Report Overview

Semiconductor Packaging Market Size:

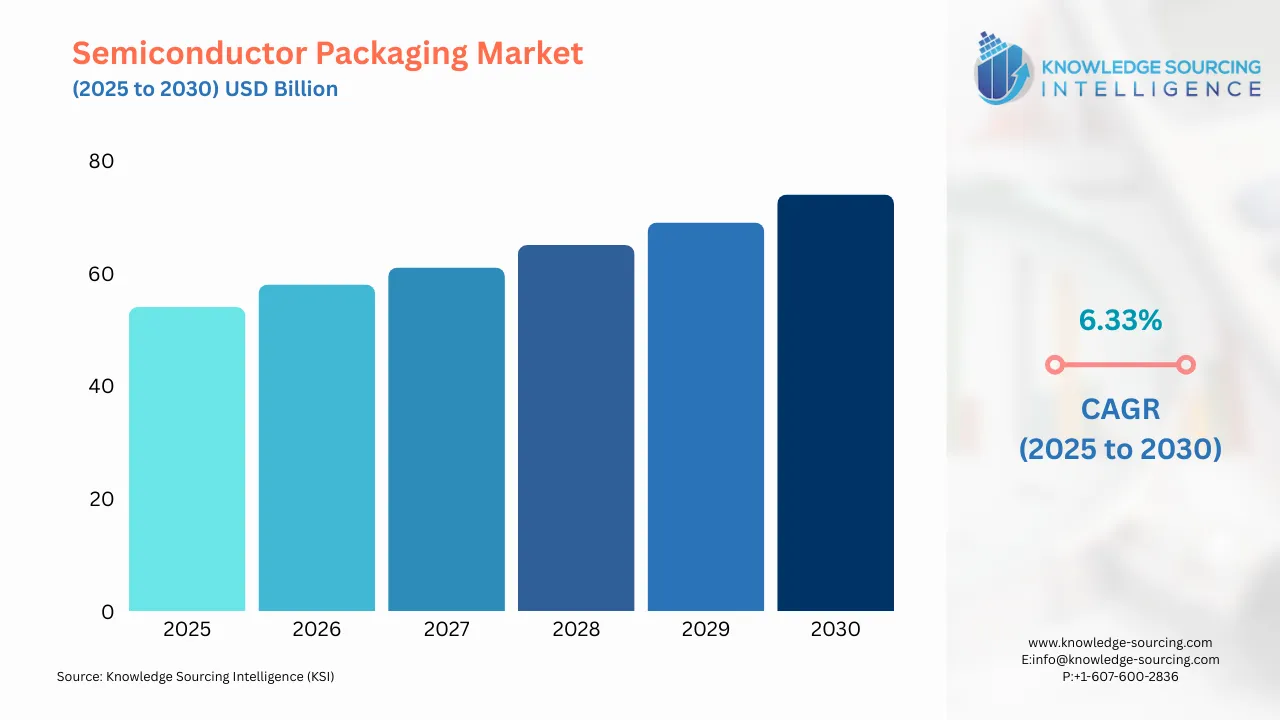

The semiconductor packaging market is projected to grow at a CAGR of 6.33% over the forecast period, increasing from US$54.171 billion in 2025 to US$73.623 billion by 2030.

Highlights:

- 1AI-driven growth surges demandAdvanced packaging for AI chips boosts market expansion.

- 23D packaging advancements dominateHybrid bonding enhances performance, density in semiconductor devices.

- 3TSMC’s CoPoS technology scalesTargets 300mm panel-level packaging for AI chips.

- 4Intel’s 2025 packaging upgradeTriple-tech combo supports 10,000 mm² silicon packages.

- 5Miniaturization fuels innovation3D integration meets compact electronics, enhancing device functionality.

Semiconductors are an important component applicable across multiple industries, like automotive, telecommunications, consumer electronics, healthcare, and aerospace, among others. Semiconductors have various properties, like integrated circuits, electronic discrete components, and transistors. They are a sensitive component, requiring a protective packaging case before being transported to multiple end-users. The semiconductor packaging offers a protective layer, which helps prevent the semiconductors from dust, scratches, or any other physical or environmental damage.

The demand for semiconductor packaging is expected to grow with the increasing demand for semiconductors globally. Semiconductors are an important component in automobiles. They offer multiple features, such as enabling the entertainment system and internet connectivity options in vehicles. The semiconductors are also embedded into various automobile safety systems, such as the ADAS and emergency braking systems.

The global production of automobiles in 2023 reached about 93.546 million units, as stated by the International Organization of Motor Vehicle Manufacturers (OICA). The organization also stated that about 55.115 million of the total vehicles produced globally were produced in the Asia Pacific region, such as China and India. The global automotive production witnessed a significant increase, from about 84.830 million units produced in 2022 to about 80.004 million units produced in 2021. Similarly, introducing various new technologies, like artificial intelligence and autonomous driving, has also pushed the demand for semiconductors in the automotive industry.

The semiconductor packaging market is estimated to grow moderately, owing to the increasing demand for consumer electronics, miniaturization, and the adoption of emerging technologies such as 5G. Additionally, the rising demand for the Internet of Things (IoT) has positively impacted the semiconductor packaging market. There is a rising demand among consumers for miniaturized electronic devices such as smartwatches and wearables, among others. There is an upsurge in semiconductor packaging demand as manufacturers look for solutions to fit everything in a limited space. Furthermore, as semiconductor performance demands continue to rise, packaging technologies have become a critical enabler for innovation. Leading companies are adopting advanced packaging techniques to improve power efficiency, performance, and integration density. Hence, the above-listed factors are expected to propel the market for semiconductor packaging in the projected period.

Semiconductor Packaging Market Growth Drivers:

- Increasing global semiconductor demand is anticipated to propel market growth.

The semiconductor is one of the most applicable components in electrical devices. It enables the use of communications and provides a better computing experience. Semiconductors are applicable in multiple industries, such as healthcare, aerospace, automotive, and consumer electronics. The increasing demand for semiconductors is expected to boost the market size of the global semiconductor packaging market.

The global semiconductor industry has witnessed a massive boost in demand, primarily due to its multi-industry applications. The global semiconductor demand increased by 15.8% from April 2023 to April 2024, as reported by the Semiconductor Industry Association (SIA). The association forecasts that the industry will grow by about 16% in 2024.

The semiconductor sales in April 2024 were estimated to be about US$46.4 billion, which marked an increase from US$40.1 billion in sales in April 2023. In 2024, the Americas region observed the highest growth of about 32.4%, followed by China, which witnessed a growth of about 23.4%. The overall Asia Pacific region observed an increase of 11.1%.

AI workloads require high-performance chips like GPUs and NPUs, which are found in everything from data centers to edge devices. At the same time, the automotive industry is shifting to electric and autonomous vehicles. These vehicles contain much more semiconductor content than traditional cars. Additionally, the rapid growth of IoT, industrial automation, and consumer electronics is driving demand higher across all major sectors.

This sharp rise in chip demand is boosting the semiconductor packaging market. Packaging is vital for achieving performance, power efficiency, and miniaturization. To shape the future of semiconductors in India, innovation is being driven by energy-efficient CPUs, advanced system-on-chip (SoC) architectures, and a new wave of semiconductor startups focused on AI-centric chip development. Key industry trends, such as the rise of AI and IoT, the push toward smaller process nodes, and the increasing importance of design-led innovation, are propelling advancements in chip design, communication technologies, and AI-powered solutions across sectors.

Apart from this, India is set to launch its first domestically produced semiconductor chip by the end of 2025, using 28 to 90 nanometre technology. As of May 2025, six chip fabrication units are under development, marking a major step forward in the country’s semiconductor mission, which was initiated in 2022. The initiative targets a critical segment that comprises around 60 percent of global semiconductor demand, focusing on applications in the automotive, telecom, power, and railway sectors.

Moreover, traditional packaging methods no longer meet today's needs for high density and speed. Instead, new packaging solutions like 2.5D/3D integration, Fan-Out Wafer-Level Packaging (FOWLP), and System-in-Package (SiP) are essential for managing interconnect density, heat dissipation, and space limitations. Packaging has therefore become a key driver of semiconductor innovation.

Semiconductor Packaging Market Geographical Outlook:

- The Semiconductor Packaging Market is segmented into five regions worldwide:

Geography-wise, the global semiconductor packaging market is divided into North America, South America, Europe, the Middle East and Africa, and the Asia Pacific. China’s semiconductor industry is one of the largest in the world. The nation is highly ambitious about semiconductors and is developing its IC industry to produce more chips. The country has one of the strongest semiconductor ecosystems with foundries, packaging equipment, and research institutions. The growth of China in the market is also driven by government support through initiatives like "Made in China 2025" and a vast consumer electronics market. The country’s focus on self-reliance has spurred investments in advanced packaging facilities, with companies like JCET and TSMC expanding operations to meet rising demand.

The Chinese government is also taking all necessary steps to promote the country’s semiconductor industry. For instance, according to the SIA, the government is making serious efforts to boost the semiconductor industry by investing about US$150 billion from 2014 to 2030. Hence, such booming investments by the government to promote the production of semiconductors are anticipated to positively impact the semiconductor packaging market.

Moreover, in September 2023, China announced an investment of US$40 billion to build a new state-backed fund for the semiconductor industry. This initiative is part of China’s broader strategy to compete with countries like the United States. The fund is expected to be the largest of the three established by the China Integrated Circuit Industry Investment Fund (also known as the Big Fund) and aims to speed up the advancement of the semiconductor sector in China.

China is one of the largest exporters of consumer electronics and other semiconductor-related materials. According to the Observatory of Economic Complexity, the country exported broadcasting equipment worth US$272 billion, computers worth US$181 billion, office machine parts worth US$111 billion, and semiconductor devices worth US$70.2 billion. The major countries where these goods were exported were the United States, Hong Kong, Germany, and South Korea.

AI’s rise, particularly in high-performance computing and data centers, further fuels demand for advanced packaging. Technologies like 2.5D/3D packaging and chiplet architectures enable high computational power and low latency, essential for AI-driven applications. This surge is evident in TSMC’s CoWoS production capacity, which doubles to 660,000 wafers by 2025.

Semiconductor Packaging Market Company Product:

- November 2025: Samsung Electro-Mechanics and Sumitomo Chemical formed a joint venture (JV) to manufacture Glass Core substrates, a next-generation material crucial for large-area AI and HPC packaging.

- October 2025: Applied Materials introduced the Kinex™ Bonding system, the industry's first integrated die-to-wafer hybrid bonder, accelerating high-volume production of multi-chiplet packages.

- October 2025: ASML delivered the first TWINSCAN XT:260 lithography scanner for advanced packaging, quadrupling productivity for high-volume interposer and 3D integration fabrication.

- October 2025: Amkor Technology broke ground on its new U.S. semiconductor advanced packaging and test campus in Arizona, expanding its investment to $7 billion to service the growing AI and HPC markets.

Semiconductor Packaging Market Key Players:

- Amkor Technology, headquartered in Tempe, Arizona, United States, started its business in Korea in 1968 and is a leader in the Outsourced Semiconductor Assembly and Test (OSAT) industry. The offerings include IC semiconductor packaging, advanced packaging, and testing of semiconductors, among others.

- Fujitsu Semiconductor Limited specializes in manufacturing LSI and provides highly reliable solutions tailored to customers requiring LSI, such as FeRAM (Ferroelectric RAM). The company aims to make the world a better place by building new sustainable products with innovation. It provides FeRAM (Ferroelectric RAM), ReRAM (Resistive RAM), and Catalogs & Datasheets.

- Intel Corporation is one of the major developers of process technology and one of the leading semiconductor manufacturers. The company’s mission is to shape the future of technology to help create a better future. Popular product category includes Intel® Evo™ Laptops., Intel vPro® for Business., Gaming Systems, Intel ® Arc™ Discrete Graphics, Intel® Wi-Fi Products, Thunderbolt™ Technology, Intel® Unison™ Software, and Chipsets, among others.

Semiconductor Packaging Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 54.171 billion |

| Total Market Size in 2031 | USD 73.623 billion |

| Growth Rate | 6.33% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Packaging Type, Packaging Material, End-User, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Semiconductor Packaging Market Segmentation:

- Packaging Type

- Advanced Packaging

- Flip Chip

- Embedded Die

- Fan-Out Level Packaging (FO-WLP)

- Fan-In Level Packaging (FI-WLP)

- By Packaging Material

- Organic Substrate

- Leadframe

- Ceramic Packaging

- Bonding-Wire

- Others

- By End-User

- Consumer Electronics

- Aerospace and Defence

- Medical Devices

- Communication and Telecom

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- China

- India

- Japan

- South Korea

- Thailand

- Indonesia

- Others

- North America

Our Best-Performing Industry Reports:

Market Segmentation

By Packaging Type

By Packaging Material

By End-user

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. SEMICONDUCTOR PACKAGING MARKET BY PACKAGING TYPE

4.1. Introduction

4.2. Advanced Packaging

4.3. Flip Chip

4.4. Embedded Die

4.5. Fan-Out Level Packaging (FO-WLP)

4.6. Fan-In Level Packaging (FI-WLP)

5. SEMICONDUCTOR PACKAGING MARKET BY PACKAGING MATERIAL

5.1. Introduction

5.2. Organic Substrate

5.3. Leadframe

5.4. Ceramic Packaging

5.5. Bonding-Wire

5.6. Others

6. SEMICONDUCTOR PACKAGING MARKET BY END-USER

6.1. Introduction

6.2. Consumer Electronics

6.3. Aerospace and Defence

6.4. Medical Devices

6.5. Communication and Telecom

6.6. Others

7. SEMICONDUCTOR PACKAGING MARKET BY GEOGRAPHY

7.1. Introduction

7.2. North America

7.2.1. USA

7.2.2. Canada

7.2.3. Mexico

7.3. South America

7.3.1. Brazil

7.3.2. Argentina

7.3.3. Others

7.4. Europe

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Spain

7.4.5. Italy

7.4.6. Others

7.5. Middle East and Africa

7.5.1. Saudi Arabia

7.5.2. UAE

7.5.3. Others

7.6. Asia Pacific

7.6.1. China

7.6.2. Japan

7.6.3. India

7.6.4. South Korea

7.6.5. Taiwan

7.6.6. Thailand

7.6.7. Indonesia

7.6.8. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

8.1. Major Players and Strategy Analysis

8.2. Emerging Players and Market Lucrativeness

8.3. Mergers, Acquisitions, Agreements, and Collaborations

8.4. Competitive Dashboard

9. COMPANY PROFILES

9.1. ASE

9.2. Amkor Technology

9.3. Powertech Technology Inc.

9.4. Fujitsu Semiconductor Limited

9.5. ChipMOS TECHNOLOGIES INC.

9.6. Intel Corporation

9.7. Samsung Electronics Co., Ltd.

9.8. Unisem (M) Berhad

9.9. ISI - Interconnect Systems Inc.

9.10. Jiangsu Changjiang Electronics Technology Co., Ltd. (JCET)

Navigate

Trusted by the world's leading organizations