Report Overview

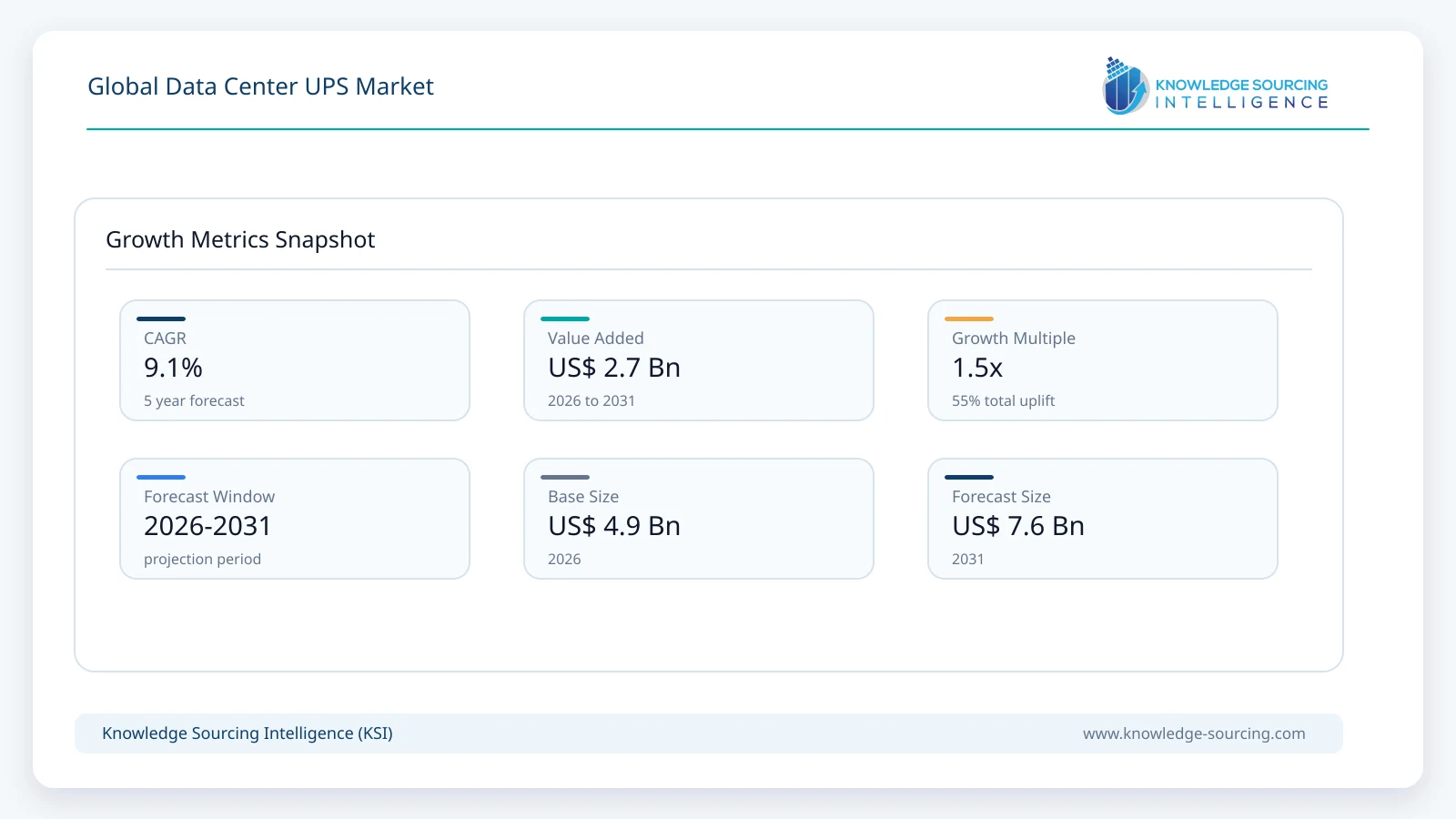

The global Data Center UPS market is forecast to grow at a CAGR of 9.13%, reaching USD 7.60 billion in 2031 from USD 4.91 billion in 2026.

Highlights:

- 1Expansion of AI computing infrastructure is increasing demand for higher-capacity and scalable UPS installations.

- 2Double Conversion UPS technology remains the preferred solution for mission-critical data center applications requiring maximum power quality.

- 3Asia Pacific continues to attract substantial investment through hyperscale, colocation, and enterprise data center construction.

- 4Lithium-ion battery integration and intelligent UPS monitoring are influencing new procurement specifications.

- 5Energy efficiency regulations and sustainability objectives encourage adoption of high-efficiency UPS operating modes.

- 6Competition increasingly centers on complete power infrastructure ecosystems, lifecycle services, and digital asset management capabilities.

The data center UPS (Uninterruptible Power Supply) market comprises power protection systems that provide continuous electricity to servers, networking equipment, storage infrastructure, and supporting systems during grid disturbances or complete utility failures. UPS systems are a core element of data center electrical architecture because even brief power interruptions can result in service outages, data corruption, regulatory non-compliance, and financial losses. As digital infrastructure expands across enterprise, colocation, hyperscale, and edge computing environments, investments in resilient power infrastructure remain a prerequisite for facility development.

Demand is primarily driven by sustained investments in cloud computing, artificial intelligence (AI) infrastructure, financial transaction platforms, telecommunications networks, healthcare information systems, and public-sector digital services. Buyers increasingly evaluate UPS solutions not only for backup capability but also for energy efficiency, scalability, serviceability, battery technology compatibility, monitoring capabilities, and lifecycle operating costs. Procurement decisions frequently involve data center developers, electrical engineering consultants, IT infrastructure teams, facility operators, and corporate sustainability departments.

The industry structure is characterized by established global suppliers with broad portfolios spanning UPS systems, switchgear, power distribution, batteries, software, and lifecycle services. Large hyperscale operators often procure customized modular systems capable of supporting phased capacity additions, while enterprise customers prioritize reliability, maintenance support, and standardized deployment across multiple facilities. The growing adoption of lithium-ion battery systems, intelligent monitoring software, predictive maintenance, and modular UPS architectures is changing purchasing priorities across both greenfield and retrofit projects.

Revenue generation extends beyond equipment sales to include installation, commissioning, preventive maintenance, battery replacement, remote monitoring, and long-term service agreements. Suppliers capable of integrating UPS equipment with broader power management and data center infrastructure management platforms gain stronger commercial positioning, particularly among operators seeking standardized infrastructure across geographically distributed facilities.

Market Drivers

Expansion of AI and High-Density Computing Infrastructure

Artificial intelligence workloads require significantly greater electrical capacity than conventional enterprise computing. High-density server deployments increase sensitivity to voltage fluctuations and require continuous power availability throughout utility disturbances. Data center developers therefore specify higher-capacity UPS systems with modular expansion capability to support phased infrastructure deployment.

Customers increasingly seek equipment capable of maintaining high efficiency under varying load conditions while supporting future rack density increases. Manufacturers have responded by introducing modular architectures, improved thermal performance, and digital monitoring capabilities. This trend expands equipment value beyond emergency backup toward long-term operational optimization.

Continued Investment in Colocation and Hyperscale Facilities

Cloud service providers, digital platforms, financial institutions, and content delivery companies continue expanding data center capacity to accommodate rising computing demand. Every new facility requires redundant electrical infrastructure designed to meet stringent uptime objectives.

Procurement increasingly emphasizes standardized designs across multiple sites to simplify maintenance, spare parts management, and operational consistency. Suppliers with global manufacturing, engineering support, and service networks benefit from these purchasing preferences because customers often seek long-term infrastructure partners rather than individual equipment vendors.

Rising Cost of Downtime

Organizations operating payment systems, healthcare records, telecommunications networks, industrial automation, and government digital services face substantial financial and operational consequences from unexpected outages. Even short interruptions can disrupt business continuity, damage customer confidence, and create regulatory liabilities.

As a result, buyers increasingly evaluate UPS investments using lifecycle risk reduction rather than initial purchase cost alone. This encourages procurement of redundant architectures, advanced diagnostics, predictive maintenance software, and service agreements that improve equipment availability throughout its operating life.

Transition Toward Intelligent Power Management

UPS systems are becoming connected assets capable of transmitting operational data for predictive maintenance, battery health analysis, remote diagnostics, and energy optimization. Facility operators use these capabilities to improve maintenance planning and reduce unexpected equipment failures.

Manufacturers continue integrating UPS platforms with broader infrastructure management software, enabling centralized visibility across multiple facilities. Such capabilities support operational efficiency while lowering maintenance expenditure over extended deployment cycles.

Market Restraints and Challenges

High Initial Capital Requirements

Large data center UPS installations require substantial investment covering equipment, batteries, electrical integration, commissioning, and redundancy. Capital expenditure can represent a meaningful share of overall facility construction costs, particularly for hyperscale developments.

Budget limitations may encourage phased deployment or modular procurement strategies. Suppliers increasingly address this challenge through scalable architectures and lifecycle service contracts that distribute investment over longer operating periods.

Battery Lifecycle Management

Battery performance directly affects UPS reliability. Operators must regularly inspect, monitor, replace, and recycle battery systems throughout equipment life. Improper battery management increases operational risk and maintenance costs.

The transition toward lithium-ion batteries reduces maintenance frequency but introduces higher upfront costs and different safety considerations. Buyers therefore evaluate total ownership costs rather than battery acquisition prices alone.

Grid Capacity Constraints

Many regions face delays in connecting new data centers due to electricity transmission limitations and lengthy utility approval processes. These delays postpone associated UPS procurement despite sustained demand for digital infrastructure.

Developers increasingly coordinate electrical planning with utilities during early project stages while considering alternative energy integration and battery energy storage systems to improve operational flexibility.

Supply Chain and Component Availability

Power electronics, semiconductors, batteries, transformers, and electrical components remain subject to periodic supply constraints. Extended lead times can delay project schedules and increase procurement costs.

Manufacturers mitigate these risks by diversifying supplier networks, expanding regional manufacturing capacity, and increasing inventory for critical components.

Major Segment Analysis

Double Conversion UPS

Double Conversion UPS represents the most commercially significant technology segment because it delivers continuous power conditioning while isolating sensitive IT equipment from utility disturbances. Unlike standby or line-interactive systems, double conversion architectures continuously convert incoming AC power to DC and back to AC, providing stable output regardless of fluctuations in the incoming supply.

Large enterprise facilities, hyperscale operators, financial institutions, healthcare organizations, and government agencies generally prioritize this technology because uninterrupted operations outweigh marginal differences in equipment cost. Buyers place considerable emphasis on efficiency, redundancy, modular scalability, battery compatibility, maintenance accessibility, and integration with facility monitoring platforms.

Competition within this segment increasingly revolves around operating efficiency, reduced footprint, modular expansion, intelligent diagnostics, cybersecurity features, and lifecycle support services. Vendors also differentiate through high-power density systems capable of supporting AI-driven computing environments with elevated electrical loads.

Commercially, the segment generates recurring revenue through maintenance contracts, battery replacement programs, remote monitoring, and modernization projects, making it strategically important across the broader UPS market.

Regional Analysis

North America remains the largest investment destination for hyperscale and colocation data centers. Cloud expansion, AI infrastructure deployment, and enterprise modernization sustain demand for high-capacity UPS systems. Procurement emphasizes operational resilience, cybersecurity integration, and energy efficiency, although utility capacity constraints have become a consideration in certain metropolitan markets.

Europe combines mature data center infrastructure with strong environmental regulations. Operators increasingly procure high-efficiency UPS solutions supporting lower operating emissions and improved energy performance. Demand also benefits from financial services, public administration, manufacturing, and research computing investments, although permitting and electricity costs influence project economics.

Asia Pacific represents the strongest long-term infrastructure opportunity due to sustained cloud adoption, digital economy initiatives, manufacturing expansion, and increasing internet penetration. China, India, Japan, South Korea, Taiwan, and Southeast Asian countries continue attracting enterprise and hyperscale investments. Buyers frequently prioritize scalable modular UPS systems suitable for phased facility expansion.

Middle East and Africa continue expanding digital infrastructure through government cloud initiatives, smart city programs, and telecommunications investment. Gulf countries remain important markets owing to substantial data center construction, while broader regional adoption depends on electricity infrastructure development and investment availability.

South America experiences growing demand from financial institutions, telecommunications operators, and colocation providers. Brazil leads regional investment due to its large digital economy, while Argentina and neighboring markets continue modernizing enterprise IT infrastructure despite macroeconomic uncertainties affecting capital expenditure.

Competitive Landscape

The competitive environment includes Vertiv Group Corp., Schneider Electric SE, ABB Ltd., Eaton Corporation plc, Huawei Digital Power Technologies Co., Ltd., Delta Electronics, Inc., Mitsubishi Electric Corporation, Socomec Group, and Hitachi Hi-Rel Power Electronics Private Limited. Competition extends beyond hardware specifications toward integrated power infrastructure solutions combining UPS systems, switchgear, batteries, monitoring software, service contracts, and engineering expertise.

Suppliers differentiate through modular product portfolios, energy efficiency, battery technology compatibility, remote monitoring capabilities, cybersecurity, and lifecycle support. Strategic partnerships with cloud providers, engineering contractors, and colocation developers strengthen market access for large infrastructure projects. Geographic manufacturing presence and global service capabilities also influence procurement decisions, particularly for multinational customers seeking standardized infrastructure across multiple regions.

Recent Developments

June 2026: Skeleton Technologies introduced a new UPS platform engineered specifically for AI data centers, providing continuous power protection through ultracapacitor-based technology to improve reliability and reduce dependence on conventional battery-based UPS systems.

May 2026: Schneider Electric secured a US$290 million infrastructure agreement with TeraWulf to supply critical power systems, including lithium-ion UPS technology, for AI-ready data center infrastructure supporting high-density computing workloads.

April 2026: Vertiv announced a collaboration with CPower to integrate battery energy storage and UPS assets into grid-interactive energy management programs, enabling data centers to improve resilience while participating in grid services.

March 2026: Vertiv introduced the PowerUPS 6000 Industrial UPS platform featuring high-efficiency operation and compatibility with multiple battery technologies. The launch broadens the company's portfolio for mission-critical power applications.

August 2025: Vertiv completed the acquisition of Waylay to strengthen AI-enabled monitoring and optimization capabilities for data center power and cooling infrastructure. The transaction expands digital service capabilities supporting intelligent UPS management.

Regulatory and Policy Environment

The market operates within a framework of electrical safety regulations, energy efficiency standards, environmental requirements, and cybersecurity expectations. Data center operators generally specify UPS systems complying with international standards governing electrical safety, electromagnetic compatibility, battery performance, and equipment reliability.

Government energy efficiency initiatives encourage adoption of high-efficiency operating modes that reduce electricity consumption without compromising availability. Environmental regulations governing battery transportation, recycling, and disposal influence lifecycle management practices, while fire safety codes affect battery installation design.

Many countries continue supporting domestic digital infrastructure through cloud adoption strategies, semiconductor investment programs, and broadband expansion initiatives. Although these policies do not directly mandate UPS procurement, they stimulate construction of facilities requiring resilient electrical infrastructure. Compliance with operational resilience requirements in banking, healthcare, telecommunications, and public administration further reinforces demand for highly reliable backup power systems.

Outlook and Strategic Implications

Over the next five years, procurement priorities are expected to shift toward scalable, software-enabled UPS platforms capable of supporting AI infrastructure, higher rack densities, and integrated energy management. Buyers will increasingly evaluate systems using total cost of ownership, operational efficiency, maintainability, cybersecurity, and compatibility with advanced battery technologies.

Manufacturers are likely to expand digital monitoring, predictive maintenance, and remote service capabilities while increasing investment in modular product architectures supporting phased capacity expansion. Integration between UPS systems, battery energy storage, renewable power, and facility energy management platforms will become more important as operators seek greater operational flexibility.

Competition will continue emphasizing complete infrastructure ecosystems rather than standalone products. Suppliers with broad service organizations, strong engineering capabilities, and established relationships with hyperscale developers are expected to maintain competitive advantages. Nevertheless, electricity infrastructure limitations, supply chain uncertainty, battery lifecycle costs, and changing regulatory requirements remain important strategic risks that market participants must address while supporting continued expansion of global data center capacity.

Data Center UPS Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 4.91 billion |

| Total Market Size in 2031 | USD 7.60 billion |

| Forecast Unit | Billion |

| Growth Rate | 9.13% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Technology, Type, Data Centre Size, Industry Vertical, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Technology

- Line-Interactive UPS

- Standby UPS

- Double Conversion UPS

By Type

- Rack-mounted UPS

- Zone-level UPS

- Centralized UPS

By Data Centre Size

- Small

- Medium

- Large

By Industry Vertical

- BFSI

- Manufacturing

- IT and Telecommunications

- Healthcare

- Government

- Energy and Utilities

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Germany

- France

- United Kingdom

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- Israel

- United Arab Emirates

- Others

- Asia Pacific

- China

- Japan

- South Korea

- India

- Taiwan

- Thailand

- Indonesia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Processes

3. EXECUTIVE SUMMARY

3.1. Key Findings

3.2. CXO Perspective

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter's Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

4.5. Analyst View

5. GLOBAL DATA CENTER UPS MARKET BY TECHNOLOGY

5.1. Introduction

5.2. Line-Interactive UPS

5.2.1. Market Trends and Opportunities

5.2.2. Growth Prospects

5.2.3. Geographic Lucrativeness

5.3. Standby UPS

5.3.1. Market Trends and Opportunities

5.3.2. Growth Prospects

5.3.3. Geographic Lucrativeness

5.4. Double Conversion UPS

5.4.1. Market Trends and Opportunities

5.4.2. Growth Prospects

5.4.3. Geographic Lucrativeness

6. GLOBAL DATA CENTER UPS MARKET BY TYPE

6.1. Introduction

6.2. Rack-mounted UPS

6.2.1. Market Trends and Opportunities

6.2.2. Growth Prospects

6.2.3. Geographic Lucrativeness

6.3. Zone-level UPS

6.3.1. Market Trends and Opportunities

6.3.2. Growth Prospects

6.3.3. Geographic Lucrativeness

6.4. Centralized UPS

6.4.1. Market Trends and Opportunities

6.4.2. Growth Prospects

6.4.3. Geographic Lucrativeness

7. GLOBAL DATA CENTER UPS MARKET BY DATA CENTRE SIZE

7.1. Introduction

7.2. Small

7.2.1. Market Trends and Opportunities

7.2.2. Growth Prospects

7.2.3. Geographic Lucrativeness

7.3. Medium

7.3.1. Market Trends and Opportunities

7.3.2. Growth Prospects

7.3.3. Geographic Lucrativeness

7.4. Large

7.4.1. Market Trends and Opportunities

7.4.2. Growth Prospects

7.4.3. Geographic Lucrativeness

8. GLOBAL DATA CENTER UPS MARKET BY INDUSTRY VERTICAL

8.1. Introduction

8.2. BFSI

8.2.1. Market Trends and Opportunities

8.2.2. Growth Prospects

8.2.3. Geographic Lucrativeness

8.3. Manufacturing

8.3.1. Market Trends and Opportunities

8.3.2. Growth Prospects

8.3.3. Geographic Lucrativeness

8.4. IT and Telecommunications

8.4.1. Market Trends and Opportunities

8.4.2. Growth Prospects

8.4.3. Geographic Lucrativeness

8.5. Healthcare

8.5.1. Market Trends and Opportunities

8.5.2. Growth Prospects

8.5.3. Geographic Lucrativeness

8.6. Government

8.6.1. Market Trends and Opportunities

8.6.2. Growth Prospects

8.6.3. Geographic Lucrativeness

8.7. Energy and Utilities

8.7.1. Market Trends and Opportunities

8.7.2. Growth Prospects

8.7.3. Geographic Lucrativeness

8.8. Others

8.8.1. Market Trends and Opportunities

8.8.2. Growth Prospects

8.8.3. Geographic Lucrativeness

9. GLOBAL DATA CENTER UPS MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. By Technology

9.2.2. By Type

9.2.3. By Data Centre Size

9.2.4. By Industry Vertical

9.2.5. By Country

9.2.5.1. United States

9.2.5.1.1. Market Trends and Opportunities

9.2.5.1.2. Growth Prospects

9.2.5.2. Canada

9.2.5.2.1. Market Trends and Opportunities

9.2.5.2.2. Growth Prospects

9.2.5.3. Mexico

9.2.5.3.1. Market Trends and Opportunities

9.2.5.3.2. Growth Prospects

9.3. South America

9.3.1. By Technology

9.3.2. By Type

9.3.3. By Data Centre Size

9.3.4. By Industry Vertical

9.3.5. By Country

9.3.5.1. Brazil

9.3.5.1.1. Market Trends and Opportunities

9.3.5.1.2. Growth Prospects

9.3.5.2. Argentina

9.3.5.2.1. Market Trends and Opportunities

9.3.5.2.2. Growth Prospects

9.3.5.3. Others

9.3.5.3.1. Market Trends and Opportunities

9.3.5.3.2. Growth Prospects

9.4. Europe

9.4.1. By Technology

9.4.2. By Type

9.4.3. By Data Centre Size

9.4.4. By Industry Vertical

9.4.5. By Country

9.4.5.1. Germany

9.4.5.1.1. Market Trends and Opportunities

9.4.5.1.2. Growth Prospects

9.4.5.2. France

9.4.5.2.1. Market Trends and Opportunities

9.4.5.2.2. Growth Prospects

9.4.5.3. United Kingdom

9.4.5.3.1. Market Trends and Opportunities

9.4.5.3.2. Growth Prospects

9.4.5.4. Spain

9.4.5.4.1. Market Trends and Opportunities

9.4.5.4.2. Growth Prospects

9.4.5.5. Others

9.4.5.5.1. Market Trends and Opportunities

9.4.5.5.2. Growth Prospects

9.5. Middle East and Africa

9.5.1. By Technology

9.5.2. By Type

9.5.3. By Data Centre Size

9.5.4. By Industry Vertical

9.5.5. By Country

9.5.5.1. Saudi Arabia

9.5.5.1.1. Market Trends and Opportunities

9.5.5.1.2. Growth Prospects

9.5.5.2. Israel

9.5.5.2.1. Market Trends and Opportunities

9.5.5.2.2. Growth Prospects

9.5.5.3. United Arab Emirates

9.5.5.3.1. Market Trends and Opportunities

9.5.5.3.2. Growth Prospects

9.5.5.4. Others

9.5.5.4.1. Market Trends and Opportunities

9.5.5.4.2. Growth Prospects

9.6. Asia Pacific

9.6.1. By Technology

9.6.2. By Type

9.6.3. By Data Centre Size

9.6.4. By Industry Vertical

9.6.5. By Country

9.6.5.1. China

9.6.5.1.1. Market Trends and Opportunities

9.6.5.1.2. Growth Prospects

9.6.5.2. Japan

9.6.5.2.1. Market Trends and Opportunities

9.6.5.2.2. Growth Prospects

9.6.5.3. South Korea

9.6.5.3.1. Market Trends and Opportunities

9.6.5.3.2. Growth Prospects

9.6.5.4. India

9.6.5.4.1. Market Trends and Opportunities

9.6.5.4.2. Growth Prospects

9.6.5.5. Taiwan

9.6.5.5.1. Market Trends and Opportunities

9.6.5.5.2. Growth Prospects

9.6.5.6. Thailand

9.6.5.6.1. Market Trends and Opportunities

9.6.5.6.2. Growth Prospects

9.6.5.7. Indonesia

9.6.5.7.1. Market Trends and Opportunities

9.6.5.7.2. Growth Prospects

9.6.5.8. Others

9.6.5.8.1. Market Trends and Opportunities

9.6.5.8.2. Growth Prospects

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. Vertiv Group Corp.

11.2. Schneider Electric SE

11.3. ABB Ltd.

11.4. Eaton Corporation plc

11.5. Huawei Digital Power Technologies Co., Ltd.

11.6. Delta Electronics, Inc.

11.7. Mitsubishi Electric Corporation

11.8. Socomec Group

11.9. Hitachi Hi-Rel Power Electronics Private Limited

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations