Report Overview

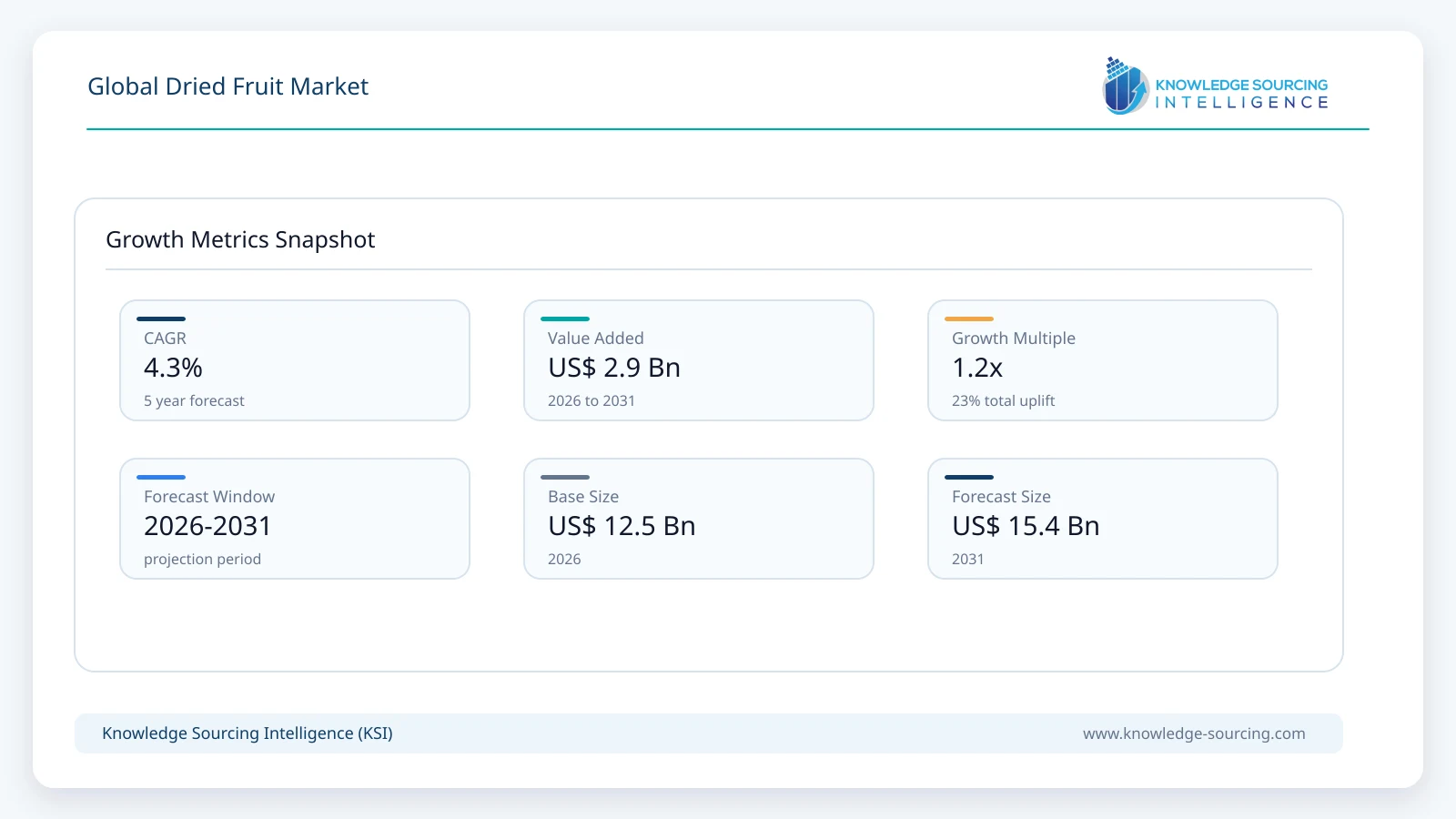

The Global Dried Fruit Market is set to grow at a CAGR of 4.26%, moving from USD 12.50 billion in 2026 to USD 15.40 billion by 2031.

Highlights:

- 1Rising consumer preference for healthy and convenient snack products continues to stimulate dried fruit consumption.

- 2Raisinsremain the largest product segment because of their extensive use in bakery, breakfast cereals, snacks, and confectionery.

- 3Asia Pacific and Europe represent important consumption markets driven by expanding packaged food industries and changing dietary preferences.

- 4Advanced dehydration, optical sorting, and packaging technologies are improving product quality and shelf stability.

- 5Food safety regulations and traceability requirements increasingly influence procurement decisions among retailers and food manufacturers.

- 6Competition is based on sourcing capability, product quality, processing efficiency, certification standards, and distribution reach.

The dried fruit market comprises fruits that undergo controlled dehydration to extend shelf life while retaining much of their nutritional value, flavor, and functionality. Common products include raisins, dates, apricots, prunes, figs, and other specialty dried fruits supplied to retail consumers and food manufacturers. Commercial demand extends across bakery and confectionery, breakfast cereals, dairy products, snack bars, desserts, and foodservice applications. Unlike fresh fruit, dried fruit offers longer storage stability, reduced transportation costs per edible unit, and year-round availability, making it an important ingredient in global food supply chains.

Demand is supported by changing dietary preferences, rising consumption of convenient nutrient-dense snacks, and increasing use of natural ingredients in packaged foods. Food manufacturers procure dried fruits as functional ingredients that provide natural sweetness, dietary fiber, texture, and micronutrients while reducing dependence on refined sugar in selected formulations. Retail consumers increasingly purchase dried fruits for home consumption because they require no refrigeration, have a long shelf life, and align with preferences for minimally processed foods.

The bakery and snack industries remain the largest commercial buyers. Dried fruits improve moisture retention, product texture, flavor, and visual appeal while supporting clean-label product positioning. Breakfast cereal manufacturers also utilize raisins, dates, and dried berries to enhance nutritional value and product differentiation. Purchasing decisions among industrial buyers depend on product consistency, moisture content, traceability, food safety certifications, origin, and long-term supply reliability.

Agricultural production trends continue to support market expansion. According to the Food and Agriculture Organization (FAO), global fruit production has continued to increase over the past decade, providing a stable raw material base for fruit processing industries, including dehydration and value-added fruit products.

Consumer interest in healthier eating habits has further strengthened demand. The World Health Organization (WHO) recommends regular fruit consumption as part of healthy diets to reduce the risk of noncommunicable diseases, encouraging manufacturers to incorporate fruit-based ingredients into packaged food products. Although dried fruits contain naturally concentrated sugars, they remain an important source of dietary fiber, potassium, and antioxidants when consumed in appropriate portions.

Supply chain quality has become an important competitive factor. Importers, retailers, and food manufacturers increasingly require compliance with internationally recognized food safety standards, pesticide residue regulations, and traceability systems. Investments in modern drying technologies, automated sorting, metal detection, optical grading, and sustainable packaging continue improving product quality while reducing waste throughout the value chain.

Market Drivers

Growing Demand for Healthy Snacking

Consumers are increasingly replacing traditional confectionery products with snacks perceived to offer greater nutritional value. Dried fruits provide naturally occurring sugars, fiber, vitamins, and minerals while requiring minimal preparation, making them suitable for on-the-go consumption. Retailers continue expanding shelf space dedicated to dried fruit mixes, portion-controlled packs, and premium snack products to address this demand.

Manufacturers are responding by introducing products without added sugar, artificial preservatives, or synthetic colors, allowing dried fruits to meet clean-label product requirements across retail channels.

Expansion of Bakery and Processed Food Applications

The bakery industry represents one of the largest industrial consumers of dried fruits because ingredients such as raisins, dates, apricots, and prunes contribute sweetness, texture, moisture retention, and visual appeal. Food processors increasingly incorporate dried fruits into breakfast cereals, granola, snack bars, dairy products, and confectionery to improve nutritional positioning while reducing dependence on refined sweeteners.

According to the International Nut and Dried Fruit Council (INC), dried fruits remain widely used across multiple processed food categories because of their functional and nutritional properties. Official source: https://inc.nutfruit.org

Increasing Consumer Preference for Natural Ingredients

Food manufacturers are reformulating products to reduce artificial ingredients and improve ingredient transparency. Dried fruits support these objectives by providing naturally derived sweetness and flavor while contributing fiber and micronutrients. This trend has encouraged broader use of dates and raisins in cereal bars, dairy products, bakery fillings, and dessert formulations.

Companies continue investing in product innovation, organic certification, and premium packaging to address consumer expectations regarding quality, sustainability, and ingredient authenticity.

Growth in Organized Food Retail

Expansion of supermarkets, specialty food retailers, and online grocery platforms has improved consumer access to packaged dried fruit products. Organized retail channels provide better product visibility, quality assurance, and packaging formats that encourage repeat purchases. E-commerce platforms also enable manufacturers to introduce premium, organic, and specialty dried fruit products directly to consumers while expanding geographic reach.

Market Restraints and Challenges

Dependence on Agricultural Production

Raw material availability depends on seasonal fruit harvests, climatic conditions, water availability, and pest management. Drought, excessive rainfall, and temperature fluctuations may reduce fruit yields and affect product quality, resulting in supply shortages and higher procurement costs for processors.

Manufacturers increasingly diversify sourcing regions and establish long-term relationships with growers to improve supply stability.

Price Volatility and Supply Chain Costs

Prices of dried fruits are influenced by fresh fruit availability, labor expenses, energy costs associated with dehydration, packaging materials, and international freight rates. Cost fluctuations can reduce processor margins and influence pricing strategies for retail and industrial customers.

Companies continue investing in efficient drying technologies, logistics optimization, and inventory management to reduce operating costs while maintaining supply continuity.

Stringent Food Safety and Quality Requirements

Export-oriented producers must comply with regulations governing pesticide residues, microbiological safety, labeling, allergen management, and traceability. Retailers and food manufacturers increasingly require internationally recognized certifications before approving suppliers.

Investment in quality assurance systems, laboratory testing, automated inspection technologies, and standardized processing practices has become essential for maintaining access to premium international markets.

Major Segment Analysis

Raisins

Raisins represent the largest commercial segment within the dried fruit market because they combine broad consumer acceptance with extensive industrial applications. Produced primarily from dried grapes, raisins are widely incorporated into bakery products, breakfast cereals, confectionery, dairy products, snack mixes, and foodservice recipes. Their natural sweetness, extended shelf life, and compatibility with diverse food formulations make them one of the most versatile dried fruit ingredients.

Commercial demand is driven by both retail and industrial buyers. Food manufacturers value raisins for their consistent moisture content, flavor profile, and processing stability, while consumers purchase them as convenient standalone snacks and ingredients for home baking. Procurement decisions focus on fruit size, color consistency, sugar content, moisture specifications, food safety certification, and origin.

Competition within this segment depends on reliable grape sourcing, efficient drying technologies, grading accuracy, packaging innovation, and strong distribution networks. Producers that maintain consistent product quality, meet international food safety standards, and establish long-term relationships with retailers and food manufacturers are expected to retain a competitive advantage as demand for naturally derived food ingredients continues to expand.

Regional Analysis

North America

North America remains a mature market supported by high consumer awareness of healthy eating, well-developed retail infrastructure, and strong demand from the bakery, snack, and breakfast cereal industries. The United States accounts for the largest regional share owing to its established food processing sector and domestic raisin production in California. Consumers increasingly prefer convenient snacks with recognizable ingredients, encouraging retailers to expand premium dried fruit assortments. According to the United States Department of Agriculture (USDA), the United States continues to be one of the world's leading producers and exporters of raisins, supporting a stable domestic supply chain.

Europe

Europe represents an important consumption market where dried fruits are widely used in bakery products, confectionery, breakfast cereals, dairy products, and seasonal food preparations. Germany, France, Italy, Spain, and the United Kingdom maintain strong import demand because domestic production is insufficient to meet year-round consumption. Buyers place considerable emphasis on food safety, traceability, sustainability, and organic certification. Compliance with European Union pesticide residue regulations and labeling standards remains a prerequisite for suppliers seeking access to retail and industrial customers.

Asia Pacific

Asia Pacific is expected to record strong demand during the forecast period due to rising disposable incomes, urbanization, and expansion of modern food retail. China, India, Japan, South Korea, Australia, and Indonesia continue to witness increasing consumption of packaged snacks, breakfast cereals, and premium bakery products containing dried fruits. The region also serves as an important production and processing hub for dates, raisins, and tropical dried fruits. Expanding organized retail and e-commerce platforms are improving product availability across both metropolitan and secondary cities.

Middle East & Africa and South America

The Middle East has traditionally been a major producer and consumer of dates, while increasing tourism, retail modernization, and packaged food demand support wider consumption of diversified dried fruit products. South Africa serves as an important regional distribution market for processed fruit products. In South America, Brazil and Argentina generate demand from bakery manufacturers, confectionery producers, and health-conscious consumers. However, economic volatility and logistics costs continue to influence purchasing patterns across several countries.

Competitive Landscape

The dried fruit market consists of established processors, grower cooperatives, exporters, and branded food companies competing on product quality, sourcing capability, processing efficiency, certification, and distribution reach. Competitive differentiation depends on maintaining consistent raw material supply, meeting international food safety standards, and providing value-added products tailored to retail and industrial customers.

Companies including Sun-Maid Growers of California, Sunsweet Growers Inc., Seeberger GmbH, Royal Nut Company, Bergin Fruit and Nut Company, Traina Foods, Inc., National Raisin Company, Lion Raisins Inc., Agthia Group PJSC, and Arimex UAB compete by strengthening grower relationships, expanding premium product portfolios, improving packaging formats, and increasing exports to high-value consumer markets. Organic certification, private-label manufacturing, sustainable sourcing programs, and product innovation continue to influence competitive positioning.

Industrial customers generally establish long-term procurement agreements to ensure stable supply, uniform product specifications, and traceable sourcing. Investments in automated grading, optical sorting, metal detection, and modern packaging technologies help suppliers improve efficiency while reducing product losses during processing.

Recent Developments

June 2026: Crispy Green Scales Up Operations for Freeze-Dried Fruit Demand. Crispy Green expanded operations and relocated its headquarters in June 2026 to support growing demand for its freeze-dried fruit snacks, enhancing production capacity as a key player in the dehydrated fruit snack segment.

June 2026: BranchOut Food Launches Major Five-SKU Line in U.S. Mass Retailer. BranchOut Food announced a significant five-SKU launch in a leading U.S. mass retailer on June 17, 2026, featuring top-selling fruit chips plus new innovative products with dried cheese and vegetables using its GentleDry technology for superior nutrition and taste preservation.

Regulatory and Policy Environment

The dried fruit market operates within comprehensive food safety and agricultural regulations covering cultivation, processing, packaging, labeling, traceability, and international trade. Regulatory compliance directly influences market access, particularly for exporters supplying premium retail and food manufacturing customers.

The Codex Alimentarius Commission, jointly established by the Food and Agriculture Organization (FAO) and the World Health Organization (WHO), provides internationally recognized standards for food hygiene, contaminants, labeling, and food safety practices that support international trade in processed fruit products.

Within the European Union, dried fruit imports must comply with regulations concerning maximum residue limits for pesticides, food contaminants, labeling, and traceability. These requirements encourage exporters to implement comprehensive quality management systems and laboratory testing before shipment.

In the United States, processors operate under the Food Safety Modernization Act (FSMA) administered by the U.S. Food and Drug Administration (FDA), which emphasizes preventive food safety controls, supplier verification, and risk-based inspection programs.

Growing demand for organic products has also increased the importance of certification programs that verify compliance with organic farming and processing standards across international supply chains.

Outlook and Strategic Implications

Demand for dried fruits is expected to remain supported by changing dietary habits, continued expansion of packaged food manufacturing, and increasing consumer preference for nutritious convenience foods between 2026 and 2031. Food manufacturers are likely to increase procurement of raisins, dates, prunes, and apricots as natural ingredients for bakery products, cereals, dairy products, snack bars, and confectionery.

Investment priorities are expected to focus on advanced dehydration technologies, automation, quality assurance systems, sustainable packaging, and digital traceability solutions that improve operational efficiency and product consistency. Companies capable of maintaining direct relationships with growers and diversified sourcing networks will be better positioned to manage agricultural supply risks.

Procurement strategies among industrial buyers will increasingly emphasize long-term supplier partnerships, internationally recognized food safety certifications, organic product availability, and transparent sourcing practices. Retailers are also expected to expand premium, clean-label, and private-label dried fruit offerings as consumers seek products with simple ingredient declarations.

Potential risks include climate variability affecting fruit harvests, fluctuations in agricultural commodity prices, higher transportation costs, and evolving regulatory requirements governing food safety and sustainability. Despite these challenges, continued innovation in product formats, packaging, and ingredient applications is expected to support steady commercial opportunities for processors and suppliers throughout the 2026 to 2031 forecast period.

Dried Fruit Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 12.50 billion |

| Total Market Size in 2031 | USD 15.40 billion |

| Forecast Unit | Billion |

| Growth Rate | 4.26% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Farming Type, Distribution Channel, Application, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

By Farming Type

By Distribution Channel

By Application

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. GLOBAL DRIED FRUIT MARKET BY TYPE

5.1. Introduction

5.2. Raisins

5.3. Dates

5.4. Apricots

5.5. Prunes

5.6. Figs

5.7. Others

6. GLOBAL DRIED FRUIT MARKET BY FARMING TYPE

6.1. Introduction

6.2. Organic

6.3. Conventional

7. GLOBAL DRIED FRUIT MARKET BY DISTRIBUTION CHANNEL

7.1. Introduction

7.2. Online

7.3. Offline

7.3.1. Supermarkets & Hypermarkets

7.3.2. Convenience Stores

7.3.3. Specialty Stores

7.3.4. Others

8. GLOBAL DRIED FRUIT MARKET BY APPLICATION

8.1. Introduction

8.2. Bakery & Confectionery

8.3. Breakfast Cereals

8.4. Dairy Products

8.5. Snacks & Bars

8.6. Desserts & Sweets

8.7. Others

9. GLOBAL DRIED FRUIT MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. United States

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. Germany

9.4.2. France

9.4.3. United Kingdom

9.4.4. Spain

9.4.5. Italy

9.4.6. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. UAE

9.5.3. South Africa

9.5.4. Others

9.6. Asia Pacific

9.6.1. China

9.6.2. India

9.6.3. Japan

9.6.4. South Korea

9.6.5. Australia

9.6.6. Indonesia

9.6.7. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Mergers, Acquisitions, Agreements, and Collaborations

10.4. Competitive Dashboard

11. COMPANY PROFILES

11.1. Sun-Maid Growers of California

11.2. Sunsweet Growers Inc.

11.3. Seeberger GmbH

11.4. Royal Nut Company

11.5. Bergin Fruit and Nut Company

11.6. Traina Foods, Inc.

11.7. National Raisin Company

11.8. Lion Raisins Inc.

11.9. Agthia Group PJSC

11.10. Arimex UAB

12. APPENDIX

12.1. Currency

12.2. Assumptions

12.3. Base and Forecast Years Timeline

12.4. Key Benefits for Stakeholders

12.5. Research Methodology

12.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES

Navigate

Trusted by the world's leading organizations