "value-based" pricing models for AI silicon, where margins are protected by the scarcity of high-performance compute. Oversupply concerns persist only in legacy nodes, while the supply for leading-edge AI nodes remains structurally constrained.

SUPPLY CHAIN ANALYSIS

Production concentration remains a critical risk factor. While design is global, high-volume, advanced-node fabrication is concentrated in East Asia. Recent developments in 2026 indicate a shift toward integrated manufacturing strategies, where hyperscalers and equipment makers are forming deeper partnerships with foundries to secure capacity. Energy-intensity requirements for large-scale fabrication facilities require proximity to reliable, renewable-heavy power grids, which is now a decisive factor in regional risk exposure and fab site selection.

Transportation of these chips is increasingly sensitive; high-value AI hardware is frequently prioritized for air freight to avoid the volatility of ocean logistics, particularly when navigating regions subject to geopolitical export controls. The industry is moving toward "digital twin" technology to simulate and monitor these supply chains, aiming to identify potential bottlenecks before they manifest in finished product inventory.

GOVERNMENT REGULATIONS

Jurisdiction | Key Regulation / Agency | Market Impact Analysis |

Europe | EU Digital Product Passport | Increases traceability requirements, raising compliance costs but promoting product lifecycle sustainability. |

United States | CHIPS and Science Act | Accelerates domestic fab construction; creates a "made-in-USA" premium for critical AI infrastructure. |

Global | Export Control Frameworks | Limits the transfer of leading-edge AI silicon to specific markets, driving regional divergence in AI model performance. |

KEY DEVELOPMENTS

June 2026: AMD announced the next generation of its Instinct AI accelerator portfolio, expanding support for large-scale generative AI workloads and strengthening competition in the AI semiconductor ecosystem.

May 2026: Intel introduced new Gaudi AI accelerator roadmap updates and advanced AI infrastructure solutions aimed at improving semiconductor-based AI training and inference capabilities across enterprise and cloud environments.

April 2026: TSMC unveiled its A13 process technology, delivering improved performance, power efficiency, and logic density for AI processors, high-performance computing chips, and next-generation semiconductor applications.

March 2026: IBM and Lam Research announced a five-year collaboration to develop sub-1nm semiconductor technologies, accelerating AI-driven chip innovation through advanced logic scaling and manufacturing research.

January 2026: NVIDIA launched its Rubin AI platform, introducing next-generation AI GPUs and the Vera Rubin architecture designed to significantly increase AI training and inference performance for hyperscale data centers.

January 2026: Intel launched the Core Ultra Series 3 (Panther Lake), the first AI PC platform built on the Intel 18A node, delivering 50 NPU TOPS for edge and client AI.

January 2026: Qualcomm unveiled the Snapdragon X2 Plus for PCs and the Dragonwing IQ10 robotics stack, featuring an 80 TOPS NPU designed specifically for "Physical AI" and humanoid systems.

MARKET SEGMENTATION

By Chip Type: Graphics Processing Units (GPUs)

GPUs remain the primary hardware for training large-scale AI models. Their architecture, which relies on thousands of small, efficient cores, is uniquely suited for parallel computation, a requirement for the matrix multiplications central to deep learning. The necessity for sustained high-bandwidth performance drives this demand. As models grow in complexity, the limitation has shifted from core count to memory bandwidth, necessitating the pairing of GPUs with high-bandwidth memory (HBM). This integration allows GPUs to process massive datasets without frequent bottlenecks, making them the standard for data centers. However, their high power consumption remains a challenge, prompting shifts toward "optimized" GPU versions that sacrifice marginal performance for lower thermal output.

By Application: AI Inference

Inference is the phase where trained AI models are deployed to make predictions or decisions. In recent years, inference demand is surging as organizations move beyond the experimentation phase. Unlike training, which occurs in centralized clusters, inference is increasingly shifting toward edge devices (laptops, industrial sensors, autonomous cars). This shift requires specialized chips optimized for low latency and high energy efficiency rather than raw training throughput. As companies embed AI into products, the demand for inference-specific ASICs is growing, as they provide a better performance-per-watt ratio for fixed-function workloads compared to general-purpose GPUs, directly addressing the cooling and power constraints of edge environments.

By End-Use: Automotive

The automotive sector is undergoing a transition to software-defined vehicles, driving an immense demand for high-performance SoCs. Centralized computer architectures now consolidate functions, from seat controls to autonomous navigation, requiring robust, safety-certified AI chips that can operate in constrained thermal conditions.

REGIONAL ANALYSIS

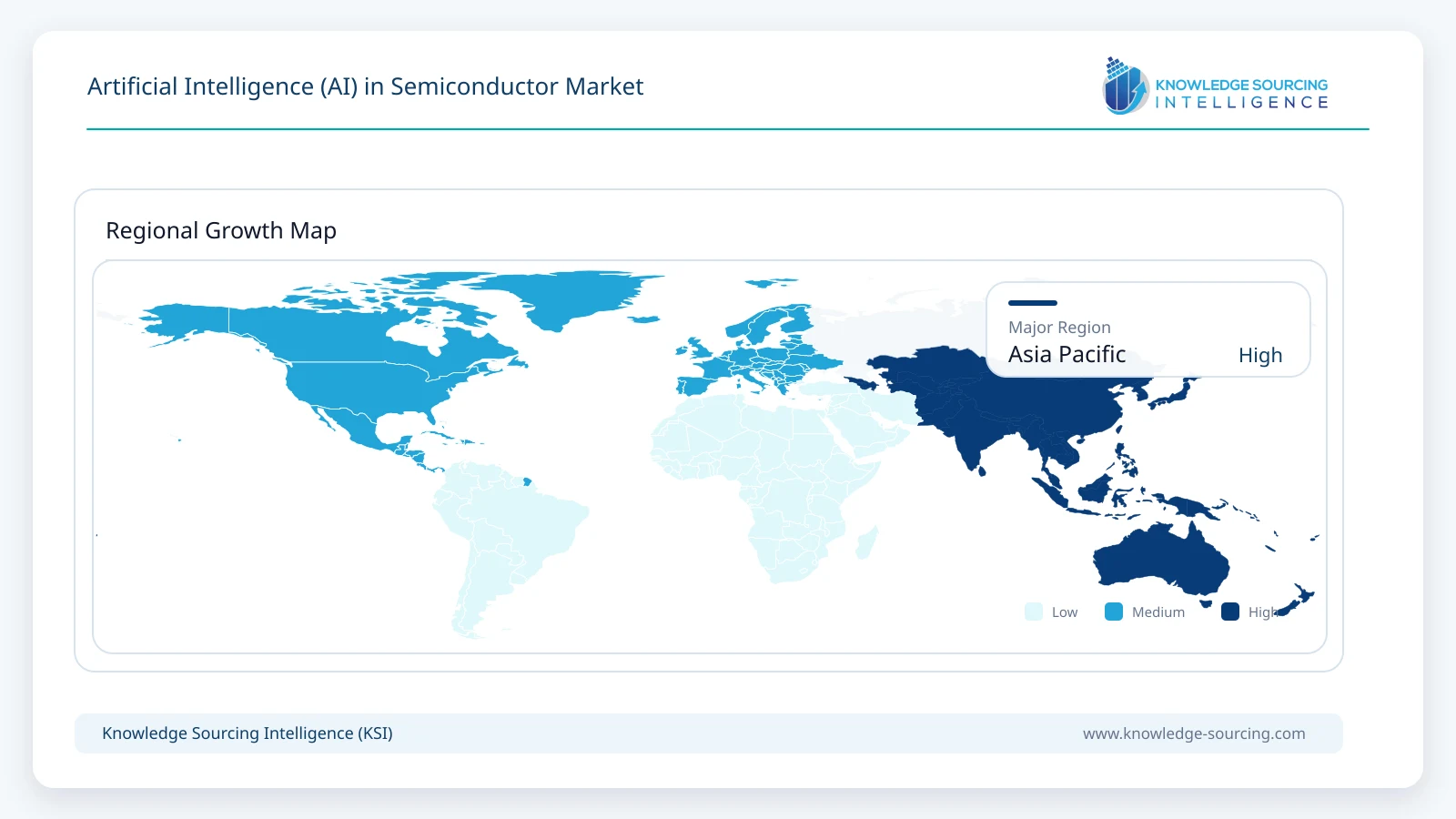

North America: Leads in AI chip design and R&D investment. Supported by the CHIPS Act, domestic manufacturing capacity is expanding, aimed at securing the supply of chips required for defense and hyperscale AI applications. Regulatory focus is primarily on national security and trade compliance.

Asia Pacific: Acts as the high-volume production engine. Japan, South Korea, and Taiwan dominate in advanced lithography and memory production, while India and Southeast Asian nations are rapidly emerging as key assembly, test, and packaging (ATMP) hubs.

Europe: Emphasizes sustainability and regulatory standards. While fabrication capacity is lower than in Asia, Europe is a leader in specialty semiconductors for automotive and industrial power, driven by strict green energy regulations and the need for regional autonomy.

Middle East and Africa: Increasing investment in data center infrastructure is driving local demand for AI hardware. These regions are prioritizing the integration of AI into public infrastructure and sovereign cloud initiatives, which necessitates the local availability of compute power.

South America: Developing as a niche market focused on the integration of AI in regional agriculture and resource management. Demand is primarily for edge compute hardware used in remote monitoring and industrial automation systems.

LIST OF COMPANIES

Google LLC

NVIDIA Corporation

Intel Corporation

Microsoft Corporation

Advanced Micro Devices, Inc. (AMD)

Qualcomm

IBM Corporation

Amazon Web Services, Inc.

Huawei

Xilinx

Google LLC

Google maintains a unique position through its proprietary Tensor Processing Units (TPUs). By designing its own ASICs, Google optimizes its infrastructure for its internal AI models (e.g., Gemini). This integration strategy provides a competitive advantage in cost-efficiency and power management within its global data centers, allowing for faster scaling than competitors reliant on external hardware providers.

NVIDIA Corporation

NVIDIA is the architect of the modern AI compute ecosystem. Its competitive advantage lies in its hardware-software synergy, particularly the CUDA platform. By controlling both the GPU architecture and the software stack that developers use to train models, NVIDIA has created a high barrier to entry. Its focus in 2026 remains on the scaling of large-cluster architectures like the GB200.

Intel Corporation

Intel is navigating a strategic transition from a CPU-centric identity to a platform-centric model including foundries and AI accelerators. Intel Foundry’s aggressive roadmap to 1.8nm processes represents its attempt to reclaim market leadership. Its competitive strength lies in its massive existing manufacturing footprint and its ability to offer integrated silicon-to-software solutions for both enterprise data centers and edge compute applications.

ANALYST VIEW

The AI semiconductor market is defined by a structural shift toward energy-efficient, specialized compute. Driven by persistent training and inference demand, growth is constrained by power and advanced packaging capacity, favoring integrated, hyperscale-linked leaders.

Artificial Intelligence (AI) in the Semiconductor Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 70.90 billion |

| Total Market Size in 2031 | USD 182.54 billion |

| Forecast Unit | Billion |

| Growth Rate | 20.8% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Chip Type, Application, End-Use, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Chip Type

By Application

By End-use

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. AI IN SEMICONDUCTOR MARKET BY CHIP TYPE

5.1. Introduction

5.2. Central Processing Units (CPUs)

5.3. Graphics Processing Units (GPUs)

5.4. Field-Programmable Gate Arrays (FPGAs)

5.5. Application-Specific Integrated Circuits (ASICs)

5.6. Tensor Processing Units (TPUs)

6. AI IN SEMICONDUCTOR MARKET BY APPLICATION

6.1. Introduction

6.2. AI Training

6.3. AI Inference

6.4. Edge AI

6.5. Cloud AI

6.6. Others

7. AI IN SEMICONDUCTOR MARKET BY END-USE

7.1. Introduction

7.2. Healthcare

7.3. Automotive

7.4. Consumer Electronics

7.5. Industrial Automation

7.6. Banking and Finance

7.7. Others

8. AI IN SEMICONDUCTOR MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Chip Type

8.2.2. By Application

8.2.3. By End-Use

8.2.4. By Country

8.2.4.1. USA

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Chip Type

8.3.2. By Application

8.3.3. By End-Use

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Chip Type

8.4.2. By Application

8.4.3. By End-Use

8.4.4. By Country

8.4.4.1. United Kingdom

8.4.4.2. Germany

8.4.4.3. France

8.4.4.4. Spain

8.4.4.5. Others

8.5. Middle East and Africa

8.5.1. By Chip Type

8.5.2. By Application

8.5.3. By End-Use

8.5.4. By Country

8.5.4.1. Saudi Arabia

8.5.4.2. UAE

8.5.4.3. Others

8.6. Asia Pacific

8.6.1. By Chip Type

8.6.2. By Application

8.6.3. By End-Use

8.6.4. By Country

8.6.4.1. China

8.6.4.2. Japan

8.6.4.3. India

8.6.4.4. South Korea

8.6.4.5. Taiwan

8.6.4.6. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. Google LLC

10.2. IBM Corporation

10.3. Microsoft Corporation

10.4. NVIDIA Corporation

10.5. Intel Corporation

10.6. Qualcomm

10.7. Advanced Micro Devices, Inc.

10.8. Xilinx

10.9. Amazon Web Services, Inc.

10.10. Huawei

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key benefits for the stakeholders

11.5. Research Methodology

11.6. Abbreviations LIST OF FIGURESLIST OF TABLES

Navigate

Trusted by the world's leading organizations