Report Overview

The federated learning market is anticipated to expand at a high CAGR over the forecast period.

Highlights:

- 1Privacy regulations and restrictions on centralized data sharing remain the principal demand catalyst across regulated industries.

- 2Software platforms account for the largest commercial opportunity due to recurring licensing and platform subscription revenues.

- 3Healthcare, financial services, and public-sector organizations represent the most active enterprise buyers.

- 4Integration of confidential computing, differential privacy, and secure multiparty computation is strengthening enterprise adoption.

- 5Asia Pacific presents considerable long-term opportunity as governments invest in sovereign AI capabilities and domestic digital infrastructure.

- 6Competition increasingly centers on interoperability, enterprise AI integration, deployment simplicity, and compliance capabilities rather than standalone algorithm performance.

The federated learning market comprises software platforms, orchestration frameworks, privacy-preserving algorithms, deployment services, and supporting infrastructure that enable machine learning models to be trained across decentralized datasets without transferring raw data to a centralized repository. Instead of aggregating sensitive information, federated learning exchanges model parameters, allowing organizations to build collaborative artificial intelligence (AI) models while maintaining data ownership and regulatory compliance. The technology has moved beyond academic research into commercial deployments across highly regulated industries where data privacy, security, and governance influence technology procurement decisions.

Demand is primarily driven by enterprises seeking to improve AI model accuracy while complying with increasingly stringent privacy regulations. Organizations managing distributed datasets particularly banks, healthcare providers, telecommunications operators, manufacturers, and public agencies are evaluating federated learning to address restrictions on cross-border data transfers and internal governance requirements. Buyers increasingly prioritize platforms that integrate with existing AI pipelines, support heterogeneous computing environments, and provide explainability, model governance, and audit capabilities alongside privacy protection.

Commercial adoption remains strongest among large enterprises because they possess extensive distributed data assets, established AI teams, and sufficient computing infrastructure to justify implementation costs. However, software vendors are introducing managed services and cloud-native deployment models that lower operational complexity, making the technology increasingly accessible to small and medium-sized enterprises.

Software constitutes the core revenue stream, while professional services continue to expand as organizations require implementation support, model optimization, cybersecurity assessments, compliance consulting, and workforce training. Enterprise purchasing decisions increasingly consider interoperability with existing cloud platforms, cybersecurity frameworks, and regulatory reporting capabilities rather than model performance alone.

Competitive activity reflects broader developments in enterprise AI. Cloud providers, semiconductor companies, enterprise software vendors, and specialist federated learning firms compete by improving scalability, supporting confidential computing, integrating privacy-enhancing technologies, and simplifying deployment across hybrid and multi-cloud environments. Partnerships between AI platform providers, healthcare organizations, financial institutions, and research networks are also expanding commercial opportunities.

Market Drivers

Growing regulatory emphasis on data privacy

Organizations increasingly face legal obligations governing personal data processing under regulations such as the European Union's General Data Protection Regulation (GDPR), sector-specific healthcare regulations, and financial supervisory requirements. Many enterprises cannot legally consolidate customer information into centralized repositories, particularly when operations span multiple jurisdictions.

Federated learning addresses this constraint by enabling collaborative model training while retaining data locally. Buyers therefore view the technology as an investment that supports AI adoption without substantially altering existing data governance policies. Vendors have responded by embedding encryption, secure aggregation, audit logging, and policy management into commercial platforms, improving enterprise procurement confidence.

Expansion of AI deployment across distributed enterprise operations

Large organizations generate operational data across numerous branches, manufacturing facilities, hospitals, retail stores, and edge devices. Traditional centralized AI development often creates bottlenecks associated with bandwidth, storage, and regulatory approvals.

Federated learning enables these organizations to utilize geographically dispersed datasets while minimizing network transfers. This capability is particularly valuable for multinational enterprises seeking consistent AI model performance across multiple operating regions without compromising local compliance obligations.

Rising investment in healthcare AI and collaborative research

Healthcare organizations continue to increase investment in AI-assisted diagnostics, clinical decision support, medical imaging, and pharmaceutical research. However, hospitals frequently face legal and ethical barriers preventing patient-level data sharing.

Federated learning enables institutions to jointly develop AI models while maintaining patient confidentiality. Pharmaceutical companies, academic medical centers, and healthcare networks increasingly consider federated learning as a practical mechanism for expanding datasets without introducing substantial compliance risk. This improves commercial demand for specialized healthcare implementations and associated consulting services.

Enterprise focus on cybersecurity and confidential computing

Cybersecurity has become an important procurement criterion for enterprise AI initiatives. Organizations increasingly recognize that centralized data lakes create attractive targets for cyberattacks.

Federated learning reduces centralized exposure while complementing technologies such as confidential computing, trusted execution environments, secure enclaves, and homomorphic encryption. Enterprise software suppliers are incorporating these capabilities into broader AI governance portfolios, strengthening purchasing interest among security-conscious industries.

Market Restraints and Challenges

High implementation complexity

Deploying federated learning requires coordination across distributed computing environments, standardized data structures, secure communications, and continuous model synchronization. Organizations with fragmented IT environments often require extensive infrastructure modernization before implementation.

This increases deployment costs and lengthens procurement cycles, particularly among organizations with limited AI expertise. Technology providers increasingly offer managed services, standardized APIs, and cloud-native deployment options to reduce implementation complexity.

Data heterogeneity affecting model performance

Enterprise datasets frequently differ in structure, quality, labeling standards, and operational processes across locations. Non-uniform data distributions may reduce model convergence and prediction accuracy.

Organizations therefore invest in data governance, metadata management, and standardized model validation before large-scale deployment. Vendors compete by providing automated quality assessment and adaptive federated optimization techniques that improve performance across heterogeneous environments.

Computing infrastructure requirements

Although federated learning reduces centralized data movement, participating endpoints require sufficient computational capacity to execute local model training. Infrastructure limitations remain particularly relevant for smaller organizations and edge environments with constrained processing resources.

Cloud-based orchestration services and hardware acceleration continue to reduce these limitations, but infrastructure investment remains an important purchasing consideration.

Limited availability of specialized expertise

Successful deployment requires knowledge spanning machine learning, distributed systems, cybersecurity, privacy engineering, and regulatory compliance. The limited availability of multidisciplinary talent increases consulting costs and slows implementation.

Software providers increasingly respond through automation, low-code deployment tools, preconfigured industry templates, and training programs designed to simplify enterprise adoption.

Major Segment Analysis

Software

Software represents the largest commercially significant segment because it forms the operational foundation for federated model development, orchestration, security management, governance, monitoring, and deployment. Organizations increasingly seek integrated platforms rather than standalone algorithms, creating recurring revenue opportunities through licensing and cloud subscriptions.

Enterprise buyers prioritize compatibility with existing AI frameworks, cloud environments, container orchestration platforms, and cybersecurity infrastructure. Procurement decisions increasingly evaluate scalability across multiple jurisdictions, centralized policy management, explainable AI capabilities, model version control, and regulatory reporting functions.

Competition within the software segment increasingly emphasizes ease of deployment, interoperability, and lifecycle management rather than raw computational performance. Vendors capable of supporting hybrid cloud architectures, confidential computing, automated compliance documentation, and enterprise-grade security certifications gain competitive differentiation. As organizations expand production AI workloads, software platforms remain the primary commercial interface through which federated learning capabilities are delivered and monetized.

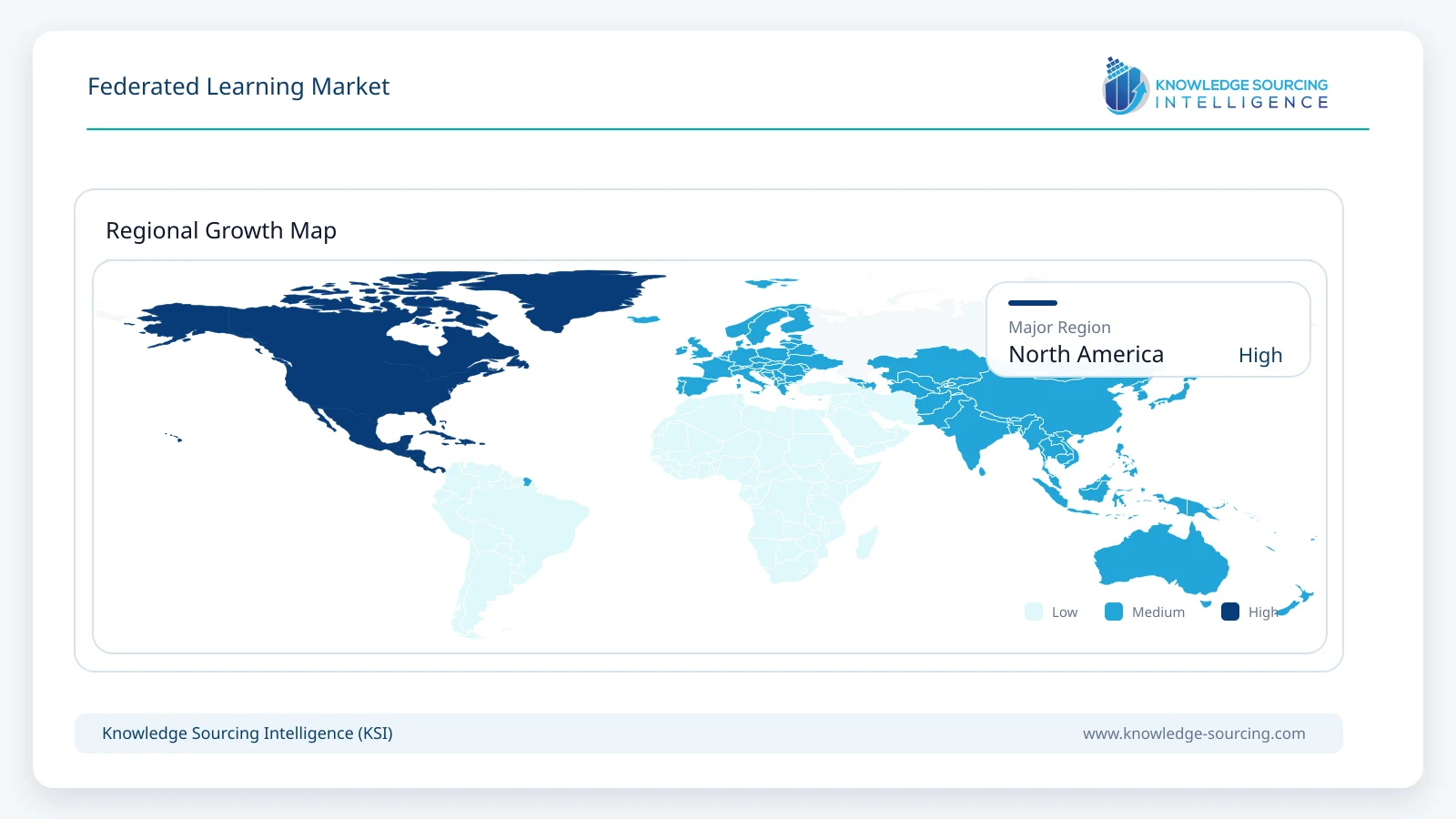

Regional Analysis

North America remains the largest commercial market due to advanced AI adoption, mature cloud infrastructure, substantial enterprise technology spending, and significant investment from hyperscale cloud providers and semiconductor companies. Healthcare networks, financial institutions, and technology companies continue to evaluate federated learning for privacy-sensitive AI applications. Strong venture capital investment and university research further support commercialization.

Europe demonstrates sustained demand driven by comprehensive privacy legislation, cross-border data governance requirements, and public investment in trustworthy AI. Enterprises increasingly prioritize compliance-oriented AI architectures that reduce legal exposure while supporting collaborative analytics across member states. Healthcare and manufacturing sectors remain important adopters.

Asia Pacific is expected to experience strong commercial expansion as governments strengthen domestic AI capabilities, semiconductor investment, digital infrastructure, and industrial automation. China, Japan, South Korea, Singapore, Australia, and India continue investing in AI research, healthcare modernization, and smart manufacturing, creating favorable conditions for federated learning deployment. National approaches emphasizing data sovereignty further reinforce adoption.

Middle East & Africa represents an emerging opportunity supported by digital government initiatives, healthcare modernization, financial technology expansion, and national AI strategies. Adoption remains concentrated among government agencies, telecommunications operators, and large enterprises, while workforce capability and infrastructure maturity continue to influence implementation speed.

South America shows gradual adoption, led by financial institutions, telecommunications providers, and public-sector digitalization initiatives. Budget constraints, uneven AI maturity, and infrastructure limitations continue to moderate deployment, although cloud adoption is improving accessibility for enterprise customers.

Competitive Landscape

Competition combines global enterprise technology companies with specialized federated learning providers. NVIDIA Corporation, IBM Corporation, Microsoft Corporation, Google LLC, Intel Corporation, Cloudera, Inc., Owkin, Inc., Apheris AI GmbH, FedML, Inc., and Sherpa.ai compete through platform integration, AI ecosystem development, privacy-enhancing technologies, and industry-specific deployment capabilities.

Competitive differentiation increasingly depends on secure orchestration, compatibility with enterprise AI frameworks, hybrid cloud deployment, governance capabilities, and support for confidential computing environments. Strategic partnerships with hospitals, financial institutions, research organizations, cloud providers, and system integrators remain an important route to commercial expansion. Vendors also compete by strengthening developer ecosystems, expanding managed services, and integrating federated learning into broader enterprise AI portfolios.

Recent Developments

June 2026: Rhino Federated Computing showcased its federated learning platform at the 2026 DIA Global Annual Meeting, demonstrating how decentralized AI can accelerate clinical trials while keeping sensitive healthcare data within participating organizations.

March 2026: NVIDIA highlighted expanded enterprise and healthcare AI workflows using NVIDIA FLARE during GTC 2026, demonstrating privacy-preserving federated learning for multi-institution AI development without centralized data sharing.

October 2025: Microsoft introduced additional confidential computing and enterprise AI capabilities within Azure designed to strengthen privacy-preserving machine learning environments. Commercial relevance: improves enterprise confidence in regulated AI deployments.

June 2025: Owkin expanded collaborative AI research initiatives with healthcare institutions to advance federated learning applications in medical research and clinical model development. Commercial relevance: demonstrates continued commercialization of privacy-preserving healthcare AI.

Regulatory and Policy Environment

Regulatory developments increasingly shape enterprise purchasing decisions in the federated learning market. The European Union's GDPR continues to encourage privacy-preserving AI architectures by limiting unnecessary movement of personal data across organizational boundaries. The EU Artificial Intelligence Act introduces additional governance expectations for high-risk AI systems, increasing demand for transparent and auditable AI development practices.

Healthcare organizations operate under national health information privacy requirements, encouraging technologies that minimize patient data exposure during AI model development. Financial regulators similarly emphasize operational resilience, cybersecurity, data governance, and model risk management, encouraging stronger AI governance frameworks.

Governments across Asia Pacific are investing in sovereign AI capabilities while introducing domestic data governance policies that encourage localized processing of sensitive information. These initiatives strengthen commercial demand for federated learning by supporting AI innovation without requiring unrestricted cross-border data transfers.

Industry standards addressing cybersecurity, information security management, cloud security, and AI governance continue influencing procurement requirements, particularly among large enterprises and government organizations.

Outlook and Strategic Implications

The commercial outlook for federated learning remains closely linked to enterprise AI expansion, evolving privacy regulations, and increasing investment in trustworthy AI infrastructure. Organizations are expected to prioritize platforms that combine federated learning with confidential computing, synthetic data generation, explainable AI, and automated governance rather than purchasing standalone privacy technologies.

Procurement strategies are expected to emphasize interoperability with existing cloud environments, enterprise security frameworks, and AI lifecycle management platforms. Buyers will increasingly evaluate total implementation cost, deployment speed, regulatory reporting capabilities, and operational scalability alongside model performance.

Technology suppliers are likely to expand managed services, industry-specific software packages, and strategic partnerships with cloud providers and system integrators to address implementation complexity. Continued investment in hardware acceleration, secure orchestration, and standardized deployment frameworks should improve commercial accessibility across a broader range of enterprise customers.

Despite challenges related to infrastructure readiness, technical expertise, and data heterogeneity, federated learning is expected to become an important architectural component of enterprise AI strategies as organizations seek to balance analytical performance with regulatory compliance, cybersecurity, and long-term data governance objectives.

Federated Learning Market Scope

| Report Metric | Details |

|---|---|

| Forecast Unit | Billion |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Component, Enterprise Size, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Component

By Enterprise Size

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. FEDERATED LEARNING MARKET BY COMPONENT

5.1. Introduction

5.2. Software

5.3. Services

6. FEDERATED LEARNING MARKET BY ENTERPRISE SIZE

6.1. Introduction

6.2. Large Enterprises

6.3. Small and Medium Enterprises

7. FEDERATED LEARNING MARKET BY END-USER

7.1. Introduction

7.2. Banking, Financial Services, and Insurance (BFSI)

7.3. Healthcare and Life Sciences

7.4. IT and Telecommunication

7.5. Retail and E-commerce

7.6. Automotive

7.7. Manufacturing

7.8. Government and Public Sector

7.9. Others

8. FEDERATED LEARNING MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. United States

8.2.2. Canada

8.2.3. Mexico

8.3. South America

8.3.1. Brazil

8.3.2. Argentina

8.3.3. Others

8.4. Europe

8.4.1. United Kingdom

8.4.2. Germany

8.4.3. France

8.4.4. Italy

8.4.5. Spain

8.4.6. Others

8.5. Middle East & Africa

8.5.1. Saudi Arabia

8.5.2. UAE

8.5.3. South Africa

8.5.4. Others

8.6. Asia Pacific

8.6.1. China

8.6.2. India

8.6.3. Japan

8.6.4. South Korea

8.6.5. Australia

8.6.6. Singapore

8.6.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. NVIDIA Corporation

10.2. IBM Corporation

10.3. Microsoft Corporation

10.4. Google LLC

10.5. Intel Corporation

10.6. Cloudera, Inc.

10.7. Owkin, Inc.

10.8. Apheris AI GmbH

10.9. FedML, Inc.

10.10. Sherpa.ai

11. APPENDIX

11.1. Currency

11.2. Assumptions

11.3. Base and Forecast Years Timeline

11.4. Key Benefits for Stakeholders

11.5. Research Methodology

11.6. Abbreviations

Navigate

Trusted by the world's leading organizations