Report Overview

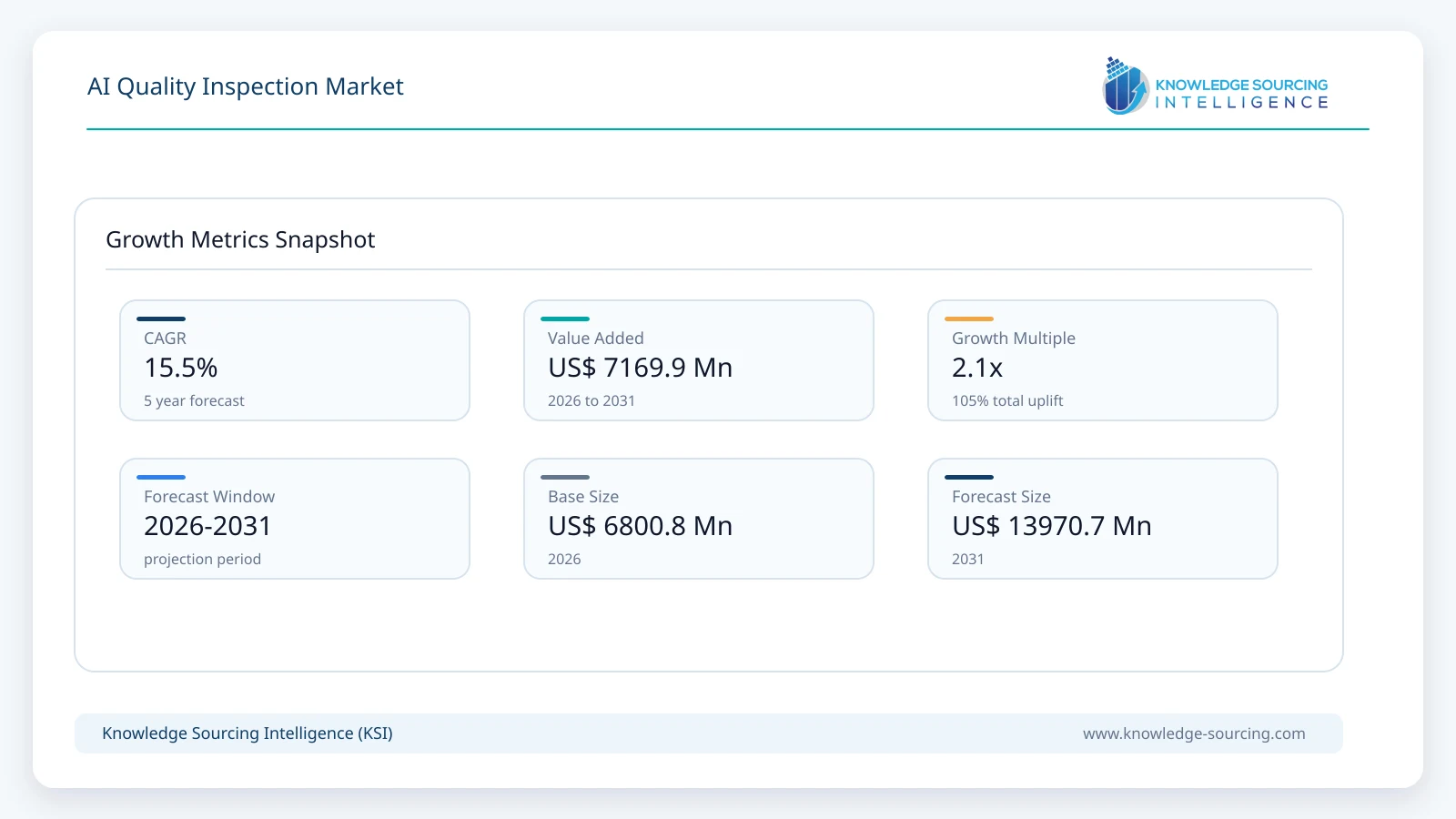

The AI Quality Inspection Market is forecast to grow at a CAGR of 15.49%, reaching USD 13,970.73 million in 2031 from USD 6,800.84 million in 2026.

Highlights:

- 1Manufacturers are accelerating AI inspection adoption to reduce quality defects, improve production efficiency, and support increasingly automated manufacturing operations.

- 2Computer vision integrated with deep learning remains commercially important, enabling accurate inspection across complex product geometries and high-speed production lines.

- 3Asia Pacific represents a major demand center, supported by electronics manufacturing, automotive production, semiconductor investment, and industrial automation initiatives.

- 4Edge AI deployment is gaining commercial traction, allowing manufacturers to perform real-time inspection with lower latency while reducing dependence on cloud connectivity.

- 5Regulatory requirements across pharmaceuticals, food processing, automotive, and aerospace industries continue to strengthen demand for traceable, standardized inspection systems.

- 6Competition increasingly centers on software intelligence, integration capabilities, lifecycle services, and industrial interoperability rather than imaging hardware specifications alone.

The AI Quality Inspection Market comprises software, hardware, and integrated inspection systems that apply artificial intelligence algorithms to automate defect identification, dimensional verification, surface analysis, assembly validation, and packaging inspection across industrial production environments. These solutions combine computer vision, machine learning, deep learning, edge computing, and advanced imaging technologies to improve inspection consistency while reducing manual intervention. Adoption has expanded from high-volume manufacturing industries into pharmaceutical production, electronics assembly, food processing, aerospace manufacturing, and precision engineering, where product quality directly influences regulatory compliance, warranty costs, and customer satisfaction.

Demand is primarily driven by manufacturers seeking higher first-pass yield, reduced scrap rates, and improved production throughput amid rising labor costs and stricter quality requirements. Traditional visual inspection methods often struggle to detect subtle defects, maintain inspection consistency across shifts, or process the growing volume of production data generated by automated manufacturing lines. AI-enabled inspection platforms address these operational limitations by continuously learning from production images and identifying quality deviations with greater repeatability. Procurement decisions increasingly emphasize measurable return on investment, ease of integration with existing manufacturing execution systems (MES), compatibility with programmable logic controllers (PLCs), and long-term software support rather than inspection hardware alone.

Industrial automation investments continue to reinforce demand for AI-powered inspection technologies. Manufacturers are expanding smart factory initiatives by connecting inspection systems with robotics, industrial Internet of Things (IIoT) infrastructure, enterprise resource planning platforms, and predictive maintenance solutions. This integration enables real-time production monitoring, root-cause analysis, and closed-loop quality control, allowing production teams to respond immediately to process deviations instead of relying on downstream quality audits. Buyers increasingly favor scalable platforms capable of supporting multiple production facilities while maintaining centralized model management and standardized inspection parameters.

The purchasing landscape has also shifted toward lifecycle value rather than initial equipment cost. Large manufacturers evaluate AI inspection solutions based on deployment flexibility, algorithm accuracy, software update frequency, cybersecurity capabilities, and compatibility with existing machine vision infrastructure. Small and medium-sized manufacturers increasingly adopt modular or subscription-based software offerings to reduce capital expenditure while benefiting from AI-driven inspection capabilities. As cloud-connected and edge-based deployment models mature, procurement teams are balancing latency requirements, cybersecurity policies, and operational reliability when selecting inspection architectures.

Technology suppliers compete by improving inspection accuracy across challenging production conditions such as reflective materials, variable lighting environments, mixed-product manufacturing lines, and high-speed production processes. Software capabilities—including automated model training, explainable AI functions, synthetic data generation, anomaly detection, and user-friendly interfaces—have become important differentiators alongside imaging hardware performance. Strategic partnerships among automation providers, robotics companies, semiconductor manufacturers, and industrial software vendors are further expanding solution interoperability, enabling customers to implement comprehensive digital quality management systems rather than standalone inspection stations.

Supply chain resilience has become another commercial consideration influencing investment decisions. Manufacturers increasingly recognize automated inspection as a means to reduce rework, improve traceability, and strengthen supplier quality management. AI inspection platforms generate structured production data that supports compliance documentation, supplier performance evaluation, and process optimization across geographically distributed manufacturing facilities. Consequently, quality inspection has evolved from a production support function into a strategic component of operational excellence and risk management.

Market Drivers

Expansion of Industrial Automation and Smart Manufacturing Programs

Manufacturers continue investing in automated production systems to improve productivity while addressing labor shortages and rising operational costs. As production lines become increasingly automated, manual inspection methods create operational bottlenecks that limit throughput and introduce variability in quality assessment. AI-powered inspection systems provide continuous, standardized quality verification that aligns with automated manufacturing workflows.

Industrial buyers increasingly require inspection solutions capable of integrating with robotics, MES platforms, industrial sensors, and factory automation infrastructure. Suppliers are responding by expanding software interoperability, supporting industrial communication protocols, and offering configurable deployment architectures suitable for diverse manufacturing environments. This strengthens recurring software and service revenue while encouraging broader enterprise-wide adoption.

Rising Quality Expectations Across High-Precision Manufacturing

Product complexity continues to increase across semiconductor fabrication, automotive electronics, aerospace components, and medical device manufacturing. Smaller component dimensions and tighter engineering tolerances reduce the effectiveness of conventional inspection techniques while increasing the financial consequences of production defects.

Manufacturers therefore prioritize AI inspection systems capable of detecting microscopic defects, identifying process anomalies, and adapting inspection models as product designs evolve. Procurement increasingly emphasizes inspection accuracy, false rejection rates, model retraining efficiency, and traceability features. Vendors that demonstrate measurable improvements in production yield and reduced warranty exposure strengthen their competitive position within capital-intensive manufacturing sectors.

Increasing Regulatory Compliance and Product Traceability Requirements

Industries such as pharmaceuticals, food processing, aerospace, and automotive manufacturing operate under extensive quality management and documentation requirements. Regulatory authorities increasingly expect manufacturers to demonstrate consistent inspection procedures, maintain digital production records, and support product traceability throughout manufacturing operations.

AI-enabled inspection platforms automatically generate inspection histories, image archives, defect classifications, and production analytics that simplify audit preparation and compliance reporting. Buyers therefore evaluate solutions not only for inspection performance but also for documentation capabilities, secure data management, and compatibility with enterprise quality management systems. This expands demand beyond inspection equipment toward integrated software ecosystems.

Advances in AI Algorithms and Edge Computing Capabilities

Recent improvements in deep learning architectures, edge processors, graphical processing units, and industrial computing platforms have improved inspection speed while reducing computational latency. Manufacturers operating high-speed production lines increasingly require inspection systems capable of making immediate quality decisions without relying on cloud connectivity.

Edge AI enables localized processing, reduces network dependency, strengthens data security, and supports continuous production even in facilities with limited internet connectivity. Technology suppliers continue investing in optimized inference engines, hardware acceleration, and simplified deployment tools, making advanced AI inspection accessible to a wider range of manufacturing environments.

Market Restraints and Challenges

High Initial Investment and Integration Complexity

Although AI quality inspection can reduce long-term operational costs, implementation often requires considerable upfront investment in cameras, industrial computing hardware, lighting systems, software licenses, network infrastructure, and system integration. Additional expenditure is frequently necessary to modify existing production lines and connect inspection platforms with factory automation systems.

These financial requirements particularly affect small and medium-sized manufacturers operating under constrained capital budgets. Buyers frequently conduct extensive return-on-investment analyses before approving procurement, extending sales cycles and slowing deployment. Vendors increasingly address this challenge through modular implementations, software subscriptions, and phased deployment strategies that reduce initial financial commitments.

Limited Availability of High-Quality Training Data

AI inspection accuracy depends heavily on representative production images covering acceptable products, manufacturing variations, and defect categories. Many manufacturers possess limited historical defect datasets, especially when introducing new products or production processes.

Insufficient training data can reduce model reliability and increase false positives or missed defect detection during initial deployment. Suppliers increasingly employ synthetic image generation, transfer learning techniques, and continuous model refinement to improve inspection accuracy while minimizing dependence on extensive labeled datasets. Nevertheless, data preparation remains a significant implementation consideration across multiple industries.

Workforce Skills Gap in Industrial AI Deployment

Successful implementation extends beyond purchasing inspection equipment. Manufacturers require personnel capable of configuring AI models, validating inspection performance, maintaining industrial computing infrastructure, and interpreting analytical outputs for process improvement.

Many production facilities continue to experience shortages of engineers with combined expertise in artificial intelligence, machine vision, industrial automation, and manufacturing operations. Consequently, organizations often depend on external system integrators and technology partners during deployment, increasing project costs and extending implementation timelines. Suppliers are responding by simplifying software interfaces, expanding training programs, and developing automated model configuration capabilities.

Cybersecurity and Industrial Data Protection Concerns

Connected inspection systems generate substantial volumes of production data, images, process parameters, and operational analytics that may contain commercially sensitive manufacturing information. Organizations operating critical industrial infrastructure remain cautious regarding cloud connectivity, remote software updates, and external data storage.

Procurement teams increasingly evaluate cybersecurity certifications, secure software architectures, access management capabilities, encryption standards, and compliance with industrial cybersecurity frameworks before selecting AI inspection platforms. Suppliers that invest in secure edge processing, controlled software lifecycle management, and enterprise-grade cybersecurity features are better positioned to address these purchasing requirements while supporting broader deployment across regulated manufacturing sectors.

Major Segment Analysis

Computer Vision Segment

Computer vision represents the most commercially important technology segment within the AI Quality Inspection Market because it serves as the foundation for automated visual assessment across virtually every industrial production environment. Modern manufacturing facilities generate large volumes of visual information from cameras, line-scan systems, thermal sensors, and three-dimensional imaging devices. Computer vision platforms convert these image streams into actionable production intelligence by identifying defects, measuring dimensions, verifying assembly accuracy, and monitoring product consistency in real time. As manufacturers pursue higher production speeds without compromising quality standards, computer vision has become an essential production asset rather than an optional inspection tool.

Demand for computer vision solutions is strongest among industries characterized by high production volumes, complex product geometries, and stringent quality requirements. Automotive manufacturers employ AI-enabled vision systems to inspect weld integrity, paint quality, component alignment, and final assembly. Electronics and semiconductor producers rely on high-resolution inspection to identify soldering defects, wafer imperfections, and microscopic contamination that cannot be consistently detected through manual inspection. Pharmaceutical manufacturers use vision systems to verify packaging integrity, label accuracy, fill levels, and serialization compliance, while food and beverage processors deploy automated inspection to detect packaging defects, contamination risks, and product inconsistencies.

Buyer expectations have shifted beyond image acquisition capability toward intelligent inspection performance. Manufacturers increasingly seek platforms capable of adapting to changing product designs without extensive rule-based programming. Deep learning models integrated with computer vision enable inspection systems to recognize previously unseen defect patterns, distinguish acceptable manufacturing variations from genuine quality issues, and improve inspection performance through continuous model refinement. Procurement teams therefore prioritize software accuracy, explainability of inspection decisions, model retraining efficiency, and compatibility with existing production infrastructure alongside camera resolution and imaging hardware specifications.

Competitive differentiation within the computer vision segment is increasingly software-driven. While imaging hardware remains important, suppliers compete through advanced defect classification algorithms, automated annotation tools, synthetic training data generation, edge deployment capabilities, and seamless integration with industrial automation platforms. Compatibility with manufacturing execution systems, programmable logic controllers, industrial robots, and enterprise quality management software has become a decisive purchasing factor for multinational manufacturers seeking standardized inspection across multiple production facilities.

The segment also benefits from favorable economics over the equipment lifecycle. Although implementation requires investment in imaging hardware and software integration, manufacturers often realize measurable reductions in scrap generation, rework costs, warranty claims, production downtime, and manual inspection labor. Continuous monitoring also produces structured production data that supports process optimization, supplier quality evaluation, and predictive manufacturing analytics. Consequently, computer vision remains the largest revenue-generating technology category and is expected to retain strategic importance as manufacturers continue expanding intelligent factory initiatives.

Regional Analysis

North America

North America remains a mature market for AI quality inspection due to widespread industrial automation, advanced manufacturing capabilities, and sustained investment in artificial intelligence technologies. Automotive manufacturing, aerospace production, medical device manufacturing, semiconductor fabrication, and pharmaceutical production represent major demand sources. Manufacturers across the United States and Canada increasingly integrate AI inspection with robotics, industrial IoT platforms, and predictive maintenance systems to improve production efficiency and strengthen quality assurance.

Buyer priorities emphasize inspection accuracy, cybersecurity, regulatory compliance, and interoperability with existing factory automation infrastructure. Investment is supported by continued modernization of manufacturing facilities, semiconductor production initiatives, and public policies encouraging domestic industrial capacity. However, relatively high implementation costs and shortages of specialized industrial AI professionals remain practical considerations influencing deployment timelines, particularly among medium-sized manufacturers.

Europe

Europe demonstrates steady demand supported by advanced automotive engineering, industrial machinery production, aerospace manufacturing, and pharmaceutical industries. Manufacturers across Germany, France, Italy, the United Kingdom, and Spain continue modernizing production facilities to improve productivity while complying with strict quality management and environmental standards.

Industrial buyers frequently prioritize long equipment lifecycles, standardized manufacturing processes, and comprehensive traceability. AI quality inspection supports these objectives by generating digital inspection records, improving production consistency, and reducing process variation. European manufacturers also place considerable emphasis on energy-efficient industrial equipment, responsible AI implementation, and cybersecurity compliance, influencing supplier product development and procurement decisions. Investment activity remains concentrated among high-value manufacturing sectors where inspection accuracy directly affects operational performance and export competitiveness.

Asia Pacific

Asia Pacific represents the largest commercial opportunity for AI quality inspection due to its extensive manufacturing base and continued investment in industrial automation. China, Japan, South Korea, Taiwan, India, Singapore, and Australia collectively account for substantial production capacity across electronics, semiconductors, automotive manufacturing, consumer goods, industrial equipment, and precision engineering.

Electronics and semiconductor manufacturing creates particularly strong demand for high-speed automated inspection because microscopic production defects can result in substantial financial losses and reduced product reliability. Automotive manufacturers throughout the region are expanding automated production lines while integrating AI-enabled quality control to improve manufacturing consistency. Governments across several Asia Pacific economies continue supporting advanced manufacturing initiatives, semiconductor investments, and smart factory development, encouraging adoption of intelligent inspection technologies.

Despite favorable demand conditions, manufacturers face challenges associated with integration complexity, workforce development, and varying levels of digital maturity across production facilities. Suppliers increasingly respond by offering modular software architectures, localized technical support, and scalable deployment models suitable for both multinational manufacturers and regional industrial enterprises.

Middle East & Africa and South America

The Middle East & Africa and South America currently represent emerging adoption markets where industrial modernization, manufacturing diversification, and infrastructure investment are gradually expanding opportunities for AI quality inspection.

In the Middle East, governments are encouraging industrial diversification through investments in advanced manufacturing, pharmaceuticals, food processing, and aerospace industries. Modern production facilities increasingly incorporate automated inspection systems as part of broader factory digitalization programs. Israel also contributes through technological innovation and industrial AI development, supporting regional adoption of advanced inspection technologies.

South America experiences demand primarily from automotive manufacturing, food processing, mining equipment production, packaging, and consumer goods industries. Brazil and Argentina remain the principal manufacturing centers where companies seek improved production efficiency and reduced operational waste. Nevertheless, capital investment constraints, currency volatility, and uneven industrial automation levels continue to moderate adoption compared with more mature manufacturing regions. Vendors often compete by offering cost-effective implementation strategies, regional service capabilities, and flexible financing arrangements that reduce barriers to investment.

Competitive Landscape

The AI Quality Inspection Market exhibits a moderately concentrated competitive structure in which established industrial automation companies, machine vision specialists, AI software developers, and precision measurement technology providers compete across integrated hardware, software, and service offerings. Competition extends beyond camera performance or inspection hardware specifications, with suppliers increasingly differentiating through software intelligence, deployment flexibility, industrial interoperability, and long-term lifecycle support.

Companies including Cognex Corporation, Keyence Corporation, Intel Corporation, Landing AI, NEC Corporation, Robert Bosch GmbH, Mitutoyo Corporation, Wenglor Deevio GmbH, Pleora Technologies Inc., IBM Corporation, Siemens AG, ABB Ltd., Solomon Technology Corporation, and Teledyne Technologies Incorporated compete by addressing different segments of the industrial quality inspection value chain. Some vendors emphasize complete end-to-end inspection platforms combining imaging hardware, AI software, industrial controllers, and analytics, while others specialize in software development, industrial computing, machine vision components, or precision measurement technologies that integrate into larger automation ecosystems.

Product differentiation increasingly depends on inspection intelligence rather than hardware specifications alone. Suppliers invest in deep learning algorithms capable of detecting complex manufacturing defects, reducing false rejection rates, accelerating model training, and supporting inspection across changing product configurations. Explainable AI capabilities, automated model optimization, synthetic training data generation, and simplified user interfaces have become important competitive attributes because manufacturers seek inspection systems that can be deployed without extensive data science expertise.

Strategic partnerships continue to influence competitive positioning. Collaboration among industrial automation providers, robotics manufacturers, semiconductor companies, cloud computing providers, and system integrators enables suppliers to deliver interoperable inspection platforms compatible with existing manufacturing infrastructure. Integration with manufacturing execution systems, enterprise resource planning software, programmable logic controllers, industrial robots, and industrial IoT platforms has become a significant purchasing criterion for multinational manufacturers seeking standardized operations across multiple production facilities.

Geographic expansion remains another important competitive strategy. Suppliers continue strengthening regional engineering teams, technical support networks, application development centers, and partner ecosystems to address growing demand across Asia Pacific and emerging industrial markets. Local implementation expertise, post-installation services, and customer training programs increasingly influence purchasing decisions because successful AI inspection deployment depends on long-term operational support rather than initial equipment installation alone.

Recurring software revenue is becoming more important within competitive strategies. Many suppliers now offer subscription-based AI software, cloud-enabled model management, remote diagnostics, software updates, and predictive maintenance services that complement equipment sales. This approach strengthens customer retention while providing manufacturers with continuous improvements in inspection accuracy and functionality throughout the operational life of deployed systems.

Recent Developments

June 2025: Cognex Corporation announced OneVision, a cloud-based platform for building, training, deploying, and scaling AI-powered machine vision applications across manufacturing sites. Commercial relevance: The platform simplifies AI model lifecycle management and supports enterprise-wide deployment of standardized quality inspection workflows.

April 2026: Siemens AG expanded its Industrial Edge ecosystem by making its Industrial AI Suite generally available and introducing new machine vision and quality inspection partner solutions. Commercial relevance: The release improves scalable deployment of AI-based visual inspection, enhances secure edge processing, and strengthens IT/OT integration for industrial manufacturers.

February 2026: Siemens AG acquired Canopus AI, a specialist in AI-driven computational metrology for semiconductor manufacturing. Commercial relevance: The acquisition expands Siemens' semiconductor inspection capabilities by strengthening AI-enabled wafer and mask metrology, addressing the industry's demand for higher manufacturing precision.

Regulatory and Policy Environment

The regulatory framework governing AI quality inspection extends beyond artificial intelligence itself and is primarily shaped by manufacturing quality standards, product safety regulations, industrial cybersecurity requirements, and sector-specific compliance obligations. Consequently, purchasing decisions are frequently influenced by the ability of inspection platforms to generate reliable inspection records, maintain traceable production histories, and integrate with enterprise quality management systems.

Automotive manufacturers widely implement quality management systems aligned with IATF 16949, which requires structured process control, defect prevention, and continuous quality improvement. AI-enabled inspection platforms support these objectives by providing repeatable inspection results, automated defect documentation, and statistical process monitoring that strengthen manufacturing consistency during supplier qualification and production audits.

Medical device and pharmaceutical manufacturers operate under comprehensive regulatory requirements, including the U.S. Food and Drug Administration (FDA) Quality System Regulation (21 CFR Part 820) and internationally recognized quality management standards such as ISO 13485. AI inspection systems assist manufacturers by automating verification of product dimensions, packaging integrity, labeling accuracy, and production documentation while improving inspection repeatability and supporting electronic quality records.

Food and beverage manufacturers increasingly adopt AI-powered inspection to comply with food safety regulations, including requirements established under the U.S. Food Safety Modernization Act (FSMA) and comparable regulatory frameworks in Europe and Asia. Automated visual inspection improves detection of packaging defects, labeling inconsistencies, contamination risks, and foreign materials while strengthening product traceability throughout processing and distribution.

Industrial cybersecurity has become an important procurement consideration as inspection platforms connect with factory networks, cloud infrastructure, and industrial control systems. Manufacturers increasingly require compliance with internationally recognized cybersecurity standards such as IEC 62443, particularly when inspection systems form part of critical manufacturing infrastructure. Vendors are therefore expanding secure edge computing, encrypted communications, user authentication, and software lifecycle management capabilities to address enterprise cybersecurity policies.

Governments also continue supporting advanced manufacturing through public investment programs that encourage factory modernization, industrial automation, semiconductor production, and artificial intelligence adoption. Initiatives supporting smart manufacturing across North America, Europe, and Asia Pacific indirectly stimulate demand for AI quality inspection because automated quality control has become an integral component of digitally connected production environments. Financial incentives for industrial modernization, combined with continued investment in semiconductor fabrication, electric vehicle manufacturing, and advanced electronics production, are expected to strengthen long-term deployment opportunities.

Outlook and Strategic Implications

Between 2026 and 2031, investment in AI quality inspection is expected to shift from isolated inspection workstations toward enterprise-scale quality intelligence platforms that connect production equipment, industrial software, robotics, and supply chain operations. Manufacturers are increasingly viewing inspection data as a strategic operational asset capable of improving production planning, reducing warranty exposure, strengthening supplier management, and supporting continuous process optimization.

Procurement priorities are expected to favor solutions that combine deployment flexibility with measurable operational performance. Buyers will increasingly evaluate software scalability, interoperability with manufacturing execution systems and enterprise resource planning platforms, cybersecurity architecture, and lifecycle software support alongside inspection accuracy. Vendors capable of delivering standardized inspection across multiple factories with centralized AI model management are likely to secure larger enterprise contracts.

Edge AI will continue gaining commercial importance because manufacturers require immediate inspection decisions without introducing network latency or exposing sensitive production data to external cloud environments. Improvements in industrial processors, embedded AI accelerators, and optimized inference software will enable increasingly sophisticated visual inspection directly on production equipment. This trend is particularly relevant for high-speed manufacturing sectors such as semiconductor fabrication, automotive assembly, electronics manufacturing, and pharmaceutical packaging.

Demand for explainable artificial intelligence is also expected to increase as manufacturers seek greater confidence in automated inspection decisions. Production engineers and quality managers require transparent defect classifications that facilitate root-cause analysis, regulatory compliance, and process validation. Suppliers investing in explainable AI, automated model validation, and simplified retraining capabilities will be better positioned to support regulated industries where inspection consistency is as important as detection accuracy.

Competitive strategies are likely to evolve toward integrated industrial ecosystems rather than standalone inspection products. Collaboration among machine vision providers, industrial automation companies, robotics manufacturers, semiconductor firms, and enterprise software vendors will continue expanding interoperable quality management solutions. Recurring software subscriptions, remote diagnostics, AI model management services, and predictive quality analytics are expected to represent an increasing share of supplier revenues, complementing traditional equipment sales.

Several commercial risks will continue influencing market expansion. Implementation complexity, shortages of skilled industrial AI professionals, cybersecurity concerns, and the availability of representative production datasets may slow adoption among smaller manufacturers. Organizations will also face ongoing challenges in integrating AI inspection into legacy production environments while maintaining uninterrupted manufacturing operations. Vendors that simplify deployment, provide comprehensive technical support, and reduce implementation risk through modular architectures will be better positioned to broaden adoption across diverse industrial sectors.

Overall, the AI Quality Inspection Market is expected to become increasingly embedded within digital manufacturing strategies during the forecast period. As manufacturers continue pursuing higher production efficiency, improved product consistency, stronger regulatory compliance, and greater operational resilience, AI-enabled inspection will transition from a quality assurance tool to a core element of enterprise manufacturing intelligence.

AI Quality Inspection Market Scope

| Report Metric | Details |

|---|---|

| Total Market Size in 2026 | USD 6,800.84 million |

| Total Market Size in 2031 | USD 13,970.73 million |

| Forecast Unit | Million |

| Growth Rate | 15.49% |

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Segmentation | Technology, Component, Application, Industry, Geography |

| Geographical Segmentation | North America, South America, Europe, Middle East and Africa, Asia Pacific |

| Companies |

|

Market Segmentation

By Technology

By Component

By Application

By Industry

By Geography

Table of Contents

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

2.1. Market Overview

2.2. Market Definition

2.3. Scope of the Study

2.4. Market Segmentation

3. BUSINESS LANDSCAPE

3.1. Market Drivers

3.2. Market Restraints

3.3. Market Opportunities

3.4. Porter’s Five Forces Analysis

3.4.1. Bargaining Power of Suppliers

3.4.2. Bargaining Power of Buyers

3.4.3. Threat of New Entrants

3.4.4. Threat of Substitutes

3.4.5. Competitive Rivalry in the Industry

3.5. Industry Value Chain Analysis

3.6. Policies and Regulations

3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. AI QUALITY INSPECTION MARKET BY TECHNOLOGY

5.1. Introduction

5.2. Computer Vision

5.3. Machine Learning (ML)

5.4. Deep Learning

5.5. Edge AI

5.6. 3D Vision Systems

5.7. Others

6. AI QUALITY INSPECTION MARKET BY COMPONENT

6.1. Introduction

6.2. Hardware

6.3. Software

6.4. Services

7. AI QUALITY INSPECTION MARKET BY APPLICATION

7.1. Introduction

7.2. Defect Detection

7.3. Dimensional Measurement

7.4. Surface Inspection

7.5. Assembly Verification

7.6. Packaging Inspection

7.7. Others

8. AI QUALITY INSPECTION MARKET BY INDUSTRY

8.1. Introduction

8.2. Automotive

8.3. Electronics and Semiconductor

8.4. Manufacturing

8.5. Healthcare and Pharmaceuticals

8.6. Food and Beverage

8.7. Aerospace and Defense

8.8. Textiles

8.9. Others

9. AI QUALITY INSPECTION MARKET BY GEOGRAPHY

9.1. Introduction

9.2. North America

9.2.1. United States

9.2.2. Canada

9.2.3. Mexico

9.3. South America

9.3.1. Brazil

9.3.2. Argentina

9.3.3. Others

9.4. Europe

9.4.1. United Kingdom

9.4.2. Germany

9.4.3. France

9.4.4. Italy

9.4.5. Spain

9.4.6. Others

9.5. Middle East and Africa

9.5.1. Saudi Arabia

9.5.2. UAE

9.5.3. Israel

9.5.4. Others

9.6. Asia Pacific

9.6.1. Japan

9.6.2. China

9.6.3. India

9.6.4. South Korea

9.6.5. Singapore

9.6.6. Australia

9.6.7. Taiwan

9.6.8. Others

10. COMPETITIVE ENVIRONMENT AND ANALYSIS

10.1. Major Players and Strategy Analysis

10.2. Market Share Analysis

10.3. Emerging Players and Market Attractiveness Analysis

10.4. Mergers, Acquisitions, Agreements, and Collaborations

10.5. Competitive Dashboard

11. COMPANY PROFILES

11.1. Cognex Corporation

11.2. Keyence Corporation

11.3. Intel Corporation

11.4. Landing AI

11.5. NEC Corporation

11.6. Robert Bosch GmbH

11.7. Mitutoyo Corporation

11.8. Wenglor Deevio GmbH

11.9. Pleora Technologies Inc.

11.10. IBM Corporation

11.11. Siemens AG

11.12. ABB Ltd.

11.13. Solomon Technology Corporation

11.14. Teledyne Technologies Incorporated

12. APPENDIX

12.1. Currency

12.2. Assumptions

12.3. Base and Forecast Years Timeline

12.4. Key Benefits to the Stakeholders

12.5. Research Methodology

12.6. Abbreviations

Navigate

Trusted by the world's leading organizations