Report Overview

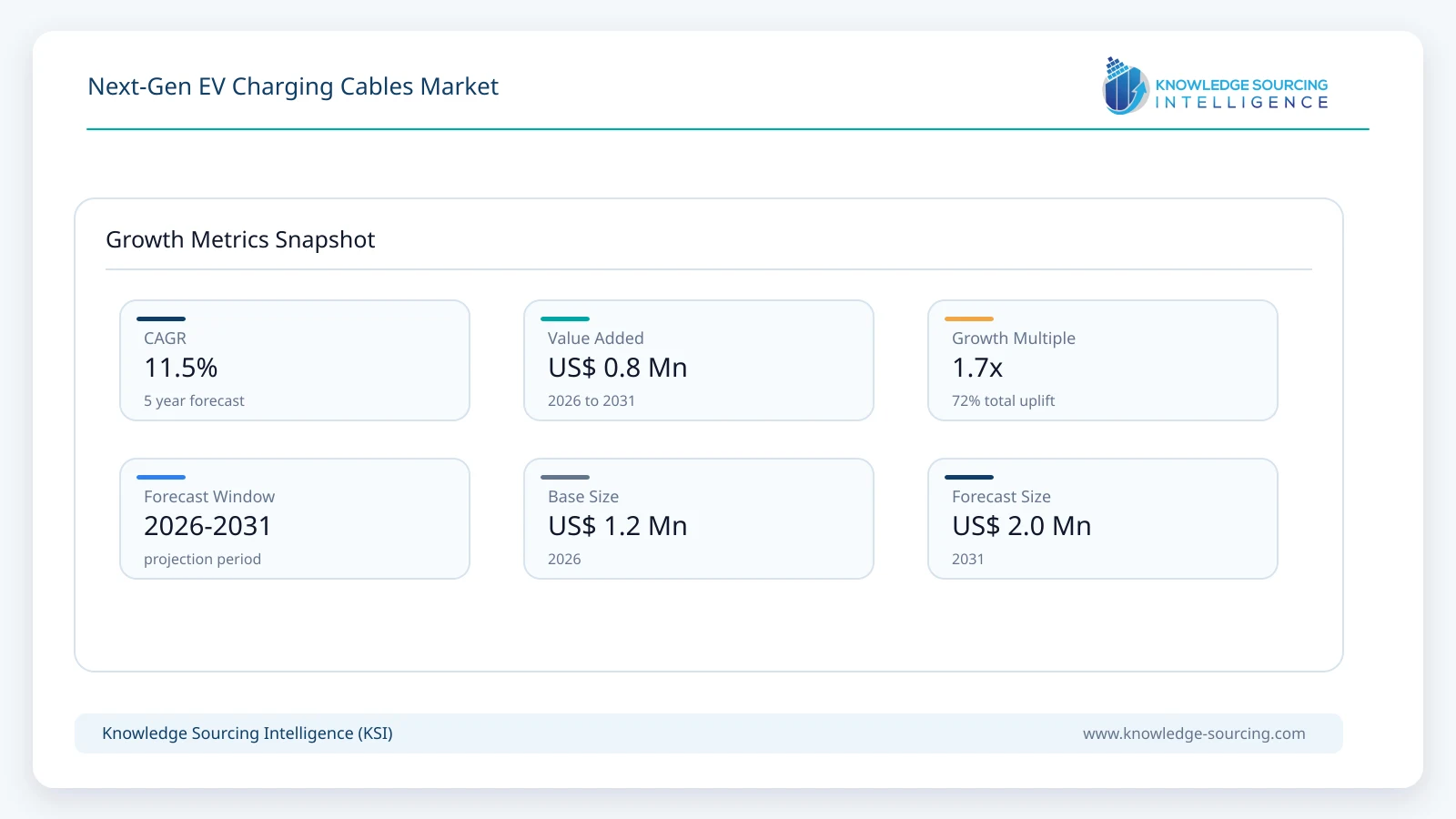

The Global Next-Gen EV Charging Cables market is forecast to grow at a CAGR of 11.5%, reaching USD 2.00 billion in 2031 from USD 1.16 billion in 2026.

Highlights:

- 1Increasing Demand of Ultra-Fast Charging:DC fast charging and HPC stations are on the rise and are fueling the use of advanced cable technologies.

- 2Move to Liquid-Cooled CablesLiquid cooling allows for providing more current and minimizing the thickness and weight of cables.

- 3Growth of Public and Fleet Charging InfrastructureSignificant rollouts of infrastructure are growing the necessary demand for durable and high-performance cables.

- 4Standardization and Safety Compliance:Global connector standards and safety regulations are defining the cable design and materials.

Next-Gen EV Charging Cables Market is determined by the overlap of the growing EV uptake, the growing charging power demands, and the necessity to find safer and more robust ways of charging. The conventional air-cooled charging cables are restricted by the inability to conduct high currents because of excessive heat production, mass, and weight. Consequently, the future generation solutions deal more with thermal management, material development, and mechanical stability.

Leading to the great variety of the demands on charging cables nowadays, they should be characterized by high levels of electrical conductivity, ability to withstand extreme temperatures, ease of use, and long working life in the case of frequent mechanical overloading. These are especially important in the public and commercial charging settings, whereby the cables are exposed to high usage, outdoor wear and tear, as well as, vandalism.

The fast development of highways and urban hubs towards fast-charging networks also has an impact on the market. The ultra-fast charging stations require cables that can safely operate very high power levels without risking the safety of the user or even the comfort. As a result, cable producers are putting in highly developed conductor materials, insulation, and cooling technology to counter these problems.

Market Dynamics

Market Drivers

Quick Development of EV Charging Infrastructure: EV charging stations, both public, commercial, and fleet, are being built faster as a result of government incentives, private investment, and utility participation. Every charging point needs good-quality charging cables, which are certified, and this drives up market growth.

Raising Charging Power Levels: As EV battery capacities grow and consumer demands change to having shorter charging times, charging power levels are also going up. This tendency requires new sophisticated cable patterns that can meet the requirements of safer work with higher currents and voltages.

Commercial and Fleet EV Growth: Commercial and Fleet EVs are growing, and buses, trucks, and logistics fleets are being electrified, which is putting pressure on high-utilization-rate, harsh operating conditions charging cables.

Technological Improvement in Cable Design: New conductor materials, insulation, and cooling technologies are ensuring that next-generation cables meet new performance demands.

Market Restraints & Opportunities

Expensive Advanced Cable Technologies: Liquid-cooled and ultra-high-power cables incur higher material and manufacturing costs that can restrict this technology in cost-sensitive markets.

Opportunity in HPC and Liquid-Cooled Solutions: With the emergence of ultra-fast charging, the demand for advanced cable technologies creates a great growth prospect to manufacturers.

Key Developments

April 2026: BYD announced the expansion of its Flash Charging infrastructure into Europe, deploying 1,500 kW CCS2-compatible ultra-high-current charging cables to support next-generation high-voltage EV platforms and cross-brand charging compatibility.

March 2026: Alpitronic introduced the second-generation Hypercharger HYC400, featuring continuous 600A liquid-cooled charging cable capability, improving sustained ultra-fast charging performance and thermal management for high-power EV charging applications.

March 2026: BYD unveiled its 1,500 kW Flash Charging system, incorporating 1,500A ultra-high-current charging cables designed for megawatt-class charging, enabling compatible vehicles to charge from 10% to 70% in approximately five minutes.

January 2026: Rolec, in partnership with EVbee, launched the updated UltraCharge DC Charging Range, featuring dual CCS2 charging cables delivering up to 350A peak current, supporting simultaneous high-power charging for two EVs at motorway and commercial locations.

Market Segmentation

The market is segmented by component, deployment mode, vehicle type, application, end user and geography.

By Cable Type: DC Fast Charging Cables

The Next-Gen EV Charging Cables Market is anticipated to be dominated by DC fast-charging cables throughout the forecast period due to the sudden increase in the number of public fast- charging stations and a higher demand by consumers in shorter charging time. With the fast-growing EV adoption, not only among the first adopters, users are getting more demanding about the charging experience being similar to fuel refueling of internal combustion vehicles. DC fast charging cables allow connecting high-power energy directly to the battery, bypassing onboard chargers and saving a lot of time on charging. The installation of DC fast chargers in highways, urban routes, and commercial areas is becoming the priority of governments, utilities, and other charging providers, and all this directly creates the demand in the strong, high-current DC charging cables. Moreover, the emergence of long-range EV and premium car segments solidifies the necessity of fast-charging compatibility, making DC fast charging cables the primary type of cable that can be deployed in future charging facilities.

By Power Rating: 151 kW to 350 kW

The 151 kW to 350 kW power rating brackish is forecasted to take over the market since it is the current industry gold standard in the speed of charging, cost of the infrastructure, and compatibility with the vehicle. The majority of the next-generation fast-charging stations implemented across the world are planned in this power range because it allows passengers EVs and light commercial vehicles to be charged rapidly without unreasonably upgrading the grid. Cables of this size should be able to operate under heavy current loads as well as be safe, flexible, and lightweight, and are therefore a center of technological improvements. Many OEMs are designing vehicles with power on the 200-300 kW level, so the infrastructure providers are standardizing on this range, which means that there will be consistent demand for charging cables ranging between 151 kW to 350 kW over the forecast period.

By Connector Type: CCS

Combined Charging System (CCS) connector, which consists of CCS1 and CCS2 models, will become the leader of the connector market because it is widely used in North America and Europe, besides gaining popularity elsewhere. CCS has both AC and DC charging over the same connector design it provides flexibility and scalability to the charging infrastructure operators. The fact that it is capable of supporting the high-power DC fast charging standard, makes it the standard of choice when it comes to the next-generation charging networks, especially networks that focus on highway corridors and the ultra-fast charging applications. OEM alignment with CCS standards further strengthens its dominance, as vehicle manufacturers seek interoperability and regulatory compliance across multiple markets. As a result, charging cables designed for CCS connectors account for the largest share of next-gen EV charging cable demand.

By Vehicle Type: Passenger Electric Vehicles

Next-generation EV charging cables should be dominated by passenger electric vehicles since they represent an overwhelming percentage of EV sales in the world. Although commercial EVs and electric buses are increasing categories, passenger cars take up most of the charging sessions, especially at the public and residential charging stations. The growing interest of the long-range passenger EV with the fast-charging capability increases the necessity of high-performance charging cables that can sustain higher power without making it challenging to use. With the growing number of passengers EVs adopting presence in a wide variety of geographies and income levels, the number of charging cables that need to serve this fleet is vast in comparison with other types of vehicles, and the sub-segment will remain dominant.

Regional Analysis

North America Market Analysis

North America should be regarded as a technologically developed and infrastructure-based market of next-generation EV charging cables, promoted by a fast increasing public fast-charging networks and an increasing number of electric SUVs, pickup trucks, and commercial vehicles. The biggest portion of demand in the region is the US, which is pushed by massive deployment of highway fast-charging networks, fleet electrification programs, and an addition of privately owned charging networks. Charging infrastructures in the area have begun installing DC fast chargers with a rating of 150 kW to 350 kW and this directly consequently requires high-current long-lasting thermally optimized charging cables. Moreover, the increasing use of the NACS and CCS connector standards is also defining the design of the cables and forcing manufacturers to consider interoperability, safety standards, and extended life.

South America Market Analysis

The next-generation EV charging cables are a new product on the South American market, and the demand is directly related to the slow adoption of EVs and the establishment of urban charging systems. Brazil is in the lead because of the growing use of public charging stations in large cities and the initial electrification of the public transport and fleet vehicle. Although the general charging power density is lower than in North America or Europe, DC fast charging is being investigated along major city and intercity rights and is starting to fuel demand towards higher-performance charging cables.

Europe Market Analysis

One of the most developed and regulation-oriented markets in the next-generation EV charging cables is Europe supported by the ambition to decarbonize aggressively, high EV penetration, and a large network of public charging cables. Germany, United Kingdom and France are among the countries that have made the greatest use of high-power DC charging stations, especially on highways and on trans-European transport corridors. This has led to the high demand of high end charging cables that can sustain high current load without compromising on safety, flexibility and convenience.

Middle East and Africa Market Analysis

The Middle East and Africa (MEA) market is a niche, yet a strategically developing market of next-generation EV charging cables. Generally, EV adoption has been low with some selective growth seen in countries like the United Arab Emirates and Saudi Arabia whereby the governments are aggressively pursuing smart city projects and sustainability initiatives which are leading to the early adoption of EV charging infrastructures in these countries. The charging cables used in such markets are exposed to harsh environmental conditions such as high temperatures, exposure to sand, and outdoor installation which makes the rugged design and thermal stability more significant.

Asia Pacific Market Analysis

The Next-Gen EV Charging Cables Market is dominated by Asia Pacific with massive volume in the type of product that is a result of the massive adoption of EVs, intensive urban charging needs and aggressive government policies of electrification. China is the largest market in the world by itself with enormous production of EVs, large numbers of charging stations spread throughout the country, and the quick establishment of fast-charging stations. The large scale adoption of high-power DC charging within the country, specifically in urban centers and highway systems, creates a high demand of complex charging cables in a broad spectrum of power rating.

List of Companies

Leoni AG

Aptiv plc

BESEN International Group

TE Connectivity

Phoenix Contact

Huber+Suhner

Sinbon Electronics

Allwyn Cables

Shanghai Mida EV Power Co., Ltd.

CPC

Leoni AG

Leoni AG is a major global cable supplier, cable systems, and cable-related services provider boasting of a good presence in electric mobility infrastructure. The company has extensive capabilities in the area of high-voltage cabling, developing conductor technologies, and system integration solutions that are being developed to be used in EV charging. Within the framework of the next-generation EV charging cables, Leoni deals with the creation of solid, high-current cable assemblies that can serve fast and ultra-fast charging specifications and provide safety, stability, and comfort of use. Based on its years of experience in automotive and industrial cable systems, Leini works with EV infrastructure providers and OEMs to provide solutions addressing the highest performance and environmental regulation standards in international markets.

TE Connectivity

TE Connectivity is a leading worldwide supplier of connectivity and sensor devices, such as the advanced charging cables solutions to electric vehicles and the charging infrastructure. The firm uses its expertise in electrical contacts, connectors and high-performance materials to develop EV charging cables capable of operating at higher power requirements and in harsh environmental conditions. The product line of TE Connectivity focuses on safety issues, reliability, as well as compatibility with global charging standards, including CCS, Type 2, and NACS. Moreover, the solutions offered by TE are characterized by both sophisticated shielding and thermal management capabilities and ruggedized design to enable high utilization rates in the public, commercial, and fleet charging systems. TE Connectivity is a favored supplier to the key charging station manufacturers and infrastructure developers due to its worldwide presence and extensive technology base.

Phoenix Contact

Phoenix contact is an established industrial automation, connectivity, and power electronics company with increasing involvement in the EV charging ecosystem. The company has come up with next-generation EV charging cables which include sophisticated materials, liquid-cooling capability, and high-power handling capacities that are applicable to DC fast charging and HPC (high-power charging) stations. The solutions provided by Phoenix Contact are combined into entire charging system portfolios which focus on safety, modularity, and effective thermal performance. Having a proven history of electrical connectivity and intelligent infrastructure products, Phoenix Contact provides charging network operators and OEMs with a future-proof cable technology capable of being expanded with new EV charging requirements.

Next-Gen EV Charging Cables Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 1.16 billion |

| Total Market Size in 2031 | USD 2.00 billion |

| Forecast Unit | USD Million |

| Growth Rate | 11.5% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Cable Type, Power Rating, Connector Type, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Cable Type

By Power Rating

By Connector Type

By Cable Material

By Application

By Vehicle Type

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. NEXT-GEN EV CHARGING CABLES MARKET BY CABLE TYPE

5.1. Introduction

5.2. AC Charging Cables

5.3. DC Fast Charging Cables

5.4. Liquid-Cooled Charging Cables

5.5. Ultra-High-Power Charging (HPC) Cables

6. NEXT-GEN EV CHARGING CABLES MARKET BY POWER RATING

6.1. Introduction

6.2. Up to 22 kW

6.3. 23 kW – 150 kW

6.4. 151 kW – 350 kW

6.5. Above 350 Kw

7. NEXT-GEN EV CHARGING CABLES MARKET BY CONNECTOR TYPE

7.1. Introduction

7.2. Type 1 (SAE J1772)

7.3. Type 2 (IEC 62196)

7.4. CCS1

7.5. CCS2

7.6. CHAdeMO

7.7. GB/T

7.8. NACS

8. NEXT-GEN EV CHARGING CABLES MARKET BY CABLE MATERIAL

8.1. Introduction

8.2. Copper

8.3. Aluminum

8.4. Hybrid

9. NEXT-GEN EV CHARGING CABLES MARKET BY APPLICATION

9.1. Introduction

9.2. Public Charging Stations

9.3. Residential Charging

9.4. Commercial Charging

9.5. Fleet & Depot Charging

10. NEXT-GEN EV CHARGING CABLES MARKET BY VEHICLE TYPE

10.1. Introduction

10.2. Passenger Electric Vehicles

10.3. Commercial Electric Vehicles

10.4. Electric Buses

10.5. Electric Trucks

10.6. Two-Wheelers & Three-Wheelers

11. NEXT-GEN EV CHARGING CABLES MARKET BY GEOGRAPHY

11.1. Introduction

11.2. North America

11.2.1. USA

11.2.2. Canada

11.2.3. Mexico

11.3. South America

11.3.1. Brazil

11.3.2. Argentina

11.3.3. Others

11.4. Europe

11.4.1. United Kingdom

11.4.2. Germany

11.4.3. France

11.4.4. Spain

11.4.5. Others

11.5. Middle East and Africa

11.5.1. Saudi Arabia

11.5.2. UAE

11.5.3. Others

11.6. Asia Pacific

11.6.1. China

11.6.2. India

11.6.3. Japan

11.6.4. South Korea

11.6.5. Indonesia

11.6.6. Thailand

11.6.7. Others

12. COMPETITIVE ENVIRONMENT AND ANALYSIS

12.1. Major Players and Strategy Analysis

12.2. Market Share Analysis

12.3. Mergers, Acquisitions, Agreements, and Collaborations

12.4. Competitive Dashboard

13. COMPANY PROFILES

13.1. Leoni AG

13.2. Aptiv plc

13.3. BESEN International Group

13.4. TE Connectivity

13.5. Phoenix Contact

13.6. Huber+Suhner

13.7. Sinbon Electronics

13.8. Allwyn Cables

13.9. Shanghai Mida EV Power Co., Ltd.

13.10. CPC

14. APPENDIX

14.1. Currency

14.2. Assumptions

14.3. Base and Forecast Years Timeline

14.4. Key benefits for the stakeholders

14.5. Research Methodology

14.6 .Abbreviations

Navigate

Trusted by the world's leading organizations