Report Overview

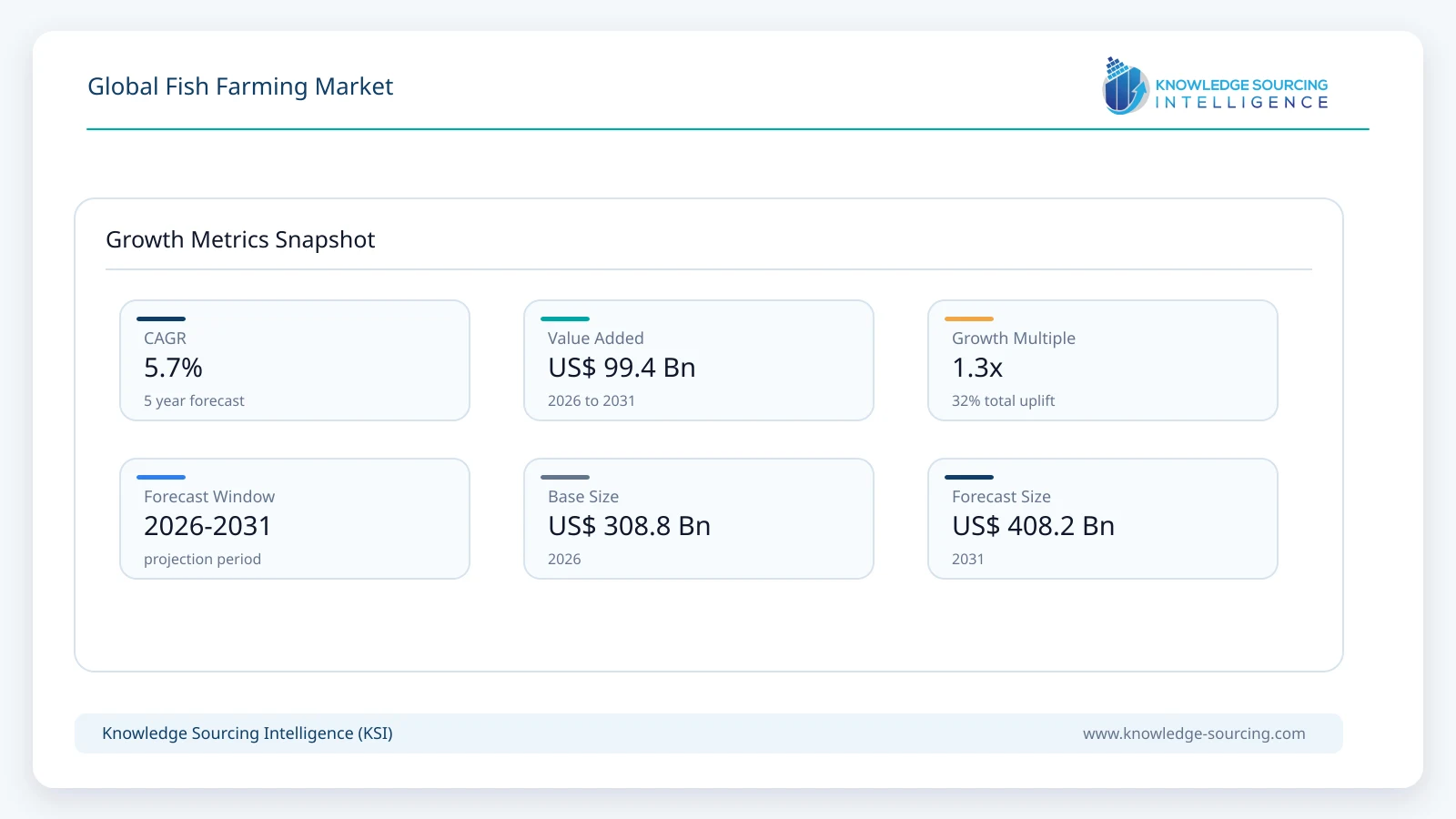

The Global Fish Farming market is forecast to grow at a CAGR of 5.7%, reaching USD 408.2 billion in 2031 from USD 308.8 billion in 2026.

Highlights:

- 1Aquaculture has become the world's largest source of aquatic animal production, strengthening long-term investment in commercial fish farming.

- 2Freshwater farming represents a commercially important production environment due to established infrastructure and favorable production economics.

- 3Asia Pacific remains the largest producer because of extensive aquaculture capacity, supportive government policies, and strong domestic seafood consumption.

- 4Automation, precision feeding, and digital farm monitoring are improving biological performance and reducing operating costs.

- 5Sustainability certification, traceability, and biosecurity compliance increasingly influence purchasing decisions across export markets.

The global fish farming market comprises the commercial production of finfish in freshwater, marine, and brackish water systems for food, processing, and export applications. Fish farming has become a strategic component of global food systems as capture fisheries have remained relatively stable while seafood consumption continues to rise. According to the Food and Agriculture Organization (FAO), global fisheries and aquaculture production reached a record 223.2 million tonnes in 2022, with aquaculture contributing 94.4 million tonnes of aquatic animals, representing 51% of total aquatic animal production for the first time. This structural shift highlights aquaculture's growing role in ensuring food security and meeting global protein demand.

Commercial demand is driven by retailers, foodservice operators, seafood processors, wholesalers, and export distributors seeking year-round availability, standardized quality, and traceable sourcing. Procurement decisions increasingly emphasize sustainability certifications, food safety compliance, disease management, and production consistency. Large buyers also prefer vertically integrated suppliers capable of managing hatcheries, feed production, grow-out operations, processing, and cold-chain logistics, reducing supply disruptions and improving contract fulfillment.

Industry investment is focused on production efficiency rather than acreage expansion. Producers continue adopting automated feeding systems, water-quality monitoring, selective breeding programs, vaccination protocols, and digital farm management platforms to improve feed conversion, reduce mortality, and optimize harvesting schedules. According to NOAA Fisheries, responsible aquaculture remains one of the most resource-efficient methods of producing animal protein while supporting coastal economies and food security.

Market Drivers

Rising Seafood Consumption Supporting Commercial Aquaculture

Growing consumer preference for nutritious protein continues to support seafood demand across developed and emerging economies. The FAO reports that aquaculture has become the principal source of aquatic animals for human consumption, reducing dependence on wild fisheries while supporting food security objectives. Retailers and processors increasingly secure long-term procurement agreements with commercial farms capable of delivering stable volumes and consistent product specifications.

Technology Improving Farm Productivity

Commercial producers are investing in automated feeding equipment, underwater imaging systems, artificial intelligence-assisted biomass estimation, and continuous water-quality monitoring. These technologies improve feed utilization, reduce production losses, and enhance operational efficiency. Improved genetics and vaccination programs further strengthen harvest consistency while reducing biological risks, enabling producers to meet buyer expectations for reliable supply.

Government Support for Aquaculture Expansion

Many national governments recognize aquaculture as an important contributor to food security, employment, and export earnings. Public investment in hatcheries, extension services, infrastructure development, and scientific research encourages commercial production while supporting sustainable resource management. Regulatory agencies are also strengthening licensing systems and environmental monitoring to facilitate responsible industry expansion.

Export Demand and Value Chain Integration

International seafood trade encourages producers to invest in processing facilities, cold-chain infrastructure, and traceability systems that satisfy import requirements in North America, Europe, and Asia. Integrated production models improve supply reliability and strengthen commercial relationships with retailers, distributors, and institutional buyers.

Market Restraints and Challenges

Disease Management and Production Risk

Disease outbreaks remain one of the most significant operational challenges affecting commercial fish farms. High-density production systems increase exposure to bacterial, viral, and parasitic infections that can reduce harvest volumes and increase operating costs. Producers continue investing in biosecurity protocols, vaccination, health surveillance, and selective breeding to reduce biological risk.

Feed Cost Volatility

Feed typically represents the largest operating expense in commercial fish farming. Fluctuating prices of fishmeal, fish oil, soybean meal, and alternative protein ingredients influence production economics and profitability. Companies increasingly evaluate novel feed ingredients and precision feeding technologies to improve feed conversion efficiency and control production costs.

Environmental and Regulatory Compliance

Environmental regulations governing water quality, nutrient discharge, stocking density, and biodiversity conservation have become more comprehensive across major producing regions. Compliance requires additional investment in monitoring systems, waste management infrastructure, and environmental reporting. Although these measures increase operating costs, they also improve long-term sustainability and market access.

Major Segment Analysis – Freshwater

Freshwater fish farming represents the largest commercial production environment because it supports efficient cultivation of carp, tilapia, and catfish using ponds, cages, tanks, and recirculating aquaculture systems. Lower capital requirements and broad geographic suitability make freshwater farming attractive for both commercial enterprises and small-scale producers.

Demand is supported by retailers, processors, institutional food suppliers, and export markets seeking affordable fish with reliable year-round availability. Buyers increasingly require traceability, food safety certification, and standardized product quality, encouraging producers to modernize hatcheries, feeding systems, and farm management practices.

Investment in digital monitoring, improved genetics, and disease prevention is strengthening productivity while reducing production losses. These operational improvements enhance profitability and position freshwater farming as an essential contributor to global seafood supply.

Regional Analysis

Asia Pacific

Asia Pacific remains the dominant production region owing to extensive aquaculture infrastructure, favorable climatic conditions, established seafood processing industries, and strong domestic demand. China, India, Indonesia, Thailand, and other regional producers continue investing in hatcheries, feed manufacturing, processing facilities, and export logistics. According to the OECD-FAO Agricultural Outlook 2025–2034, aquaculture will remain the primary driver of global fisheries production growth over the coming decade, with Asia continuing to account for most additional output.

Europe

Europe maintains a technologically advanced aquaculture industry supported by comprehensive food safety and environmental regulations. Norway remains a leading salmon producer, while producers across the region continue investing in fish health management, digital monitoring technologies, and sustainable feed solutions to satisfy retailer and consumer expectations regarding responsible seafood production.

North America

North American demand is driven by premium seafood consumption, retail expansion, and increasing investment in domestic aquaculture production. Land-based recirculating aquaculture systems are attracting investment because they improve biosecurity, reduce transportation costs, and strengthen local seafood supply. NOAA continues supporting science-based aquaculture development through research, regulatory coordination, and sustainable production initiatives.

South America, Middle East and Africa

South America benefits from export-oriented salmon production and expanding freshwater aquaculture. In the Middle East and Africa, governments are encouraging aquaculture development to improve food security and reduce seafood imports. Infrastructure investment, financing availability, and technical training remain important factors influencing commercial expansion.

Competitive Landscape

The global fish farming market is moderately consolidated, with multinational aquaculture companies competing alongside regional producers specializing in freshwater and marine species. Competition is primarily based on production efficiency, fish health management, feed optimization, sustainability performance, product quality, and access to international distribution networks. Companies with vertically integrated operations that include hatcheries, feed production, farming, processing, and distribution benefit from stronger supply chain control and greater operational flexibility.

Leading companies including Mowi ASA, Cooke Aquaculture Inc., Lerøy Seafood Group ASA, Cermaq Group AS, Grieg Seafood ASA, Thai Union Group PCL, Stolt Sea Farm, Andromeda Group, SalMar ASA, and Blue Ridge Aquaculture continue investing in automation, selective breeding, digital farm management, and fish health technologies to improve biological performance and production efficiency. These investments support higher survival rates, improved feed conversion, and consistent harvest volumes while helping companies comply with increasingly stringent environmental and food safety requirements.

Sustainability has become a major purchasing criterion for seafood retailers and foodservice companies. Buyers increasingly prefer suppliers that demonstrate responsible feed sourcing, traceability, environmental stewardship, and certification under internationally recognized aquaculture standards. Consequently, producers are investing in renewable energy, precision feeding, recirculating aquaculture systems (RAS), and real-time environmental monitoring to strengthen operational resilience and improve market access.

Strategic expansion is also occurring through acquisitions, farming license optimization, processing capacity expansion, and partnerships with feed manufacturers and technology providers. Companies with geographically diversified farming operations are generally better positioned to manage biological risks, regulatory changes, and climate-related disruptions while maintaining stable supply for global customers.

Recent Developments

February 2026: Mowi ASA reported record harvest volumes of approximately 559,000 tonnes for 2025 and announced a production target of 605,000 tonnes for 2026, supported by continued investment in farming capacity and post-smolt production.

December 2025: Mowi ASA announced a strategic feed partnership with Skretting (Nutreco) to improve feed procurement, formulation, and logistics. The agreement is expected to deliver annual cost savings exceeding EUR 55 million and improve operational efficiency.

November 2025: Mowi ASA increased its harvest guidance for 2025 and 2026 following the consolidation of Nova Sea, supporting higher production volumes and strengthening its long-term supply position in the global salmon market.

Regulatory and Policy Environment

Fish farming is regulated through national and international frameworks covering food safety, environmental protection, aquatic animal health, and sustainable resource management. Commercial producers are generally required to obtain environmental permits, comply with disease surveillance programs, monitor water quality, and follow regulations governing stocking density, waste discharge, and the use of veterinary medicines.

The Food and Agriculture Organization (FAO) adopted the Guidelines for Sustainable Aquaculture in 2024, providing member countries with a global framework for responsible aquaculture governance. The guidelines promote science-based licensing systems, biosecurity measures, ecosystem protection, and responsible production practices that support long-term sector development.

In the United States, NOAA Fisheries coordinates federal aquaculture policy by supporting sustainable production, scientific research, seafood safety, and environmental compliance. The agency works with federal and state authorities to improve regulatory efficiency while protecting marine ecosystems.

Within Europe, the European Commission promotes sustainable aquaculture through strategic guidelines focused on environmental performance, innovation, animal welfare, and competitiveness. Member states are encouraged to simplify licensing procedures while maintaining high environmental standards.

In India, the National Fisheries Development Board (NFDB) supports aquaculture modernization through financial assistance, hatchery development, infrastructure improvement, skill development, and technology adoption to increase domestic fish production.

Outlook and Strategic Implications

The commercial outlook for the fish farming market remains favorable as seafood demand continues to outpace the growth of capture fisheries. Future production is expected to rely increasingly on productivity improvements rather than large-scale expansion of farming areas. Investments in digital technologies, selective breeding, advanced nutrition, and fish health management are expected to improve production efficiency while reducing biological risk.

Procurement strategies among retailers, seafood processors, and foodservice companies are expected to place greater emphasis on long-term supply agreements with producers capable of demonstrating traceability, sustainability certification, food safety compliance, and reliable year-round production. These requirements are likely to strengthen the competitive position of vertically integrated producers with diversified farming operations.

Climate variability, disease outbreaks, feed ingredient availability, and evolving environmental regulations will remain important business risks. Companies that diversify feed sources, strengthen biosecurity programs, adopt precision farming technologies, and improve environmental performance are expected to achieve stronger operational resilience and more stable financial performance.

Competitive differentiation during the forecast period is likely to depend on production efficiency, sustainability performance, technological capability, and regulatory compliance rather than production scale alone. Continued public investment in aquaculture infrastructure, research, and farmer training across major producing regions is expected to support long-term industry development while contributing to global food security and expanding international seafood trade.

Global Fish Farming Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 308.8 billion |

| Total Market Size in 2031 | USD 408.2 billion |

| Forecast Unit | Billion |

| Growth Rate | 5.7% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Environment, Species, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Environment

- Freshwater

- Marine Water

- Brackish Water

By Species

- Salmon

- Tilapia

- Carp

- Catfish

- Tuna

- Milkfish

- Others

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Norway

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Thailand

- Indonesia

- Taiwan

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base, and Forecast Years Timeline

2. RESEARCH METHODOLOGY

2.1. Research Data

2.2. Research Design

2.3. Validation

3. EXECUTIVE SUMMARY

3.1. Research Highlights

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Market Opportunities

4.4. Porter’s Five Forces Analysis

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Power of Buyers

4.4.3. Threat of New Entrants

4.4.4. Threat of Substitutes

4.4.5. Competitive Rivalry in the Industry

4.5. Industry Value Chain Analysis

5. GLOBAL FISH FARMING MARKET BY ENVIRONMENT

5.1. Introduction

5.2. Freshwater

5.3. Marine Water

5.4. Brackish Water

6. GLOBAL FISH FARMING MARKET BY SPECIES

6.1. Introduction

6.2. Salmon

6.3. Tilapia

6.4. Carp

6.5. Catfish

6.6. Tuna

6.7. Milkfish

6.8. Others

7. GLOBAL FISH FARMING MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. USA

7.2.2. Canada

7.2.3. Mexico

7.3. South America

7.3.1. Brazil

7.3.2. Argentina

7.3.3. Others

7.4. Europe

7.4.1. UK

7.4.2. Germany

7.4.3. France

7.4.4. Italy

7.4.5. Spain

7.4.6. Norway

7.4.7. Others

7.5. Middle East and Africa

7.5.1. Saudi Arabia

7.5.2. UAE

7.5.3. Others

7.6. Asia Pacific

7.6.1. China

7.6.2. Japan

7.6.3. India

7.6.4. South Korea

7.6.5. Australia

7.6.6. Thailand

7.6.7. Indonesia

7.6.8. Taiwan

7.6.9. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Emerging Players and Market Lucrativeness

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Vendor Competitiveness Matrix

9. COMPANY PROFILES

9.1. Mowi ASA

9.2. Cooke Aquaculture Inc.

9.3. Lerøy Seafood Group ASA

9.4. Cermaq Group AS

9.5. Grieg Seafood ASA

9.6. Thai Union Group PCL

9.7. Stolt Sea Farm

9.8. Andromeda Group

9.9. SalMar ASA

9.10. Blue Ridge Aquaculture

Navigate

Trusted by the world's leading organizations