Report Overview

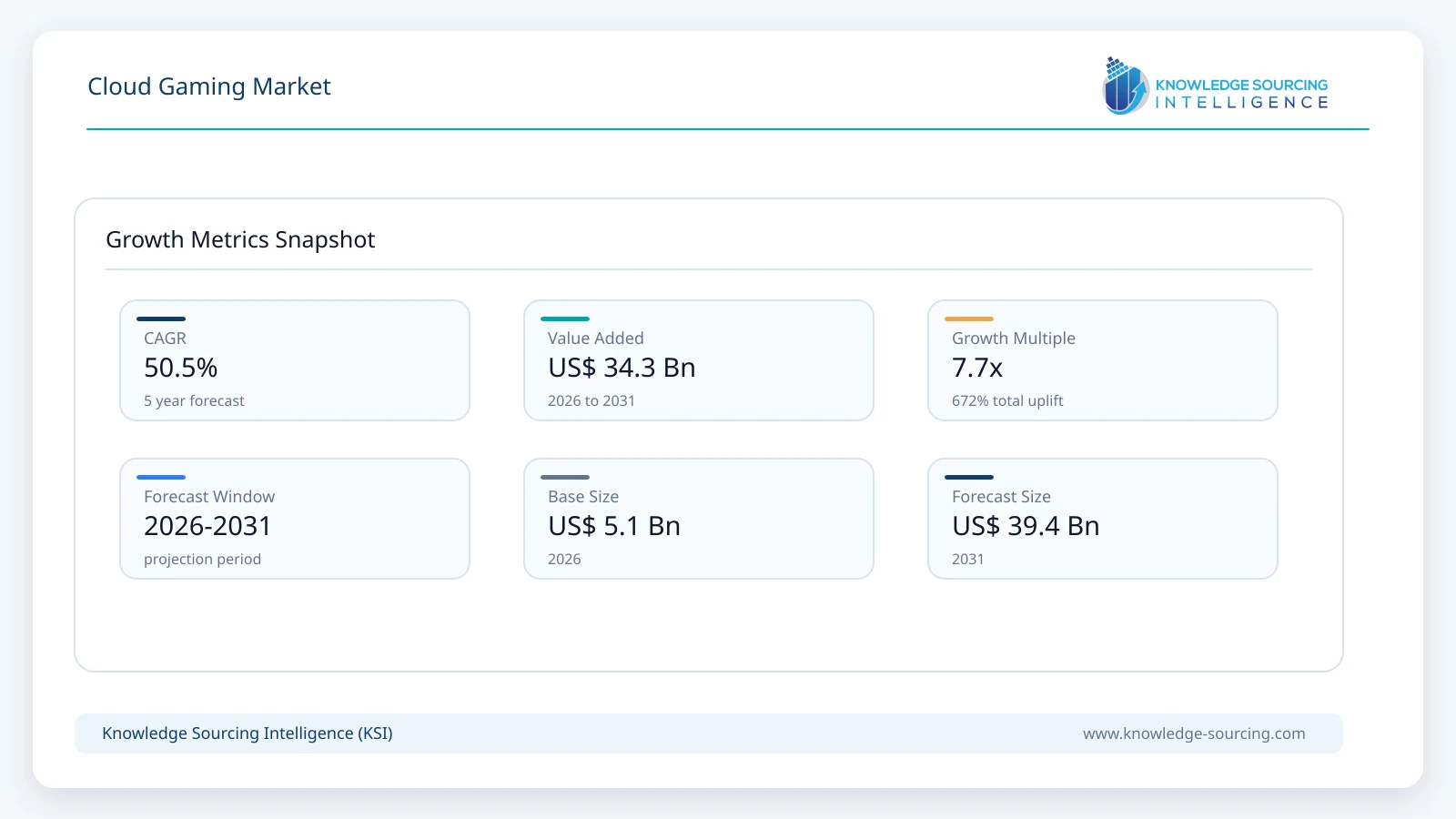

The Cloud Gaming Market is forecast to grow at a CAGR of 50.48%, reaching USD 39.35 billion in 2031 from USD 5.10 billion in 2026.

Highlights:

- 1Growing consumer preference for subscription-based gaming services continues to support demand for cloud gaming platforms.

- 2Smartphones represent the most commercially significant platform due to extensive global mobile internet adoption.

- 3Asia Pacific offers substantial expansion opportunities through increasing 5G deployment and rising digital entertainment spending.

- 4GPU virtualization, AI-assisted video encoding, and edge computing continue to improve streaming quality and latency performance.

- 5National broadband expansion initiatives and spectrum policies supporting 5G networks indirectly encourage cloud gaming adoption.

- 6Competition increasingly centers on exclusive content partnerships, infrastructure investments, and ecosystem integration rather than hardware ownership alone.

The cloud gaming market comprises platforms and infrastructure that enable users to play video games streamed from remote data centers rather than relying on local processing hardware. By shifting graphics rendering and game execution to cloud servers, cloud gaming reduces hardware dependency while allowing access to premium gaming experiences across smartphones, PCs, laptops, gaming consoles, smart TVs, and other connected devices. The commercial ecosystem includes cloud infrastructure providers, game publishers, streaming platform operators, telecommunications companies, and hardware manufacturers that collectively support low-latency content delivery.

Demand is being shaped by changing consumer preferences toward subscription-based digital entertainment, wider deployment of high-speed broadband and 5G networks, and growing acceptance of cross-device gaming. Instead of investing in expensive gaming hardware, consumers increasingly evaluate access flexibility, subscription value, game catalog availability, and streaming quality. Enterprise buyers, including telecommunications operators and internet service providers, are also entering the ecosystem by bundling cloud gaming services with broadband and mobile subscriptions to improve customer retention and increase average revenue per user.

The industry's revenue model extends beyond subscription fees. Platform operators generate income through game licensing agreements, premium memberships, in-game purchases, advertising-supported services, and strategic partnerships with telecommunications companies. Infrastructure providers benefit from increased utilization of graphics processing units (GPUs), edge computing resources, and cloud data centers, while publishers gain new distribution channels that expand audience reach without requiring dedicated gaming hardware.

Technology adoption varies by platform. Smartphones account for a broad user base due to widespread mobile internet access and expanding 5G coverage, while PCs and laptops remain important among users seeking access to larger game libraries and higher performance. Smart TV integration is gradually reducing the need for dedicated gaming devices, supported by advances in controller compatibility and embedded cloud gaming applications. Console manufacturers are simultaneously incorporating cloud capabilities into their existing ecosystems, offering hybrid gaming experiences that combine local and cloud execution.

Commercial adoption also depends on network quality. Latency, bandwidth stability, and server proximity directly influence user experience, making investment in regional edge computing infrastructure a competitive requirement. As cloud infrastructure expands geographically, providers can improve responsiveness while reducing service interruptions, supporting higher customer satisfaction and longer subscription retention.

The competitive environment remains closely linked to cloud computing capabilities, exclusive content partnerships, software optimization, and regional infrastructure deployment. Companies compete not only through game libraries but also through streaming performance, pricing models, device compatibility, and integration with broader digital ecosystems.

Market Drivers

Expansion of High-Speed Connectivity and 5G Infrastructure

Cloud gaming performance depends heavily on network quality. Continued investments in fiber broadband, standalone 5G networks, and edge computing infrastructure have reduced latency while improving streaming consistency. Telecommunications operators view gaming services as an opportunity to differentiate broadband offerings and improve customer retention. As network performance improves, consumers become more willing to replace traditional hardware purchases with cloud-based subscriptions, creating recurring revenue opportunities for service providers.

Rising Consumer Acceptance of Subscription-Based Entertainment

Digital subscription models have become well established across music, video, and software markets. Similar purchasing behavior is influencing gaming, where consumers increasingly prioritize access to extensive game libraries over ownership of individual titles. Subscription offerings reduce upfront spending while enabling users to explore a broader selection of games. Publishers benefit from recurring licensing revenue, while platform operators improve customer lifetime value through bundled premium services.

Growth in Graphics Processing Infrastructure

Cloud gaming requires substantial GPU capacity within distributed data centers. Continued investment by cloud infrastructure providers in advanced graphics hardware enables simultaneous support for larger user populations while improving rendering performance. Higher processing efficiency also allows operators to introduce premium streaming tiers offering enhanced image quality and higher frame rates, supporting differentiated pricing strategies.

Cross-Platform Gaming Preferences

Consumers increasingly expect uninterrupted gaming experiences across multiple devices. Cloud gaming allows users to begin gameplay on one device and continue on another without requiring local installation or synchronization. This flexibility appeals to both casual and experienced gamers, encouraging platform providers to expand compatibility across smartphones, PCs, smart TVs, and consoles while strengthening customer engagement.

Market Restraints and Challenges

Network Latency and Connectivity Variability

Even where broadband availability has improved, network consistency remains uneven across rural and developing regions. Packet loss, latency fluctuations, and bandwidth limitations can reduce gameplay quality, particularly for competitive multiplayer games. Service providers continue investing in regional edge infrastructure and adaptive streaming technologies to reduce these performance limitations.

High Infrastructure and Operating Costs

Operating cloud gaming platforms requires substantial investment in GPU-equipped data centers, networking equipment, software optimization, and electricity. Hardware refresh cycles further increase capital expenditure. Providers therefore face pressure to balance subscription pricing with infrastructure utilization while maintaining acceptable profit margins.

Content Licensing Complexity

Cloud streaming rights often differ from conventional digital distribution agreements. Publishers negotiate separate licensing arrangements covering geographic availability, subscription models, and revenue-sharing mechanisms. These negotiations can delay catalog expansion and create regional inconsistencies in game availability, influencing customer acquisition and retention.

Consumer Expectations for Performance

Gaming users generally maintain lower tolerance for delays compared with traditional video streaming audiences. Minor increases in latency or image compression can negatively affect user satisfaction. Providers therefore compete continuously through encoding improvements, predictive rendering techniques, and infrastructure optimization to maintain consistent performance.

Major Segment Analysis

Smartphones Lead Commercial Adoption

Smartphones represent the most commercially important platform because they combine extensive installed device bases with expanding mobile broadband coverage. Unlike dedicated gaming hardware, smartphones require no additional investment for most consumers, lowering adoption barriers for cloud gaming subscriptions. The combination of affordable mobile devices and growing 5G availability has expanded the addressable customer base across developed and emerging economies.

Buyer priorities within this segment emphasize accessibility, low latency, battery efficiency, controller compatibility, and flexible subscription pricing. Casual users often prefer instant game access without downloads, while experienced players increasingly expect console-quality graphics delivered through mobile networks. These expectations encourage providers to optimize adaptive bitrate streaming, touch-based interfaces, and external controller integration.

Competition within the smartphone segment extends beyond gaming platforms themselves. Telecommunications companies, smartphone manufacturers, cloud providers, and game publishers increasingly collaborate through bundled subscriptions and pre-installed applications. Such partnerships improve customer acquisition while reducing marketing costs. Commercially, smartphones remain the primary channel through which cloud gaming providers can expand user numbers and recurring subscription revenue over the forecast period.

Regional Analysis

North America

North America maintains strong demand due to high broadband penetration, widespread cloud infrastructure, and established gaming expenditure. Consumers demonstrate relatively high acceptance of subscription entertainment services, while major cloud infrastructure investments support low-latency streaming. Competition remains intense as global technology companies expand content partnerships and service integration.

Europe

European demand benefits from mature digital infrastructure, strong fixed broadband availability, and increasing fiber deployment. Regulatory attention toward digital competition, consumer data protection, and cloud services influences operating strategies. Regional growth also depends on multilingual content availability and partnerships with telecommunications providers operating across multiple countries.

Asia Pacific

Asia Pacific represents the largest long-term expansion opportunity due to its substantial gaming population, improving mobile connectivity, and accelerating 5G deployment. Countries including China, Japan, South Korea, and India continue investing in digital infrastructure that supports cloud-based entertainment services. Price-sensitive consumers encourage providers to introduce flexible subscription options alongside localized gaming content.

Middle East and Africa

Investment in digital infrastructure, smart city initiatives, and expanding fiber broadband networks supports gradual market development across selected countries. Gulf economies continue strengthening cloud computing capabilities, although infrastructure disparities across several African markets constrain broader adoption. Consumer awareness and affordable connectivity remain important determinants of future demand.

South America

South American adoption continues to improve with expanding broadband coverage and increasing digital payment adoption. Brazil represents the region's largest commercial opportunity due to its sizable gaming community and improving telecommunications infrastructure. However, network quality differences and economic volatility continue influencing subscription affordability and infrastructure investment decisions.

Competitive Landscape

The cloud gaming market exhibits moderate concentration, with competition driven by cloud infrastructure capabilities, exclusive gaming content, streaming quality, ecosystem integration, and geographic coverage. NVIDIA Corporation, Microsoft Corporation, Sony Group Corporation, Amazon Web Services, Inc., Google LLC, Ubisoft Entertainment SA, Tencent Holdings Ltd., Ubitus K.K., Boosteroid, and OVH Groupe SAS compete through different combinations of technology infrastructure, software ecosystems, publishing partnerships, and regional deployment strategies.

Competitive differentiation increasingly depends on GPU performance, edge computing presence, AI-assisted video encoding, platform interoperability, and subscription value. Strategic partnerships between cloud providers, telecommunications operators, and game publishers continue influencing customer acquisition while reducing distribution costs. Companies are also expanding regional data center capacity to improve latency performance and comply with national data governance requirements.

Recent Developments

April 2026: Boosteroid announced it is scaling its global cloud gaming platform using AMD high-performance compute and graphics technologies, supporting its growing infrastructure and enabling enhanced cloud gaming performance for millions of users worldwide.

March 2026: Boosteroid expanded its European cloud gaming infrastructure by deploying an additional batch of GPU servers at ?eské Radiokomunikace (CRA) data centers in the Czech Republic to improve low-latency gaming capacity and regional service availability.

January 2026: Boosteroid officially launched its cloud gaming application on Whale TV-powered 4K Smart TVs, including supported models from Philips, RCA, Sharp, Telefunken, and JVC, expanding high-performance cloud gaming across Europe and the Americas.

Regulatory and Policy Environment

Cloud gaming providers operate within a regulatory framework that extends beyond gaming regulations to include cloud computing, digital content licensing, cybersecurity, telecommunications policy, and consumer data protection. Privacy regulations, including regional data governance requirements, influence how providers process user information and deploy cloud infrastructure.

Broadband expansion programs and national 5G deployment initiatives indirectly support cloud gaming adoption by improving connectivity quality. Telecommunications regulators continue allocating spectrum to accelerate mobile broadband deployment, benefiting latency-sensitive applications such as cloud gaming.

Competition authorities also monitor digital platform practices, particularly regarding app distribution, subscription ecosystems, and cloud service integration. Compliance with consumer protection requirements, digital taxation frameworks, intellectual property laws, and content licensing obligations remains essential for multinational platform operators.

Outlook and Strategic Implications

Commercial prospects for the cloud gaming market will depend on infrastructure economics as much as consumer demand. Continued investment in edge computing, GPU acceleration, and AI-based streaming optimization should improve service quality while supporting greater operational efficiency. Buyers are expected to prioritize service reliability, content diversity, device compatibility, and transparent subscription pricing rather than hardware specifications.

Procurement strategies among telecommunications providers are likely to emphasize partnerships with cloud gaming platforms that strengthen bundled broadband offerings and improve subscriber retention. Publishers will continue evaluating cloud distribution as an additional revenue channel, particularly for expanding access in regions with lower ownership of high-performance gaming hardware.

Competition is expected to shift further toward ecosystem integration, combining cloud infrastructure, digital storefronts, subscription libraries, and social gaming features within unified platforms. Companies capable of balancing infrastructure investment, exclusive content availability, regulatory compliance, and consistent streaming performance will be better positioned to strengthen long-term customer retention. At the same time, network quality disparities, licensing complexity, and rising infrastructure costs will remain important commercial risks that influence investment priorities throughout the forecast period.

Cloud Gaming Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 5.10 billion |

| Total Market Size in 2031 | USD 39.35 billion |

| Forecast Unit | Billion |

| Growth Rate | 50.48% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Platform, Service Type, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Platform

- Smartphones

- PCs and Laptops

- Gaming Consoles

- Smart TVs

- Others

By Service Type

- Video Streaming

- File Streaming

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Others

- Asia Pacific

- Japan

- China

- India

- South Korea

- Indonesia

- Thailand

- Taiwan

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits for the Stakeholder

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. CLOUD GAMING MARKET BY PLATFORM

5.1. Introduction

5.2. Smartphones

5.3. PCs and Laptops

5.4. Gaming Consoles

5.5. Smart TVs

5.6. Others

6. CLOUD GAMING MARKET BY SERVICE TYPE

6.1. Introduction

6.2. Video Streaming

6.3. File Streaming

7. CLOUD GAMING MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. United States

7.2.2. Canada

7.2.3. Mexico

7.3. South America

7.3.1. Brazil

7.3.2. Argentina

7.3.3. Others

7.4. Europe

7.4.1. United Kingdom

7.4.2. Germany

7.4.3. France

7.4.4. Spain

7.4.5. Italy

7.4.6. Others

7.5. Middle East and Africa

7.5.1. Saudi Arabia

7.5.2. UAE

7.5.3. Israel

7.5.4. Others

7.6. Asia Pacific

7.6.1. Japan

7.6.2. China

7.6.3. India

7.6.4. South Korea

7.6.5. Indonesia

7.6.6. Thailand

7.6.7. Taiwan

7.6.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. NVIDIA Corporation

9.2. Microsoft Corporation

9.3. Sony Group Corporation

9.4. Amazon Web Services, Inc.

9.5. Google LLC

9.6. Ubisoft Entertainment SA

9.7. Tencent Holdings Ltd.

9.8. Ubitus K.K.

9.9. Boosteroid

9.10. OVH Groupe SAS

Navigate

Trusted by the world's leading organizations