Report Overview

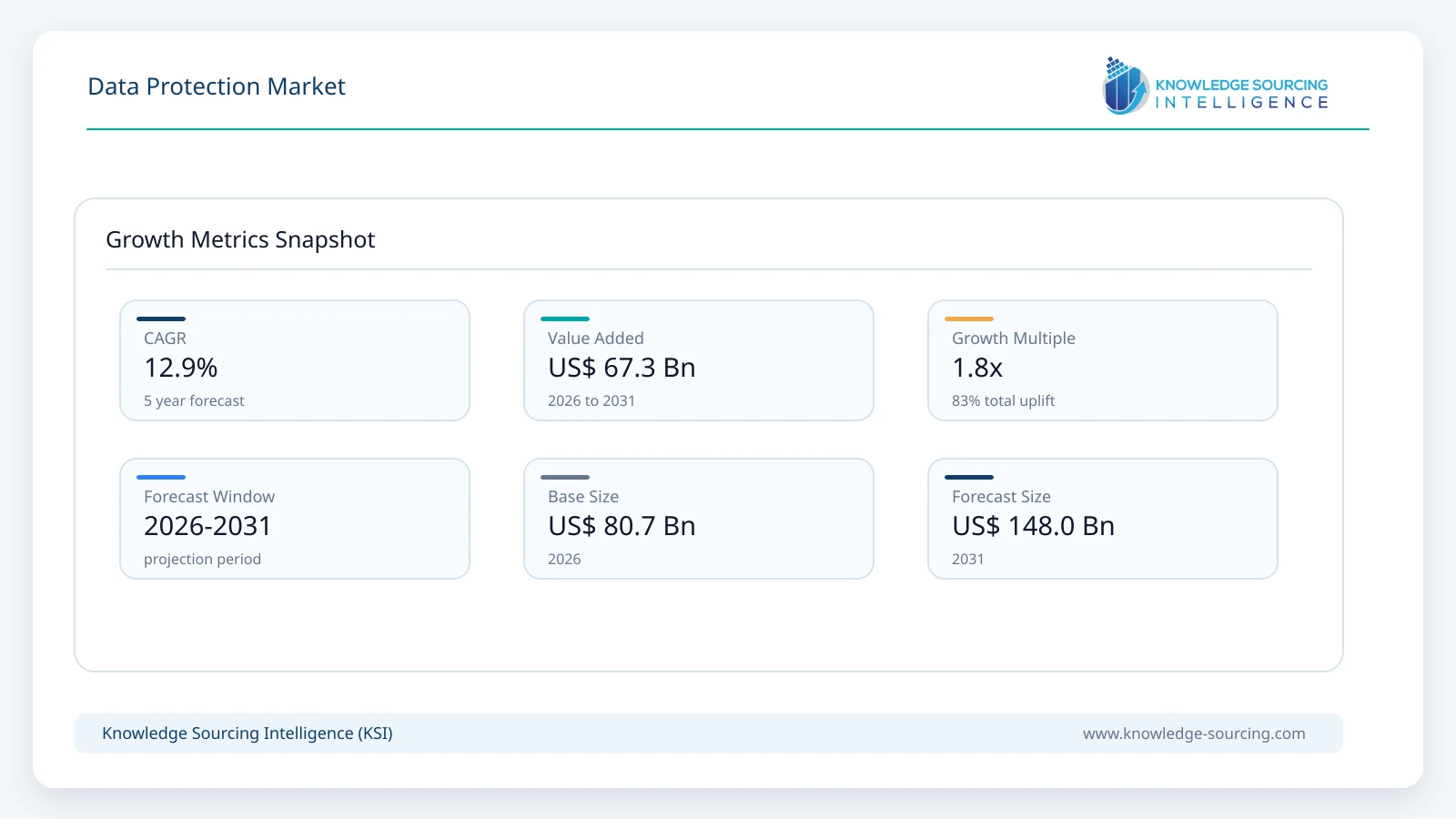

The data protection market is forecast to grow at a CAGR of 12.9%, reaching USD 148.0 billion in 2031 from USD 80.7 billion in 2026.

Highlights:

- 1Ransomware preparedness has become the strongest purchasing catalyst, driving investment in immutable backup, recovery automation, and cyber recovery capabilities.

- 2Cloud deployment represents the primary technology transition, supported by expanding hybrid and multi-cloud enterprise environments.

- 3Large enterprises remain the leading revenue contributorsbecause of complex infrastructure, regulatory obligations, and extensive data estates.

- 4North America maintains substantial commercial leadership, supported by mature cybersecurity spending and strict compliance requirements.

- 5Artificial intelligence is improving backup management, enabling anomaly detection, policy automation, and predictive infrastructure monitoring.

- 6Regulatory compliance continues influencing procurement, particularly across financial services, healthcare, government, and critical infrastructure sectors.

The data protection market comprises software platforms, integrated solutions, and managed services designed to safeguard enterprise data throughout its lifecycle by ensuring availability, confidentiality, integrity, recovery, and regulatory compliance. Modern data protection extends beyond conventional backup and recovery to include ransomware resilience, immutable storage, disaster recovery, encryption, data loss prevention (DLP), workload protection, cloud backup, endpoint security integration, and governance capabilities. Organizations across both public and private sectors now consider data protection an operational necessity rather than a discretionary IT investment, as business continuity increasingly depends on uninterrupted access to trusted information assets.

Demand is being shaped by a combination of expanding digital data volumes, widespread adoption of hybrid cloud infrastructure, stricter regulatory obligations, and the financial consequences of cyber incidents. Enterprises are managing structured databases alongside rapidly growing volumes of unstructured information generated through collaboration platforms, industrial systems, customer applications, and edge devices. This diversification of enterprise data has increased procurement of unified protection platforms capable of managing on-premises infrastructure, multiple cloud environments, software-as-a-service (SaaS) applications, and distributed endpoints through centralized policy management.

Purchasing priorities have shifted noticeably during the past several years. Buyers increasingly evaluate recovery speed, cyber resilience, workload portability, automation, and compliance reporting alongside traditional backup performance. Recovery time objectives (RTOs), recovery point objectives (RPOs), immutable backup storage, ransomware detection, and orchestration capabilities have become influential purchasing criteria, particularly for highly regulated industries such as banking, healthcare, telecommunications, and government. Organizations also seek platforms that reduce operational complexity by integrating backup, disaster recovery, archiving, and security controls within a common management framework.

The competitive structure includes global enterprise software vendors, cybersecurity providers, storage infrastructure companies, and specialized backup solution developers. Suppliers differentiate themselves through cloud-native architectures, artificial intelligence-assisted threat detection, ransomware recovery capabilities, scalability across hybrid environments, workload-specific optimization, and subscription-based commercial models. Managed service providers are expanding their role by delivering continuous monitoring, backup management, disaster recovery testing, and compliance support for organizations lacking specialized cybersecurity resources.

Growing investment in cloud infrastructure is reshaping deployment preferences. Although large regulated enterprises continue maintaining critical workloads on dedicated infrastructure, cloud-based deployment is attracting increasing adoption due to scalability, operational flexibility, and predictable operating expenditure. Small and medium-sized enterprises are particularly attracted to managed cloud data protection services that eliminate substantial capital investments while improving resilience against cyber threats.

Market Drivers

Rising ransomware attacks are redefining enterprise resilience strategies

Cyberattacks increasingly target backup repositories to prevent organizations from restoring operations after encryption events. Consequently, enterprises now invest in immutable storage, isolated recovery environments, continuous replication, and automated recovery verification rather than relying solely on conventional backup systems. Vendors have responded by embedding cyber recovery features directly into enterprise backup platforms, strengthening customer retention while expanding recurring software revenues.

Hybrid cloud adoption is increasing demand for unified protection platforms

Organizations rarely operate within a single infrastructure environment. Critical applications frequently span private data centers, public cloud platforms, SaaS applications, and edge computing resources. This operational model encourages procurement of integrated data protection solutions capable of delivering centralized governance across heterogeneous environments. Buyers increasingly prioritize platforms supporting workload mobility without requiring multiple management interfaces or separate licensing structures.

Regulatory compliance is expanding enterprise investment

Data governance regulations require organizations to demonstrate secure storage, controlled access, retention management, and rapid recovery of critical information. Financial institutions, healthcare providers, public agencies, and multinational corporations therefore allocate higher budgets toward data protection technologies capable of simplifying audits and documenting compliance. Suppliers increasingly differentiate themselves by integrating policy enforcement, reporting, encryption, and long-term archival capabilities within their product portfolios.

Growth in enterprise data volumes is increasing infrastructure requirements

Machine-generated information, connected devices, customer analytics, enterprise applications, and multimedia content continue expanding storage requirements across industries. Protecting these workloads requires scalable architectures capable of supporting petabyte-scale environments without compromising recovery performance. Organizations therefore seek solutions emphasizing automation, storage efficiency, deduplication, and intelligent workload prioritization to manage long-term operational costs.

Market Restraints and Challenges

Complex hybrid environments increase implementation difficulty

Many organizations operate legacy applications alongside modern cloud-native workloads, creating interoperability challenges during deployment. Protecting diverse operating systems, virtual machines, containers, databases, and SaaS applications often requires extensive configuration and integration work. This complexity extends implementation timelines and increases professional service expenditures, particularly for multinational enterprises.

Budget constraints affect adoption among smaller organizations

Although cybersecurity awareness continues improving, many small and medium-sized enterprises remain constrained by limited technology budgets and shortages of experienced security personnel. Subscription pricing has improved accessibility, yet organizations frequently postpone comprehensive deployment until regulatory requirements or cybersecurity incidents justify additional expenditure. Managed services partially address this limitation but introduce ongoing operational costs.

Data sovereignty requirements complicate multinational operations

Cross-border data transfer restrictions require enterprises to maintain localized storage and recovery capabilities across multiple jurisdictions. Organizations operating internationally must align backup architectures with country-specific regulatory frameworks while maintaining operational consistency. This increases infrastructure investment and administrative complexity, particularly for industries handling sensitive customer or government information.

Skills shortages limit operational effectiveness

Successful deployment requires expertise spanning cybersecurity, cloud infrastructure, storage architecture, disaster recovery planning, and regulatory compliance. Many organizations experience shortages of qualified professionals capable of designing and maintaining resilient protection strategies. Vendors increasingly address this challenge through automation, managed services, and simplified administration interfaces, although implementation expertise remains an important procurement consideration.

Major Segment Analysis

Cloud Deployment

Cloud deployment represents the most commercially influential segment because enterprises increasingly seek scalable protection strategies aligned with evolving infrastructure models. Rather than replacing on-premises environments entirely, organizations are adopting hybrid architectures where backup, disaster recovery, and archival workloads are distributed across multiple locations. Cloud-native protection platforms provide operational flexibility while supporting centralized policy management, automated scaling, and geographic redundancy.

Procurement decisions within this segment emphasize security architecture, workload portability, recovery speed, encryption, API integration, and predictable subscription pricing. Buyers also assess vendor support for public cloud platforms, Kubernetes environments, Microsoft 365, enterprise databases, and virtualized infrastructure. Vendors compete by expanding ecosystem compatibility while integrating ransomware detection, immutable storage, and orchestration capabilities that reduce administrative complexity.

Commercially, cloud deployment supports recurring revenue through subscription licensing, managed recovery services, and continuous software updates. This consumption model also encourages stronger long-term customer relationships because enterprises increasingly rely on providers for ongoing operational resilience rather than periodic software upgrades.

Regional Analysis

North America represents the largest regional market due to mature enterprise cybersecurity investment, widespread hybrid cloud deployment, and comprehensive regulatory oversight. Financial institutions, healthcare organizations, telecommunications providers, and federal agencies continue modernizing backup infrastructure to strengthen operational resilience against cyber threats. Procurement increasingly favors integrated cyber recovery capabilities instead of standalone backup products.

Europe demonstrates sustained demand driven by strict privacy legislation, cybersecurity directives, and enterprise modernization initiatives. Organizations emphasize data governance, encryption, localized storage, and audit readiness when selecting suppliers. Manufacturing, financial services, and public administration remain major investment sectors, although economic uncertainty influences procurement timing across certain industries.

Asia Pacific presents substantial commercial opportunities supported by expanding cloud adoption, digital banking, manufacturing automation, and government-led digital economy initiatives. Enterprises throughout China, India, Japan, Australia, and Southeast Asia continue investing in resilient infrastructure to support growing digital workloads. However, varying regulatory frameworks and uneven cybersecurity maturity require vendors to tailor regional deployment strategies.

Middle East and Africa continue strengthening cybersecurity investment as governments expand national digital infrastructure and critical sectors modernize technology environments. Banking, energy, telecommunications, and public administration remain important demand centers. Budget limitations and specialist workforce shortages continue influencing deployment pace in several developing economies.

South America is experiencing gradual adoption as financial institutions, retailers, and telecommunications providers strengthen disaster recovery capabilities and regulatory compliance. Brazil remains the largest regional opportunity due to its sizeable enterprise sector and growing investment in cloud infrastructure. Economic volatility continues influencing purchasing cycles across portions of the region.

Competitive Landscape

Competition is characterized by broad enterprise technology providers competing alongside specialized backup and cybersecurity vendors. Suppliers differentiate themselves through workload coverage, recovery performance, cloud integration, ransomware resilience, storage efficiency, and centralized management capabilities rather than solely on backup functionality.

Strategic partnerships with hyperscale cloud providers, managed service providers, and infrastructure vendors remain an important competitive strategy because enterprise customers increasingly require integrated deployment models. Subscription licensing, software-as-a-service offerings, and managed recovery services continue reshaping revenue structures while improving long-term customer retention.

Artificial intelligence capabilities, workload automation, threat intelligence integration, and cyber recovery orchestration are becoming stronger sources of differentiation. Vendors are also expanding geographic presence through regional cloud infrastructure, channel partnerships, and localized compliance capabilities to address country-specific regulatory requirements.

Companies active within the competitive landscape include IBM, Oracle Corporation, Broadcom Inc., Forcepoint, McAfee, LLC, Acronis International GmbH, Hewlett Packard Enterprise Development LP, Palo Alto Networks, Veeam Software, Thales, NetApp, Inc., Quest Software, and Sophos.

Recent Developments

February 2026: N-able expanded Cove Data Protection with new Anomaly Detection capabilities that identify suspicious backup policy changes in real time, helping organizations detect identity-based attacks before ransomware compromises backup environments.

January 2026: Druva introduced Threat Watch, an automated cloud-native capability that continuously scans backup data for dormant threats and indicators of compromise, enabling faster incident response and more reliable cyber recovery.

November 2025: Veeam Software expanded ransomware recovery and cloud-native workload protection capabilities across enterprise environments. The enhancement supports organizations adopting hybrid infrastructure while improving recovery confidence.

Regulatory and Policy Environment

The regulatory environment increasingly influences enterprise procurement decisions. Privacy legislation, cybersecurity regulations, financial supervisory requirements, and healthcare data protection rules require organizations to maintain secure storage, documented recovery procedures, encryption, and controlled access throughout the information lifecycle. Compliance obligations increasingly extend to cloud providers and outsourced service partners, requiring transparent governance frameworks and auditable operational controls.

International standards such as ISO/IEC 27001, ISO/IEC 27701, the NIST Cybersecurity Framework, sector-specific resilience requirements, and national cybersecurity strategies continue shaping enterprise investment priorities. Governments are also expanding cyber resilience expectations for critical infrastructure operators, encouraging adoption of continuous backup verification, disaster recovery testing, and incident reporting capabilities.

Outlook and Strategic Implications

Enterprise investment over the 2026–2031 period is expected to prioritize cyber resilience rather than conventional backup modernization. Procurement decisions will increasingly evaluate recovery assurance, operational automation, cloud interoperability, and compliance management within unified platforms. Organizations are likely to favor suppliers capable of reducing administrative complexity while supporting heterogeneous infrastructure across on-premises, cloud, edge, and SaaS environments.

Artificial intelligence will play a growing operational role by improving anomaly detection, policy optimization, capacity planning, and recovery orchestration. Managed services are expected to capture additional demand from organizations addressing cybersecurity workforce shortages, while larger enterprises will continue investing in integrated platforms combining backup, disaster recovery, cyber recovery, and governance capabilities.

Competitive differentiation will increasingly depend on measurable recovery performance, ransomware resilience, ecosystem integration, regulatory support, and operational simplicity rather than storage capacity alone. Suppliers capable of combining strong cybersecurity capabilities with scalable hybrid cloud architectures and predictable subscription pricing are likely to strengthen long-term enterprise relationships as data protection continues evolving into a core component of organizational resilience strategies.

Data Protection Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 80.7 billion |

| Total Market Size in 2031 | USD 148.0 billion |

| Forecast Unit | Billion |

| Growth Rate | 12.9% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Deployment, Enterprise Size, End User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

- Solutions

- Services

- Professional Services

- Managed Services

By Deployment

- On-Premises

- Cloud

By Enterprise Size

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

By End User

- BFSI

- Healthcare

- IT and Telecommunications

- Retail and Consumer Goods

- Media and Entertainment

- Manufacturing

- Government and Public Sector

- Education

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Thailand

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits for the Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

3.2. Analyst View

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of New Entrants

4.3.4. Threat of Substitutes

4.3.5. Competitive Rivalry in the Industry

4.4. Industry Value Chain Analysis

5. DATA PROTECTION MARKET BY COMPONENT

5.1. Introduction

5.2. Solutions

5.3. Services

5.3.1. Professional Services

5.3.2. Managed Services

6. DATA PROTECTION MARKET BY DEPLOYMENT

6.1. Introduction

6.2. On-Premises

6.3. Cloud

7. DATA PROTECTION MARKET BY ENTERPRISE SIZE

7.1. Introduction

7.2. Small and Medium-sized Enterprises (SMEs)

7.3. Large Enterprises

8. DATA PROTECTION MARKET BY END USER

8.1. Introduction

8.2. BFSI

8.3. Healthcare

8.4. IT and Telecommunications

8.5. Retail and Consumer Goods

8.6. Media and Entertainment

8.7. Manufacturing

8.8. Government and Public Sector

8.9. Education

8.10. Others

9. DATA PROTECTION MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. United States

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. United Kingdom

9.4.2. Germany

9.4.3. France

9.4.4. Italy

9.4.5. Spain

9.4.6. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. United Arab Emirates

9.5.3. South Africa

9.5.4. Others

9.6. Asia Pacific

9.6.1. China

9.6.2. Japan

9.6.3. India

9.6.4. South Korea

9.6.5. Australia

9.6.6. Indonesia

9.6.7. Thailand

9.6.8. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. IBM

11.2. Oracle Corporation

11.3. Broadcom Inc.

11.4. Forcepoint

11.5. McAfee, LLC

11.6. Acronis International GmbH

11.7. Hewlett Packard Enterprise Development LP

11.8. Palo Alto Networks

11.9. Veeam Software

11.10. Thales

11.11. NetApp, Inc.

11.12. Quest Software

11.13. Sophos

Navigate

Trusted by the world's leading organizations