Report Overview

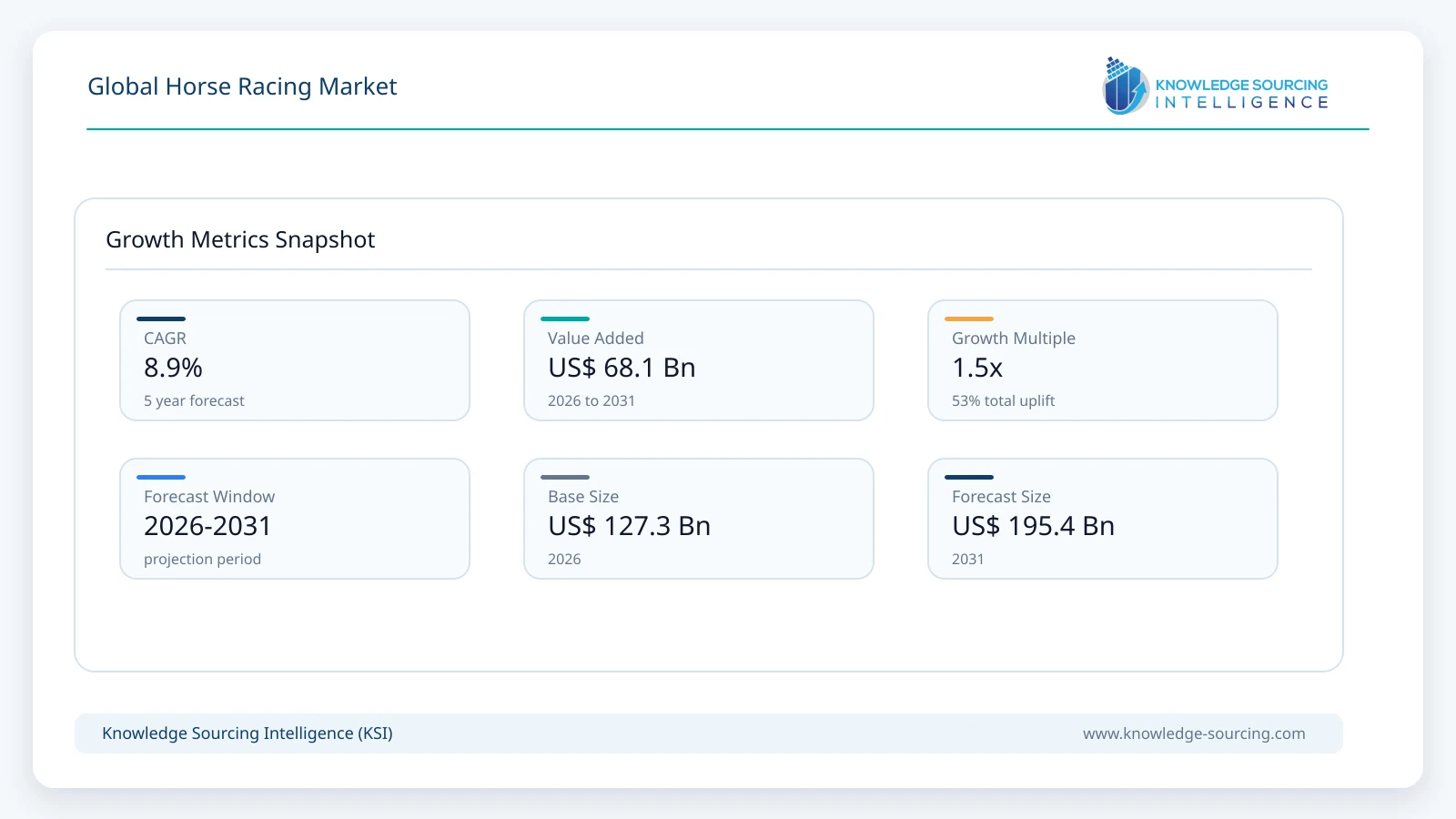

The Global Horse Racing market is forecast to grow at a CAGR of 8.94%, reaching USD 195.40 billion in 2031 from USD 127.34 billion in 2026.

Highlights:

- 1Online wagering continues to expand as bettors increasingly prefer mobile and digital betting platforms.

- 2Online betting channels represent the leading commercial opportunity because they offer broader geographic reach and lower operating costs.

- 3Asia Pacific remains one of the largest revenue-generating regions due to mature wagering markets in Japan, Hong Kong, and Australia.

- 4Digital payment systems, live streaming, and data analytics are improving customer engagement and operational efficiency.

- 5Responsible gambling regulations and licensing frameworks continue to influence operator investment and market entry.

- 6Competition increasingly depends on customer experience, media rights, digital platforms, and exclusive racing content.

The horse racing market comprises organized racing events, pari-mutuel wagering, fixed-odds betting where permitted, media rights, sponsorships, hospitality, racecourse admissions, and associated digital betting services. The industry supports an extensive value chain that includes racetrack operators, betting operators, horse breeders, owners, trainers, veterinary service providers, media companies, and regulatory authorities. Commercial activity is closely linked to regulated wagering, as betting turnover remains the primary revenue source supporting prize money, racing operations, and investment in equine welfare.

Demand is influenced by consumer participation in regulated betting markets, the popularity of premier racing festivals, and the expansion of digital wagering platforms. Online and mobile betting have broadened customer access beyond racecourses, allowing licensed operators to engage both experienced bettors and casual participants. Buyers increasingly prioritize secure payment systems, real-time race information, competitive betting odds, live streaming, and responsible gambling safeguards when selecting betting platforms.

The commercial structure varies across jurisdictions because horse racing is governed through national licensing systems, taxation policies, and betting regulations. Mature markets such as the United Kingdom, Japan, Hong Kong, Australia, France, and the United States benefit from well-established racing calendars, regulated wagering ecosystems, and significant media rights revenues. According to the International Federation of Horseracing Authorities (IFHA), more than 21,000 races were conducted globally under Group and Graded race classifications in 2024, reflecting the industry's extensive international racing calendar.

Revenue generation increasingly depends on diversified income streams rather than wagering alone. Racecourse operators continue investing in premium hospitality, digital broadcasting, customer engagement platforms, sponsorship agreements, and international simulcasting to strengthen financial performance. Meanwhile, betting operators are enhancing mobile applications, data analytics, and personalized customer experiences to improve user retention while complying with evolving responsible gambling regulations.

Technology adoption has also become an important commercial factor. Artificial intelligence-assisted fraud detection, cloud-based wagering platforms, live race analytics, cashless transactions, and digital identity verification improve operational efficiency while supporting regulatory compliance. These investments help operators enhance customer experience and strengthen trust in regulated betting markets.

Market Drivers

Expansion of Online and Mobile Betting Platforms

Licensed betting operators continue expanding digital wagering services as consumers increasingly place bets through smartphones and online platforms. Mobile applications provide convenient access to live racing schedules, race statistics, real-time odds, and secure payment options, improving customer participation across domestic and international racing events.

Operators continue investing in cloud infrastructure, personalized betting interfaces, and live streaming capabilities to improve customer retention. The UK Gambling Commission reports that remote gambling remains the largest segment of Britain's regulated gambling market, illustrating the growing importance of digital betting channels.

Growth in International Racing Events and Media Rights

Prestigious racing festivals attract global audiences, sponsorship investment, and international broadcasting agreements that extend revenue beyond wagering. Events such as the Kentucky Derby, Royal Ascot, Prix de l'Arc de Triomphe, Melbourne Cup Carnival, and Japan Cup generate substantial economic activity through tourism, hospitality, broadcasting, and commercial partnerships.

Race organizers increasingly develop international broadcasting agreements and simulcasting arrangements that enable betting operators to offer racing content across multiple jurisdictions while expanding audience reach.

Investment in Premium Customer Experience

Racecourse operators are investing in hospitality facilities, digital ticketing, premium seating, entertainment offerings, and integrated customer engagement platforms to diversify revenue sources. These investments attract corporate customers, international visitors, and younger audiences seeking entertainment experiences beyond traditional wagering.

Enhanced visitor experiences improve attendance, sponsorship opportunities, and ancillary spending while strengthening the long-term commercial sustainability of racecourses.

Regulatory Support for Licensed Betting Markets

Governments in regulated jurisdictions continue supporting licensed wagering frameworks that improve consumer protection, betting integrity, taxation transparency, and anti-money laundering compliance. Stable regulatory systems encourage investment by licensed operators while improving consumer confidence in legal betting channels.

Market Restraints and Challenges

Increasing Regulatory Compliance Costs

Horse racing operators and betting companies must comply with licensing requirements, anti-money laundering regulations, responsible gambling obligations, data protection laws, and integrity monitoring systems. Compliance investments continue increasing operating expenses, particularly for companies expanding across multiple regulatory jurisdictions.

Technology-based monitoring systems, identity verification platforms, and responsible gambling tools help operators improve compliance while reducing regulatory risk.

Animal Welfare and Public Perception

Public scrutiny regarding equine welfare has intensified in several racing jurisdictions. Concerns relating to horse injuries, race safety, transportation, and retirement programs influence public perception and regulatory oversight.

Industry organizations continue strengthening veterinary inspections, racecourse safety standards, medication controls, and aftercare initiatives to improve welfare outcomes and maintain public confidence in the sport.

Competition from Alternative Sports Betting

Horse racing competes directly with sports betting, online casinos, esports wagering, and other digital entertainment options. Younger consumers often demonstrate broader betting preferences, requiring racing operators to improve customer engagement through digital content, interactive betting features, and integrated entertainment experiences.

Strategic partnerships with media companies and betting platforms help expand audience reach while strengthening customer retention across multiple wagering products.

Major Segment Analysis

Online Betting

Online betting represents the most commercially important segment because it provides continuous customer access to regulated wagering without geographic dependence on physical racecourses. Mobile connectivity, digital payment infrastructure, and real-time race broadcasting have fundamentally changed how consumers engage with horse racing, making online platforms the primary channel for wagering growth.

Commercial demand is driven by convenience, broader race coverage, competitive betting markets, and instant access to live odds and historical race data. Bettors increasingly expect secure transactions, rapid payouts, personalized recommendations, and live streaming integrated into a single digital platform. These expectations encourage operators to invest in cloud-native wagering systems, artificial intelligence-based customer analytics, and cybersecurity capabilities.

Competition within the online segment extends beyond betting odds. Operators differentiate themselves through user experience, exclusive racing content, loyalty programs, responsible gambling tools, multilingual interfaces, and seamless mobile applications. Partnerships with race organizers and media companies also strengthen customer acquisition by providing access to premium racing events and exclusive broadcasting rights.

The continued expansion of regulated online betting markets is expected to reinforce this segment's commercial importance during the 2026 to 2031 forecast period, particularly as licensed operators continue modernizing digital infrastructure and enhancing customer engagement.

Regional Analysis

North America

North America remains one of the most commercially significant horse racing markets due to its established wagering ecosystem, iconic racing events, and diversified revenue streams. The United States accounts for the largest regional share through major race meetings, advance deposit wagering (ADW), historical horse racing facilities, media rights, sponsorships, and hospitality revenues. Canada also maintains a well-regulated racing industry supported by pari-mutuel wagering and provincial oversight.

Demand is primarily generated by regulated betting activity, premium racing festivals, and digital wagering platforms. Racecourse operators continue investing in customer experience, premium hospitality, mobile wagering applications, and broadcast partnerships to diversify revenue beyond admissions. According to the Horseracing Integrity and Safety Authority, nationwide integrity and safety standards are strengthening confidence in U.S. Thoroughbred racing through uniform medication controls and racetrack safety requirements.

Europe

Europe benefits from mature racing traditions, well-developed regulatory frameworks, and strong consumer participation in pari-mutuel and fixed-odds betting markets. The United Kingdom, France, Germany, Italy, and Spain remain important markets because of established racing calendars and extensive betting infrastructure.

Commercial activity is supported by media rights, sponsorship agreements, international simulcasting, and digital wagering. Regulatory oversight continues to emphasize responsible gambling, betting integrity, and anti-money laundering compliance. According to the UK Gambling Commission, remote gambling continues to account for the largest proportion of Britain's regulated gambling market, reinforcing investment in licensed online betting platforms.

Asia Pacific

Asia Pacific represents one of the highest-value horse racing regions owing to strong wagering turnover, internationally recognized racing events, and highly regulated betting systems. Japan, Hong Kong, Australia, Singapore, and South Korea generate substantial betting revenues through licensed operators and racing authorities.

The Japan Racing Association continues investing in digital wagering services, racecourse modernization, and equine welfare initiatives to improve customer participation and operational efficiency. Meanwhile, the Hong Kong Jockey Club remains one of the world's largest regulated racing organizations, supported by extensive betting turnover and international simulcasting. Buyers increasingly expect mobile wagering, live race analytics, and integrated digital payment systems, encouraging operators to modernize customer engagement platforms.

Middle East and Africa / South America

Commercial horse racing activity in the Middle East is supported by government investment, international racing festivals, and high-value thoroughbred breeding programs, particularly within the Gulf region. Saudi Arabia and the UAE continue positioning themselves as global destinations for premium racing events that attract international owners, trainers, and sponsors.

South American markets remain important for breeding, racing, and export of thoroughbreds, although wagering volumes vary considerably between countries because of differing regulatory frameworks and economic conditions. Infrastructure modernization and digital betting adoption are expected to improve long-term commercial opportunities.

Competitive Landscape

The global horse racing market combines racetrack operators, wagering companies, racing authorities, and betting technology providers operating within highly regulated environments. Competition extends beyond race organization and increasingly focuses on digital wagering capabilities, media rights, customer engagement, hospitality services, and exclusive racing content.

Organizations including Churchill Downs Incorporated, The Stronach Group (1/ST), Woodbine Entertainment Group, Keeneland Association, Inc., The New York Racing Association, Inc., Del Mar Thoroughbred Club, Kentucky Downs LLC, Hong Kong Jockey Club, Japan Racing Association (JRA), PMU (Pari Mutuel Urbain), Betfair (Flutter Entertainment plc), and Tabcorp Holdings Limited continue investing in mobile betting platforms, broadcast partnerships, customer analytics, and premium race-day experiences.

Competitive differentiation increasingly depends on regulatory compliance, wagering technology, racecourse modernization, customer loyalty programs, and international simulcasting. Operators with diversified revenue streams across wagering, hospitality, sponsorship, and media rights are generally better positioned to manage fluctuations in betting activity and attendance.

Recent Developments

June 2026: Arena Racing Company (ARC) confirmed enhanced prize-money opportunities through its £1 million All-Weather Bonus Scheme, continuing the 2025–2026 programme across Lingfield Park, Newcastle, Southwell, and Wolverhampton racecourses to encourage participation and reward consistent performance.

May 2026: Horse Racing Ireland (HRI) and GAIN Equine Nutrition officially launched the 2026 GAIN The Advantage Series, expanding the industry initiative by adding Listowel Racecourse and continuing support for owners, breeders, trainers, jockeys, and stable staff.

February 2026: Churchill Downs Incorporated reported record full-year revenue for 2025 and expanded its historical racing operations with the opening of Marshall Yards Racing & Gaming in Kentucky, strengthening wagering capacity and regional revenue generation.

Regulatory and Policy Environment

Horse racing operates under comprehensive regulatory frameworks governing wagering integrity, race safety, licensing, anti-money laundering, and consumer protection. National racing authorities and gaming regulators supervise betting operators, racecourse operators, and licensed participants to maintain transparency and public confidence.

In the United States, the Horseracing Integrity and Safety Authority establishes nationwide standards covering racetrack safety, equine welfare, medication control, and integrity monitoring for Thoroughbred racing.

In the United Kingdom, the UK Gambling Commission regulates licensed betting operators through requirements covering responsible gambling, customer protection, financial crime prevention, and operator licensing.

In France, PMU operates within a regulated pari-mutuel framework while contributing funding to the French horse racing industry through wagering revenues.

In Japan, the Japan Racing Association oversees race operations, wagering integrity, veterinary standards, and racecourse management under national legislation.

Growing regulatory emphasis on responsible gambling, digital identity verification, cybersecurity, and anti-money laundering compliance is expected to influence investment priorities throughout the forecast period.

Outlook and Strategic Implications

The horse racing market is expected to benefit from continued expansion of regulated online wagering, stronger international broadcasting agreements, and modernization of racecourse infrastructure between 2026 and 2031. Digital betting channels are likely to account for an increasing share of wagering turnover as consumers continue adopting mobile applications that provide live streaming, real-time odds, and secure digital payments.

Investment priorities are expected to include cloud-based wagering platforms, artificial intelligence for fraud detection and customer analytics, advanced cybersecurity, and personalized betting experiences. Racecourse operators are also expected to expand premium hospitality, entertainment offerings, and year-round venue utilization to diversify revenue beyond betting activity.

Procurement decisions among racing organizations will increasingly emphasize technology partners capable of supporting secure payment processing, scalable wagering systems, customer relationship management, and regulatory compliance. Media rights and international simulcasting are expected to remain important revenue sources as racing organizations seek to expand global audience reach.

The industry will continue facing challenges related to regulatory compliance costs, responsible gambling requirements, changing consumer entertainment preferences, and public scrutiny regarding equine welfare. Organizations that successfully balance customer engagement, technological innovation, regulatory compliance, and welfare standards are expected to strengthen their competitive position during the 2026 to 2031 forecast period.

Horse Racing Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 127.34 billion |

| Total Market Size in 2031 | USD 195.40 billion |

| Forecast Unit | Billion |

| Growth Rate | 8.94% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Bet Type, Betting Channel, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Bet Type

- Win Bet

- Single

- Double

- Treble

- Others

By Betting Channel

- Online

- Racecourse

- Off-Track Betting (OTB)

- Retail Betting Shops

- Others

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- Japan

- Australia

- Hong Kong

- China

- India

- South Korea

- Singapore

- Others

Geographical Segmentation

North America, South America, Europe, Middle East and Africa, Asia Pacific

Table of Contents

1. INTRODUCTION

1.1. Market Overview

1.2. Market Definition

1.3. Scope of the Study

1.4. Market Segmentation

1.5. Currency

1.6. Assumptions

1.7. Base and Forecast Years Timeline

1.8. Key Benefits to the Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Design

2.2. Research Process

3. EXECUTIVE SUMMARY

3.1. Key Findings

3.2. CXO Perspective

4. MARKET DYNAMICS

4.1. Market Drivers

4.2. Market Restraints

4.3. Market Opportunities

4.4. Porter’s Five Forces Analysis

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Power of Buyers

4.4.3. Threat of New Entrants

4.4.4. Threat of Substitutes

4.4.5. Competitive Rivalry in the Industry

4.5. Industry Value Chain Analysis

4.6. Analyst View

5. GLOBAL HORSE RACING MARKET BY BET TYPE

5.1. Introduction

5.2. Win Bet

5.3. Single

5.4. Double

5.5. Treble

5.6. Others

6. GLOBAL HORSE RACING MARKET BY BETTING CHANNEL

6.1. Introduction

6.2. Online

6.3. Racecourse

6.4. Off-Track Betting (OTB)

6.5. Retail Betting Shops

6.6. Others

7. GLOBAL HORSE RACING MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. By Bet Type

7.2.2. By Betting Channel

7.2.3. By Country

7.2.3.1. USA

7.2.3.2. Canada

7.2.3.3. Mexico

7.3. South America

7.3.1. By Bet Type

7.3.2. By Betting Channel

7.3.3. By Country

7.3.3.1. Brazil

7.3.3.2. Argentina

7.3.3.3. Others

7.4. Europe

7.4.1. By Bet Type

7.4.2. By Betting Channel

7.4.3. By Country

7.4.3.1. United Kingdom

7.4.3.2. Germany

7.4.3.3. France

7.4.3.4. Italy

7.4.3.5. Spain

7.4.3.6. Others

7.5. Middle East and Africa

7.5.1. By Bet Type

7.5.2. By Betting Channel

7.5.3. By Country

7.5.3.1. Saudi Arabia

7.5.3.2. UAE

7.5.3.3. Others

7.6. Asia Pacific

7.6.1. By Bet Type

7.6.2. By Betting Channel

7.6.3. By Country

7.6.3.1. Japan

7.6.3.2. Australia

7.6.3.3. Hong Kong

7.6.3.4. China

7.6.3.5. India

7.6.3.6. South Korea

7.6.3.7. Singapore

7.6.3.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Market Share Analysis

8.3. Competitive Benchmarking

8.4. Mergers, Acquisitions, Agreements, and Collaborations

8.5. Competitive Dashboard

9. COMPANY PROFILES

9.1. Churchill Downs Incorporated

9.2. The Stronach Group (1/ST)

9.3. Woodbine Entertainment Group

9.4. Keeneland Association, Inc.

9.5. The New York Racing Association, Inc.

9.6. Del Mar Thoroughbred Club

9.7. Kentucky Downs LLC

9.8. Hong Kong Jockey Club

9.9. Japan Racing Association (JRA)

9.10. PMU (Pari Mutuel Urbain)

9.11. Betfair (Flutter Entertainment plc)

9.12. Tabcorp Holdings Limited

Navigate

Trusted by the world's leading organizations