Report Overview

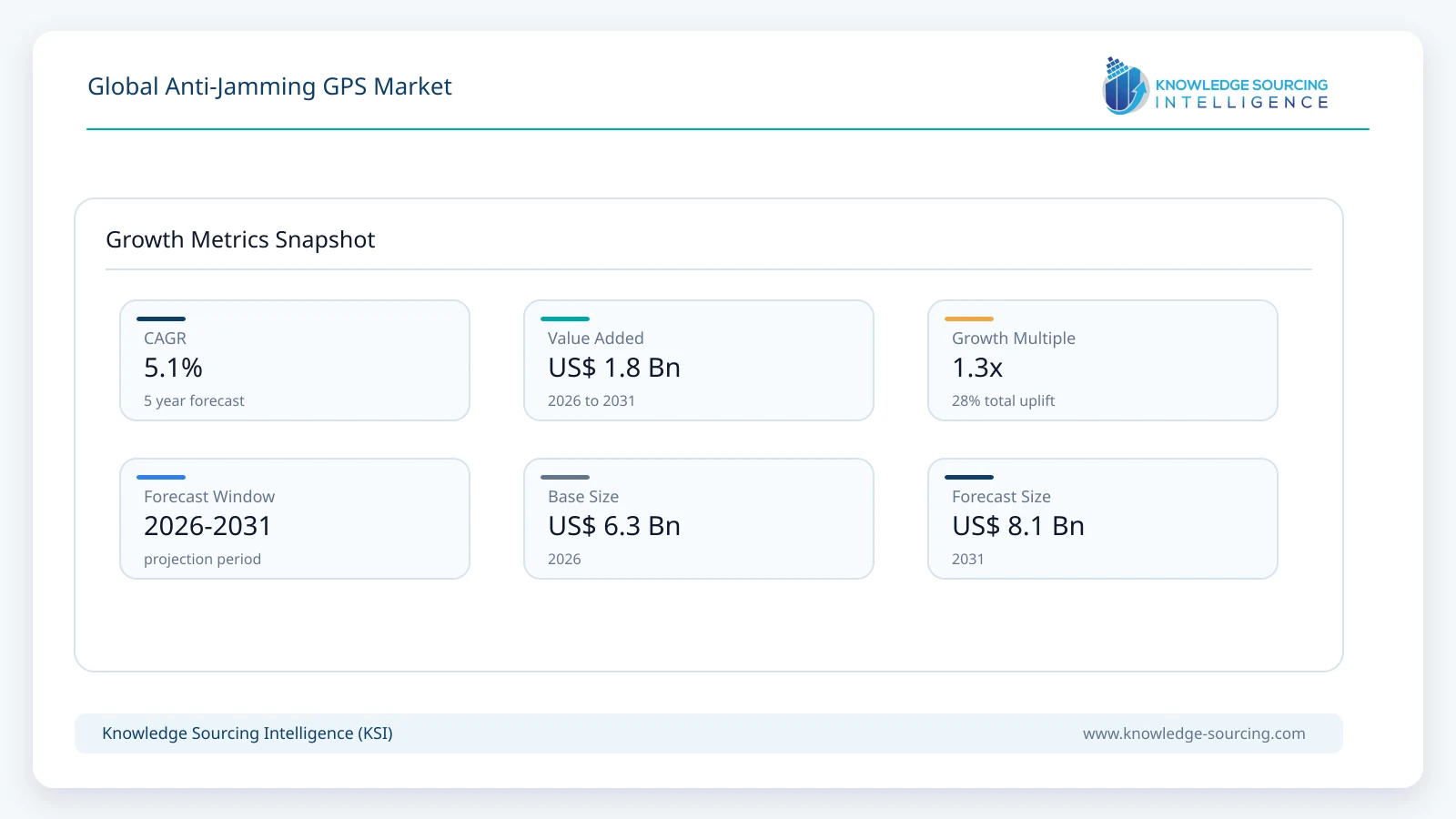

The global anti-jamming GPS market is forecast to grow at a CAGR of 5.14%, reaching USD 8.08 billion in 2031 from USD 6.29 billion in 2026.

Highlights:

- 1Military modernization and electronic warfare preparedness remain the primary demand catalyst for anti-jamming GPS technologies.

- 2Military and Government Grade receivers represent the leading commercial segment due to stringent operational reliability requirements.

- 3North America continues to account for substantial procurement activity through sustained defense modernization and resilient PNT investments.

- 4Controlled Reception Pattern Antenna (CRPA) technology is receiving strong adoption for its ability to suppress multiple interference sources simultaneously.

- 5Defense procurement regulations and aviation certification standards continue to shape product development and supplier qualification.

- 6Competition increasingly depends on integration capability, multi-constellation compatibility, platform certification, and long-term support services.

The anti-jamming GPS market comprises hardware and software solutions designed to maintain reliable Global Positioning System (GPS) or Global Navigation Satellite System (GNSS) performance in environments affected by intentional jamming, unintentional radio-frequency interference, or electronic warfare. These solutions include controlled reception pattern antennas (CRPA), beam steering technologies, nulling systems, signal processing algorithms, and integrated navigation receivers deployed across military, government, commercial aviation, maritime, critical infrastructure, and transportation applications. As reliance on precise Positioning, Navigation, and Timing (PNT) data expands across both defense and civilian operations, anti-jamming capabilities have become an operational requirement rather than an optional enhancement.

Demand is primarily influenced by the growing frequency of GPS interference incidents, modernization of military navigation systems, and expanding dependence on satellite-based navigation for autonomous and connected platforms. Defense organizations remain the largest buyers because electronic warfare has become an integral component of modern military operations. Commercial demand is also increasing as airports, ports, telecommunications operators, energy utilities, and unmanned system operators seek resilient navigation systems capable of maintaining service continuity during interference events.

Buyer priorities have shifted beyond simple positioning accuracy toward resilience, multi-frequency capability, compatibility with multiple satellite constellations, low size, weight, and power (SWaP), cybersecurity integration, and lifecycle support. Procurement decisions are frequently tied to platform modernization programs, long-term maintenance contracts, and interoperability requirements established by military alliances and aviation authorities. Buyers increasingly evaluate suppliers based on certification capability, proven operational performance, integration expertise, and production capacity.

The industry's commercial structure combines large defense electronics manufacturers with specialized GNSS technology developers and antenna manufacturers. Revenue generation is closely linked to defense procurement cycles, aerospace production programs, maritime navigation upgrades, and integration into unmanned platforms. Long qualification periods and stringent certification requirements create high entry barriers, favoring suppliers with established relationships across defense agencies, aircraft manufacturers, and government organizations. Growing investment in resilient PNT infrastructure and multi-layer navigation architectures is further broadening commercial opportunities beyond traditional defense applications.

Market Drivers

Expansion of Electronic Warfare Capabilities

Electronic warfare has become a standard operational component across modern defense forces. Military planners increasingly expect navigation systems to function despite deliberate jamming and spoofing attempts. This requirement has accelerated procurement of anti-jamming GPS receivers for aircraft, armored vehicles, naval vessels, missiles, and unmanned systems.

Defense agencies now prioritize systems capable of operating with multiple satellite constellations while integrating inertial navigation technologies. Suppliers have responded by investing in adaptive antennas, digital beamforming, and advanced signal processing architectures that improve navigation resilience without substantially increasing equipment size or power consumption. Long-term defense modernization programs provide predictable demand while encouraging continuous technology improvements.

Rising Dependence on Positioning, Navigation, and Timing Infrastructure

Critical infrastructure sectors increasingly depend on highly accurate timing and positioning data for communications networks, power grid synchronization, financial transactions, maritime logistics, and aviation operations. Even brief GPS disruption can create operational delays and financial losses.

Infrastructure operators therefore seek navigation systems capable of maintaining operational continuity during interference events. Procurement increasingly favors receivers supporting multi-frequency operation, interference detection, and integration with backup timing technologies. This broader customer base is gradually expanding commercial demand beyond defense procurement.

Growth in Unmanned and Autonomous Platforms

Military drones, autonomous maritime systems, precision-guided munitions, and commercial unmanned aircraft require uninterrupted navigation throughout complex missions. GPS interference can compromise operational safety, mission success, and regulatory compliance.

Platform manufacturers increasingly integrate anti-jamming capability during initial system design rather than offering it as an aftermarket option. This trend supports recurring demand for compact, lightweight receivers and advanced antenna technologies that meet strict payload limitations while delivering reliable navigation performance.

Government Investment in Resilient Navigation Infrastructure

Several governments have increased funding for resilient PNT initiatives that reduce dependence on a single satellite navigation source. Programs supporting alternative navigation systems, multi-GNSS adoption, and enhanced military communications indirectly stimulate investment in anti-jamming technologies.

Government-funded research programs also accelerate commercialization of advanced receiver architectures, digital antennas, and integrated navigation software, creating additional opportunities for technology suppliers.

Market Restraints and Challenges

High Procurement and Integration Costs

Anti-jamming GPS systems incorporate sophisticated antennas, digital processing units, and specialized software, making them considerably more expensive than conventional navigation receivers. Integration costs further increase for legacy military platforms requiring extensive certification and testing.

Budget-constrained organizations may postpone modernization programs, particularly within smaller defense agencies or commercial operators. Manufacturers attempt to address this challenge through modular architectures and scalable product configurations suitable for different operational requirements.

Lengthy Certification and Qualification Processes

Products intended for military aviation, commercial aerospace, or maritime navigation must satisfy demanding certification requirements before deployment. Testing under operational conditions often extends development timelines and delays commercial revenue.

Suppliers with established certification experience possess a competitive advantage, while newer companies encounter substantial barriers when attempting to enter highly regulated markets.

Evolving Jamming and Spoofing Techniques

Electronic threats continue to become more sophisticated, requiring continuous updates to hardware and software capabilities. Solutions that effectively mitigate current interference methods may require upgrades as adversaries adopt more advanced electronic attack techniques.

Manufacturers therefore maintain sustained investment in research and development, increasing operating costs while shortening technology refresh cycles.

Supply Chain Constraints for Specialized Components

Advanced semiconductors, radio-frequency components, precision antennas, and secure electronics remain subject to export controls and limited manufacturing capacity. Extended lead times can delay deliveries for major defense contracts and increase inventory costs.

Suppliers increasingly diversify sourcing strategies and expand regional manufacturing partnerships to improve supply chain resilience.

Major Segment Analysis

Military and Government Grade Receivers

Military and Government Grade receivers represent the most commercially significant segment because operational reliability directly influences mission effectiveness and national security. Unlike commercial navigation equipment, these receivers must continue operating under severe electronic interference while maintaining precise positioning accuracy.

Defense organizations typically procure anti-jamming receivers through multi-year modernization programs covering aircraft, naval vessels, armored vehicles, missile systems, and unmanned platforms. Procurement decisions emphasize validated operational performance, environmental durability, encrypted signal compatibility, multi-frequency capability, and interoperability with allied defense systems.

Competitive differentiation within this segment depends less on hardware specifications alone and more on integration expertise, certification capability, software adaptability, and long-term sustainment support. Suppliers capable of integrating receivers into complex defense platforms while meeting stringent military standards secure stronger contract opportunities. Since procurement programs frequently include maintenance, upgrades, and lifecycle support, recurring service revenue complements initial equipment sales and strengthens supplier profitability.

Regional Analysis

North America

North America remains the leading regional market due to sustained defense modernization programs, extensive aerospace manufacturing, and investment in resilient navigation capabilities. The United States continues to allocate substantial funding toward electronic warfare readiness, advanced military aviation, and secure satellite navigation infrastructure. Commercial aviation, telecommunications, and critical infrastructure operators also invest in resilient PNT technologies as interference incidents receive greater regulatory attention.

Europe

European demand is supported by defense modernization initiatives, NATO interoperability requirements, and heightened attention to navigation resilience. Governments increasingly prioritize secure navigation for military platforms, border surveillance, maritime security, and civil aviation. Regional aerospace manufacturers further contribute to procurement through integration of advanced navigation technologies into new aircraft programs. Budget constraints in some countries remain a limiting factor, although collaborative defense procurement helps support investment.

Asia Pacific

Asia Pacific demonstrates expanding demand due to rising defense expenditures, indigenous aerospace development, and maritime security initiatives. Countries including Japan, South Korea, India, Taiwan, and Australia continue investing in resilient navigation technologies to strengthen operational readiness. China also supports domestic navigation technology development through its broader satellite navigation ecosystem. Expanding unmanned systems production further contributes to regional demand.

Middle East & Africa and South America

Defense procurement remains the principal demand source across these regions. Gulf countries continue upgrading military aviation, missile defense, and surveillance capabilities, supporting purchases of advanced navigation systems. South American demand is comparatively smaller and largely associated with defense modernization and maritime surveillance. Budget limitations and procurement cycles create uneven adoption across individual countries.

Competitive Landscape

Competition within the anti-jamming GPS market combines established global defense contractors with specialized GNSS technology providers possessing expertise in antenna design, receiver engineering, and navigation software. Companies including Hexagon AB, RTX Corporation, NovAtel Inc., Safran Electronics & Defense, Furuno Electric Co., Ltd., L3Harris Technologies, Inc., BAE Systems plc, InfiniDome Ltd., Cobham Aerospace Communications, and Chelton Limited compete through technology performance, certification capability, platform integration expertise, and long-term customer support.

Product differentiation increasingly centers on adaptive antenna performance, multi-frequency reception, multi-constellation compatibility, reduced SWaP characteristics, cybersecurity integration, and interoperability with existing defense architectures. Strategic partnerships with aircraft manufacturers, defense system integrators, and government agencies remain important for securing long-term procurement programs. Geographic expansion increasingly focuses on supporting regional defense modernization initiatives while strengthening manufacturing resilience and localized technical support.

Recent Developments

May 2026: RTX Corporation expanded resilient navigation capabilities within its defense electronics portfolio through enhanced PNT technologies supporting contested operational environments. The development strengthens integrated defense navigation offerings for military procurement.

April 2026: Hexagon completed its acquisition of Inertial Sense on 30 April 2026, expanding its resilient navigation portfolio by integrating advanced inertial navigation technology with GNSS positioning solutions for improved performance in GNSS-denied and jamming-prone environments.

April 2026: Lockheed Martin, SpaceX, and the U.S. Space Force successfully launched GPS III SV10 ("Hedy Lamarr") on 21 April 2026, completing the GPS III constellation and strengthening secure military positioning with advanced anti-jamming M-Code capabilities.

Regulatory and Policy Environment

The regulatory framework governing anti-jamming GPS technologies combines defense procurement standards, aviation certification requirements, spectrum management policies, export controls, and cybersecurity regulations. Military procurement programs require compliance with rigorous defense standards covering environmental performance, electromagnetic compatibility, secure communications, and interoperability.

Civil aviation authorities continue strengthening resilience requirements for navigation infrastructure as GPS interference incidents receive greater operational attention. Telecommunications regulators also monitor radio-frequency interference to protect satellite navigation services. Export control regimes influence international sales of advanced navigation technologies, particularly products with military applications.

Government investment in resilient PNT programs, satellite modernization initiatives, and electronic warfare preparedness continues supporting long-term procurement opportunities. Compliance with evolving regulatory requirements remains essential for suppliers seeking participation in national defense modernization and critical infrastructure projects.

Outlook and Strategic Implications

Demand for anti-jamming GPS technologies is expected to remain closely aligned with defense modernization, resilient infrastructure investment, and wider deployment of autonomous platforms. Procurement priorities will increasingly favor integrated navigation solutions capable of combining multiple satellite constellations, inertial navigation, interference detection, and secure software architectures within compact system designs.

Manufacturers are expected to prioritize adaptive antenna technologies, artificial intelligence-assisted signal processing, improved cybersecurity protection, and modular receiver architectures supporting rapid platform integration. Long-term contracts incorporating maintenance, software upgrades, and lifecycle support are likely to become more valuable components of supplier revenue models.

Competition will increasingly emphasize engineering capability, certification experience, supply chain resilience, and integration expertise rather than hardware specifications alone. Organizations capable of delivering resilient navigation systems that satisfy evolving defense, aerospace, maritime, and critical infrastructure requirements while maintaining compliance with international regulatory standards will be best positioned to benefit from procurement activity over the coming years.

Anti-Jamming GPS Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 6.29 billion |

| Total Market Size in 2031 | USD 8.08 billion |

| Forecast Unit | Billion |

| Growth Rate | 5.14% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Receiver Type, Technology, Application, End User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Receiver Type

- Commercial and Transportation Grade

- Military and Government Grade

By Technology

- Beam Steering Technique

- Controlled Reception Pattern Antenna (CRPA)

- Nulling Technique

By Application

- Surveillance and Reconnaissance

- Flight Control

- Position, Navigation, and Timing (PNT)

- Others

By End User

- Military

- Civilian

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- UK

- Germany

- France

- Italy

- Others

- Middle East and Africa

- Saudi Arabia

- South Africa

- Others

- Asia Pacific

- Japan

- China

- India

- South Korea

- Taiwan

- Thailand

- Indonesia

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Market Segmentation

1.4. Research Scope

2. RESEARCH METHODOLOGY

2.1. Research Data

2.2. Assumptions

3. EXECUTIVE SUMMARY

3.1. Research Highlights

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Market Opportunities

4.4. Porter Five Forces Analysis

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Power of Buyers

4.4.3. Threat of Substitutes

4.4.4. Threat of New Entrants

4.4.5. Competitive Rivalry in the Industry

4.5. Industry Value Chain Analysis

5. GLOBAL ANTI-JAMMING GPS MARKET BY RECEIVER TYPE

5.1. Introduction

5.2. Commercial and Transportation Grade

5.3. Military and Government Grade

6. GLOBAL ANTI-JAMMING GPS MARKET BY TECHNOLOGY

6.1. Introduction

6.2. Beam Steering Technique

6.3. Controlled Reception Pattern Antenna (CRPA)

6.4. Nulling Technique

7. GLOBAL ANTI-JAMMING GPS MARKET BY APPLICATION

7.1. Introduction

7.2. Surveillance and Reconnaissance

7.3. Flight Control

7.4. Position, Navigation, and Timing (PNT)

7.5. Others

8. GLOBAL ANTI-JAMMING GPS MARKET BY END USER

8.1. Introduction

8.2. Military

8.3. Civilian

9. GLOBAL ANTI-JAMMING GPS MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. North America Anti-Jamming GPS Market, By Receiver Type

9.2.2. North America Anti-Jamming GPS Market, By Technology

9.2.3. North America Anti-Jamming GPS Market, By Application

9.2.4. North America Anti-Jamming GPS Market, By End User

9.2.5. By Country

9.2.5.1. United States

9.2.5.2. Canada

9.2.5.3. Mexico

9.3. South America

9.3.1. South America Anti-Jamming GPS Market, By Receiver Type

9.3.2. South America Anti-Jamming GPS Market, By Technology

9.3.3. South America Anti-Jamming GPS Market, By Application

9.3.4. South America Anti-Jamming GPS Market, By End User

9.3.5. By Country

9.3.5.1. Brazil

9.3.5.2. Argentina

9.3.5.3. Others

9.4. Europe

9.4.1. Europe Anti-Jamming GPS Market, By Receiver Type

9.4.2. Europe Anti-Jamming GPS Market, By Technology

9.4.3. Europe Anti-Jamming GPS Market, By Application

9.4.4. Europe Anti-Jamming GPS Market, By End User

9.4.5. By Country

9.4.5.1. UK

9.4.5.2. Germany

9.4.5.3. France

9.4.5.4. Italy

9.4.5.5. Others

9.5. Middle East and Africa

9.5.1. Middle East and Africa Anti-Jamming GPS Market, By Receiver Type

9.5.2. Middle East and Africa Anti-Jamming GPS Market, By Technology

9.5.3. Middle East and Africa Anti-Jamming GPS Market, By Application

9.5.4. Middle East and Africa Anti-Jamming GPS Market, By End User

9.5.5. By Country

9.5.5.1. Saudi Arabia

9.5.5.2. South Africa

9.5.5.3. Others

9.6. Asia Pacific

9.6.1. Asia Pacific Anti-Jamming GPS Market, By Receiver Type

9.6.2. Asia Pacific Anti-Jamming GPS Market, By Technology

9.6.3. Asia Pacific Anti-Jamming GPS Market, By Application

9.6.4. Asia Pacific Anti-Jamming GPS Market, By End User

9.6.5. By Country

9.6.5.1. Japan

9.6.5.2. China

9.6.5.3. India

9.6.5.4. South Korea

9.6.5.5. Taiwan

9.6.5.6. Thailand

9.6.5.7. Indonesia

9.6.5.8. Others

10. COMPETITIVE INTELLIGENCE

10.1. Major Players and Strategy Analysis

10.2. Emerging Players and Market Attractiveness

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Vendor Competitiveness Matrix

11. COMPANY PROFILES

11.1. Hexagon AB

11.2. RTX Corporation

11.3. NovAtel Inc.

11.4. Safran Electronics & Defense

11.5. Furuno Electric Co., Ltd.

11.6. L3Harris Technologies, Inc.

11.7. BAE Systems plc

11.8. InfiniDome Ltd.

11.9. Cobham Aerospace Communications

11.10. Chelton Limited

Navigate

Trusted by the world's leading organizations