Report Overview

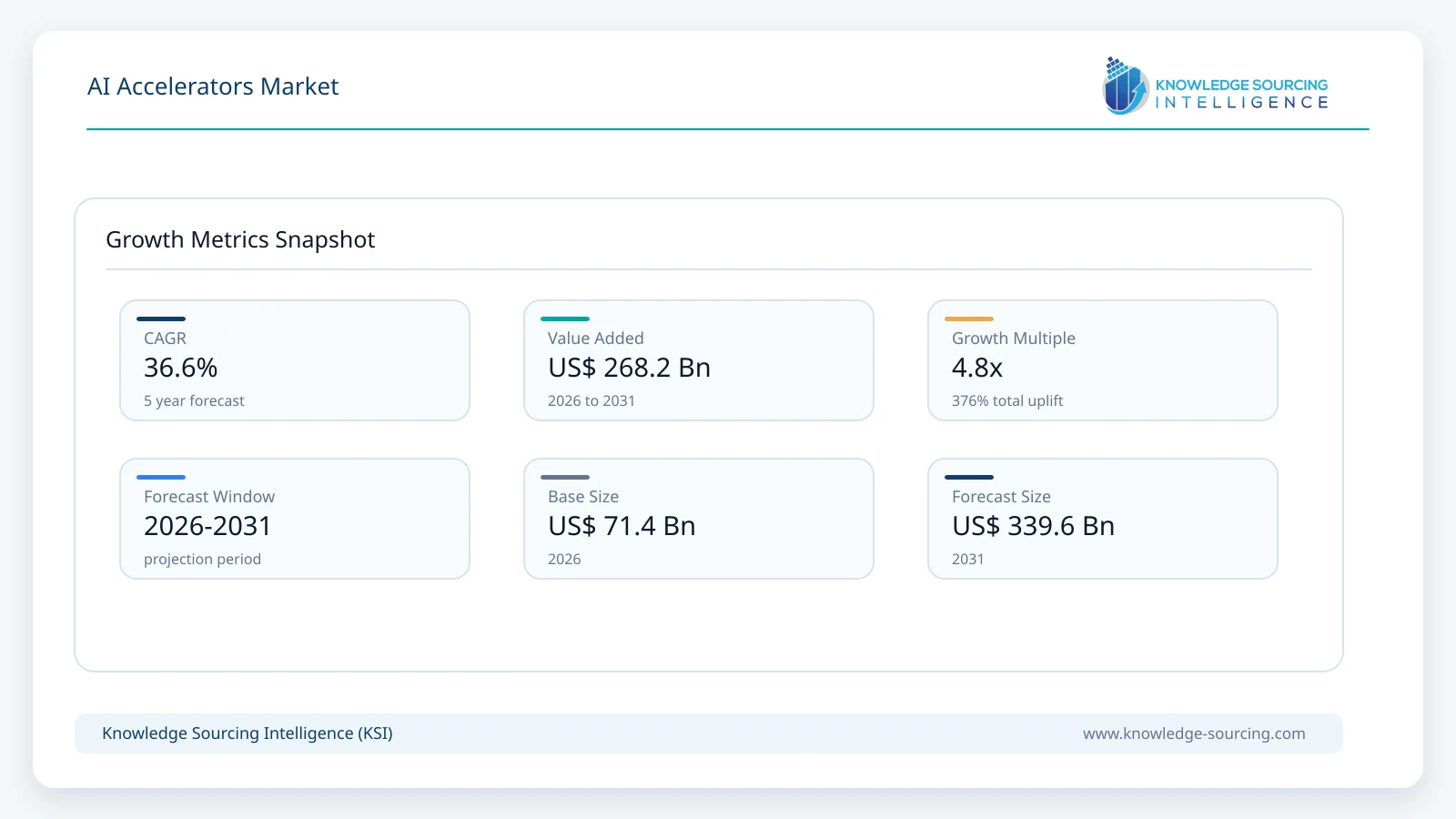

The AI accelerator market is forecast to grow at a CAGR of 36.6%, reaching USD 339.6 billion in 2031 from USD 71.4 billion in 2026.

Highlights:

- 1The AI accelerator market is rapidly expanding due to rising demand for machine learning.

- 2Companies are developing advanced GPUs and TPUs for efficient AI processing.

- 3Cloud-based AI accelerators are enabling scalable computing for SMEs and industries.

- 4North America is leading the market growth with significant AI research investments.

An artificial intelligence (AI) accelerator is a specialized piece of hardware or software that is used to speed up AI applications, especially those that involve machine learning and deep learning. These accelerators are made to process enormous amounts of data quickly and efficiently, which is essential for training and implementing AI models. The global industry involved in manufacturing and distributing technology such as GPUs, ASICs, FPGAs, and TPUs is included in the AI accelerator market. These accelerators are included in a large variety of equipment in industries like telecommunications, healthcare, banking, and automobiles.

The growing need for AI technologies across sectors, including consumer electronics, healthcare, and automotive, all of which demand strong computational resources for machine learning tasks, is propelling the market for AI accelerators. The market for AI accelerators is expanding due to developments in machine learning and artificial intelligence algorithms, as well as the rising need for specialized hardware. The rise of the market is further fueled by government and corporate sector support for AI R&D through investments and legislation, which improve AI's capabilities and accessibility on a global scale.

The rapidly expanding use of artificial intelligence in various industries, including data centers, cloud computing, robotics, autonomous vehicles, healthcare diagnostics, edge devices, and high-performance computing, is propelling the global AI accelerator market. AI accelerators, which are specialized hardware components such as GPUs, TPUs, FPGAs, and ASICs, are designed to optimize AI workloads. This allows for faster processing, lower latency, and improved energy efficiency compared to general-purpose CPUs. The market is profiting from the increase in demand for sophisticated AI models, such as deep neural networks, generative AI, and large language models, which demand enormous amounts of processing power for both training and inference. The growth of real-time analytics, IoT devices, and edge AI, which enables quicker decision-making without exclusively depending on cloud infrastructure, all contribute to this demand.

To meet the evolving demands of industries like manufacturing, defense, and finance, top tech companies are making significant investments in research and development to create next-generation AI chips with improved parallelism, higher processing capabilities, and lower power consumption. High development costs, supply chain limitations in semiconductor manufacturing, and the need for ongoing innovation to keep up with the complexity of AI models are some of the market's obstacles, despite its robust growth trajectory. The market will reach multi-billion-dollar valuations in the coming years due to the incorporation of AI accelerators into edge devices, improvements in chip architectures, and strategic alliances between cloud service providers and semiconductor giants.

AI Accelerator Market Overview:

An artificial Intelligence (AI) accelerator is a hardware accelerator, such as a deep learning processor or neural processing unit (NPU), that is designed to increase the speed of AI computation, especially in machine learning and deep learning. These are created to effectively process the AI workload, such as a neural network. With the AI technology growing, the demand for AI accelerators is expected to increase, as they are an important tool for processing a large amount of data required for the smooth running of AI applications. These AI accelerators are utilized in diverse applications, including smartphones, laptops, robotics, edge computing, and autonomous vehicles, among others.

The rise in demand for advanced high-performance computing and hardware for handling increased and complex workload of AI with more energy efficiency and speed is promoting the demand for AI accelerators globally. Another factor promoting market expansion is the increasing utilization of these AI accelerators in the development of the robotics sector, driven by their ability to handle machine learning and computer vision, which is critical to the growth of robotics. The rapid increase in the development of AI-enhanced robotics globally for accomplishing diverse tasks, both personal and industrial, will lead to continuous growth in the AI accelerators due to their ability to perceive and react to the environment and situations with the same accuracy and speed as a human, contributing to market expansion in the coming years.

According to the report titled “World Robotics 2024” by the International Federation of Robotics (IFR), the operating stock of industrial robots reported 3,904 thousand units of robots in 2022, which increased by 10 percent to 4,282 thousand robot units in 2023. Similarly, as per the same source, data from July 2025, there was an increase in industrial robots in the Japanese automotive industry, which was reported to be an 11 percent rise in 2024 from the previous year. The total number of robots installed in 2023 was 12,000 units, which increased to 13,000 units in 2024.

Moreover, product innovations and launches are also promoting the AI accelerator market expansion by providing increased real-time data processing and speed with enhanced parallel processing globally. For instance, in May 2025, Tavant launched its advanced AI accelerator suite named Algnite, developed to assist enterprises in quickly unlocking the utilization of Gen-AI-powered IT automation, along with data transformation, and designing and adopting intelligent usage and AI agents. In addition to this, in July 2025, the White House introduced “Winning the AI Race: America’s AI Action Plan,” which is part of President Trump’s January executive order focused on reinforcing U.S. leadership in AI. The plan focuses on establishing more than 90 Federal policy actions, which are focused on increasing innovation in AI, constructing AI infrastructure, and international diplomacy and security. It involves removing restrictive regulations on AI development and seeking private sector advice on further improvements. These policies lead to an increase in the construction and permitting development of new data centers and semiconductor fabrication plants, which will demand AI accelerator chips, promoting market expansion.

The leading companies in the AI Accelerator Market are AMD (Advanced Micro Devices), which competes fiercely with its Radeon GPUs and AI-focused hardware, offering scalable solutions for gaming, professional graphics, and AI inference/training tasks across various industries; Google (Alphabet Inc.), which is well-known for its proprietary TPUs that power large-scale AI workloads within Google Cloud and support advanced deep learning applications; and NVIDIA Corporation, which is a dominant force with its high-performance GPUs and AI platforms that are widely used in data centers, cloud computing, and autonomous systems. Intel Corporation also offers a diverse portfolio that includes CPUs, FPGAs, and AI-optimized chips like the Habana Gaudi processors. The AI accelerator market is segmented by:

Type: The AI accelerator market is segmented into graphics processing units, tensor processing units, application-specific integrated circuits, central processing units, and field-programmable gate arrays. Continuous advancements by major companies like NVIDIA and AMD, which are committed to enhancing processing power and energy efficiency, have reinforced the GPU segment's growth. These developments have led to the broad use of GPUs in a variety of industries by making them indispensable for high-performance computing, especially in AI applications. GPUs have become a popular option for AI researchers and developers because of their compatibility with well-known AI frameworks like TensorFlow and PyTorch. Due to their smooth integration into current development environments, they are often used for AI acceleration, which lowers deployment complexity and time.

Technology: The market for AI accelerators is divided into cloud-based AI accelerators and edge AI accelerators. Cloud-based AI accelerators are advantageous because they may deliver significant processing power without requiring hardware installations on-site. Small and medium-sized businesses that might lack the funds to purchase pricey gear will find this feature very alluring. When it comes to implementing deep learning models and intricate algorithms that require a lot of processing power, cloud-based AI accelerators are essential. They assist activities like fraud detection, sophisticated diagnostics, and autonomous driving technologies, and they spur innovation in industries like banking, healthcare, and automotive.

End-Use: The use of AI accelerators in telecom and IT also makes it easier to apply increasingly complex machine learning models that can improve customer service, optimize network quality, and forecast equipment breakdowns. Telecom firms may provide higher-quality services while more efficiently controlling costs thanks to these accelerators, which speed up data processing times and increase output accuracy. The need for strong AI accelerators in this industry is also fueled by the growing reliance on virtualized network services and the proliferation of IoT devices. As telecom companies keep developing their infrastructure to accommodate an increasing number of smart devices and services, integrating AI technologies becomes essential.

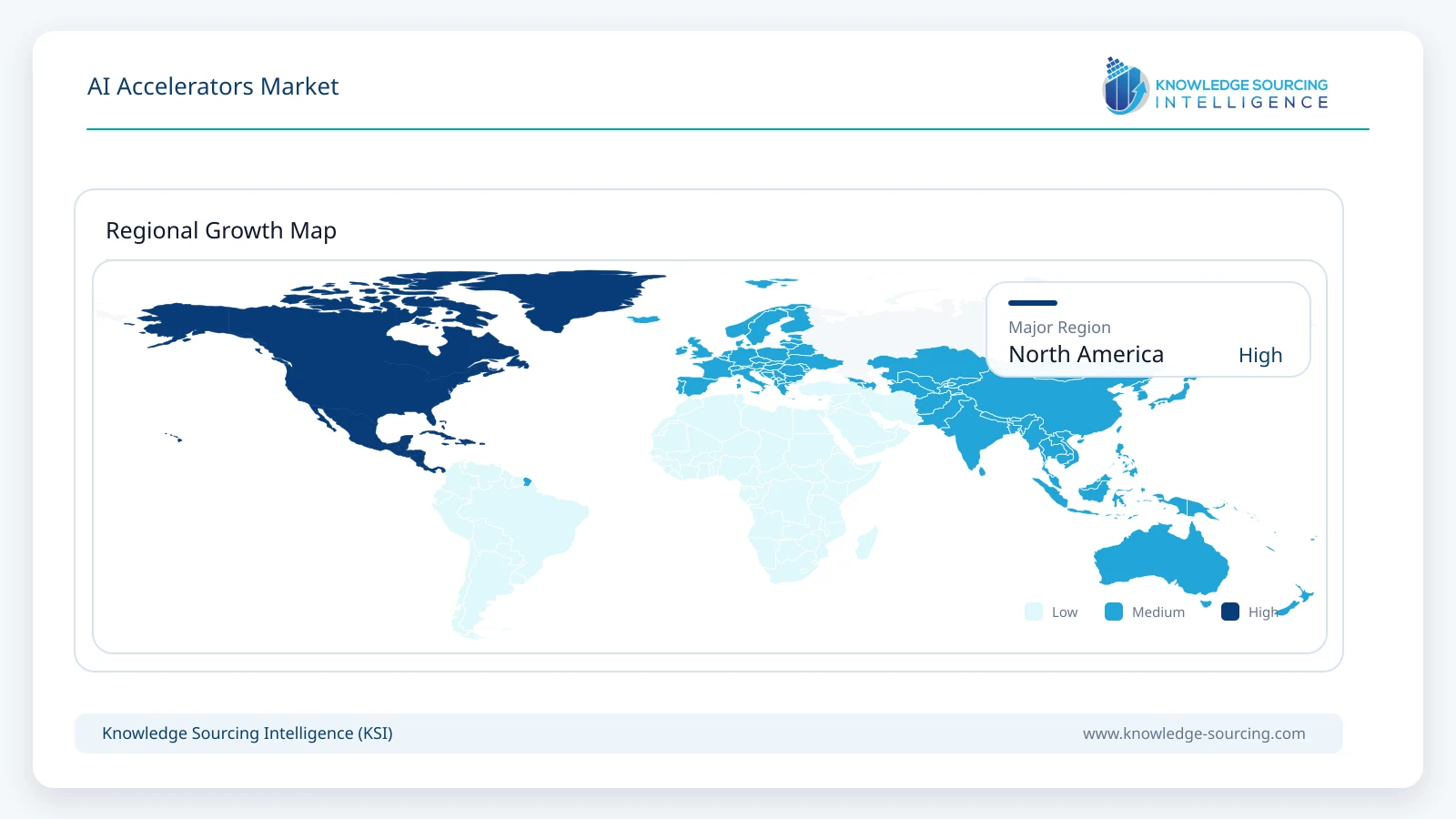

Region: The market is segmented into five major geographic regions, namely North America, South America, Europe, the Middle East Africa, and Asia-Pacific. North America is anticipated to hold the largest share of the market, and it will be growing at the fastest CAGR.

AI Accelerator Market Growth Drivers vs. Challenges:

Opportunities:

Developments in the Field of Generative AI: The market for AI accelerators is poised to benefit greatly from developments in generative AI. Technologies like GPT-4 and DALL-E have completely changed the content creation process by enabling robots to produce high-quality text, photos, and videos. The need for AI-generated content is rising, and this innovation is changing sectors including media, entertainment, and marketing. AI accelerators are crucial elements in this changing environment because of their capacity to effectively manage the intricate calculations needed for generative AI models. The need for reliable AI accelerators is anticipated to increase in tandem with the continued popularity of generative AI.

Growth in AI Applications: The market for AI accelerators is significantly influenced by the quick growth of AI applications in a variety of industries. AI is being used more in industries including consumer electronics, healthcare, finance, and automotive to boost productivity and creativity. AI accelerators make it possible to create individualized treatment programs and sophisticated diagnostic tools in the healthcare industry. They make it easier to analyze data in real-time for better financial decision-making. While consumer electronics gain from improved features in gadgets like smartphones and smart home systems, the automotive sector uses AI accelerators for autonomous driving technology. This broad use emphasizes how important AI accelerators are to satisfy the processing demands of contemporary applications.

Surge in Demand for High-Performance Computing and Hardware for Complex AI Tasks: Increasing demand for high-performance computing power and specific hardware for sophisticated AI is a major driving factor in the AI-accelerated market growth. All types of AI accelerators, such as GPUs, TPUs, and ASICs, work to generate highly specialized computational needs for processes of machine learning, deep learning, and neural networks with more speed and efficiency than a traditional central processing unit. Thus arises the demand for such accelerated processors.

Furthermore, AI applications are growing exponentially in various industries, ranging from healthcare, finance, and autonomous vehicles to entertainment, processing large datasets for training huge models like large language models (LLMs) and carrying out real-time inference, contributing to the demand for AI accelerators in the coming years. Moreover, the Stanford University 2024 data reported that private investment in AI is the highest globally, with the United States dominating the private investment in AI with €62.5 billion in 2023. This is followed by China, valued at €7.3 billion in investment, while the United Kingdom and Germany attracted €3.5 billion and €1.8 billion worth of private investment, respectively, in 2023. This robust private investment is fuelling both the development of advanced AI technologies and the infrastructure, along with the hardware, like an AI accelerator, to support and power these computations. Apart from this, data centers are important for scaling of AI workloads, necessitating AI accelerators to optimise the machine learning and neural network tasks. According to International Energy Agency (IEA) data of October 2024, a consistent increase in investment in new data centers, with the United States' spending on the data centers' construction having reportedly doubled from 2022 to 2024. Additionally, the investment by major companies like Google, Amazon, and Microsoft, which are global leaders in AI adoption and data centers installation, accounted for 0.5 percent of the entire US GDP.

Challenges:

High Implementation Costs and Initial Investment: The market for AI accelerators is facing difficulties because of high startup and implementation costs, despite its encouraging growth. It costs a lot of money to develop or buy AI accelerator technology, set up the required infrastructure, and integrate these systems into current workflows. The absence of precise ROI (Return on Investment) indicators is another crucial issue. It is challenging for many SMEs to estimate the long-term advantages of implementing AI, which makes it challenging to defend the initial outlay. Decision-makers might be reluctant to invest in AI technologies in the absence of hard facts or industry-specific success stories, which would further restrict acceptance and impede market growth.

AI Accelerator Market Segment Analysis:

The automotive sector is expected to grow significantly: By end-use, the AI accelerator market is segmented into it & telecom, healthcare, automotive, BFSI, retail, and others. AI accelerators are revolutionizing the automotive industry by enabling the computational foundation of advanced driver assistance systems (ADAS), autonomous driving technologies, and next-generation in-vehicle experiences. The ever-expanding array of sensors found in modern cars, such as cameras, LiDAR, radar, and ultrasonic systems, produces enormous amounts of real-time data that must be processed quickly for perception, control, and decision-making. AI accelerators, such as GPUs, ASICs, and edge AI chips, allow cars to recognize and categorize objects, anticipate the movements of other cars and pedestrians, and make split-second navigation decisions with extremely low latency, all of which are vital for both performance and safety. Apart from autonomy, these accelerators facilitate predictive maintenance, driver monitoring systems, intelligent traffic management, and AI-driven infotainment platforms that provide personalized recommendations, voice recognition, and natural language interaction. The need for scalable, upgradeable AI hardware that can manage over-the-air updates and changing AI models throughout the vehicle's lifecycle is being further increased by the move toward software-defined vehicles (SDVs).

With the help of AI accelerator manufacturers like NVIDIA, Intel, and Qualcomm, leading automakers and Tier-1 suppliers are integrating advanced AI chips directly into cars. This ensures compliance to strict safety regulations, like ISO 26262, while maximizing computational efficiency within limited thermal and power constraints. AI accelerators are also enabling vehicle-to-everything (V2X) communication, improving situational awareness, and enabling cooperative driving strategies due to the proliferation of connected cars and the rollout of 5G networks. The automotive industry's dependence on cutting-edge AI accelerators is anticipated to increase as laws and consumer demands drive for greater levels of autonomy (Level 3, Level 4, and beyond), making them essential to the mobility of the future. Since the integration of AI hardware is becoming a standard feature in both premium and increasingly mid-range vehicles, global car production trends are a major factor driving the expansion of the AI accelerator market. Approximately 94 million automobiles were produced worldwide in 2023. The global market for automotive components was estimated to be worth USD 2 trillion, of which USD 700 billion was exported. With an annual production of almost 6 million vehicles, India has risen to become the fourth-largest producer in the world, behind China, the United States, and Japan.

AI Accelerator Market Regional Analysis:

North America: North America is home to major investments in AI research and development as well as top AI technology developers. The market is driven ahead in large part by the existence of big tech firms like Google, IBM, and Microsoft, which are constantly investing in and inventing AI technology. The region's market growth is further reinforced by pro-AI government policies that aim to improve AI capabilities in several industries, such as manufacturing, healthcare, and the automotive sector. The need for AI accelerators has grown because of programs encouraging the application of AI in healthcare for individualized treatment options and diagnostics.

AI Accelerator Market Competitive Landscape:

Acquisition: In April 2024, the Israeli startup Run: ai, which focuses on AI infrastructure management, was fully acquired by NVIDIA. To improve its usability across other hardware platforms outside of NVIDIA's own systems, the software will be made publicly available.

Collaboration: In March 2024, Google and NVIDIA announced a collaboration to incorporate NVIDIA's artificial intelligence tools into Google Cloud services. The goal of this partnership is to improve the functionality of AI apps running on Google's infrastructure.

Product Innovation: In 2024, NVIDIA launched its new Blackwell GPU architecture. It is designed to reduce inference cost and energy by up to 25× and enable real-time generative AI with trillion-parameter models.

AI Accelerator Market Scope:

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 71.4 billion |

| Total Market Size in 2031 | USD 339.6 billion |

| Forecast Unit | Billion |

| Growth Rate | 36.6% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Type, Technology, End-Use, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Type

By Technology

By End-use

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. AI ACCELERATOR MARKET BY TYPE

5.1. Introduction

5.2. Graphics Processing Units (GPUs)

5.3. Tensor Processing Units (TPUs)

5.4. Application-Specific Integrated Circuits (ASICs)

5.5. Central Processing Units (CPUs)

5.6. Field-Programmable Gate Arrays (FPGAs)

6. AI ACCELERATOR MARKET BY TECHNOLOGY

6.1. Introduction

6.2. Cloud-Based AI Accelerators

6.3. Edge AI Accelerators

7. AI ACCELERATOR MARKET BY END-USE

7.1. Introduction

7.2. IT & Telecom

7.3. Healthcare

7.4. Automotive

7.5. BFSI

7.6. Retail

7.7. Others

8. AI ACCELERATOR MARKET BY GEOGRAPHY

8.1. Introduction

8.2. North America

8.2.1. By Type

8.2.2. By Technology

8.2.3. By End-Use

8.2.4. By Country

8.2.4.1. USA

8.2.4.2. Canada

8.2.4.3. Mexico

8.3. South America

8.3.1. By Type

8.3.2. By Technology

8.3.3. By End-Use

8.3.4. By Country

8.3.4.1. Brazil

8.3.4.2. Argentina

8.3.4.3. Others

8.4. Europe

8.4.1. By Type

8.4.2. By Technology

8.4.3. By End-Use

8.4.4. By Country

8.4.4.1. United Kingdom

8.4.4.2. Germany

8.4.4.3. France

8.4.4.4. Spain

8.4.4.5. Others

8.5. Middle East and Africa

8.5.1. By Type

8.5.2. By Technology

8.5.3. By End-Use

8.5.4. By Country

8.5.4.1. Saudi Arabia

8.5.4.2. UAE

8.5.4.3. Others

8.6. Asia Pacific

8.6.1. By Type

8.6.2. By Technology

8.6.3. By End-Use

8.6.4. By Country

8.6.4.1. China

8.6.4.2. Japan

8.6.4.3. India

8.6.4.4. South Korea

8.6.4.5. Taiwan

8.6.4.6. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

9.1. Major Players and Strategy Analysis

9.2. Market Share Analysis

9.3. Mergers, Acquisitions, Agreements, and Collaborations

9.4. Competitive Dashboard

10. COMPANY PROFILES

10.1. NVIDIA Corporation

10.2. Intel Corporation

10.3. Google LLC (Alphabet Inc.)

10.4. AMD (Advanced Micro Devices)

10.5. Qualcomm Technologies, Inc.

10.6. SoftBank Group Corp.

10.7. Graphcore

10.8. MediaTek Inc.

10.9. Synopsys

10.10. Meta Platforms, Inc.

10.11. IBM

10.12. Teradyne, Inc.

10.13. EdgeCortix Inc.

11. RESEARCH METHODOLOGY

Navigate

Trusted by the world's leading organizations