Graphite Market expected to reach USD 24,932.133 million by 2030

Graphite Market Trends & Forecast

According to a research study published by Knowledge Sourcing Intelligence (KSI), the global graphite market is projected to grow from USD 15,902.732 million in 2025 to USD 24,932.133 million by 2030, at a CAGR of 9.41% during the forecast period.

The market is expanding due to the increasing adoption of electric vehicles (EVs) worldwide. Graphite is a critical material in lithium-ion batteries, which are essential for EV functionality. Its properties make it well-suited for high-performance batteries. The demand for energy storage technologies has surged with the growth of renewable energy projects, making graphite valuable in aerospace, where weight and strength are key considerations.

Additionally, the rising production of smartphones and tablets, which utilize graphite in batteries and other components, is another key driver. The steel industry, particularly in Asia and the Middle East, relies heavily on graphite for electric arc furnaces. The expansion of nuclear power generation, aligned with the trend toward cleaner energy sources, also contributes to market growth. Advances in graphite technology, refinement, and processing continue to enhance the quality and availability of graphite, further driving market expansion.

➥ View a sample of the report or purchase the complete study at: Graphite Market Report

Graphite Market Report Highlights

- Natural Graphite Segment: The natural graphite segment is expected to capture a larger market share by 2030. This segment is experiencing high demand from lithium-ion battery applications due to its affordability and environmental sustainability, making it a vital component in EVs and renewable energy storage systems. The smaller carbon footprint of natural graphite during production further supports its sustainability. Advances in purification and material modification techniques are improving the performance of natural graphite, leading to new applications in various industries and technologies.

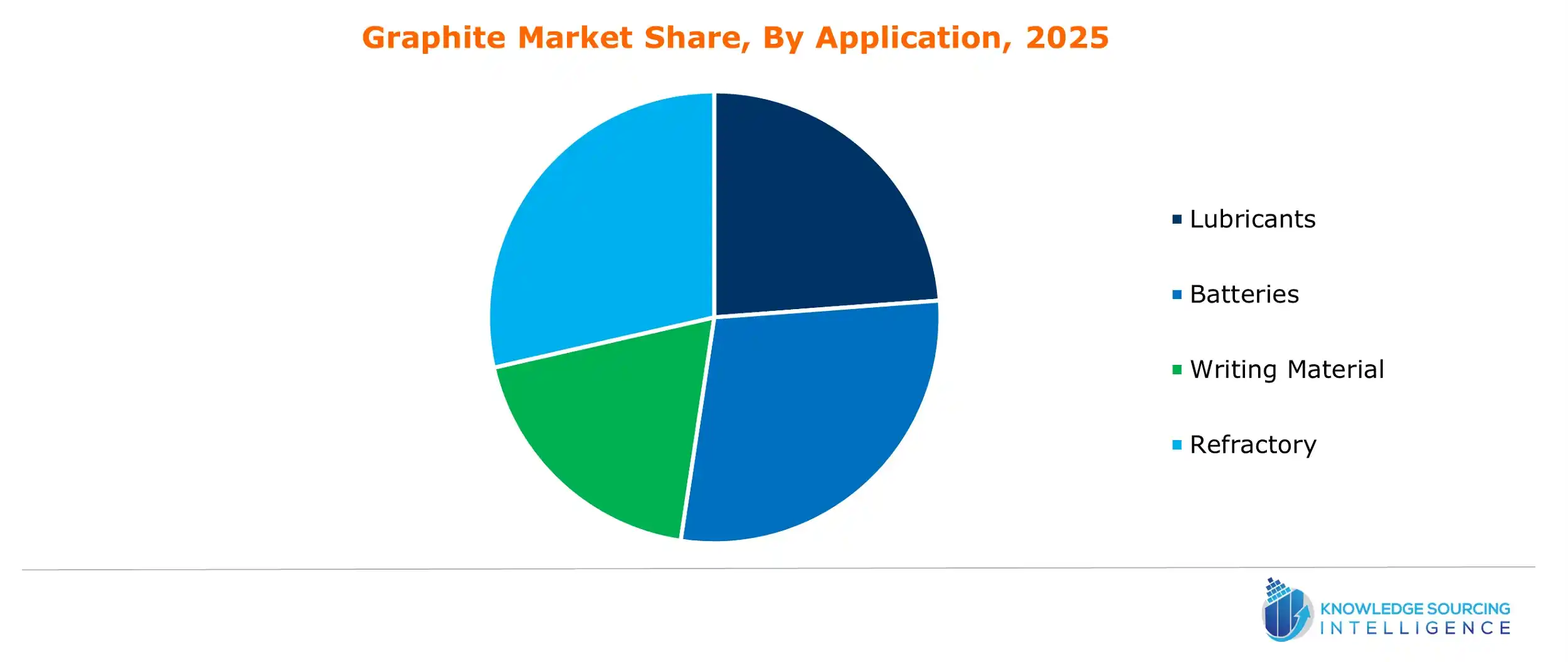

- Batteries Segment: The batteries segment is the fastest-growing application in the global graphite market, driven by the increasing demand for high-quality graphite. Graphite is a critical component in lithium-ion battery anodes, which are essential for EV performance. The growing emphasis on renewable energy has heightened the need for efficient energy storage systems. Lithium-ion batteries, which use graphite to store energy from renewable sources like solar and wind, are significantly contributing to the growth of this segment.

- Steel Industry Segment: The steel industry dominates the end-user segment due to the extensive use of graphite electrodes in steel production processes. Rising steel demand has increased the need for graphite electrodes in electric arc furnaces, which are more sustainable than traditional blast furnaces. Graphite electrodes are essential due to their high conductivity and thermal resistance. Government mandates and investments in constructing new steel-making facilities and upgrading existing ones to enhance local production capabilities are further driving demand for graphite electrodes.

- North America: North America holds the largest share of the global graphite market, driven by growing demand for EVs, domestic production initiatives, government support, and widespread applications across industries. The increasing adoption of EVs in countries like the USA and Canada has heightened the need for graphite, particularly as a critical material in lithium-ion battery anodes. Supportive government policies, such as the Inflation Reduction Act, promote domestic EV production and battery manufacturing, further boosting market growth.

Report Coverage:

| Report Metric | Details |

| Graphite Market Size in 2025 | USD 15,902.732 million |

| Graphite Market Size in 2030 | USD 24,932.133 million |

| Growth Rate | CAGR of 9.41% |

| Drivers |

|

| Restraints |

|

| Segmentation |

|

| List of Major Companies in Graphite Market |

|

Graphite Market Growth Drivers and Restraints

Growth Drivers:

- Increase in Steel Production: Graphite is essential in the steel industry for electric arc furnace electrodes and as a refractory material in high-temperature industrial processes, enhancing steel quality.

- Expansion of Electric Vehicles: The growing adoption of EVs is increasing the demand for renewable energy storage, thereby boosting the need for graphite. Lithium-ion batteries, which rely on both natural and synthetic graphite, are driving demand in battery manufacturing.

Restraints:

- Supply Concentration & Resource Scarcity: Limited graphite reserves and processing capacity create supply chain constraints and competitive instability.

- Price Volatility & Cost Challenges: While natural graphite offers cost advantages, its supply is constrained. Synthetic graphite production, which requires high temperatures, is sensitive to global energy price fluctuations, posing cost challenges for manufacturers.

Graphite Market Key Developments

- Collaboration: In July 2025, Graphite One announced a strategic collaboration with Lucid Group, Inc. for electric vehicle manufacturing. The agreement includes Graphite One supplying both natural and synthetic graphite to Lucid Group.

- Product Launch: In February 2025, Northern Graphite announced the launch of a demonstration-grade graphite-based battery anode material for use in electric vehicles.

Graphite Market Segmentation

Knowledge Sourcing Intelligence has segmented the Global Graphite Market based on type, application, end-user, and region:

Graphite Market, By Type

- Natural

- Synthetic

Graphite Market, By Application

- Lubricants

- Batteries

- Writing Material

- Refractory

- Nuclear Rectors

- Graphene Sheets

Graphite Market, By End-User

- Automotive

- Energy & Power

- Steel

- Electronics

- Aerospace

- Others

Graphite Market, By Region

- North America

- USA

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Others

- Asia Pacific

- China

- India

- Japan

- South Korea

- Taiwan

- Thailand

- Indonesia

- Others

- South America

- Brazil

- Argentina

- Others

- Middle East and Africa (MEA)

- Saudi Arabia

- UAE

- Others

Graphite Market Key Players

- Triton Minerals Ltd

- Volt Resources Limited

- Hexagon Energy Materials Limited

- Mason Graphite

- Focus Graphite Inc.

- NextSource Materials Inc.

- SGL Carbon

- Mersen Corporate Services SAS

- Tokai Carbon Co., Ltd.

- Toyo Tanso Co.,Ltd.

- CM Carbon

- NovoCarbon

- Ceylon Graphite Corp.

- China Carbon Graphite Inc.

About Knowledge Sourcing Intelligence (KSI)

Knowledge Sourcing Intelligence (KSI) is a market research and consulting firm headquartered in India. Backed by seasoned industry experts, we offer syndicated reports, customized research, and strategic consulting services. Our proprietary data analytics framework, combined with rigorous primary and secondary research, enables us to deliver high-quality insights that support informed decision-making. Our solutions empower businesses to gain a competitive edge in their markets. With deep expertise across ten key sectors, including ICT, Chemicals, Semiconductors, and Healthcare, we effectively address the diverse needs of our global clientele.